This is certainly a TGIF week. A massive 41% of our LionTree Universe (89 companies) reported this week, so it was earnings prints left and right! The heavy flow, especially on Thursday night, made for a challenging end of the week, but we did our best to cover as many key companies as we were able.

The market reaction to earnings in the sector skewed negative as just 44% of companies traded up, while 56% traded down. Of the broader 90% of S&P 500 companies that have reported, per Factset, the blended earnings growth rate was +11.7%, which is an improvement to where we stood last week and well above +4.9% expected at the beginning of the quarter.

The major indices had a strong week with the S&P 500 rallying +2.4% and Nasdaq rising +3.9%.

We focused on the below themes this week:

- Earnings Scorecard – Week 4

- Disney Continues Its Strategic Balancing Act

- Investors Are Awaiting More Details On WBD’s Act II

- Fox Finished FY25 Strongly… Though Has Tough Cyclical Comps In FY26

- Snap & Pinterest: Investors Had Hoped For More

- The Coming Inflection For TTWO Is Tracking On Plan

- Warner Music Group Is Finding Its Rhythm Again

- DraftKings: Sports Betting Outcomes Swing Back To The Sportsbook Just In Time For A Seasonally Strong Fall

- TKO Remains At The Center Of Premium Content & Live Events

- Uber’s “Barbell” Strategy Is Yielding Results

- DoorDash/Instacart – Delivery Keeps Delivering

Given the length of our Update this week, you may want to consider downloading the PDF 😊

Lastly, I would like to highlight that LionTree proudly served as financial advisor to Paramount Global on its merger with Skydance Media, which officially closed this week.

Have a nice weekend.

Best,

Leslie

Earnings Scorecard – Week 4

It was an absolute avalanche of earnings this week, with a massive 89 companies in our LionTree Universe reporting their second quarter earnings (an all-time record!). Similar to last week, stock price reactions skewed negative, with 49 companies (55%) trading down post their report and 40 companies (45%) trading up. The Trade Desk was the worst performer, plunging -39% in reaction, while Lemonade was the best performer, up +30%.

Earnings reports were across a multitude of sectors this week. Starting off with Media, it was a bit of a tougher week for the group, with Warner Bros. Discovery falling -7% (see Theme #3), Fox down -4% (see Theme #4), and Disney losing -3% (see Theme #2). Also in media but on the music label side, Warner Music Group report its results and the stock traded up +4% (see Theme #7). That said, Take-Two also had a bit of a tough going, falling -4% in reaction to its print (see Theme #6).

Shifting over to digital advertising, Snap and Pinterest both saw a less-than-favorable reaction from the Street, down -17% and -10%, respectively (see Theme #5).

The major last-mile names also published their reports, with Uber and Lyft down -0.2% and up +2%, respectively (see Theme #10), while Instacart and DoorDash traded up +4% and +5%, respectively (see Theme #11).

Finally, to round out the week, DraftKings fell -0.4% after its print (see Theme #8), while TKO was up +3% (see Theme #9).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Disney Continues Its Strategic Balancing Act

Disney has been pushing hard to position the business to thrive no matter where consumers choose to watch content. They view themselves as being in the “TV business” rather than in the distinct linear or streaming businesses. That said, it doesn’t mean that the shift to streaming is not occurring, nor that it will be a smooth transition. In FQ3, the Co made a lot of progress with DTC profitability (op income increased $346mn y/y and beat Street expectations) and mgmt. raised the FY25 DTC operating income guidance, but core Disney+ domestic subscriber adds and ARPU fell below projections. In the coming quarter though, Disney will stop reporting subscriber adds and ARPU, following in Netflix’s footsteps. Also looking ahead, a unified Disney+ and Hulu streaming app experience will be an important catalyst for growth when it is made available to consumers “next year.” Turning to the Linear business, it performed worse than expected and Content Sales/Licensing & Other op income fell -$100mn short of expectations due to tough comps and this overhang will continue into next qtr.

What was smooth sailing though was FQ3 performance in the Experiences division, where revenue and profitability trends surpassed Street expectations. Importantly, consumers continued to flock to the Co’s domestic theme parks and in particular Walt Disney World despite increased competition in Orlando (ie, Comcast’s opening of Epic). All in all, Disney raised FY25 Experiences op income guidance. There are high hopes as well for the Disney Adventure Singapore cruise ship as we look ahead.

In Sports, the Co has been VERY busy, finally confirming an ESPN deal with the NFL, expanding its array of sports programming while the NFL takes a 10% stake in ESPN. The Co also set a date for the launch of its ESPN DTC streaming offer (Aug 21st – the same day as FOX One). Last, but not least, Disney’s film slate remains strong, with recent hits like Lilo & Stitch and Fantastic Four: First Steps and a pipeline featuring Zootopia 2, Avatar: Fire and Ash, and Toy Story 5.

To close it out, Disney raised its FY25 adj EPS guidance by 10c but investors pushed back as this quarter’s beat was by 15c. Is this another case of conservatism?

-> Disney shares traded down -2.7% in reaction to results and dragged down other media conglomerates on the day (FOX down -1.3% and Paramount Global fell -6% though Warner Bros Discovery was flattish); YTD, FOX is still leading performance wise

Disney’s FQ3 EPS Beat Was Below The Line, While Core Headline Results Were ~In-Line…Mgmt Raised FY25 EPS Guidance But By Less Than The Qtrly Beat

- Total FQ3 revs were a tad light while op income was a tad better

- Experiences – Beat: Upside was a key standout

- Linear- Missed: Underperformed on both the top line & profitability

- DTC – Mixed: Better profitability was of note but revs were weaker than expected

- CSLO – Mixed: While revs beat, op income fell -$100mn short of expectations

- Sports- Mixed: Slightly lower revs, but slightly higher op income

- Note that the India JV impact was a ~$50mn loss in FQ3 & expect ~$20mn loss In FQ4

- FY loss expected at ~$200mn

- OUTLOOK – Raised FY25 adj EPS by 10c…from ~$5.75 to ~$5.85 (vs cons $5.75) BUT it raised the question regarding why not more since the Co beat FQ3 by 15c

- Implies that FQ4 adj EPS consensus Street estimates come down 5c

Overall Segment Growth Snapshot & FY25 Segment Outlook

- Entertainment – FQ3 headline performance & outlook

- Revs rose +1% y/y

- Op income fell -15% y/y given lower results at Content Sales/Licensing, Other and Linear Networks offset by DTC

- Maintained FY25 guidance – Expect DD operating income growth

- Expect difficult theatrical comparisons to continue into in FQ4: CSL&O operating income guided to decline ~$400mn y/y in FQ4 (vs a decline of -$275mn y/y in FQ3)

- Sports – FQ3 headline performance & outlook

- Revs fell -5% y/y

- Ad rev at Domestic ESPN was up +3% y/y in Q3 due to rate increases; Incls 1ppt adverse impact due to comparability

- Op income grew +29% y/y, w/ a -7% decrease at domestic ESPN due to higher programming and production costs reflecting contractual rate increases for the NBA and college sports

- Raised FY25 guidance – expect +18% y/y increase in operating income (incls a $636mn loss at Star India in fiscal 2024)

- Revs fell -5% y/y

- Experiences – FQ3 headline performance & outlook

- Revs rose +8% y/y

- Op income grew +13% y/y (from +9% y/y in FQ2)

- Drivers: An increase in guest spend at theme parks and incr’d costs due to new guest offerings, including the new fleet expansion; Also benefitted from ~$40mn benefit of Easter timing

- Raised FY25 guidance – Expect +8% y/y increase, vs the prior guide of “higher end” of 6-8%

- Results include ~$30mn of pre-opening expenses: Driven primarily by Disney Destiny & Disney Adventure

- Expected FY 2025 pre-opening expenses for Disney Cruise Line are ~$185mn, with $50mn in FQ4

Mixed FQ3 Subscriber Performance (International Beat/Domestic Missed)…But Mgmt Raised DTC FY25 Profitability Guidance

- FQ3 DTC revs grew + 6% y/y…incls 3ppts headwind from D+ Hotstar being included in FQ324’s

- Overall D+ core was marginally ahead of expectations on both subscribers & ARPU w/ intl the driver

- Domestic: Subs were flat seq and ARPU missed cons by -0.6%

- Internationally: Added 1.7mn subs and ARPU beat cons by 1.7%

- FQ4 subs outlook

- Expect D+ & Hulu subscriptions to increase by more than 10mn vs FQ3

- W/ the majority of the increase from Hulu due to expanded Charter deal

- Expect a modest increase in D+ subscribers

- Expect D+ & Hulu subscriptions to increase by more than 10mn vs FQ3

- **NOTE**…following in Netflix’s footsteps, Disney will no longer share subscriber numbers nor ARPU

- This will be as of FQ1:26 for Disney+ and Hulu (and FQ4:25 for ESPN+)

- It will instead focus on Entertainment DTC profitability in its financial disclosures

- FQ3 DTC op income was much stronger than expected at $346mn vs cons $206mn (and up from $365mn y/y)

- Margins reached 5.6%…and the goal is to improve DTC op income margins beyond the targeted 10% through higher engagement in US and deeper penetration internationally rather than cost-cutting

- And raised FY 2025 DTC op income guidance from $875mn to ~$1.3bn

- Expect international DTC content spend to increase while domestic spend remains the same

- Domestic: “You shouldn’t expect that we need to increase the spend on content significantly”

- Intl: “Where we believe we should be investing is to grow our international businesses”

A Unified Disney+ & Hulu Streaming App Experience Will Be Available To Consumers “Next Year”

- Disney annc’d that it is fully integrating Hulu into D+

- It consolidates the “highest caliber” brands and franchises, general entertainment, family programming, news and live sports into one app

- Internationally, Hulu will replace the Star tile on D+

- Expect improvements to D+ app in the “coming months”

- The unified Disney+ and Hulu streaming app experience will be available to consumers next year

Disney ESPN’s NFL Deal Is Expected To Be “Accretive”

- Also annc’d was that ESPN will acquire the NFL Network and other media assets owned from the NFL in exchange for a 10% equity stake in ESPN

- ESPN also expanded its NFL partnership: It will now receive more games, enhanced fan engagement and broader streaming rights

- Key terms:

- These are both non-binding agreements

- ESPN will own & operate the NFL Network: Integrating it into ESPNs DTC while continuing traditional pay TV

- ESPN will gain broad rights to the RedZone: Distributing the RedZone Channel to Pay TV operators

- NFL Fantasy Football will merge w/ ESPN Fantasy Football

- ESPN will license 3 addtl NFL games per season to air on NFL Network

- Also, ESPN will adjust its overall NFL game schedule: 4 games will shift to the NFL Network (which will continue to present seven games per season)

- ESPN will also gain the ability to sell and bundle NFL+ Premium to its ESPN DTC subs, along with rights to addtl non-exclusive preseason NFL games for its DTC offering

- Both starting in the 2025 season

- ESPN will have addtl NFL highlights: And enables more features like betting & fantasy

- ESPN gains expanded draft rights: ESPN will have NFL Draft streaming rights across ESPN DTC, HULU and Disney+

- Gives ESPN a record 28 NFL game windows (up from the previous 22)

- The NFL will retain ownership of its other media businesses: Including NFL Films, NFL+, NFL.com and the digital distribution of the NFL RedZone

- The deal will be “accretive” in the first year that it closes: “Even with this exchange of assets, and the fact that the NFL, obviously, will be paid a dividend from ESPN’s earnings, it will be accretive in the first year after it closes, and I think that’s significant”…“It will be about $0.05 accretive before purchase accounting”

- Timing: lt “likely won’t close until the end of next calendar year”

- “This is one of the most important steps ESPN has taken”

- Other sports related news

- ESPN will be the exclusive home for WWE Premium Live Events

- See Theme #9 for more details disclosed by TKO

- ESPN will be the exclusive home for WWE Premium Live Events

The ESPN DTC Launch Is Officially Slated For Aug 21st

- ESPN DTC launch is Aug 21st – The full suite of networks and series will be made directly to fans

- Will have an enhanced ESPN app at launch

- Multiview

- Enhanced personalization

- Stats integration

- Betting

- Fantasy sports and commerce

- Personalized SportsCenter

- Pricing:

- Unlimited package = $29.99/mo

- A Select option package = $11.99/mo

- Promo: Special offer at launch for $29.99/mo for the first 12 mos for subs who bundle ESPN unlimited plan w/ Disney+ and Hulu

- Go to market: Will meet subscribers where they want to be reached…ie, both linearly and digitally, but digital will be a more fulsome experience.

- Will have an enhanced ESPN app at launch

- Could there be an oppty to bundle other companies’ sports offering as well? Yes…the more sports that can be offered and make it easier for users to find sports the better

Experiences Business Is Operating On All Cylinders…& Mgmt Raised The FY25 Segment Op Income Guidance

- Experiences segment results reflect:

- Higher guest spending at theme parks

- More passenger cruise days due to the launch of the Disney Treasure

- Higher occupied room nights

- Partially offset by higher costs reflecting new guest offerings, including the expansion of the Disney Cruise Line fleet

- “Encouraged by the continued resiliency of our domestic parks business, particularly at Walt Disney World given increased competition in the Orlando market”

- Accelerating performance at Domestic Parks & Experiences

- Domestic Parks & Experiences revenue rose +10% y/y up from +9% y/y in FQ2

- Domestic Parks & Experiences op income grew +22% y/y, up from +13% y/y last qtr

- Domestic Park margins were up +260bp y/y

- Per cap domestic spend growth was up a strongly but attendance was strong as well

- Mgmt didn’t provide much color on the drivers but said that there was not a material change in visitor mix (local vs non-local) which can affect per caps

- “We feel good about the per caps” but “also feel good about the attendance”, especially given competition in the market

- The aim is to growth attendance and per cap in a “balanced way”

- International Parks & Experience

- International Parks & Experiences revs grew +6% y/y

- International Parks & Experiences op income fell -3% y/y

- RAISED guidance – Given the FQ3 Experiences op income beats to date, the Co incr’d segment FY25 op income growth from the “higher end” of 6-8% to ~8% y/y (note the segment has growth +7% YTD)…drivers include

- Parks:

- WDW had a “record” FQ3

- Disneyland Paris is expected to do well (easier comps but biz is also performing well)

- But China is challenged with per cap spend

- Cruise ships

- Are doing very well

- Forward bookings “look great”

- Running at high occupancy

- Experiences bookings for FQ4 are up 6% right now…”So, we certainly feel positively about that as well”

- Parks:

- Very bullish on the new Disney Adventure ship launching in Singapore…it is the largest ship ever (7k passengers) & will extend Disney’s brand into the region

- Initial sales were extremely robust…trips sold out very quickly in the first 2 qtrs of operations

- View this as a huge opportunity in Asia

- What underpins the growth of the Cruise business? The fleet is set to double over the coming years

- The Co sees strong repeat visitation: With existing customers being first to book on new ships

- There is also geographic expansion: Into areas they have not visited which expands the reach

- Visibility is strong: Already “half booked out for all of next year, and the newer ships are even higher in that regard”

- “So, we feel terrific from the perspective of consumer receptivity to our new offerings”

- Have a long list of theme park expansions and new cruise ships in the works looking ahead which includes…

- A new World of Frozen land opening at Disneyland Paris in 2026

- Villains and Cars themed areas coming to Magic Kingdom

- A Monsters, Inc. area coming to Disney’s Hollywood Studios

- An Avatar-themed destination coming to Disney California Adventure

- And have a new theme park coming to Abu Dhabi

- Preparing to launch two new ships (brings fleet to 8)

- In November, we will launch the Disney Destiny, followed by the Disney Adventure, largest cruise ship ever and the first to have its homeport in Asia.

- The Disney Treasure, launched last year, has gotten off to a strong start and continues to perform well.

There Is Also A Strong Film Slate Looking Ahead

- Recent successes

- Lilo & Stitch crossed $1bn WW box office recently

- It is the 2nd largest license merchandise franchise this year w/ 70% y/y growth and has been deployed across parks and experiences

- Fantastic Four: First Steps had a strong opening 2 weeks ago

- Lilo & Stitch crossed $1bn WW box office recently

- Disney has a compelling pipeline over the next year+:

- This year: Zootopia 2 and Avatar: Fire and Ash

- Highlighted next year: Star Wars: The Mandalorian and Grogu, Toy Story 5, a live action Moana, Avengers: Doomsday

- Mgmt stressed that the Co is focused on both new IP and leverageing popular older IP: They “don’t have a priority one way or another”

Investors Are Awaiting More Details On WBD’s Act II

Back in June, WBD announced plans to split into two separate companies – Warner Bros., which will house the streaming and studios businesses, and Discovery Global Media, which will operate the linear networks. The move came close to three yrs after WarnerMedia and Discovery merged in 2022 to create what is now Warner Bros. Discovery. Investors still have many questions about the future given all the moving pieces at WBD at present, hence there were no shortage of updates this quarter.

Looking at performance, WBD delivered a strong Q2 with beats across all segments on both revenue and profitability. The Studios business was a highlight generating $2bn+ in global box office YTD. Mgmt credited the turnaround to the rebuilding efforts of the past three yrs, saying, “we were in last place… together we went from last to first.” Streaming profitability was another key highlight, though a restructuring of an HBO Max US distribution deal, which will have a “more pronounced” impact on domestic ARPU and distribution revenues in H2, caught some investors by surprise. Another short-term headwind is the Co’s decision over the past three yrs to license less content in order to keep it for HBO Max, but mgmt is confident on this strategy, believing it will build the platform’s value and pave the way for price increases in the coming yrs. In the meantime, the Co is going crack down on account sharing, with benefits expected to begin in Q4 and ramp meaningfully in 2026.

In addition to the above, the Co provided interesting commentary on ad trends, sports rights strategy, theatrical release momentum, and more. There is a lot in motion at WBD, and investors will certainly be looking for more clarity on the split to assess the future strategic direction.

See below.

-> WBD stock fell -7.3% in reaction to earnings and is now up +3.2% YTD (vs DIS up +1.0%, PARA +5.5%, and FOX +7.5% YTD)

WBD Posted Strong Q2 Results With Beats On Revenue & Adj. EBITDA Across All Segments

- Q2 consolidated revs beat by +0.4% and adj. EBITDA beat by +10.3%

- All segments beat

- Though FCF came in at $702mn, well below cons $863mn

- Paid ~$250mn in separation-related costs in Q2, primarily accrued interest, which impacted Q2 FCF

Some Addtl Color On Upcoming Separation Into Warner Bros (Streaming & Studios) & Discovery Global Media (Global Networks)

- Leadership teams are “largely in place”

- Timeline – “remain focused” on delivering 2025 goals and executing separation plans so that both organizations “hit the ground running” once split, which mgmt continues to expect to occur in mid-2026

- Expect to incur one-time transaction and restructuring costs that will impact FCF through the closing of the separation

- Will be quantified once key operating model and separation decisions are finalized

- “Believe that there are very significant pockets of growth and opportunity, and we’ll work really hard over the next half year here to identify those and get in position to deliver what I think is going to be a business with much more longevity than what the market sees right now”

Streaming Outperformance In Subscribers And Monetization Is Being Driven By Intl / Domestic Streaming ARPU Will Continue To Be Challenged In The Near-Term

- Added 3.4mn+ subscribers in Q2, including 3.2mn+ intl subscribers (total subs beat was driven by intl coming in +3.5% ahead, as domestic missed by -3.3%)

- Growth was driven partly by the “very successful” launch of HBO Max in Australia at the end of Q1, with “healthy” retail traction, in addition to the launch of HBO Max’s wholesale partnership with Foxtel

- Saw “some really positive improvements” in churn from March to June “but we’re not satisfied with where we are”

- Will continue to work on reducing churn through bundling, driving engagement more consistency in content slate and better personalization features on the product itself

- Saw a “modest” negative impact on Q2 domestic ARPU and distribution revs in Q2, which is expected to be “more pronounced” in H2:25: Due to the restructuring of a HBO Max US distribution deal w/ “a former related party” in Q2

- Distribution rev growth expected to be in the LSD range starting in Q3

- Impact will linger into H1:26, but expect to see a re-acceleration in global distribution rev in H1:26, in part helped by the Q1 launch of HBO Max in Germany and Italy, and in the United Kingdom and Ireland in Q2

- US growth will reaccelerate starting in H2:26 as they lap that reset

- Reiterated 2025 streaming adj EBITDA guidance of “at least” $1.3bn…: Driven by “healthy” subscriber-related rev growth

- …and to “surpass” 150mn streaming subs by end of 2026

- Q2 content highlights –

- S1 of The Pitt, “one of the most successful debut shows of 2025

- S3 of The White Lotus, which delivered 26mn+ avg viewers per episode (up ~40% vs S2)

- Return of The Last of Us (“one of the most widely viewed shows” of Q2 “across all platforms), And Just Like That…, Hacks, The Gilded Age, and The Righteous Gemstones

- Intl content also continues to attract and engage more subscribers in Q2, including “recent successes” like –

- Turkey – S3 of The Prince, which was viewed by 74% of the country’s total HBO Max subscribers

- Mexico – Chespirito: Not Really on Purpose, which was viewed by 60% of the country’s HBO Max subscribers and ranks as the most acquisitive and most watched intl series ever on HBO Max

- “Symbiotic” relationship w/ Warner Bros. Studios has been “one key driver of HBO Max’s success”

- In H1:25, content created by Warner Bros. Studios accounted for over half of global hrs streamed on HBO Max, with almost all of our global viewing accounts having watched a WB-produced title

- Strategy to reaccelerate ARPU? Will crack down on acct sharing before increasing prices

- “We want the market to accept the product, to recognize it as high quality” which in turn will “give us what we think is a very big upside over time to raise price…over the next couple of years”

- “Just in the first inning” on converting unauthorized account shares into paying customers and expect to see benefit starting in Q4 and then “kick off” in 2026

- Will turn on the more aggressive languaging vs the voluntary process that is in place right now

- Wholesale partnerships are driving strong LTV, activation, and upsell economics

- Have been increasingly partnering w/ distributors on product activation, and activation rates have been trending above expectations

- Upsell capabilities (ad-supported -> ad-free) have been “very healthy”

- Has led to better ARPU, particularly outside the US, where ad sales is still a growth biz and starts off a lower base

- Have benefit of an existing “embedded audience” internationally, in places like the UK, Germany, and Italy, HBO shows have been popular but aired on other platforms (like Sky)

- When HBO Max launches in those mkts, expect high engagement and retail sign-ups from existing fans

- Already seeing that in Australia, where “launch was essentially dual-track” (retail and partnership w/ Foxtel) and has been a “great success story”

Prioritizing Long-Term Asset Value & HBO Max Differentiation Over Near-Term Licensing Rev

- Have sold “significantly less” content to streaming and traditional mkt over the past 3 yrs “in order to differentiate HBO Max” – “that’s working for us in terms of driving growth.”

- Has put some pressure on near-term financial results – “we have taken a short-term financial hit for some real value that’s going to flow through”

- Have put a “10-digit figure of value” of intercompany profits on the balance sheet that’s going to come back into the P&L “over the next few yrs” as the content gets utilized on WBD platforms

- “One company” strategy facilitated collaboration b/w HBO + Warner Bros Television has been a “net value and a net positive that will drive sustainable growth at HBO Max”

- “Innovated with The Pitt as a procedural that was very, very successful for us…they’re working together with J.K. Rowling on Harry Potter, which is extremely promising and is already in production”

- What will content licensing strategy look like post-split?

- On general entertainment strategy –

- “Reimagining” US networks portfolio “as a content engine around very strong, unscripted brands, and less of “just traditional linear networks”

- As a result, content licensing is going “to be a meaningful contribution going forward as we think about recovering our content investment”

- On sports strategy –

- “We will continue to be looking at investments with the same discipline that we have in the past”

- BUT “unlikely we will sublicense rights out… I don’t think there is a need to”

- …instead working on building a stand-alone product that can be DTC or bundled w/ HBO Max, Discovery+ and potentially 3Ps

- On general entertainment strategy –

- Other areas w/ “tremendous amount of untapped value” – theme parks, live events, and gaming

- “Have a lot of upside”: Three yrs ago, for every $1 Disney made from circulating its IP, WBD made 22c; Now it has increased to 30c, but still room to grow

- Harry Potter is an exception – “we’re extremely effective in monetizing that”: Through gaming and a “very mutually beneficial” deal w/ Universal and the Harry Potter parks they have

- Got back some DC rights they had given to Six Flags, which “we think can be very compelling”, particularly internationally: “A lot of those rights weren’t tied up at all outside the US, and we’re in different stages of deploying those assets”

- NOT going to build theme parks themselves but will pursue licensing and partial ownership deals: Already doing something like this in Abu Dhabi, “which is quite lucrative”

- Wizard of Oz will premieres at the Sphere on the 28th: “It’s very exciting. It’s very innovative”

Reinvesting Some Of The Cost Savings From NBA Exist Into Strategic Sports Rights

- There is going to be a benefit from the NBA coming out of WBD’s financials: “Looking at just advertising and content cost as a differential, the deal is loss-making”

- Q2 is “by far the biggest chunk” of both content costs and ad rev generations, followed by Q1; Q4 is the smallest qtr

- Have already reinvested some of those savings into other sports rights (i.e., college football playoffs)

- Expected savings –

- Can expect ~$100mn sports cost benefit in Q4

- Turning to 2026, expect a net benefit of “hundreds of million of dollars” from the rights cost coming up and some offsetting rev losses from an EBITDA perspective

- Expected savings –

- On overall live sports strategy – “we will continue to be strategic and disciplined in our pursuit of live sports rights that enhance the way we extend the reach of our content and drive engagement across all platforms – linear, streaming and digital”

Advertising Trends Have Remained Generally Steady / No Change Expected Post Co Separation

- Overall Q2 ad revs fell -10% y/y ex-FX (vs -8% y/y in Q1), as ad-lite streaming subscriber growth was more than offset by domestic linear audience declines

- “Nothing is going to change” from an advertiser perspective post separation

- “We’re going to continue to go to the market as business as usual”

- On the recent upfront – the “market has held up very well”

- “We’ve seen prices up across all categories, more so in sports than in general entertainment”

- “Strong pricing” and “resilient demand” for sports programming

- “Firm pricing” for general entertainment which was “essentially consistent with recent trends”

- “On the digital side, there is some price pressure, but we’ve maintained a very strong price premium for the quality of inventory that we’re delivering”

- “Healthy” demand for HBO Max

- “We’ve seen prices up across all categories, more so in sports than in general entertainment”

- How have ad mkts been faring overall?

- US ad market environment “continues to remain steady with limited, if any, incremental impact from macro concerns”

- EMEA remains healthier, and continue to see pockets of growth in key mkts such as Poland and Italy

- LatAm (which is still a smaller mkt) continues to see both secular and cyclical headwinds

- Global Linear Networks ad revs in Q3 are expected to decline at a y/y higher rate than Q2’s -13% y/y ex-FX due to tough comps

- Given the lighter sports schedule, comp w/ last yr’s summer Olympics, and the benefit to CNN in the prior yr from US election coverage

- Will also not have the NBA in the US beginning in Q4, which will impact both ad revs and cost of revs

Studios Is Starting To See The Fruits Of Its Labor From Its “Deliberate Rebuilding” Over The Last Three Yrs

- Studios segment expected to generate “at least” $2.4bn of adj. EBITDA in 2025

- Reiterated plans of getting the Studios biz back to $3bn in EBITDA – “this represents a substantial step toward our goal”

- Released 4 films in Q2 which have generated $2bn+ in global box office to date

- A Minecraft Movie

- Sinners

- Final Destination: Bloodlines

- F1

- Momentum continues into Q3 w/ release of Superman, which “marked the beginning of a new era for DC Studios”

- Superman generated $220mn globally in its opening weekend, the strongest ever debut for a solo Superman film, and strongest DC Studios global opening since 2022

- Warner Bros. Studios has been setting records –

- Distributed five films in a row that opened to $45mn+ domestically, a first for any studio

- Has four of the top 10 global Hollywood movies YTD, more than any other studio

- What has been driving recent momentum? “A deliberate rebuilding and transformation strategy executed over the last three years”

- Implemented a more “bottoms-up, analytically rigorous greenlighting process,” which includes –

- More granular input from distribution and global marketing teams

- More systematic marketing and distribution checkpoints ahead of releases w/ an emphasis on the final eight weeks prior to release

- Utilizing real-time data to make better windowing decisions

- Reorganized marketing and distribution teams into a globally integrated model that has enabled them to seamlessly coordinate film releases across territories

- “We’ve had an extraordinary run. We were in last place…together we went from last to first”

- Implemented a more “bottoms-up, analytically rigorous greenlighting process,” which includes –

- Targeting 12-14 theatrical releases annually across their 4 labels –

- 1-2 Warner Bros. Pictures tentpoles (primarily utilizing well-known Warner Bros. IP)

- 1-2 DC Studios films

- 3-4 New Line Cinema releases (including horror)

- 1-2 WB Animation titles

- A select number of moderately budgeted original films

- 10-yr vision for DC Universe…building out DC franchise in a “precise and measured way” that will “increasingly overlay across the studio’s broad efforts”: From film and TV to consumer products, games, experiences and social

- Next installments of the DC super family are in works, including –

- Supergirl: Woman of Tomorrow (2026), Clayface (2026), and the next Wonder Woman

- The Batman II (2027) is preparing to begin shooting next spring, among several other projects in development

- Also includes “an exciting array” of TV projects, including –

- The Penguin, which garnered 24 Emmy nominations and was watched by ~20mn HBO Max subscribers

- Upcoming new season of Peacemaker

- Debut of Lanterns in 2026

- Next installments of the DC super family are in works, including –

- On the TV front…“SVOD funnel continues to grow” – expect to deliver a new record for scripted series sold into development for SVOD svs, surpassing 2024’s previous high watermark

Fox Finished FY25 Strongly… Though Has Tough Cyclical Comps In FY26

While Fox delivered a blow-out FQ4, following a much better than expected FQ3 as well, it turned into a sell the news event for the stock given the strong performance and that the Co is now entering a cyclically slower year. We thought the most incremental updates and learnings from the results included: 1) the ad market remained very “healthy” especially in Fox’s core news and sports areas and mgmt. is bullish on ad trends into FY26; 2) pay-tv subscriber losses remained steady at -7% y/y but FY26 will be a slower year for affiliate deal renewals (25% of the total); 3) Tubi engagement remains strong and profitability will improve “substantially” in H2 FY26; 4) Fox One will launch August 21st (same day as ESPN DTC) but aspirations remain modest; 5) digital investments will increase from ~$300mn in FY25 to ~$350mn in FY26; and 6) the World Cup will be a driver this fiscal year.

All in all, it was a very strong qtr which was deja vu as mentioned and while the Co is entering a cyclically slower year, the underlying trends in its News & Sports businesses remain on strong footing.

-> Fox share fell ~-4% in reaction to earnings but the stock is still up +7.5% YTD, which is still above WarnerBrosDiscovery’s +3.2% and Paramount Global’s +5.5%

FQ4 = Yet Again, Another Big Beat Qtr For Fox

- Similar to last qtr, the Co topped Street expectations across the board… the huge beat on adj EBITDA (by 28%) was a standout (w/ upside in both Cable Nets and TV) as was better than expected advertising performance

- The Co incr’d the buyback by $5bn to $12bn total authorization

Fox News Viewership Remained Sky High…Though FQ4 Was Seasonally Slower For Fox Sports

- Fox News saw strong total audience growth in FQ4…total day audience is up 25% in total viewers & +31% in demo and maintained 60%+ share of cable news audience in FQ4

- It was the “second most watched network in M-F Prime in all of television going above all but one network”

- “Fox News finished as the highest rated television network in America for the month of July”

- Fox News Digital also achieved new records for engagement during Q4

- 5bn+ YouTube views & 3.7bn+ views on social media

- Fox Sports calendar was lighter in FQ4 but its first airing of the Indianapolis 500 was an “unqualified success”, avg’ing 7mn+ viewers (+41% y/y), and was the most-watched running of the race in 17 yrs

Puts & Takes For Fiscal 2026…Digital Investments Return To FY24 Levels

- FY26 will be a light year for affiliate renewals: Only ~25% of total distribution revs are up for renewal

- There are moving parts cyclically

- Tough TV segment comps…mostly FQ1 & FQ2: Stations in H2 FY25 generated $270mn of political revs

- FQ3 Super Bowl will be “an ad revenue negative for us, but from an EBITDA perspective, it’s a bit of a push”

- Had a massive MLB in H1 FY25: Hope for a “blockbuster post-season again, but who knows?”

- FY26 investments in digital initiatives are likely to return to ~$350mn (vs ~$300mn in FY25 & inline w/ FY24 levels):

- Latam streaming & Fox One spend will be concentrated in H1

- Fox One spend will be on launch/marketing, not incremental content costs

- Tubi is expected to significantly improve profitability in H2

- Latam streaming & Fox One spend will be concentrated in H1

- The 2026 FIFA Men’s World Cup will span Q4 FY26 and Q1 FY27

- World Cup rights pmts hit in FY26 but related advertising receivables will be collected in FY27

Expect A Substantial Increase In Tubi Profitability In H2 FY26

- Tubi revenue rose +32% y/y in FQ4, slightly down from +35% y/y in FQ3

- Tubi’s profitability moderately improved in FY25 & it is expected to show more “substantial” improvement in H2 FY26

- Total view time grew +17% y/y in FQ4, down from +24% y/y in FQ3

- Two-thirds of Tubi users are outside the traditional cable bundle (ie, a hard to reach audience)

Subscriber Losses Remains Stable Though This Year Will Light On Affiliate Renewals

- Total affiliate revs grew +5% y/y vs FQ3 +3% y/y

- TV affiliate revs grew +3.6% y/y in line FQ3’s +4% y/y

- “This healthy growth in fees across both FOX-owned and affiliated stations more than offset the impact from industry subscriber declines.”

- Cable affiliate revs grew +1.9% y/y vs FQ3 +2.8%

- Pricing gains from affiliate renewals outpaced the impact from net subscriber declines of under 7%, which is stable vs last qtr

Remain Bullish On The Ad Market Into FY26

- Total advertising revenues grew +7% y/y vs +65% in FQ3

- Cable ad revs rose +15% y/y…Fox News engagement + “healthy” national and DR pricing

- TV ad revs rose +3% y/y…led by Tubi which more than offset tough comps

- Strong upfront – achieved “record-setting” double-digit volume growth & strong pricing growth across the portfolio

- FOX Sports had the “record breaking” up front

- Ex the impact of the Super Bowl, had over $2bn committed in the upfront

- Tubi saw a 35% volume increase w/ stable pricing which is important given the competitiveness in the CTV mkt

- Tubi accounted for ~25% of total committed revenue

- On entertainment, very healthy with double-digit increases in scatter pricing

- “Incredibly encouraged by the demand, the kind of incredible demand for the FIFA World Cup later on in the year”

- In News, DR pricing is up 30% and scatter pricing in news is up 54% above the upfront…”so all very good”

- National ad sales are strong led by pharma, Fin svs, and consumer packaged goods BUT the local market remains “mixed”

- Bullish on FY26: “As we look to fiscal 26, the overall advertising market for Fox continues to be healthy and robust”

FoxOne Is Launching In A Few Weeks But Aspirations Remain Modest

- Release date of Fox One is August 21st with a price of $19.99/mo standalone

- Incls all Fox brands & content, incl Fox Nation

- It will be marketed to the cordless mkt but also available to current payTV subs on an authenticated basis

- “Focused at keeping FOX One as a very targeted service that’s targeted on the cordless audience… but we also want to make it easy for our consumers and our viewers to gain our content”

- The Co will offer bundling oppties “that make sense to achieve our targeted goals”

- Aspirations for Fox One subscribers are “modest” and “measured investments” will match

- Any impact from speculation about NFL taking an ownership position in ESPN? Mgmt did not comment… “have a tremendous relationship with the NFL”

Snap & Pinterest: Investors Had Hoped For More

After Snap did not provide guidance for Q2 given the macro situation which spooked investors, the disclosure that Q2 topline growth was negatively impacted by a flawed update to its advertising platform, which resulted in some ad campaigns clearing “the auction at substantially reduced prices,” further spooked investors (though the Co has since reverted the change). Q2 adj EBITDA was also a focus as it came in -22% below expectations. On the plus side, Q2 DAUs of 469mn beat expectations by 2mn, but overall ARPU fell below projections as RoW missed and dragged down overall ARPU.

Looking into Q3 guidance, rev, adj EBITDA and DAUs were all ahead of the Street, though for the full year, infra cost per DAU is expected to come in at the top half of the range as they continue to invest in AI and ML infrastructure to drive improvements in their ad platform and content engagement.

As has been the case for some time, the Co has been growing its ad supply, but growth in demand is still lagging. Sponsored Snaps was emphasized as a “large incremental revenue opportunity,” as usage is ramping up and starting to show tangible results. Outside of advertising, Snapchat+ continues to grow at a steady pace of ~1mn subs per qtr and has reached an ARR of ~$700mn. The Co intro’d a new Snapchat+ subscription tier as well and spoke about having “room to experiment” on pricing. The other key update we would flag is on the AR front, with the Co announcing plans to make Specs available to the public in 2026. This comes after the previous five generations were available only to developers and is a “critical step toward realizing our long-term vision for augmented reality.”

Overall, there is still work to be done and investors are waiting for a cleaner quarter and confidence in sustained growth. See below for more thoughts on the key points from Snap’s results.

ALSO, SEPARATELY, BUT RELATED… we included some thoughts and takeaways on Pinterest results at the bottom as well, given it was another key result in the Social Media/Digital Advertising space.

->Snap plunged -17.2% on the back of its print and is down -31.2 YTD; Pinterest shares also fell -10.3% on the back of results but the stock is still up +21% YTD

It Was A Tough Q2 For Snap

- Q2 top-line growth was impacted by some disruptive factors, including an issue related to their ad platform, the timing of Ramadan, and the effects of the de minimis changes

- “Unfortunately, in our efforts to improve advertiser performance, we shipped a change that caused some campaigns to clear the auction at substantially reduced prices”

- “We have since reverted this change and advertising revenue growth has improved as advertisers adjust their bid strategies to achieve their objectives”

- Q2 adj EBITDA was disappointing…missed by -22%

Q2 DAUs Beat Expectations But Monetization Was A Challenge In RoW

- Q2 DAUs reached 469mn and beat cons 467mn, as a miss in N. America was offset by beats in Europe and RoW

- America unique Snap senders grew +2% y/y, “which is an important input to long term retention”

- Reached 932mn MAUs in Q2, +64mn or +7% y/y

- Reiterated “our goal of serving 1 billion Snapchatters around the world”

- Q2 ARPU of $2.86 missed cons $2.90, as beats in N. America and Europe were not enough to offset RoW coming in below expectations

Q3 Guidance Beat Consensus / FY25 Infra Costs To Come In At The High-End Of The Range Driven By Continued Investments

- Q3 rev – Slightly BEAT by +0.7% at the midpt: $1.475-1.505bn vs cons $1.48bn

- Q3 adj. EBITDA – BEAT by +4.8% at the midpt: $110-135mn vs cons $116.9mn

- Q3 DAUs to reach ~476mn vs cons 475.7mn

- Implied Q3 DAU growth of +7.4% y/y which is a seq decel from Q2’s +8.6% y/y

- For FY25, guided to be at the top half of the infrastructure cost per DAU range per qtr of 82c-87c

- “As we continue to prioritize investments in ML and AI infrastructure to drive improvements in our ad platform and depth of content engagement”

Annc’d “New, Distributed Structure” To “Better Align Snap’s Engineering And Technology Investments With Our Business Priorities”

- Distributing engineering teams to directly support business functions –

- Core applications team reporting to Bobby Murphy, Co-Founder and Chief Technology Officer

- Monetization engineering team reporting to Ajit Mohan, Chief Business Officer

- Chief Information Officer and Chief Information Security Officer will lead enterprise-wide foundational infrastructure and platform integrity, and will report to Evan Speigel, Co-Founder and Chief Executive Officer

- Meant to “empower our teams to take greater ownership and drive continued innovation for our community and advertising partners”

Building Ad Demand, Particularly For Sponsored Snaps, Remains A Key Focus

- Q2 total ad rev grew +4% y/y (vs +9% y/y in Q1) driven primarily by growth from DR ad rev

- Q2 direct response ad rev incr’d +5% y/y (vs +14% y/y in Q1)

- Driven by “strong” demand for Pixel purchase and app purchase optimizations as well as continued strength from the SMB client segment

- Q2 brand-oriented rev was flat y/y (vs -3% y/y in Q1)

- Q2 direct response ad rev incr’d +5% y/y (vs +14% y/y in Q1)

- Total ad rev growth trajectory in Q2…

- April – ad rev growth declined ~1%

- May – “largely recovered”

- Worked on reverting the ad platform change, and factor around Ramadan diminished

- Moving into June – rolled out Sponsored Snaps more broadly

- Impacted inventory and translated into lower platform-wide eCPMs and improved pricing for advertisers

- Going from June into July – post the rollback of the ad change, have seen ad rev grow at a rate b/w 3-4%

- SMBs were the largest contributor to Q2 ad rev growth, driven by a combination of more performant DR products, improved go-to-market operations, and a simplified ad buying experience

- Supply is growing, but demand isn’t keeping up

- Q2 global impression volume grew ~15% y/y (vs ~17% y/y in Q1), driven by “strong” engagement on Spotlight and creator Stories, as well as early contributions from Sponsored Snaps

- Q2 avg eCPMs were down -10% y/y (vs ~7% y/y in Q1)

- 7-0 Purchase volume incr’d +39% y/y for commerce advertisers, and total purchase-related ad rev grew 25%+ y/y in Q2 (+14% in Q1)

- Driven by enhanced AI and ML capabilities that improved conversion attribution, real-time personalization, and product relevance

- “Sponsored Snaps remain a large incremental revenue opportunity” / Has driven “meaningful” growth in incremental reach, conversion, and engagement thus far / Working to build demand

- Performance so far – early signs are “very positive”

- Delivered up to a 22% increase when included in an advertiser’s broader Snap campaign mix

- Drove an 18% lift in unique converters across app installs and app purchases

- 2x increase in conversion, 5x increase in click-to-convert ratios, and a 2x increase in website dwell times compared to other inventories

- Working to build more demand for Sponsored Snaps inventory: “We try to be really thoughtful about managing the supply growth with things like frequency caps and relevancy filters as we work to build more demand”

- Expanded Sponsored Snaps in the US and several other regions globally, activating all Pixel and App DR objectives

- Introduced First Snap, a single-day takeover format that delivers the first Sponsored Snap in the Chat inbox

- Began testing App End Cards, that reinforce advertiser messaging and guide users to a conversion at the end of a Snap Ad

- Introduced smarter tools like Target Cost Bidding to deliver performance and scale while remaining within an advertiser’s cost constraints

- Performance so far – early signs are “very positive”

- Investment in automation continues… launched Snapchat Smart Campaign Solutions, an AI-powered suite designed to enhance campaign performance and simplify advertiser workflows

- Includes Smart Bidding, which dynamically adjusts bids to achieve a desired cost per action

- “Encouraged” by initial testing of Smart Budget…, which automatically adjusts campaign budgets across ad sets

- …and the alpha testing of Auto-Targeting, which leverages AI to identify and reach high-value users

Announced Plans To Make Specs Available To The Public In 2026

- Working to make their first, fully standalone, lightweight Specs AR glasses available to the public in 2026 – a “critical step toward realizing our long-term vision for augmented reality”

- Will be “significantly smaller, lighter, and more capable” than 5th-gen Spectacles released to developers in 2024

- Snap is “uniquely positioned as the only company in the world with a fully-integrated AR computing stack”

- “We’re incredibly passionate about the opportunity to reinvent the computer”

- Cited stat that people spend 7+ hrs on avg staring at screen, “even just moving a couple of hours of that to […] see-through lenses and a pair of glasses can make a meaningful difference for people’s well-being, but also the way they interact with computing and AI in general”

- Advanced machine learning and AI + spatial intelligence = enable Specs to deliver “digital experiences embedded directly into the world around us”

- Recently launches Lenses for Specs include –

- Gowaaa’s “Super Travel” for real-time translation and currency conversion

- Paradiddle’s “Drum Kit” for interactive music learning overlaid on a physical drum set

- ANRK’s “Pool Assist” to help players make better shots while playing pool

- Recently launches Lenses for Specs include –

- Expanding utility and accessibility of AR platform to enable developer community to “build more unique, industry-leading experience” in advance of Specs public launch

- Introduced updates to Snap OS and new tools to unlock deeper AR capabilities

- Enabling creation of multimodal AI-powered lenses through –

- AI-powered experiences with OpenAI and Gemini on Google Cloud

- Hosted open-source models

- New Automated Speech Recognition API supports real-time transcription across dozens of languages

- Snap3D API empowers developers to generate 3D objects on the fly from any prompt

- Future enhancements include –

- New partnership with Niantic Spatial to develop a shared AI-powered map of the world

- Recently announced WebXR support

As More Creators Build New Lenses, More Snapchatters Are Using Them / Highlighted Games On Snapchat As A “Compelling” Oppty

- In Q2, 350mn+ Snapchatters engaged with AR every day, on avg

- Key Lenses stats –

- Snapchatters use AR Lenses in our camera 8bn+ times each day

- 400k+ creators from nearly every country have built 4mn+ Lenses using Snap’s AR tools day

- 90’s School Photos AI Lens, Different Eras AI Lens, and Cartoon World AI Lens were collectively viewed 1bn+ times in Q2

- Momentum in AR driven by “growing” AR creator and developer ecosystem

- Lens Studio, Snap’s desktop authoring tool, gives professional developers “powerful” tools to create “innovative” AR experiences

- Latest update supports creators building Lens Games…: Includes new Bitmoji Suite that makes it easier to bring 3D Bitmoji avatars to any game environment, along with new game assets, including leaderboards and multi-player features built specifically for Snapchat

- …driving Games engagement to reach 175mn+ MAUs, up +40% y/y – “We believe games represent a compelling long-term opportunity for driving engagement on Snapchat, and eventually new monetization opportunities for creators and our business”

- Easy Lens is an AI tool has made AR creation “increasingly more accessible” by enabling creators to build a Lens in just minutes by typing out a prompt for the Lens that they want to create

- Expanded access in Q2 “to help more people at all skill levels get started with AR: Introduced new Lens Studio iOS app and a new web-based Lens Studio creation tool at lensstudio.snapchat.com

- Lens Studio, Snap’s desktop authoring tool, gives professional developers “powerful” tools to create “innovative” AR experiences

Content Creation And Consumption On The Platform Continues To Grow + Other Community Feature Updates

- Global time spent watching content and the # of content viewers “increased” y/y in Q2, reflecting multi-year investment in machine learning infrastructure & cont’d growth in Spotlight

- Began testing their largest Mixed Feed model to date in Q2…: Cut training time by 50% & drove content view time growth

- …and these “strategic investments and improvements” have been “fundamental” in Spotlight reaching an avg of 550mn+ MAUs (vs 500mn+ in Q1)

- Time spent on Spotlight grew +23% y/y in Q2 (vs +25% y/y in Q1)

- Spotlight now contributes 40%+ of the total time spent watching content

- # of Spotlight posts by Snap Stars grew 145%+ y/y in N. America in Q2 (accel from +125% y/y in Q1)

- Introduced suite of new tools and features in Q2 to make it easier for Snap Stars to create and share content

- Creators can now generate videos from their saved Memories using templates

- Have access to new insights like returning viewers, top content, and total view time

- Introduced suite of new tools and features in Q2 to make it easier for Snap Stars to create and share content

- Snapchatters spending +30% more time video chatting y/y in Q2

- Leveraging investments in AI and machine learning to enhance Group suggestions “to help people connect more easily with their closest friends”

- Launched Snapchat app on Apple Watch in Q2, allowing Snapchatters to preview incoming messages and respond using the Keyboard, Scribble, Dictation, or emojis

- Acquired Saturn in in Q2, a social calendar app that helps high school and college students manage and share their class schedules

- Students from 80%+ of US high schools use Saturn with their friends to organize their day

- “We are excited to support Saturn’s growth and explore ways to integrate its calendaring expertise into Snapchat in new and innovative ways”

Snapchat+ Growth Continues At A Steady Cadence / Launched New Snapchat+ Tier And Seeing Potential “Room To Experiment” On Pricing

- Snapchat+ is the primary driver of “Other” rev which was up +64% y/y (vs +75% y/y in Q1) to reach an ARR of “nearly” $700mn (vs “just over” $600mn in Q1)

- Snapchat+ “approached” 16mn subs in Q2

- Vs “nearly” 15mn in Q1, 14mn in Q2, 12mn+ in Q3, and 11mn+ in Q2

- Intro’d new Snapchat+ subscription tier – Lens+: Offers access to exclusive new AI video Lenses, Bitmoji Games Lenses, as well as early access to new features

- Opportunity to offer exclusive Lenses and AI Lenses (“which have proven incredibly popular”) will be “a strong driver of growth” for Lens+

- “Room to experiment” on pricing: Primary focus is on continuing to build the value prop for customers but “given the size of the revenue opportunity in front of us, we’ll be investing more in pricing experiments”

SEPARATELY, as mentioned above, we included some abbreviated thoughts and takeaways on PINTEREST results as well.

Pinterest: Q2 was strong, led by better-than-expected revenue and adj EBITDA, though the UCAN performance underwhelmed on ARPU vs expectations (users were in-line though did grow +5% y/y). While the overall tariff impact was less than expected in Q2 but it did impact the US as Asia-based ecommerce companies pulled back. Despite the nice Q2 beat, Q3 guidance was just slightly ahead of the Street and in looking at H2, the level of margin expansion will be below that of H1 given growth investments. See below for some addtl details.

-> Pinterest shares fell -11% on the back of results though is still up +15% YTD

- Q2 rev – BEAT by +2.4%: Grew +17% y/y to reach $998mn

- UCAN – MISSED by -0.3%: Grew +11% y/y, with strength coming from retail and financial svs

- Europe – BEAT by +10.4%: Grew +34% y/y (+29% ex-FX), fueled by retail

- RoW – BEAT by a wide +16.7%: Grew +65% y/y (+72% ex-FX)

- Q2 adj EBITDA – BEAT by +7.3%: Reached $251mn (25.2% margin, ~+310bps y/y)

- Verticals –

- Retail and Financial svs: “Continue to be a source of strength”

- Food and beverage: Incr’d actionability in food & beverage by partnering w/ Instacart, enabling users to shop directly from ads

- Q2 ad impressions grew +55% y/y (vs +49% y/y in Q1), and ad pricing declined -25% y/y (vs -22% y/y in Q4), driven by growing mix shift from ad impressions in previously unmonetized or under-monetized international markets, which carry lower ad pricing than more mature markets

- Q2 Global MAUs reached a new milestone of 578mn, growing +11% y/y (increase from +10% y/y in Q1)

- Users continue to grow y/y across all geographies in Q2, but declined q/q in Europe

- US and Canada MAU +5% y/y

- Europe MAU +7% y/y

- RoW MAU +14% y/y

- Users continue to grow y/y across all geographies in Q2, but declined q/q in Europe

- Q2 ARPU grew +6% y/y overall with US & Canada In-line w/ cons and Europe & RoW beat by +0.7% & +0.6%, respectively

- Tariff impact in Q2 was less significant than initially expected, as the Co did see some impact affecting the UCAN region

- Asia-based e-commerce retailers reduced their US ad spend due to changes in the de minimis exemption

- But this was partially offset by spend in other regions

- Q3 guidance was just slightly ahead of the Street

- Q3 rev guidance – BEAT by +1.6% @ midpt: Range implies +15-17% y/y growth (assumes the impact of foreign exchange to be ~1 point of tailwind based on current spot rates)

- Q3 adj EBITDA guidance – INLINE @ midpt

Adj EBITDA margin are expected to expand in H2 but the magnitude will be lower than posted in H1 given investments (head count growth within R&D to support efforts in AI and other product initiatives as well as global enterprise sales team)

- Update on Performance+…lower-funnel revenue more than doubling since the end of last year

- Notable early adoption w/ mid-market advertisers… “feel really good about adoption”

- Entered beta testing for Pinterest Performance+ Creative Preview –

- Advertisers can now preview generative backgrounds and image resizing directly in the campaign setup flow

- Pins can be regenerated easily, giving brands more control and transparency over creative output

- Customer groups in Performance+:

- New functionality allows advertisers to merge their audience data with Pinterest’s data while utilizing AI trained on unique signal of user tastes and preferences

- Enables more granular targeting and bidding strategies, especially for acquiring new customers

- Their Gen Z focus remains a key demo

- Gen Z now makes up over 50% of Pinterest’s monthly active users (MAUs)

- Leveraging AI to deliver visual search and curated recommendations, which resonate strongly with Gen Z’s preference for intuitive, image-based browsing

- Per a recent Adobe study, 47% of Gen Z participants use Pinterest as a search engine, with over 70% citing its visual appeal as the main reason

The Coming Inflection For TTWO Is Tracking On Plan

Following EA’s results last week, Take-Two gave us another look at key video game trends. Overall, the Co beat expectations and while next qtr’s guidance was underwhelming, mgmt upped the full year bookings outlook and now expects growth of +8% y/y at the mid-pt. Points from TTWO’s results that we thought were most incremental include: 1) a strong acceleration in RCS growth in FQ1 (+17% y/y) but it will slow considerably in FQ2 (to ~+1%); 2) mobile had a very strong qtr but growth is expected to slow down next qtr; 3) NBA 2K strongly outperformed and NBA 2k26 (to launch Sept 5th) will be a key catalyst; 4) GTA Online had a nice boost this qtr but will likely decline next qtr; and 5) while the Co raised FY26 net bookings guidance they also raised opex growth guidance as well (due to marketing investment).

When all is said and done, the business is moving in the right direction and mgmt remains very bullish… “we have exceptional confidence in our multi-year outlook…expect to achieve record levels of net bookings in fiscal 2027 that we believe will establish a higher baseline for our business and sets us on a path of enhanced profitability.” We think that sounds about right.

See below for more on what we thought was most incremental from TTWO’s call and results.

ALSO, SEPARATELY, BUT RELATED… we included Quick Takes on Unity and AppLovin’s results at the bottom given they were other key prints in the videogame space this week as well.

-> TTWO fell -4.0% post its print and ended the week down -1.5%; However, YTD, the stock is still up +18.1%

FQ1 Net Bookings Topped Guidance & Recurrent Consumer Spend (RCS) Accelerated Growth

- FQ1 net bookings BEAT by +8.6%: Up +17% y/y (vs +14% y/y in FQ4) and was well above the guidance range

- Led by the outperformance of several mobile titles, as well as the continued success of NBA 2K & the Grand Theft Auto series

- Recurrent consumer spending growth accelerated from +14% y/y last qtr to +17% this qtr (and well above the guidance of +7% y/y); It accounted for 83% of net bookings

- NBA 2K: Grew nearly 50%

- GTA Online: Grew low SD

- Mobile: Incr’d low teens

- Adj EPS of $61 vs cons $0.29

FQ2 Will Be A Slower Bookings Growth Period Than Expected…

- FQ2 net bookings guidance was lower than expected (missed cons by -2%)…mid-pt implies +8% growth y/y

- Net bookings missed cons: Mid pt of net bookings range of $1.7-1.47bn was -2% below cons and slightly above $1.47bn in the yr-ago qtr

- Op expenses are expected to grow +7% y/y due to marketing

- GAAP net revs $1.65-1.7bn

- EPS range of $0.20-$0.30

- Release slate for the qtr: Mafia: The Old Country, NBA 2K26 & Borderlands 4

- Largest contributors to Net Bookings are expected to be: NBA 2K, Borderlands 4, the Grand Theft Auto series, Toon Blast, Match Factory, Empires & Puzzles, Color Block Jam, the Red Dead Redemption series, Words With Friends, and Mafia: The Old Country

- RCS growth of +~1%, which assumes –

- NBA 2K: Grow low SD growth

- Mobile: “Slight” growth

- Grand Theft Auto Online: “Decline”

BUT The Co Raised FY 2026 Bookings Guidance W/ NBK 2k and Mobile Key Drivers…Though Also Raised FY26 OpEx Growth Expectations

- Raised FY26 net bookings guidance to $6.05-6.15bn (from $5.9-6bn) which implies +8% y/y growth at the midpoint

- Largest contributors to Net Bookings are expected to be: NBA 2K, the Grand Theft Auto series, Toon Blast, Borderlands 4, Match Factory, the Red Dead Redemption series, Color Block Jam, Empires & Puzzles, and Words With Friends

- Raised RCS growth to +4% y/y vs prior guidance of ~flat y/y due to improved view on NBK 2k and mobile; RCS is expected to represent 76% of Net Bookings

- NBK 2k: Grow mid- teens, up from previous HSD

- Mobile: Grow low SD, up from “declines”

- Grand Theft Auto Online: “Decline”, in-line w/ previous guidance

- Expect the Net Bookings breakdown from labels to be ~45% Zynga, ~39% 2K, and ~16% Rockstar Games (no change)

- Reiterated operating CF of ~$130mn and CapEx of ~$140mn

- Raised GAAP net revenue $6.1-6.2bn (up from $5.95-6.05bn) and raised cost of revenue $2.55-2.57bn (up from $2.519-2.545bn)

- Also now expect higher OpEx growth of ~5% y/y, from prior ~3% y/y guidance due to higher personnel cost and higher mkting spend to support mobile, and FX

Biggest Drivers in FQ1 = Mobile + GTA Series & NBA 2k25

- The Mobile business “vastly” outperformed…grew “low teens”

- Toon Blast grew +22% y/y and almost 75% on a 2-yr basis: The Co’s “seasonal collection” feature drove a new path for engagement

- Match Factory grew 33% y/y: Driven by new features

- Color Block Jam “maintained momentum”

- 2K’s mobile offerings also had “a great quarter”

- Continue to focus on mobile DTC business: Are achieving better conversion driven by new offers, events, and enhanced personalization

- The recent court ruling also provides further growth in this area

- GTV series also exceeded expectations, again, and momentum remains “exceptionally strong”…GTV Online grew low SD

- GTA V to date has sold-in 215mn+ units worldwide

- GTV Online engagement benefited GTA VI Trailer 2 + release of the “Money Fronts” Summer content pack

- New player accounts for GTA Online grew over 50% y/y

- Recurrent consumer spend beat expectations

- NBA 2K25 delivered “another quarter of fantastic results” …was up “nearly 50%”

- To date:

- Sold-in 11.5mn+ units

- Engagement grew significantly y/y: DAU and MYCAREER DAU each up 30% y/y

- Recurrent consumer spend grew + 48%

- Annc’d a new multiyear global partnership expansion w/ the NBA, NBPA, and WNBPA, and extended its longstanding relationships with the NBA G League and USA Basketball

- To date:

- WWE 2K25 was another game call out: Launched on Nintendo Switch 2 in July, which expanded its audience

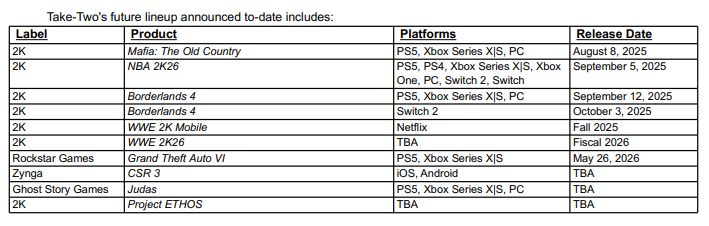

Have “Enormous Anticipation” For FQ2’s Launches

- August 8th: Mafia: The Old Country

- Have a 2.5mn wish lists across platforms, showing strong consumer interest

- Feedback from early play has been encouraging

- Sept 5th: NBA 2K26 – which will “again raise the bar” for basketball experiences

- Aug 29th is early access

- It will be the first game from the series to launch on Nintendo Switch 2

- It will feature new immersive technology

- 30 unique storylines to win a championship

- More details will be shared in the “coming weeks”

- Sept 12th: Borderlands 4 – the “eagerly anticipated next entry in our iconic looter-shooter franchise”

- “Extremely” positive feedback from global press and content creators

- June’s Borderlands Fan Fest generated 600k hours of streams & videos

- The title will launch on Nintendo Switch 2 in Oct

- Later this fiscal year: WWE 2K26…will have more to share in the “coming months”

A Few Other Key Comments

- FQ1 ad revs were flat y/y as adjusted approach… Moved from hyper-casual to hybrid-casual

- “We certainly hope to grow from here”

- Philosophy on pricing is to deliver more value than what they charge…Variable pricing is part of the industry and do not think that will change

- Mgmt expects consumers to be more selective on spend in this macro environment but that they will focus on “quality”

- “We have exceptional confidence in our multi-year outlook…expect to achieve record levels of Net Bookings in Fiscal 2027 that we believe will establish a higher baseline for our business, and set us on a path of enhanced profitability”

SEPARATELY from Take-Two’s results, Unity and AppLovin also reported this week. See below for our Quick Takes

Quick Take – Unity:

- Reported stronger than expected results especially as it related to margins though despite the beat, Q3 guidance was ~in-line w/ expectations

- Adj EBITDA margin of 21% easily beat cons 18% and led to a +17% beat on adj EBITDA, on the back of better-than-expected revenue (beat by +3.2% which was mostly driven by Create Solutions)

- That said, revenues are still in decline (fell -2% y/y but an improvement from -5% y/y in Q1)

- The Q3 revenue guidance implies mid-single digit seq growth and DD growth is expected for the Unity ad network

-> Unity share price fell -6% on the back end and is up +48% YTD

Quick Take – AppLovin:

- Reported solid results vs cons with a modest beat in Q2 and slightly better than expected Q3 guidance

- Revs grew +77% y/y; Net revenue per installation rose +70% & installations increased +8%; Adj EBITDA rose +99% y/y

- Generated $768mn in FCF and repurchased $341mn in stock in the qtr

- On June 30th, completed the sale of the Apps business to Tripledot Studios for $400mn in cash

–> AppLovin share price rallied +12% on the back end and is up +41% YTD

Warner Music Group Is Finding Its Rhythm Again

Over the past year, Warner Music Group’s shares have had its ups and downs, leaving it almost exactly flat from where it was ~one year ago. The Co had been contending with slowing streaming growth and FX weighing on its margin trajectory, amongst other things but investments in people and operations showed signs of progress this quarter with a broad-based beat relative to Street consensus. What we thought were the biggest stand-outs include 1) revenue growth accelerated thanks to Recorded Music Subscription streaming growth bouncing back (to +8.5% adjusted from +3.2% last qtr ex-FX); 2) the Co gained market share in the US based on 3rd party data; 3) while Ad supported streaming remains under pressure (driven by short form media), it was encouraging to see a continued sequential improvement in that decline; 4) M&A is expected to ramp on the back of the year with the $1.2bn JV with Bain (its first acquisition is expected “soon”; 5) WMG remains in “deep discussions” with DSPs about launching super fan tiers (which we all have been waiting for!); and 6) efficiency efforts are accelerating as well.

While WMG has stepped up investment on a targeted basis, mgmt. stressed its commitment to shareholder returns via the existing buyback and dividend, which it just increased as well. Overall, it looks like the strategy and people are in place and it will come down to continuing to execute as mgmt did this quarter.

-> WMG shares rallied +3.7% on the back of earnings which brings the YTD performance into positive territory, up +2.3%

WMG Delivered A Broad-Based Beat In FQ3…Re-Accelerating Growth

- Total FQ3 revs BEAT cons by +6.2% and adj OIBDA BEAT by a larger +10.1%:In constant currency –

- Total revs rose +7% y/y or +8% y/y adjusted for notable items (vs up from +1% y/y in FQ2)

- Adj OIBDA grew +16% or +17% y/y adjusted for notable items (vs -1% y/y in FQ2

- Margins incr’d +170bp y/y

- Performance by segment (in constant currency) –

- Recorded Music – BEAT: Revs grew +6.4% or +8.3% y/y on adjusted basis (vs FQ2 +1% y/y) & beat cons by +6.6% while adj OIBDA rose +12.2% y/y (vs 1% in FQ2) & beat by 8.5%

- Music Publishing – BEAT: Revs were up +9.4% y/y (vs +3% y/y in FQ2) & beat by 1.6% while adj OIBDA rose +20% y/y & beat by 8.2%

- Margins were stronger than expected… adj OIBDA margin of 22.1% beat cons 21.3%

- This included a $9mn benefit from a copyright settlement in FQ3: Last qtr included a $12mn benefit from DSP true-up payments, making the year-over-year comparison affected by these one-time items

- Overall the margin growth was driven by revenue mix, impact of acquisitions and cost savings

- FQ3 operating CF conversion was 12% but mgmt continues to target 50-60% over a multi-yr period

Subscription Streaming Growth Bounced Back While Ad-Support Streaming Remains Under-Pressure

- Recorded Music Subscription streaming grew +2% y/y ex-FX, or +8.5% adjusted (+3.2% y/y last qtr)

- Ad-supported streaming is still in decline but showing seq improvement in FQ3…it fell -1.8% y/y ex-FX (vs the -3% y/y in FQ2 and -7.5% y/y in FQ1) given the “soft overall ad environment”

- The Co is actually seeing growth with core DSP – there is a lot of oppty to accelerate

- The challenge is really in short form media – will take time to improve

The Co is Making Progress On Many Of Its Growth Pillars

- Reaccelerating growth came through this qtr and was broad based

- Looking ahead…they are stepping up targeted investment in key markets that they have zero’d in on

- WMG incr’d market share in the qtr: US where mkt share rose 1pp y/y (per Luminate data)

- M&A will accelerate on the back of the $1.2bn JV with Bain…expect news of their first acg “soon”

- Continue to see “progress in aligning contracts” w/ streaming services “in this new price-driven growth approach”: Expect to see the impact of renewals (since Feb) “in 2026 and beyond”

- Spotify’s annc’d price increase outside the US earlier this week points to the music value proposition

- WMG is in “deep discussions” w/ DSPs on the design & implementation of the super fan tiers…this is something they are still very optimistic about

- Plan to further increase efficiency post last’s months annc’d $300mn annual run rate savings by the end of fiscal 2027

- Expect to see margin expansion of 150- 200 bp in F26

Other Key Updates/Comments

- Capital returns also remain a priority: While the Co is stepping-up investment in the core music business & catalog M&A, they are also returning capital to shareholders via a $100mn buyback authorization + annc’d raising the qtrly div by 6% to 19c (5th yr in a row of increase)

- Have exciting music coming out: Ed Sherran, Zavh Bryan, Alex Warren, Twenty One Pilots, Somber, Cardi B, David Guetta, and more

DraftKings: Sports Betting Outcomes Swing Back To The Sportsbook Just In Time For A Seasonally Strong Fall

After a couple quarters of unusually higher customer friendly sports betting outcomes, the pendulum swung back the other way for DraftKings in Q2, helping to drive better-than-expected results (revenues and adj EBITDA beat consensus by +6.3% and +24.3%, respectively). Much higher user monetization (ARPMUP exceeded Street estimates by +23.5%) more than offset softer user growth (stemmed from Losing Jackpocket Texas) and helped drive revenue growth to +37% y/y, meaningfully accelerating from Q1’s +20% y/y. In addition to Sportsbook-friendly outcomes, a growing parlay mix also helped drive revenue and live betting has been a major growth engine (and continues to be a big opportunity). Mgmt remains keen on exploring new opportunities like prediction markets as well and while iGaming showed steady progress, there is still work to be done.

Looking ahead, given the current trends YTD and expectations headed into its seasonally important H2 with the NFL and NBA season start, the Co now expects to hit the high end of its 2025 revenue range outlook, though at the same time, expects to hit the mid-point of its adj EBITDA range as it absorbs Missouri launch costs and higher taxes. With that said, the Co remains optimistic about the long term adj EBITDA margin trajectory target (to 30%).

See below on more of what we thought were the most incremental and important takeaways from DraftKings’ earnings and conference call and the odds are in favor of a strong H2.

-> DraftKings shares closed the day flat post results but is up +15% YTD

Headline Q2 Was Very Strong Given Much Better User Monetization (Though User #s Disappointed)

- DKNG easily outpaced consensus estimates and revenue accelerated

- Q2 rev BEAT by +6.3%: Incr’d +37% y/y (accelerating from +20% y/y in Q1)

- Q2 adj EBITDA BEAT by +24.3%: $301mn vs yr-ago $127mn (vs +363% y/y in Q1)

- Q2 adj EPS BEAT by +12.5%: Up 72% y/y vs 60% y/y in Q1

- User monetization (ARPMUP) was materially higher than expected BUT monthly unique players (MUPs) disappointed

- MUPs at 3.3m fell short of cons 3.85mn: Losing Jackpocket Texas had a neg impact

- ARPMUP of $151 was 23.5% ahead of cons $122: Y/Y improvement was driven by their Sportsbook hold of 10.9% (9.5% in Q1) + promotional reinvestment

- Sportsbook promotional reinvestment improved nearly 600bps y/y as a % of gross gaming revenue

Now Expects To Hit The High End Of The 2025 Revenue Guidance Range But Only The Mid-Pt On Adj EBITDA Guidance On Higher Taxes & Missouri Launch Costs

- 2025 guidance is ahead of estimates

- Rev – expects to hit “closer to the high end” of the $6.2-6.4bn guidance range: Due to Q2’s sportsbook-friendly outcomes

- This is above Street estimates that were at the mid-pt of guidance

- Adj EBTDA – expects to hit the “mid-pt” of the $800-900mn guidance range: This is slightly above the Street as well

- Rev – expects to hit “closer to the high end” of the $6.2-6.4bn guidance range: Due to Q2’s sportsbook-friendly outcomes

- What is, and is not, factored into the guidance?

- Missouri: Includes costs associated the mobile sports betting launch in Missouri later this year

- Missouri will launch in early Dec and have a ~$35-45mn EBITDA impact this year

- Expect the cadence of customer acquisition to look similar to states like Ohio and Mass)

- “CACs should be fantastic as it is right in the middle of NFL and NBA and will have all major sports outside baseball”

- Taxes: Includes anticipated financial impacts from higher tax rates in New Jersey, Louisiana, & Illinois

- The impact of Illinois is unclear; The approach was “unprecedented” and “it isn’t a great solution”; Mgmt hopes that Illinois will make a change; “It is uncharted territory”

- Does not include potential launch of a Prediction Markets offering

- Missouri: Includes costs associated the mobile sports betting launch in Missouri later this year

- Other 2025 guidance related updates –

- Sportsbook net revenue margin is expected to exceed 7.5%, ahead of the 7-7.5% range provided last Q1