Taking a break from all the volatility and uncertainty that has been non-stop over the last few weeks, I wanted to start on a lighter side with 3 call outs…1) It was fun to watch the excitement from Monday’s successful all-female (incl Katy Perry) Blue Origin space launch, which marked the 1st time in over 60 years that a crew entirely composed of women has been launched into space; 2) Google’s Dolphin Gemma LLM is interesting in that it is helping scientists decipher dolphin’s communication (think of the implications here!); and 3) not to date myself, but this week 38 years ago, 21 Jump Street premiered. I used to love that show. 😊

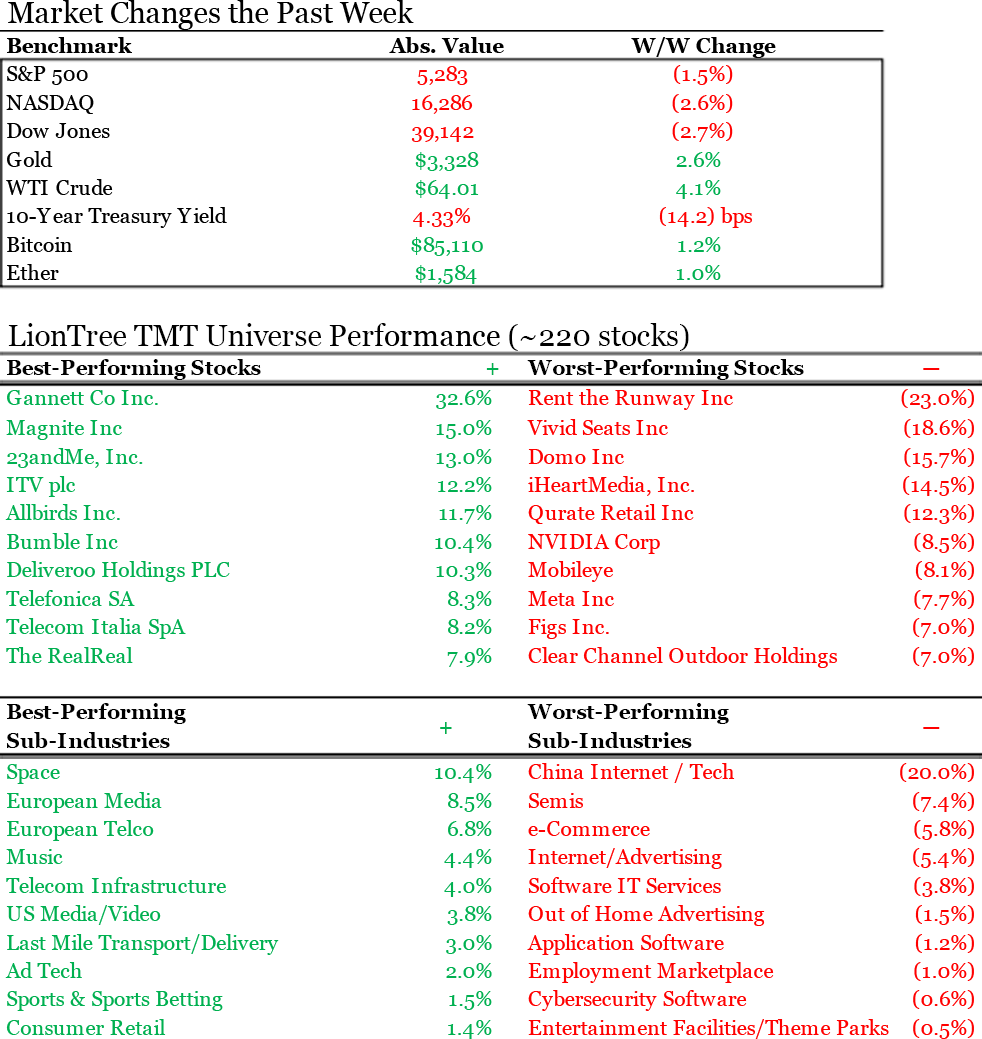

Back to business, after the huge market rally the week prior, we had some give back this week (S&P 500 down -1.5% and Nasdaq down -2.6%) as tensions with China escalated and impacts of the trade war remains uncertain. Fed Chairman Powell’s hawkish comments during Wednesday’s FOMC meeting also left investors less confident in any near-term rate cuts. We have started to see a string of company pivots and strategic shifts to navigate these choppy waters (see Theme #2) and expect many more to come.

In this edition, we focused on the below updates, developments and themes (and thanks a lot Netflix for reporting on a Thursday night before the holiday market close!):

- Where Do CEOs Think Their Companies & The Economy Are Headed?

- TMT Companies' Pivots Left & Right To Adjust To The Trade Wars...

- Netflix’s Steady As She Goes…A Beacon Of Stability During These Volatile Times

- The TMT Sell-Side Scrambles To Factor Business Conditions + Uncertainty Into Company Estimates

- Both Publicis & Omnicom Contend That Brands Still Need To Spend On Advertising Even In Tough Times

- 'Meta Vs FTC' Enters The Ring... While New Tech Regulatory Actions Also Emerge

- Global Media Usage Is Expected To Take A Dip In 2025

- AI Chatbot Momentum Continues / US Startup Funding Hits Highest Levels Since 2021 / Lyft Enters Europe With FREENOW Acq

Have a nice weekend.

Best,

Leslie

Just wanted to flag one last time our most recent LionTree’s Lens: Sector Insights & A Look Ahead, Spring 2025 deck, which offers our current perspectives on the key themes shaping the TMT and consumer space – click HERE to watch the ~20-minute VIDEO presentation and to access the full slide DECK.

Where Do CEOs Think Their Companies & The Economy Are Headed?

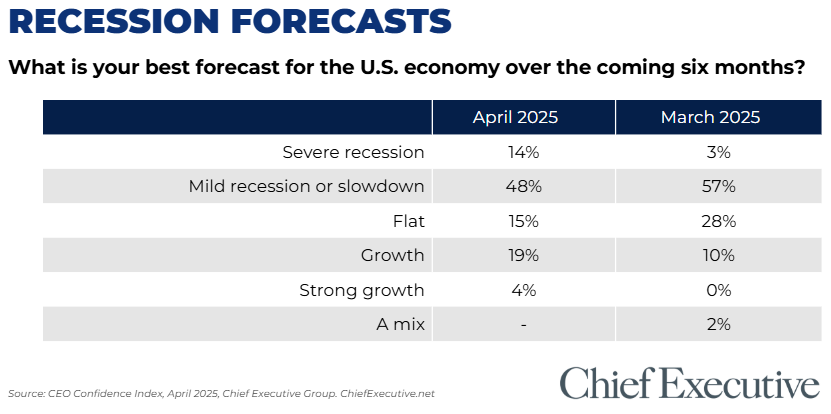

The latest monthly survey conducted by Chief Executive and released on Monday seemed very timely and provided at least some perspectives on sentiment from the C-Suite, who are trying to navigate and steer the ship during the current macro storm of events. Big picture, based on a polling of 300+ CEOs in April, expectations for a recession jumped sharply to 62% (though a smaller 14% anticipate a severe recession). Overall, CEO sentiment has quickly moved quite negative over the last month. See below for the takeaways in the survey that we found most interesting and see link to survey if you would like to see more.

-> For reference, based on Bloomberg data, Wall Street economists foresee a 30% probability of a recession but as mentioned in prior editions, banks such as Goldman Sachs & JP Morgan have recently raised their recession probability estimates to 45% and 60%, respectively, hence the bias seems to be moving up. (link/link)

- 62% of respondent CEOs anticipate a recession or other economic downturn in the next 6 months, which is up from 48% who said the same in March

- This is the lowest level since the early months of the pandemic in 2020

- Digging a little deeper, 48% expect a mild recession (DOWN from 57% in March) BUT 14% expect a severe recession (UP from 3)

- View on tariffs? 76% of CEOs said tariffs would negatively or very negatively impact their businesses this yr

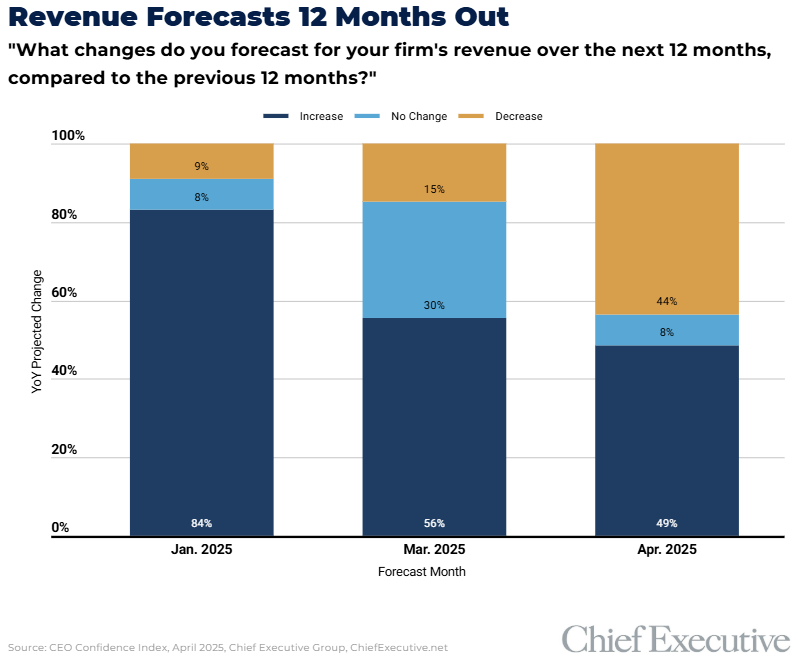

- Revenue outlook expectations have materially worsened since Jan

- 49% anticipate rev to grow in 2025, which is DOWN from 84% anticipating the same in Jan

- 44% expect reve to decline in 2025, which is UP from 9% anticipating the same in Jan

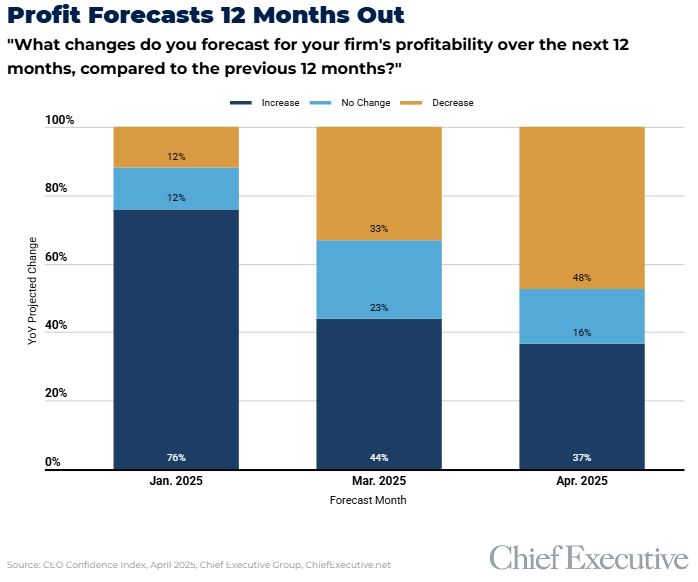

- Profitability outlook expectations have also materially worsened since Jan

- Only 37% believe their companies’ profits will increase in 2025, which is down materially from 76% who said the same in Jan

- 48% expect profits to decrease, which is up from 12% who said the same in Jan

TMT Companies' Pivots Left & Right To Adjust To The Trade Wars...

The ripple effect of the ongoing trade and tariff policies are beginning to take shape, with companies adjusting operations and expectations in response. This was especially evident amongst the semiconductor Cos this week, as Nvidia and AMD reported multibillion- and multimillion-dollar impacts, respectively, from export restrictions on chips to China. While ASML maintained its long-term outlook, it also noted heightened macroeconomic uncertainty due to the tariffs. Industry estimates cited by US govt officials point to the semiconductor equipment industry potentially losing over $1bn annually due to these policies.

Beyond chips, consumer electronics companies are also navigating these added pressures. Apple accelerated $2bn in iPhone shipments to the US, while Sony pointed to macroeconomic factors when it annc’d its PlayStation 5 price increases across several international markets.

A multitude of companies are also adjusting their supply chains. Nvidia plans to produce up to $500bn of AI infrastructure in the US, while Apple is ramping up production in India and Vietnam. Additionally, broadband providers like Comcast and Verizon are introducing long-term price lock plans in response to rising consumer cost sensitivity.

In the midst of all this, Chinese Cos are also taking steps to support domestic exporters by facilitating local distribution which helped prop up the Chinese Tech stocks this week.

There are a lot of moving pieces to keep track of but likely the first of many more of these sorts of updates as we look in the weeks and months ahead …see below.

Semiconductor Cos Are Flagging Substantial Impacts To Top-Line

Nvidia expects $5.5bn hit in FQ1 due to new limits on China exports (link/link/link/link/link)

- The US govt informed Nvidia on Monday (Apr 14) that its H20 chip would require a license to export them to China “for the indefinite future”

- To note, no licenses for GPU shipments into China have ever been granted

- The new rules are meant to address concerns that “the covered products may be used in, or diverted to, a supercomputer in China”

- Nvidia said that it will report ~ $5.5bn in charges during fiscal Q1 from “inventory, purchase commitments and related reserves” tied to the H20 line

- For context, China is Nvidia’s fourth-largest region by sales, after the US, Singapore, and Taiwan

- NVIDIA has reportedly secured $18bn worth of H20 orders YTD, with a considerable portion of that demand coming from Chinese companies, including Tencent, Alibaba and ByteDance

-> NVIDIA fell -6.9% in reaction and is now down -24.5% YTD

Advanced Micro Devices expects an $800mn hit from US chip restrictions on China (link/link)

- AMD said in a filing that it could incur charges of up to $800mn for exporting its MI308 products to China and other countries

- The new US license requirement, which applies to exports of certain semiconductor products, would hit inventory, purchase commitments and related reserves

- While the Co said it plans to apply for export licenses, it cautioned “there is no assurance that licenses will be granted”

-> AMD shares closed down -7.4% on the day of the announcement and is now down -27.6% YTD

ASML maintains guidance, but warns of incr’d macro uncertainty due to US tariffs (link/link/link)

- CEO Christophe Fouquet said his conversations w/ customers supported ASML’s expectations that 2025 and 2026 would be growth years BUT “the recent tariff announcements have increased uncertainty in the macro environment”

- Reiterated net sales and gross guidance for 2025 and 2026, but increased the range for Q2

- The Co also said it does NOT have plans to move more production to the US to limit the exposure of potential tariffs

- It also plans to pass more of the tariff costs onto customers – “the burden of tariffs from our vantage point should be allocated in a fair way…We think that those taking it in the United States should, therefore, take the lion’s share of that allocation”

Taking A Step Back – Trump’s Tariffs Could Cost US Semiconductor Equipment Makers $1bn+ Annually, Per Industry Calculations (link)

- Lawmakers and administration officials reportedly discussed these tariff costs with chip industry execs and SEMI representatives (an intl trade group) in Washington as part of ongoing dialogue

- Each of the three largest US chip equipment makers – Applied Materials, Lam Research and KLA – may suffer an annual loss of ~$350mn related to the tariffs

- Smaller Cos, such as Onto Innovation, may also face tens of millions of dollars in extra spending

- The estimated costs included –

- Lost revenue, primarily for missed sales of less sophisticated equipment to overseas rivals

- Costs of finding and using alternative suppliers for the complex components of chipmaking tools

- Tariff compliance costs, such as adding personnel to handle the complexities of following the rules

Cos Are Taking Costlier and More Complex Steps To Work Around The Tariffs

Apple airlifted $2bn worth of iPhones from India to the US ahead of Trump tariffs back in March, an all-time high (link/link)

- Apple airlifted 600 tons of iPhones using at least six cargo jets from Chennai, with most shipments landing in Chicago, as well as Los Angeles and New York to maintain US inventory amid a 26% duty on Indian imports

- To expedite shipments, Apple lobbied Indian airport authorities to cut the time needed to clear customs at Chennai airport to six hours, down from 30 hours

- Apple’s suppliers Foxconn and Tata Electronics exported $1.31bn and $612mn, respectively, worth of iPhones

- Foxconn, Apple’s main India supplier, exported smartphones worth $1.31bn in March, its highest ever for a single month and equal to shipments for Jan and Feb

- Included shipments of the iPhone 13, 14, 16, and 16e models

- Tata Electronics, another Apple supplier, saw March exports increase +63% from February

- Included shipments of iPhone 15 and 16

- Foxconn, Apple’s main India supplier, exported smartphones worth $1.31bn in March, its highest ever for a single month and equal to shipments for Jan and Feb

Sony is raising PlayStation 5 prices in Europe due to a “challenging” economic environment (link/link/link)

- Increasing prices in “select markets” in Europe, the Middle East, Africa, Australia and New Zealand

- The “tough decision” was against the “backdrop of a challenging economic environment, including high inflation and fluctuating exchange rates”

- What do the hikes look like?

- The Digital Edition is the main target for price increases, rising in all four markets (+€50 in Europe, +£40 in UK, +AUD $100 in Australia, and +NZD $89.99 in New Zealand)

- Standard version (includes a disc drive) is only going up in Australia (+AUD $30) and New Zealand (+NZD $50)

- PlayStation 5 Pro will remain the same price across all four markets

- Price of add-on disc drive accessory is slightly decreasing

- Sony previously raised the price of the PlayStation 5 in Canada, Mexico, Europe, UK, Australia, Japan, and China back in 2022, due to “challenging economic conditions,” including global inflation rates and adverse currency trends

-> On a related note, shortly after Sony’s announcement, Nikkei Asia reported that an internal memo from a major Chinese supplier for Nintendo suggested that the upcoming $450 Switch 2 could also see its price go up (link)

Comcast has launched a 5-yr price guarantee for Xfinity internet customers to address “two significant consumer pain points – rising costs and transparency” (link/link/link)

- For the first time Comcast is offering new Xfinity Internet customers plans starting at $55/mo, locked in for 5 yrs w/ no annual contract required

- Also includes a free unlimited wireless line for one year

- Customers are free to cancel at any time

- Comcast internet customers will also no longer have a data cap if they are using one of these plans with a 5-yr price lock guarantee

-> This comes just a couple weeks after Verizon introduced a 3-yr price lock for all new and existing customers on myPlan & myHome (link)

Cos Are Adjusting Their Supply Chains As They Navigate Ongoing Tariff Changes

Nvidia aims to manufacture Nvidia AI supercomputers entirely in the US (link/link)

- The Co plans to produce up to $500bn of AI infrastructure in the US via its manufacturing partnerships with TSMC, Foxconn, Winstron, Amkor, and SPIL over the next 4 yrs

- It has commissioned 1mn+ sq ft of manufacturing space to build and test Blackwell chips in Arizona, as well as AI supercomputers in Texas

- Mass production at both plants is expected to ramp-up in the next 12-15 months

Apple is reportedly trying to ramp manufacturing in India and Vietnam (link)

- Apple has tasked key suppliers w/ increasing iPhone manufacturing in India to at least 50mn units this yr

- The Co is also pushing to produce the majority of its upcoming US-bound iPhone model in India

- Apple has addt’lly directed suppliers to shift MacBook and iPad production for the US mkt to Vietnam

- But the Co is reportedly dealing with tightened Chinese customer screening, which have been ongoing for months and stalling the export of production equipment from China

- Another challenge is that India’s factory utilization is already at max capacity and key components, like connectors, metal cases, and mechanical parts remain most cost-effective to produce in China

Amongst The Tariff Chatter, China Tech Has Been Coming To The Rescue Of China Exporters

- JD.com annc’d that it will spend Y200bn+ to help Chinese exporters sell their products in the domestic market in the coming year (link)

- JD.com is sending sales and procurements teams to firms and will directly purchase products from them

- Alibaba’s retail brand Freshippo, Yonghui Supermarket and China Resources Vanguard are setting up “green channels” for Chinese exporters which allows them to sell their products in the supermarket, per Cailian reports (link)

Netflix’s Steady As She Goes…A Beacon Of Stability During These Volatile Times

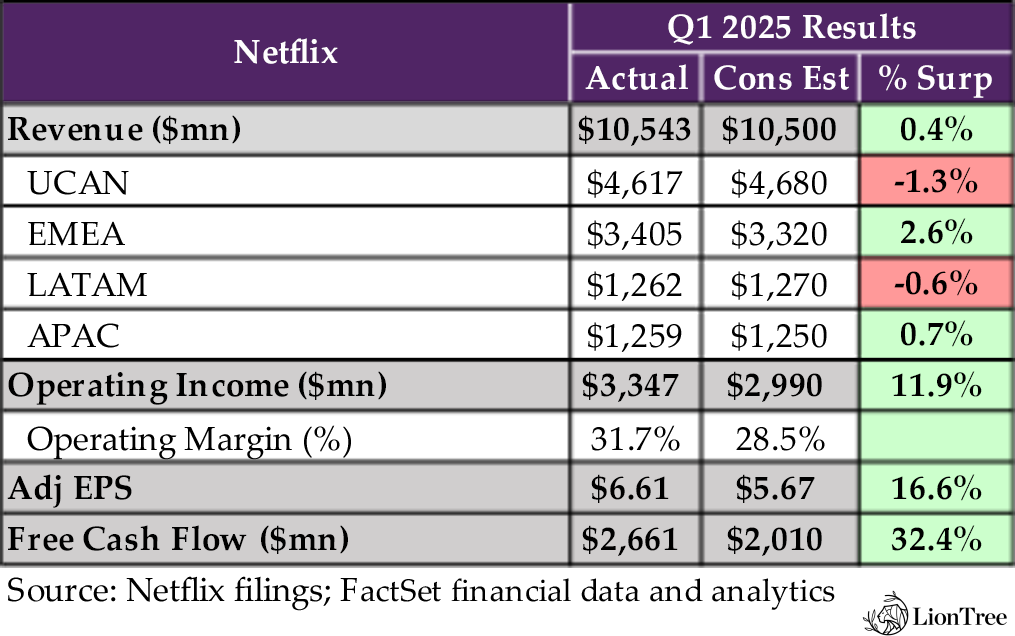

It was a bit of an unusual print post the close on Thursday night ahead of a market holiday on Good Friday, but in the big scheme of things with all the market turmoil and uncertainty, Netflix’s Q1 performance was mostly steady as she goes, which in this environment is a big win. The streaming business has been more resilient than other sub-sectors during challenging periods and it looks like it is shaping up along those lines again as we look into 2025. The Co has not seen any negative consumer impacts from the macro environment, nor any advertising pull-backs (its small scale might also be helping to insulate the Co). This was the first qtr where Netflix stopped disclosing its subscriber numbers, so that is something to get used to, but Q1 itself was solid with slightly better than expected revenue along with much better operating margins. However, the margin upside was solely due to timing as some costs have shifted into H2 given the content slate. The existing FY 2025 revenue and operating margin guidance was reiterated. Notably in the qtr, the Co launched its 1P ad tech suite in Canada and the US, which should help drive more ad adoption and underpin a further ramp in ad revenue growth (the Co should roughly double ad revenue in 2025).

Mgmt didn’t provide any additional color around the WSJ report (link) citing its internal goal to reach a $1T valuation, earn ~$9bn in global ad sales, double its $39bn 2024 revenue, and triple its $10bn 2024 operating income by 2030 other than to sound a bit perturbed that this memo leaked. But it does paint a nice growth picture for years to come.

Overall, Netflix shares have outperformed YTD and likely remain a place where investors will feel comfortable, especially in these uncertain times. See below for our main takeaways from Netflix’s results and conference call.

-> The stock is trading +2.6% after hours after being up +5.7% this week; YTD, the stock is up 9.2%, easily outperforming the market

Solid Q1 Though Expense Timing Boosted Margins In The Qtr / 2025 Guidance Was Reiterated

- Q1 rev decel’d q/q but beat cons by +0.4%: Grew +13% y/y or +16% y/y ex-FX (vs +16% y/y or +19% y/y ex-FX

- Driven primarily by membership growth and higher pricing, partially offset by F/X, net of hedging

- BIG seq step up in Q1 op margin: Easily beat at 31.7% vs cons 28.5% and yr-ago 28% (also up from 22.2% in Q4, 29.6% in Q3 and 27.2% in Q2), driven by rev upside and timing of expense spending

- Q2 rev guidance beat cons by +1.4%: $11.04bn vs cons $10.89bn

- Implies seq accel in growth of +15% y/y or +17% y/y ex-FX

- Will see the full qtr benefit from recent price changes and cont’d growth in membership and ad rev

- Regionally – UCAN rev growth expected to reaccelerate in Q2 (did not specify by how much): Grew +9% y/y in Q1 vs +15% y/y in Q4 due to only a partial qtr impact from price changes, plan mix and the absence of ad rev from the Christmas Day NFL games

- Q2 op margin expected to come in a 33%, an ~6ppts y/y improvement

- REAFFIRMED FY rev and op margin guidance: “No material change to our overall business outlook since our last earnings report”

- Rev guidance range was a tad below cons at midpt: $43.5bn-$44.5bn vs cons $44.25bn

- At current F/X rates (with the recent weakness of the US dollar relative to most other currencies), currently tracking above the mid-point of 2025 rev guidance range

- Assumes “healthy” member growth, higher subscription pricing, and a “rough doubling” of ad rev, partially offset by F/X net of hedging

- Continuing to target 29% op margin for FY and will be lower in H2 due to content expense ramp: Q3 and Q4 tend to have a heavier slate, which in turn will also lead to higher sales and mkting expenses to support the slate

- Rev guidance range was a tad below cons at midpt: $43.5bn-$44.5bn vs cons $44.25bn

Have Not Seen Any Negative Consumer Impacts From The Macro

- Paying close attention to consumer sentiment but based on what they are seeing, there is “nothing significant to note”

- Retention is stable and strong despite the strong Q4 paid net adds

- Have not seen big changes in plan mix

- Most recent price changes have been as expected

- Entertainment has been resilient in tougher economic times and having the low-cost ads plan in their largest markets also provides resilience to the business

- The environment doesn’t change how they think about price increases: The Co has been able to keep a “positive fly wheel” even in challenging environments

- Recent pricing increases have performed “in-line with expectations”: Including in the US, UK, and Argentina

- Announced price increase in France, which is factored into 2025 guidance

Netflix Has Also NOT Seen Softness In Its Advertising Business But Its Small Size Might Be Providing Insulation

- “Keeping a close eye on the marketing place but aren’t currently seeing any signs of softness from their direct interactions with buyers”

- Actually to the opposite “we’re seeing some positive indicators from clients as we approach our upfront event”

- But Netflix’s relatively small size in ads vs the big ad pie “provides some insulation to market shr shifts right now”

- The Co rolled out their proprietary ad tech suite in Canada and US (will roll out in the remaining 10 mkts over the “coming months”), which will open up new demand

- The roll-out thus far has gone well though they are still in the middle of it

- The biggest benefit is enabling more flexibility to how advertisers can buy; An improved buyer experience makes it easier for advertisers to transact

- Overtime, the 1P platform will help with more programmatic availability, provide more enhanced targeting, leverage more data sources, and offer more measurement and reporting capabilities

- Continue to expect to roughly double ad revenue in 2025

The Addressable Market Remains Large & Can Support Future Growth

- Netflix reaches “a minority of their potential addressable market… we believe we’ve got plenty of room to grow our engagement, our revenue and our profit”

- “We’re less than 10% of TV hours for an audience or a connected household’s perspective”

- “We’ve still got hundreds of millions of folks to sign up”

- “And from a revenue perspective, we’re about 6% of consumer spend and ad revenue in the countries we serve in the areas that we serve”

- Going after 80% of TV time that neither Netflix nor YouTube has today…that is an “immediate opportunity”

Content Strategy Remains Consistent

- No incremental comments on appetite for sports content: The live events strategy (sports and non-sports) is unchanged

- Live events is a relatively small part of content spend and only 200bn view hours which is also small, but “not all viewing is equal” and it helps with acquisition and retention

- Intend to grow live outside the US

- WWE RAW is performing well and has been on Netflix’s global Top 10 list every week

- There is a lot of demand for animation, so the Co wants to keep focusing here: They have had some hits and misses but are still learning

- Continue to test new formats

- Licensed four episodes of the toddler learning series Ms. Rachel, which has consistently been in the global Top 10

- Debuted S2 of Inside, a reality show from the Sidemen

- It didn’t sound like the Co has plans to move into short form and USG but that they could expand podcast content

- “The lines between podcasts and talk shows are blurring”

The Co Is Finding Ways To Improve The Member & Creator Experience Via AI

- “There is a ton of excitement on what AI can do for content creators”; Jim Cameron says that movies can be made 50% cheaper and I think there is a bigger opportunity to make movies 10% better”

- Using AI to do set references for previews, VFX sequence prep, shop planning, etc. that makes the process better

- Smaller projects now have access to VFX which they didn’t have before

- AI plays an important role in discovery and recommendations and there is still room to go with this: The buzziest titles drive <1% of viewing so discovery and recommendations “are critical to unlock the value of the content spend”

- Still see more room for improvements

- The Co is testing a new, simpler home page that will be rolled out later this year

- They are also building interactive search based on gen AI

Gaming Is Still A “Multi-Yr Iterative Journey” And A Big LT Oppty

- The Co has learned “quite a bit”

- Focused on what has been working –

- Immersive narrative games based on their IP

- Squid Games Unleashed, one of their biggest games to date, will have an update for the newest season

- Thronglets, which is their Black Mirror based Tamagotchi style game

- Mainstream established titles (like GTA) and will launch more of those

- Games for kids (just annc’d Peppa Pig game)

- Also experimenting w/ socially engaging party games

- Immersive narrative games based on their IP

- Spending levels on gaming will remain measured until they have confidence they will earn a compelling return: It is still a small % of their content budget

- Mgmt still sees this as a large LT oppt

The TMT Sell-Side Scrambles To Factor Business Conditions + Uncertainty Into Company Estimates

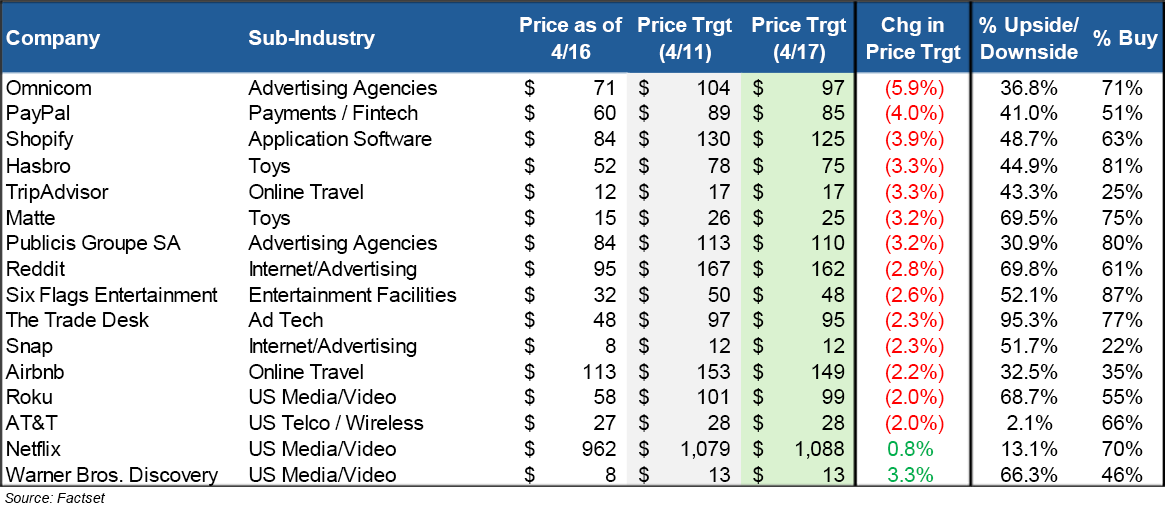

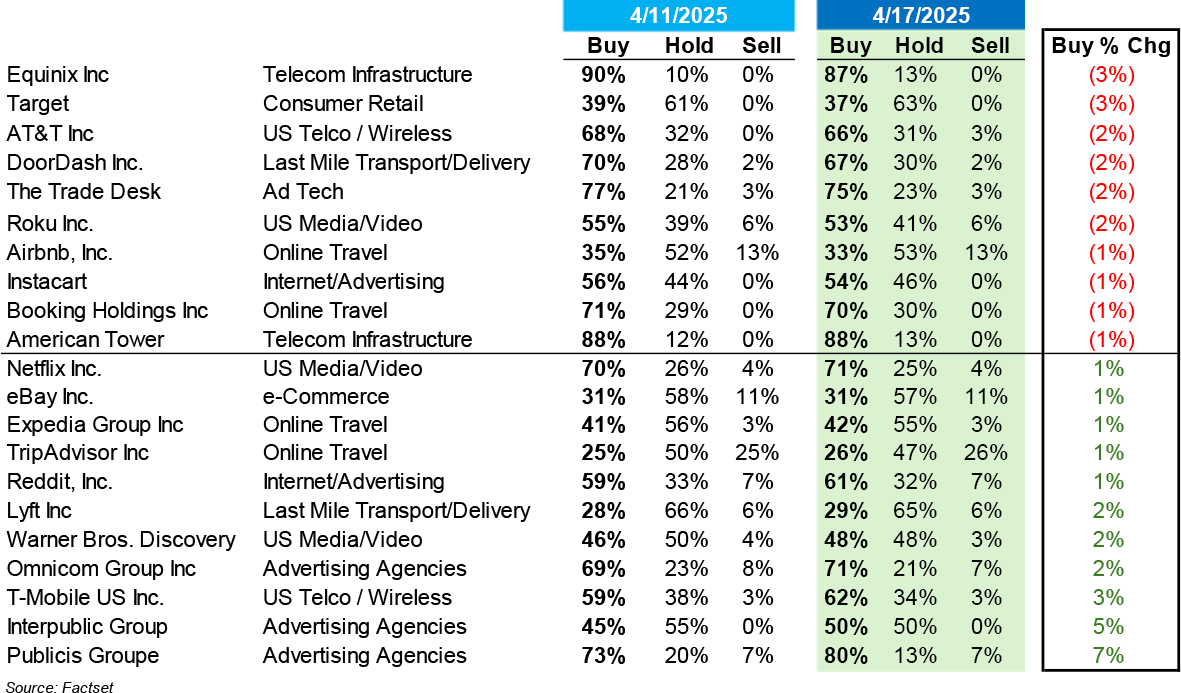

There were what seemed like an avalanche of sell-side analyst price target revisions this week so we decided to take a deeper look into where expectations are being revised down the most and, in limited cases, revised up. Overall, among our LT Universe of TMT/Consumer stocks w/ $1bn market caps and at least 10 analysts covering the stock, 55% were hit with sell side consensus price target cuts over the course of the last week, though there were a handful of price target increases which positively impacted 11% of our Universe.

- A few call outs for the biggest cuts to consensus PTs –

- Omnicom, PayPal, and Shopify topped the list of the largest decreases; Of those, the Street is least bullish on PayPal with only 51% Buy ratings in general

- Which companies saw consensus PT increases?

- Warner Bros Discovery and Netflix were among the limited number to see this trend

- In general, advertising, retail/toys/ecomm, and travel were well represented on the list of largest PT cuts

- What about changes to Buy ratings over the past week? There were not as many changes to ratings as there were for PTs but a few things stood out –

- Equinix and Target had the largest cuts to # of Buy ratings

- A couple of the YTD winners like AT&T and American Tower resulted in some analysts becoming more cautious from here

- Despite the ad agencies’ PT’s being cut over the past week, analysts actually moved more constructive on the group from a ratings perspective

Both Publicis & Omnicom Contend That Brands Still Need To Spend On Advertising Even In Tough Times

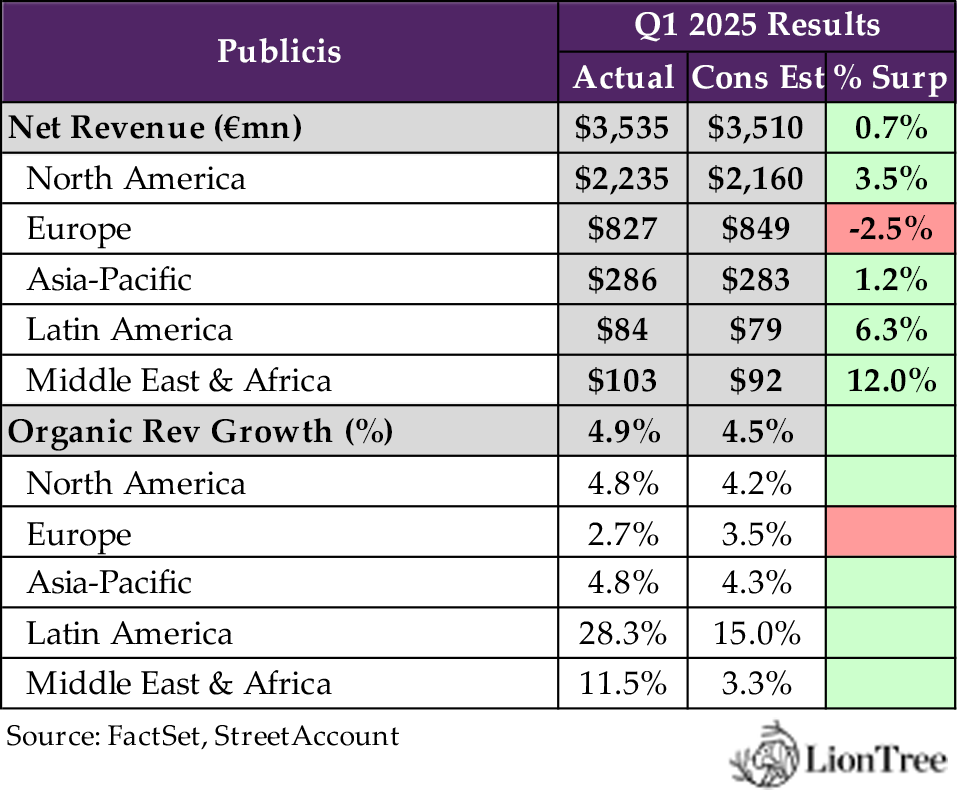

Earnings have begun in the advertising sector with holding Co’s Publicis and Omnicom both reporting results, but with mixed reactions. Publicis’s organic revenue growth rate of +4.9% headily surpassed consensus expectations and even when factoring in uncertainty stemming from macro concerns, mgmt. was highly confident that the Co will hit the full year 2025 organic growth range of +4-5% as new business wins will offset any weakness in other areas. Mgmt highlighted that they have not missed guidance in 5 years which gives investors a level of confidence.

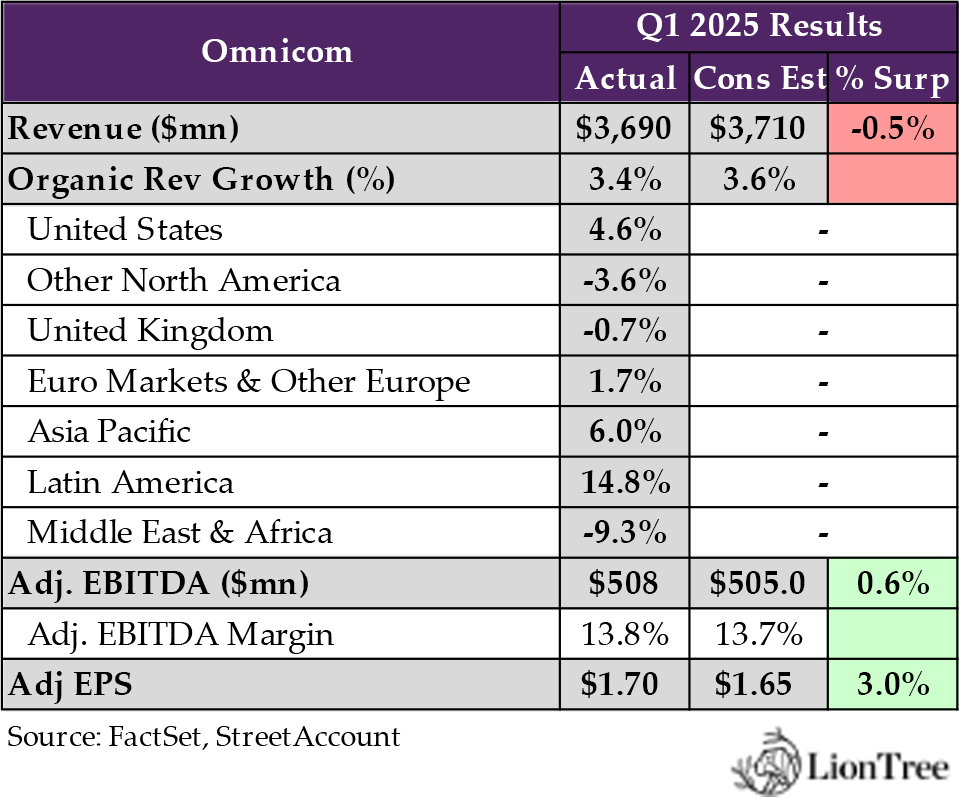

Omnicom, on the other hand, slightly missed Street projections for organic growth (+3.4% vs cons +3.6%) and lowered the bottom end of its FY 2025 organic growth guidance by 1pps to a new range of 2.5-4.5%, to be “conservative”.

Neither Publicis nor Omnicom has seen a pull-back in ad spend at this point and both stress that marketers know they still need to spend in order to support, defend, and grow their brands, even during tough times. But that spend does become more targeted in periods of uncertainty, so the mix could certainly be impacted. With that said, Publicis was also vocal about the “wait & see attitude” with respect to IT consulting spend, which has indeed been impacted.

Lastly, another big catalyst for the sector is the OMC/IPG merger which is still expected to close in H2 of this year. Publicis sees this as an opportunity for new business wins while OMC mgmt dismissed the notion that they will lose clients on the back of the merger and characterized this notion as “nonsense”.

Overall, this is the first of many updates and datapoints regarding overall advertising budgets, and business has not fallen off a cliff. However, we’d expect to hear more examples of where ad spend is being tabled as this macro uncertainty persists.

-> Publicis shares rallied +3.6% in reaction to earnings while OMC fell -6.2% (though during a strong down day in the markets as well); For the week, Publicis shares are up +1.5% while OMC is down -3.1%.

Publicis Lead Upside On Q1 Organic Revenue Growth While Omnicom Slightly Disappoints

- PUB: +4.9% organic growth beat cons +4.5% even with “incr’d macroeconomic tensions” & tough comps: This is an accelerated rate vs the 5 yr CAGR of +4.5%; Currency had a net positive impact of 200bp

- Verticals

- Connected Media (~60% rev): High single digit increase in organic growth

- Intelligent Creativity (~25% of rev): High single digit increase in organic growth

- Technology (~15% of revs): Mid-single digit decline in organic growth

- Regions

- US (63% of net revs): +4.1% organic (+6% ex Sapient) and on the top of +5% y/y last yr

- Europe: +2.7% organic (+5.2% ex Sapient) following +6% in Q1:24

- Asia Pac: +4.8% organic, w/ China +9.3%, largely driven by mkt share gains despite macro uncertainties

- Verticals

- OMC: +3.4% organic growth slightly missed cons 3.6%: Due to strong growth in Media & Advertising and Precision Marketing disciplines (66% of revs combined); FX decr’d reported rev by 1.6% which was less than guidance of 2-2.5%

- Verticals

- Media & Advertising: +7.2%

- Precision Marketing: +5.8%

- Public relations: -4.5%

- Healthcare: -3.2%…working through loss of Pfizer and 1-2 minor accounts

- Branding & Retail commerce: -10%… due to uncertain mkt conditions impacting both new brand launches & rebranding projects and a slowdown in M&A

- Execution & Support: +1.9%

- Experiential: -1.5%

- Verticals

- Regions

- US (~50% of rev): +5%

- Latam: +15%

- Europe was mixed

- Asia Pac saw growth (China was only 2% of rev in 2024)

- Declines UK, ME and Africa

- Adj EBITDA @ 13.8% was a tad ahead of cons 13.7%; Adj EPS beat by +3

Pressure On IT Consulting Has Accelerated But Brands Still Need To Spend Even In Times Of Uncertainty, Though There Could Be Some Pullbacks

- PUB: Seeing a “wait & see attitude” for IT consulting firms BUT have not yet seen pullback in marketing spend budgets as clients need to spend to sustain and win mkt share

- On CAPEX – the “wait & see attitude” that has been reflected in every IT consulting firm, incl Sapient (which is down mid-SDs), has only accelerated due to lack of visibility (i.e., clients are waiting to see if there is more visibility before starting to invest)

- On OPEX (spend on mkting budgets) clients continue to invest b/c they need to sustain and win mkt share but mgmt is confident they can offset any future cuts with new wins

- March was their best month and the Co is still seeing momentum

- It is too early to talk about April but the macro uncertainty is “rising by the day” so there “could be some reduction across some industries through the rest of the year”

- But with the strong Q1 and material new business wins, they are confident to offset potential cuts and hit their guidance

- Clients’ “mood” is “definitely cautious”, but they are also “very competitive”, and are looking for opportunities to grow despite the uncertainty

- “It’s all about being more targeted”…”and being more connected w/in the media to be more efficient, and it’s all about measurement, which makes, again, the role of data so important”

- OMC: Mgmt is “assessing the implication of these events to determine how they will affect our clients and our business” BUT has not seen specific client actions of cuts to spending yet

- Clients are seeking flexibility during these periods of uncertainty but still need to invest in their brands: “In past periods of uncertainty, our clients must continue to compete for share in a dynamic marketplace by investing and leveraging the strength of their brands and increasing and actively expanding their connection with customers”

- But have NOT seen any specific client actions taken to date

- Clients are seeking flexibility during these periods of uncertainty but still need to invest in their brands: “In past periods of uncertainty, our clients must continue to compete for share in a dynamic marketplace by investing and leveraging the strength of their brands and increasing and actively expanding their connection with customers”

- The Advertising media and CRM businesses “remain strong”: “We didn’t change the forecast on those”

- The Events business is more exposed: “If we had doubts, it was really more in the events business, as companies probably get a little bit more conservative”

Despite Potential Headwinds In Spend From Macro, Publicis Remains Confident In Its Current FY Organic Growth Range Guidance While Omnicom Tweaked Down Its Guidance To Be “Conservative”

- PUB: Remains very confident they will hit the FY guidance (4-5% organic growth vs the market avg of < 1%)

- The 4% is a floor: “It factors in the current deteriorating economic landscape, including cuts in marketing spend as a result of the reduced client visibility in the context of US tariffs. But also a negative performance at Publicis Sapient throughout the year in-line with peers expectations”; Also govt contract is <1% of revs at group level

- Having “record business wins” over the period gives confidence in FY guidance: New biz wins contribute 200bp to growth; These will offset any weakness due to macro

- Organic growth could reach 5% if clients regain visibility, leading to fewer cuts in traditional spend and resumption of CapEx spend translating into an improvement of Publicis Sapient performance

- Have strong track record of hitting guidance: “It has been more than 5 years that we haven’t missed a guidance and that we have always delivered the number that we promised”

- Revenue visibility? Putting Sapient (a time and materials business) aside, ~2/3 of their biz is retainer-based and/or with good visibility today

- Mgmt also reiterated a slight increase in margin for 2025 vs 18% in ’24, along with FCF projection of E1.9-2bn

- Also expects a very “homogenous” yr w/ respect to organic rev growth in the 4-5% range for each qtr in the yr

- OMC: Lowered the bottom end of its FY organic growth guidance range by 1ppt to 2.5-4.5% “given the uncertainty of the current environment” though maintained adj EBITDA mrgn guidance of a 10bp incr y/y (from 15.5%): Estimate FX impact on rev to be -0.5% for Q2, -1% for Q3, and flat in Q4, which implies-1% reduction for the full yr 2025

- “We are being conservative in lowering the bottom end”

- Potential new business in Advertising Media and CRM businesses could get them to the top-end of guidance

- “We were planning for a glass that could be half empty, but we’re personally striving for what we really believe and have believed for a long time that we’re optimistic and that it will wind up half full”

OMC/IPG Deal Close Timing Remains On Track & Publicis Expects To Benefit From A Shrinking Competitive Landscape

- OMC/IPG merger remains on track for H2 2025 close

- Received shareholder approval in March

- Received approval from 5 of the 18 jurisdictions in the last 5 wks (incl from China where they had trouble before with the proposed Publicis merger)

- Working through approvals w/Colombia, Brazil, Saudi Arabia, & Egypt (relatively small for the combined businesses)

- Made progress on integration planning work, which will help the Co meet the $750mn run rate cost synergies target following the closing of the proposed transaction

- PUB mgmt believes the Co is “ideally positioned” to seize the opportunities of a shrinking competitive landscape in what is a growing sector

- “This 25% reduction of the competitive landscape is already having a material impact on our client decision on partners and will mechanically benefit us once the deal is completed”

- BUT OMC mgmt views competitor comments about them losing employees and clients as a result of the merger as “nonsense”

- “We have not had any client of any significance that we’re in fear of losing because of the transaction (competitors are perpetuating this “nonsense” that they will lose people and lose account, etc)

- “It’s very disruptive for the client to make a change, and especially in this environment, there will have had to be some underlying strategic reasons why they would go ahead and do that beyond the ones that had started that process already

A Couple Other Notable Comments

- Publicis mgmt. thinks that the sector is “undervalued”: “The marketing service industry we belong to is undervalued, despite the resilience showed during COVID and its ability to grow faster than GDP in the last year”

- OMC resumed its buyback

- After pausing share repurchases until the shareholder vote on March 18th, expect to continue buybacks for the rest of the yr; For 2025, expect to return to an annual repurchase level of ~ $600mn

'Meta Vs FTC' Enters The Ring... While New Tech Regulatory Actions Also Emerge

The antitrust dispute between Meta and the Federal Trade Commission (FTC) officially kicked off on Monday (April 14th) with a non-stop stream of updates. Over the course of the next several weeks, Chief Judge James Boasberg of the DC District Court will decide whether Meta unlawfully maintained a monopoly in the market for “personal social networking services” by acquiring Instagram and WhatsApp.

Originally filed in late 2020, the FTC’s case was dismissed at first but revived after the agency submitted a more detailed complaint outlining Meta’s alleged anticompetitive behavior. This stage of the proceedings focuses on whether Meta violated antitrust laws. If Judge Boasberg rules in the FTC’s favor, a later phase will address potential remedies—most notably, the agency’s push to force Meta to divest Instagram and WhatsApp.

Separately, but related, the trial also comes the same week a Virginia court ruled that Google violated antitrust law in the ad tech market, which was also a key regulatory development along with Google now facing a £5bn lawsuit in the UK for abusing “near-total dominance” in the online search mkt.

See below for the highlights that came out of Week 1 of the trial. (link/link/link/link)

A Quick Refresher On How The Trial Came About

- Dec 2020 – FTC filed an initial antitrust lawsuit against Meta (then Facebook), alleging the company engaged in anticompetitive conduct

- Jun 2021 – Judge James Boasberg dismisses the case, stating the FTC failed to present enough evidence to prove Facebook holds market power

- Aug 2021 – FTC files an amended complaint, adding more detailed data on Meta’s user base and market positioning relative to competitors like Snapchat, Google+, and Myspace

- Jan 2022 – Judge Boasberg allows the case to proceed, noting the FTC had now “cleared the pleading bar” and could move into discovery

- Apr 2023 – Meta files a motion to dismiss the case again, seeking to avoid a full trial

- Nov 2023 – Judge Boasberg denies Meta’s motion, allowing the case to go to trial

- However, he dismisses one FTC claim — that Meta restricted third-party developer access to maintain dominance

A Drilldown On What Happened In This Week 1

- What is the FTC arguing? Meta abused its powers and acted as a monopoly by acquiring rivals to remove them as competitors

- “Acquiring these competitive threats has enabled Facebook to sustain its dominance—to the detriment of competition and users—not by competing on the merits, but by avoiding competition,” the FTC said in a legal filing

- The result, the FTC is arguing, has been lower-quality social media apps for consumers, as Meta prioritizes preserving its power and boosting its profits above all else

- What is Meta arguing?

- Meta is NOT a monopoly b/c it has never raised prices on consumers, noting that all of its major apps are free

- Meta’s svs have evolved from being focused on friends and family connections to “more of a broad discovery-entertainment space”

- Meta purchased Instagram and WhatsApp “to improve and grow them” and the quality of Meta’s apps “has improved on every objective measure”, pointing out Meta’s user growth over the years

- Instagram grew far larger than Zuckerberg ever imagined: At the time of the deal in 2012, Zuckerberg hoped to grow Instagram from 10mn to 100mn users – it reached 1bn in 2018; Had Meta not bought Instagram, Zuckerberg says, “it’s very hard to know” how things would have turned out, which is a key challenge for the FTC to address

- Meta is arguing that people use more of something when it becomes better, “that’s economics 101”

- Zuckerberg argued that the FTC’s case involves the “incoherent parsing of competition” to make the case that Meta is dominant, but is deploying a social media market definition it created that excludes TikTok, YouTube and Apple’s iMessage

- The FTC has NOT included TikTok or YouTube in the market where it says Meta has a monopoly, arguing that they are broadcast platforms rather than networks for connecting with friends and family

- With TikTok and YouTube included, Meta’s share of the market drops below 30%, Meta has argued

- And TikTok, in particular, slowed Meta’s growth “dramatically,” per Zuckerberg

- What acquisitions are under the spotlight?

- Purchase of Instagram for $1bn in 2012 (Before acquiring Instagram in 2012, Zuckerberg wrote in an internal email he sought to “neutralize a potential competitor”)

- Purchase of WhatsApp for $19bn in 2014 (Ahead of Meta purchasing WhatsApp, in 2014, Zuckerberg wrote an email saying the messaging service represents “a big risk for us”)

- What is the outcome the FTC is looking for? If the FTC prevails, Meta could be forced to break up its $1.3 trillion advertising business through possible spinoffs of Instagram and WhatsApp

- Prior to the trial kickoff, there were negotiation talks to settle, but they ultimately failed (link)

- In late March, Zuckerberg called the head of the FTC and offered $450mn to settle

- But that was far less than the FTC’s $30bn demand and a fraction of the value of Instagram and WhatsApp

- On the call, Zuckerberg reportedly sounded confident that Trump would back him up with the FTC, as he’s been developing closer ties to Trump (Meta donated $1mn to Trump’s inauguration and settled a $25mn lawsuit)

- FTC Chairman Andrew Ferguson found the offer not credible, and wasn’t ready to settle for anything less than $18bn and a consent decree barring Meta from anticompetitive practices

- As the trial approached, Meta upped its offer to close to $1bn, which was ultimately not accepted and led to the kicking off of the trial

- Prior to the trial kickoff, there were negotiation talks to settle, but they ultimately failed (link)

- Timeline: The trial is expected to last several weeks and it could be months before a ruling is issued

Some Other Interesting Revelations Were Flagged At Trial

- Meta offered to buy Snap for $6bn back in 2013, but the offer was rejected (link)

- In court, Zuckerberg said “for what it’s worth, I think if we would have bought them, we would have accelerated their growth, but that’s just speculation”

- In 2018, Zuckerberg considered spinning out Instagram due to concerns over the rising threat of antitrust litigation against Facebook, according to an email that was presented during the trial

- “And I’m beginning to wonder whether spinning Instagram out is the only structure that will accomplish a number of important goals,” Zuckerberg wrote in the email

- “As calls to break up the big tech companies grow, there is a non-trivial chance that we will be forced to spin out Instagram and perhaps WhatsApp in the next 5-10 years anyway. This is one more factor we should consider”

- Zuckerberg also wrote that, ”while most companies resist break-ups, the corporate history is that most companies actually perform better after they’ve been split up”

- In 2022, Zuckerberg proposed “wiping” everyone’s Facebook friends to boost the platform’s relevance (link/link)

- He thought that if everyone’s friend lists were deleted and they had to “start again”, it could get them to engage more with the platform.

- Zuckerberg felt that Facebook’s “cultural relevance is decreasing quickly”, and he proposed starting the plan with a smaller country and seeing how it went

- Others at Meta, including the head of Facebook, Tom Alison, pushed back on the plan, and ultimately, the strategy was never implemented.

- Meta has considered creating an all-ad feed on Instagram (link)

- Zuckerberg suggested that Meta has contemplated introducing a feed consisting entirely of ads.

- “I think we have discussed it at different points but I don’t think we have done it,” he said.

Also There Was Another Big Antitrust Ruling In Big Tech This Week… Google Was Found Guilty Of Breaching Antitrust Law In AdTech (link/link)

- A court in Virginia ruled that Google had violated antitrust law by “willfully acquiring and maintaining monopoly power” for the sale of ads on independent websites across the internet

- In its case, the govt argued that Google leveraged its dual role in the market to inflate prices and edge out competitors

- Google may be compelled to break up significant portions of its advertising technology business — specifically the tools it uses to control both the buying of ads by advertisers and the selling of ad space by publishers

- The ruling was the second time in a year that a US federal court had found that Google had acted illegally to maintain its dominance (link): Another federal judge ruled in August that the company had a monopoly in online search and is now considering a request by the Justice Department to break the Co up

- ALSO, across the pond, Google is facing a £5bn lawsuit in the UK for abusing “near-total dominance” in the online search mkt to drive up prices (link): The UK Competition Appeal Tribunal filed a class action lawsuit alleging that Google used its market position to limit the ability of rival search engines to compete, which is turn strengthened strengthening its own position in the online search advertising market

- Google called the case “yet another speculative and opportunistic case” and said that it plans to “argue against it vigorously.”

Global Media Usage Is Expected To Take A Dip In 2025

Also noteworthy this week were a couple of updates on consumer media usage and viewership stats that we thought were worth highlighting. First, PQ Media published a report forecasting that after a rebound in 2024 due to the elections and summer Olympics, global consumer media usage is expected to slightly decline by -0.3% in 2025, which would be the first decline since the 2009 Recession. Below we outlined some of the other key trends and expectations from this report. (link)

Also related, based on Nielsen’s March 2025 The Gauge report, The Roku Channel took the top spot among free ad-supported streaming TV services in the US with 2.2% of all streaming activity for the period. Tubi secured 1.9% shr and while Pluto TV used to take <1% shr, the services is now bundled with Paramount+ and, combined, accounts for 2.3% shr of all streaming activity. More broadly, YouTube maintains its position as the leader across all streaming platforms, accounting for 12% viewership. (link)

PQ Media Forecasts The 1st Decline In Media Usage Since The 2009 Repression

- Global consumer media usage (digital and linear media channels) ROSE +2.4% in 2024 to an avg 57.2 hrs per wk, which is a rebound from a sharp decline in 2023 due to Federal elections in 15 of the top 20 mkts and the summer Olympics in France

- Digital media usage incr’d from 37.3% share in 2023 -> 39.7% in 2024 (now accounts for 50%+ of consumption in 11 of the top 20 mkts)

- BUT expected global consumer media usage to DECLINE -0.3% in 2025, the first since the 2009 Recession…

- Consumption has reached saturation in major developed markets like the US

- Expect deceleration in discretionary spending on media devices and content in 2025

- Possible recession due to tariff wars

- …And then tick up again in 2026

- Media usage is expected to rise in even years (elections, major international sporting events) and decline in odd years (fewer elections, less impactful sports events)

- Given the new AI-generation who have been intro’d to digital media at an earlier age, the firm anticipates the use of linear media platforms & channels will continue to decline at a more rapid rate each yr

- Other 2024 global media consumption stats –

- The avg global consumer spent 8.17 hrs/day w/ media in 2024, up from 7.36 hrs in 2019 (in some markets, such as Japan and the Netherlands, daily media usage exceeded 12 hrs/day)

- Ad-supported media accounted for 52.7% of time spent in 2024, down from 55.5% in 2019

- Men used media more than women globally at 58.29 hrs/wk vs. 57.02, respectively

- The Greatest Generation (born before 1945) used media the most @ 98.37 hrs/wk, while the m-Gen used media the least @ 31.73 hrs/wk

- Mobile video posted the highest gain of the 22 digital channels that PQ Media monitors, up 16.7% in 2024, while OTT (including VoD, PPV and DVR) viewing is the most used digital channel at 8.77 hrs/wk

AI Chatbot Momentum Continues / US Startup Funding Hits Highest Levels Since 2021 / Lyft Enters Europe With FREENOW Acq

- Continued strong adoption of AI chatbots

- Alibaba’s Quark is now China’s Top AI app, surpassing ByteDance’s Doubao, DeepSeek (link/link)

- Quark has ~150mn MAUs worldwide, followed by ByteDance’s Doubao w/ ~100mn and DeepSeek with ~77mn, according to Aicpb.com, which tracks the popularity of AI products

- In March, Alibaba restructured Quark, powered by the Co’s Qwen reasoning models, which are designed to think before responding to queries, making them very good at complex tasks; Alibaba said it could help with academic research, document drafting, image generation, and more

- A separate report released in early March by VC firm Andreessen Horowitz ranked Quark as the 6th-most popular AI app globally by MAU, just behind Baidu’s AI Search and trailing OpenAI’s ChatGPT and Microsoft’s AI-enhanced Edge browser

- ChatGPT has likely hit between 800mn-1bn users – “doubled in just weeks,” per OpenAI CEO Sam Altman (link/link)

- At a TED Conference, when asked about how many users are on the platform, Altman had said ““I think the last time we said was 500 million weekly actives, and it is growing very rapidly”

- TED curator Chris Andersen then said “You told me that it like doubled in just a few weeks” to which Altman said “I said that privately, but I guess…That’s ok, no problem. It’s growing very fast”

- Altman followed that by saying “something like 10% of the world uses our systems, now a lot,” which would bring the number closer to 800mn users

- Much of that growth has been in the last several months, with the release of several products that have gone viral, including its March 25 introduction of a new image generation feature which creates images and videos in various styles

- Alibaba’s Quark is now China’s Top AI app, surpassing ByteDance’s Doubao, DeepSeek (link/link)

-> Separately, but related, there has been strong speculation that OpenAI is working on its own X-like social network; While the project is still in early stages, reports suggest that an internal prototype focused on ChatGPT’s image generation that has a social feed (link/link)

- US startup funding hits highest level since 2021, per Pitchbook (link)

- US startups raised $91.5bn in Q1:25, up +116% y/y to the highest level since Q4:21

- For the second straight qtr, investments in AI startups made up more than half of total funding, rising to a record 71% in Q1

- BUT while investments rose, # of deals fell 25% to 3,003 as more money went into fewer very large rounds including –

- Anthropic’s $4.5bn raise

- AI chipmaker Groq’s $1.5bn financing

- OpenAI’s planned $40bn funding (has reportedly raised $10bn of that through a SoftBank-led round from investors including Thrive Capital, Microsoft, Altimeter Capital Management and Coatue Management)

- Lyft enters the European market through acquisition of taxi app FREENOW for $200mn (link/link)

- Founded in 2009, FREENOW is a ride-hailing platform headquartered in Germany and has been jointly owned by German automotive Cos BMW and Mercedes-Benz since 2019

- The app is available in 150+ cities across 9 countries, including Ireland, the UK, Germany and France

- Beyond traditional taxi and ride-hailing services, FREENOW also offers other mobility options including e-scooters, e-mopeds and e-bikes

- There will be no immediate changes to FREENOW’s customer experience, but “over time, new benefits will be made available to FREENOW drivers and riders”

- Once combined, the 2 Cos will serve 50mn+ combined annual users

- The transaction is expected to close in H2:25

- The acquisition is Lyft’s most significant expansion outside N. America, nearly doubling Lyft’s TAM to 300bn+ personal vehicle trips per year and increasing annualized Gross Bookings by ~€1bn

- Up to this point, Lyft has only operated in the US and Canada

- Founded in 2009, FREENOW is a ride-hailing platform headquartered in Germany and has been jointly owned by German automotive Cos BMW and Mercedes-Benz since 2019

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- In 2024, Google utilized AI to suspend 39.2mn ad accounts, tripling the prior yr’s figures, tackling fraud via biz impersonation and fake payment details. 50+LLM updates boosted safety measures, cutting deepfake ad reports by 90%. India saw 2.9mn account suspensions for financial svs, trademark misuse, and gambling. Globally, Google blocked 5.1bn ads, removed 1.3bn pages, and verified 8,900 election advertisers (TechCrunch)

Artificial Intelligence/Machine Learning

- OpenAI is reportedly in discussions to acquire Windsurf for ~$3bn, aiming to enhance its AI tech capabilities and expand its biz portfolio. This move aligns w/ OpenAI’s strategy to strengthen its position in the competitive AI landscape. The deal, if finalized, could mark a significant milestone in the AI industry, reflecting the growing demand for advanced AI solutions. (Bloomberg)

- The Trump administration is considering banning Americans from accessing DeepSeek’s AI models and restricting its purchase of Nvidia AI chips, aiming to limit China’s access to US tech. DeepSeek’s competitive pricing has pressured Silicon Valley to lower costs, but allegations of IP theft and ties to the Chinese government have raised concerns. The next steps remain uncertain (TechCrunch)

- OpenAI has introduced a new safety-focused reasoning monitor for its latest AI models, o3 and o4-mini, to prevent misuse related to biological and chemical threats. The monitor, custom-trained on OpenAI’s content policies, blocks risky prompts 98.7% of the time, based on internal tests. OpenAI plans to continue human monitoring alongside automated systems to mitigate risks effectively (TechCrunch)

- The US House Select Committee on China is investigating Nvidia’s alleged role in aiding DeepSeek’s AI chip development, focusing on whether restricted H20 chips were sold indirectly via Singapore. DeepSeek reportedly trained its AI models using ~60,000 Nvidia chips, including 20,000 restricted units. The probe highlights concerns over export controls and China’s growing AI capabilities. (Business Insider)

- Perplexity is reportedly in talks to integrate its AI assistant into Samsung and Motorola phones, aiming to expand its presence in the mobile tech ecosystem. This move could enhance user experience by offering advanced AI capabilities directly on devices, positioning Perplexity as a competitor to established virtual assistants like Google Assistant and Siri. (Bloomberg)

- OpenAI has unveiled its latest AI models, o3 and o4-mini, which can “think with images,” analyzing and reasoning with visual data like sketches and diagrams. The o3 model is optimized for math, coding, science, and image understanding, while o4-mini offers faster performance at a lower cost. Both models are available to ChatGPT Plus, Pro, and Team customers (CNBC)

- Microsoft’s Copilot Studio introduced “computer use” for AI agents, allowing them to interact w/ websites & apps, akin to OpenAI’s Operator. Cos can build AI agents for automating tasks like data entry, mkts research, or invoice processing. The tool detects screen changes to avoid breaking. Consumer Copilot’s “Actions” lets agents book tickets, make purchases, etc., but is limited to partners. (The Verge)

- OpenAI is reportedly exploring its own AI-driven social network, focusing on image generation tools like ChatGPT’s capabilities. The project, still in early stages, may launch as a standalone app or integrate w/ ChatGPT. The network could provide OpenAI w/ real-time data to enhance AI systems and expand its biz (Social Media Today)

- OpenAI has updated its Preparedness Framework, stating it may adjust safety requirements if rival labs release high-risk AI systems without comparable safeguards. The Co emphasizes rigorous risk assessment before adjustments, ensuring safeguards remain protective. The framework also introduces automated evaluations to accelerate development. Critics argue OpenAI prioritizes speed over safety, raising concerns about its testing processes (TechCrunch)

- Google has expanded access to its Veo 2 AI video generation tool, enabling users to create 8-second clips from text prompts in 720p cinematic quality. Integrated w/ Whisk, Veo 2 allows dynamic animations from text and image prompts. The tool enhances realism and motion accuracy but faces challenges in avoiding overly polished or unrealistic depictions. (Social Media Today)

- Grok, Elon Musk’s chatbot from xAI, has introduced Grok Studio, a canvas-like tool for creating and editing docs and basic apps. Available to free and paid users, it supports code execution, Google Drive integration, and dynamic previews for HTML, Python, C++, and JavaScript. Grok Studio aims to enhance collaboration and content creation, competing w/ similar tools like OpenAI’s Canvas and Anthropic’s Artifacts (TechCrunch)

- Alibaba-backed AI startup Zhipu plans to go public this yr, aiming to raise ~$1bn. Zhipu, known for its AI agent AutoLM Rumination, has seen rapid growth, w/ nearly 150mn monthly active users. The IPO will help Zhipu expand its tech capabilities and global reach. The Co has secured $69mn in Series D funding, following a $137mn round, and is valued at $2.74bn. Zhipu’s IPO comes amid heightened interest in AI and competition from giants like Tencent and ByteDance. (Analytics India Magazine)

- Apple plans to analyze user data on devices to enhance its AI tech while maintaining privacy. The Co will use differential privacy, a method that identifies trends without collecting data linked to individual users. This approach will improve AI features like image generation, text creation, and object recognition. Apple aims to balance innovation w/ privacy protection, ensuring user data is anonymized and secure. The initiative is part of Apple’s broader strategy to advance AI capabilities. (Bloomberg )

- OpenAI has launched GPT-4. 1, GPT-4.1 mini, and GPT-4.1 nano, optimized for coding and instruction following. GPT-4.1 excels in real-world software engineering tasks, w/ a 1mn-token context window. It outperforms GPT-4o and GPT-4o mini on coding benchmarks like SWE-bench. GPT-4.1 nano is the fastest and cheapest model, ideal for low latency tasks. These models aim to create an “agentic software engineer” capable of end-to-end app development. (TechCrunch )

- Meta will resume AI training using public content from European users, which was paused last year due to privacy concerns. The Co will use public posts and comments from adult users in the EU to train its AI models. Meta assures that private messages won’t be used and users can object to their data being used. This move follows the launch of Meta AI assistant in Europe and aims to enhance AI capabilities while complying w/ EU privacy laws. (Associated Press)

- The race to expand large language models (LLMs) beyond the million-token threshold has ignited debate in the AI community. Models like MiniMax-Text-01 (4mn tokens) and Gemini 1.5 Pro (2mn tokens) promise game-changing applications, analyzing entire codebases, legal contracts, or research papers in one go. However, the biz case for these models is questioned, as larger context windows may not always translate to real-world value. (VentureBeat )

Audio/Music/Podcast

- AI-generated music now makes up 18% of all tracks uploaded to Deezer, reflecting the growing influence of AI in the music industry. Deezer is exploring ways to identify and label AI-generated content to ensure transparency for listeners. This trend highlights the increasing role of AI in creative fields, raising questions about originality and copyright (Reuters)

Broadcast/Cable Networks

- Warner Bros Discovery has decided against selling its Polish network TVN. Following a strategic review, WBD management concluded that retaining ownership of TVN is the best path forward. TVN, which includes news networks TVN24 and TVN24BiS, is highly profitable and a key part of WBD’s international biz. The decision comes amid geopolitical concerns and the Polish government’s classification of TVN as a “strategic company” that cannot be sold without approval. (Deadline )

Cable/Pay-TV/Wireless

- Altice France reported a 14% EBITDA decline in Q4, driven by a 20% rev drop in its biz division. The Co’s overall rev fell 6.5% to €1.2bn, impacted by mkts challenges and reduced svs demand. Despite adj cost measures, the Co faces pressure in its tech and telecom sectors. Altice plans strategic investments to stabilize performance and enhance svs offerings, aiming for long-term growth (Telecompaper)

- Ericsson CEO Borje Ekholm emphasized that a financially stronger Vodafone Idea would enhance competitiveness in India’s telecom mkts. He praised the Indian government’s equity conversion in Vodafone Idea as a positive step for stability. Ericsson plans to leverage India’s growing wireless connectivity demand, focusing on 5G monetization, Fixed Wireless Access, and enterprise manufacturing use cases. India remains Ericsson’s largest employee base w/ 22,500 staff (TelecomTalk)

Cloud/DataCenters/IT Infrastructure

- Elliott Investment Management has acquired a $1.5bn stake in HP Enterprise, signaling confidence in the Co’s long-term growth potential. The move aligns w/ Elliott’s strategy of investing in undervalued tech cos. HP Enterprise plans to leverage the investment to expand its cloud svs and AI capabilities, aiming to strengthen its position in global mkts. (Bloomberg)

- Applied Digital missed its quarterly rev estimates due to clients delaying data center renewals. The Co reported $43.3mn in rev for Q1 2025, below the expected $51.92mn. The net loss widened to $62.8mn from $7.3mn a yr earlier, impacted by power disruptions at its Ellendale facility in Jan. 2025. The Co anticipates operating capacity to reach 65%-75% by May. Applied Digital is addressing internal control weaknesses to improve financial reporting. (Reuters )

Crypto/Blockchain/web3/NFTs

- China is evaluating approaches to manage confiscated crypto assets from criminal cases, considering whether to auction or destroy them. This debate reflects challenges in regulating digital currencies, balancing legal frameworks, and preventing misuse. Authorities strive to develop clear policies for seized assets, ensuring transparency and alignment w/ international standards (Reuters)

- Webull’s stock surged 375%, its second trading day after completing a SPAC merger w/ SK Growth Opportunities Corp. The rally boosted Webull’s market cap to ~$30bn. Founded in 2016, Webull gained traction in the US during the Covid pandemic, competing w/ Robinhood, Charles Schwab, and E-Trade. The platform has 23mn registered users globally, offering stock, ETF, and cryptocurrency trading. Webull’s premium tier costs $40/yr and provides real-time data. (CNBC )

Cybersecurity/Security

- Hertz has experienced a data breach due to vulnerabilities in Cleo’s file transfer software, exploited by the Clop ransomware gang. The breach, which occurred in Dec. 2024, affected 59 companies, including Hertz. Clop has threatened to publish the stolen data unless ransom negotiations begin by Friday. Cleo has since patched the vulnerabilities and urged clients to update their software. (The Verge)

eCommerce/Social Commerce/Retail

- Retail sales in Mar saw a 1.4% rise, surpassing the 1.2% forecast, marking the largest monthly increase since Jan 2023. Excluding autos, sales grew 0.5%, beating the 0.3% estimate. Auto-related sales surged 5.3%, while sporting goods rose 2.4%, building materials climbed 3.3%, and food svs increased 1.8%. Gasoline stations reported a 2.5% decline due to falling prices. (CNBC)

- Indonesia’s e-commerce mkts are projected to exceed $46bn by 2025, driven by a doubling of internet users to 215mn and rapid digital adoption. The sector has grown from $1.7bn a decade ago, making Indonesia the third-largest e-commerce mkts in Asia after China and India. Challenges include high logistics costs, but local cos are leveraging infrastructure to enhance efficiency and accessibility. (Inside Retail Asia)

- Chinese e-commerce cos Temu and Shein have cut back US ad budgets and plan price hikes due to new tariffs ending tax exemptions. Temu reduced ad spend by 31% across Meta, X, and YouTube, while Shein’s fell 19% in early Apr. Tariffs on low-value packages now cover 90% of their value or $75-$150, underscoring the broader impact of trade disputes. (Financial Times)

- Proposed cuts to the Supplemental Nutrition Assistance Program (SNAP) could slash funding by $230bn over the next decade, impacting low-income shoppers and retailers. At least 11 states have proposed restrictions on SNAP purchases, such as banning soda and candy. SNAP accounts for ~$112.8bn or 4% of U.S. food spending, with beneficiaries spending 20% more on groceries than non-SNAP shoppers. (CNBC)

- March retail sales grew moderately, up 0. 6% month-over-month and 4.75% year-over-year, as consumers stocked up ahead of tariff hikes. Core retail sales rose 0.4% month-over-month and 5.07% year-over-year. Despite strong economic fundamentals, tariff uncertainty weakened consumer sentiment, shifting disposable income to savings. (Chain Store Age)

- Temu has pulled its US Google Shopping ads as of April 9, 2025, leading to a sharp drop in its App Store ranking from the top 5 to 58th within three days. This decision coincides with heightened US tariffs on Chinese imports, which have risen to 125%. Temu’s business model, reliant on heavily subsidized orders from its parent company PDD Holdings, faces challenges due to these tariffs and tightened import rules. The move has temporarily reduced digital advertising costs for other e-commerce advertisers (Search Engine Land)

- Investors have criticized Shein’s upcoming IPO, which could see its valuation cut from £50bn to ~£40bn ($50bn) due to US tariff changes and supply chain concerns. The Trump administration’s decision to end the “de minimis” duty exemption may impact Shein’s profitability and lead to price increases in its largest mkt. Human rights campaigners have also attempted to block the IPO over alleged links to forced labor. The UK regulator has yet to decide on Shein’s listing application. (Retail Gazette)

- Mytheresa has signed an agreement to acquire 100% of the share capital of YOOX NET-A-PORTER (YNAP) from Richemont, aiming to create a leading global multi-brand digital luxury group. The transaction includes a €555mn cash position and a €100mn revolving credit facility provided by Richemont. The acquisition will integrate YNAP’s luxury division into Mytheresa, forming one group with three distinct storefronts: MYTHERESA, NET-A-PORTER, and MR PORTER. The deal is expected to close in H1 2025. (Retail Gazette)

Film/Studio/Content/IP/Talent

- Netflix’s Welsh productions have contributed £200mn to the UK economy since 2020, including the upcoming film Havoc, directed by Gareth Evans. Wales has become a key hub for Netflix, hosting iconic shows like Sex Education and The Crown. Productions have supported ~500 Welsh cos and created trainee roles, boosting local talent. For every £1 spent by Netflix in Wales, an additional 80p is generated across the supply chain (Advanced Television)

Last Mile Transportation/Delivery

- Uber has opened its interest list in Atlanta for those wanting to use Waymo driverless vehicles. Joining the list increases chances of being matched w/ a robotaxi when the service launches this summer. Riders can join the list via the Uber app and will pay standard Uber rates. (CNET )

Macro Updates

- Global consumer media usage rose 2. 4% in 2024, averaging 57.2hrs/week, driven by federal elections in 15 of the top-20 mkts and the Summer Olympics in France. Digital media’s share grew to 39.7%, up from 37.3% in 2023, with 11 of the top-20 mkts seeing digital media surpass 50% of total consumption. However, 2025 is projected to see a 0.3% decline due to inflation, recession fears, and peaked digital device penetration in developed mkts. (Advanced Television)

- US banks have flagged risks to consumer spending amid tariff policy uncertainties, highlighting potential impacts on economic growth. Concerns include inflationary pressures from tariffs on imported goods and reduced purchasing power for households. Banks are closely monitoring these developments, emphasizing the need for strategic adjustments to navigate the evolving economic landscape. (Reuters)

- China’s Q1 economic growth is projected to slow to 4. 5% in 2025, with US tariffs posing significant challenges to exports, corporate investments, and household consumption. Analysts expect policymakers to introduce stimulus measures, including fiscal spending and rate cuts, to counteract the impact. Despite a 5% growth target, trade tensions and a protracted property crisis may hinder economic recovery, highlighting vulnerabilities in China’s domestic and global mkts (Reuters)

- The “Silicon Six” tech giants—Amazon, Apple, Google, Microsoft, Facebook, and Netflix—have been accused of avoiding ~$278bn in US corporation taxes over the past decade. The Fair Tax Foundation’s report highlights that these cos have inflated their tax payments by shifting profits to low-tax jurisdictions. The analysis suggests that substantive tax avoidance is embedded in these multinationals, calling for a root-and-branch reform of international tax rules to address the issue. (The Guardian )

- US Treasury Secretary Scott Bessent stated that the Treasury has a “big toolkit” to support the bond mkt if needed. Bessent emphasized the Treasury’s readiness to intervene to stabilize mkts amid economic uncertainties. He highlighted the importance of maintaining liquidity and confidence in the financial system. Bessent also mentioned potential measures, including bond buybacks and enhanced communication strategies, to address mkt volatility. (Bloomberg )

- Former Treasury Secretary Janet Yellen stated that the recent selloff in Treasuries signals a worrying drop in confidence in US economic policy rather than market dysfunction. Yellen emphasized that while liquidity hasn’t completely dried up, the pattern suggests a loss of confidence in American policymaking. She believes this situation doesn’t warrant Federal Reserve intervention but highlights the need for robust economic strategies to restore confidence. (Bloomberg )

Regulatory

- Temu and Shein have seen a surge in US sales ahead of new tariffs on small parcels from China, which will end tax exemptions for goods valued under $800. The tariffs, set to take effect on May 2, have prompted both companies to adjust their strategies, including price increases and reduced ad spending. (Bloomberg)

- A group of US businesses is suing over Trump-era tariffs, claiming they’re illegal under the IEEPA, which they argue doesn’t allow unilateral action without a true emergency. Filed by Liberty Justice Center, the suit says only Congress can impose tariffs. A similar challenge was filed by another group in Florida. (CNN)

- The UK has suspended import tariffs on 89 products, including pasta, fruit juices, and agave syrup, until Jul 2027. This move, part of the Plan for Change, aims to save UK businesses £17mn annually and reduce costs for consumers. The suspension applies to goods not covered by free trade agreements, supporting economic growth and easing cost-of-living pressures. The government is also negotiating new trade deals to open mkts and lower biz costs (Just Food)

Satellite/Space

- AST SpaceMobile is reportedly at the center of takeover rumors, sparking interest in the satellite tech sector. The Co, known for its direct-to-cell svs, has partnerships w/ major telecom operators like Verizon & AT&T. (Moomoo)

- AT&T briefly teased its satellite service, developed w/ AST SpaceMobile, before pulling the announcement, hinting at a launch soon. The service aims to provide satellite texting this yr & voice support by late 2026. AST SpaceMobile plans to launch 45-60 satellites by 2026 to enable texting, calling, & data. The initiative targets areas w/o land-based network signals, focusing on connectivity for first responders & select devices during initial testing (PhoneArena)

- SpaceX is launching rockets every 2. 38 days in 2025, boosting Starlink’s speed and reliability w/ over 7,000 satellites in space. As of Apr. 12, SpaceX completed 41 launches this yr, including 39 Falcon 9 missions and 2 Starship flights. Starlink’s recent Falcon 9 launch on Apr. 12 carried 21 Starlink V2 Mini satellites, marking the 400th flight-proven booster mission. Starlink now serves 5mn subscribers across 125 countries, transforming connectivity in remote areas. (Cord Cutters News)

Social/Digital Media

- Threads continues to show strong growth momentum, reaching 320mn monthly active users since its launch in Jul 2023, with projections to exceed 400mn users this yr. In contrast, X has added only 50mn users in the past yr, totaling 600mn active users. Bluesky, while growing steadily, remains far behind at 35mn users. (Social Media Today)

- Pinterest has explored acquisitions to bolster its ad biz, targeting cos w/ tech that enhances ad personalization and measurement. The Co aims to compete w/ Meta and Google by integrating AI-driven tools for better user engagement and ad performance. While no major deals have been finalized, Pinterest’s strategy reflects its ambition to expand its presence in the digital ad mkts. (The Information)

- A federal judge in Ohio has struck down the Social Media Parental Notification Act, which required platforms to verify users’ ages and obtain parental consent for those under 16. The law was challenged by NetChoice, a tech industry group, on grounds that it violated First and Fourteenth Amendment protections. The court issued a permanent injunction, marking another win for NetChoice in its fight against similar laws nationwide. (Bloomberg Law)

- WPP has won the $30mn L’Oreal Groupe influencer account, consolidating influencer activity for all 32 brands in Australia and New Zealand under WPP’s new Beauty Tech Labs. This bespoke agency will leverage talent, tech, and expertise from WPP’s network, including Wavemaker, GroupM, and Ogilvy PR. The collaboration aims to drive innovation and enhance brand strategies, helping L’Oreal connect w/ diverse communities and strengthen its position as a leader in the beauty industry. (Mumbrella )

Software

- Japan’s Fair Trade Commission has ordered Google to cease certain practices deemed anticompetitive under the Antimonopoly Act. The investigation, initiated on Oct 23, 2023, revealed Google allegedly required Android manufacturers to prioritize its search engine, preinstall Google Search and Chrome, and restrict changes to Chrome’s default settings. Financial incentives were reportedly offered to exclude rival services. Google has yet to comment (Yahoo Finance)

- Figma, valued at ~$20bn, has filed confidentially for an IPO amidst Wall Street volatility. This IPO may gauge investor sentiment in tech mkts as cos face economic uncertainty and shifting valuations. Analysts suggest Figma’s move could pave the way for other tech cos contemplating public offerings (Fortune)

Sports/Sports Betting

- DAZN has rejected the LFP’s proposal to terminate their €400mn/yr five-year Ligue 1 domestic rights deal after just one season. The LFP sought €140mn for the current season and €125mn in compensation, but DAZN cited unmet obligations, including piracy control and promotion. Mediation failed, and legal action looms, with the next meeting set for Apr.30. (SportsPro)

- The average MLB team is valued at $2. 62bn, with the New York Yankees leading at $8bn, followed by the Los Angeles Dodgers at $5.8bn. The Yankees generated $705mn in rev for 2024, the highest in MLB, while the Dodgers earned $701mn. MLB’s avg enterprise value-to-sales multiple is 6.4, lower than the NFL (10.1) and NBA (11.9). Revenue headwinds include the decline of regional sports networks and national TV rights concerns. (CNBC)

- MLS has introduced Sunday Night Soccer in its 30th season, aiming to expand visibility w/ fans. While the Apple TV deal offers global access w/o blackouts, some MLS executives advocate for more linear TV exposure, citing broader audience reach. The league’s current Fox deal airs 34 matches annually, including playoffs. MLS may adjust its schedule post-2026 World Cup to align w/ international soccer (Cord Cutters News)

- Netflix’s acquisition of WWE broadcasting rights has significantly boosted UK engagement for flagship shows RAW and SmackDown. RAW saw a 34% rise in Q1 2025 engagement compared to Q4 2024, while SmackDown increased by 40%. WrestleMania 41, airing Apr.19-20, has an addressable UK audience of 35.8mn. The deal has expanded WWE’s discoverable audience, highlighting the growing popularity of wrestling content (Advanced Television)

- The 2025 WNBA Draft, featuring Paige Bueckers as the No. 1 pick by the Dallas Wings, drew 1.25mn viewers on ESPN, marking the second-highest viewership in league history. However, this figure is down 49% from last yr’s record 2.45mn viewers, driven by Caitlin Clark’s popularity. Despite the drop, the draft saw a 119% increase compared to 2023, reflecting growing interest in women’s basketball (Front Office Sports)