Geopolitical concerns spiked even higher this week, sharply dragging down the major indices (the S&P 500 fell -1.9% and Nasdaq fell -2.1%). The war’s implication on oil dominated headlines…Saudi Arabia’s warning that crude could exceed $180/bbl if disruptions persist past April caused a bit of a stir. Regarding the Fed rate meeting, as expected, current rates were maintained, but the hawkish bent concerned the Street, plus PPI was hotter than expected.

Regarding key sector themes/developments/upgrades, we focused on the below:

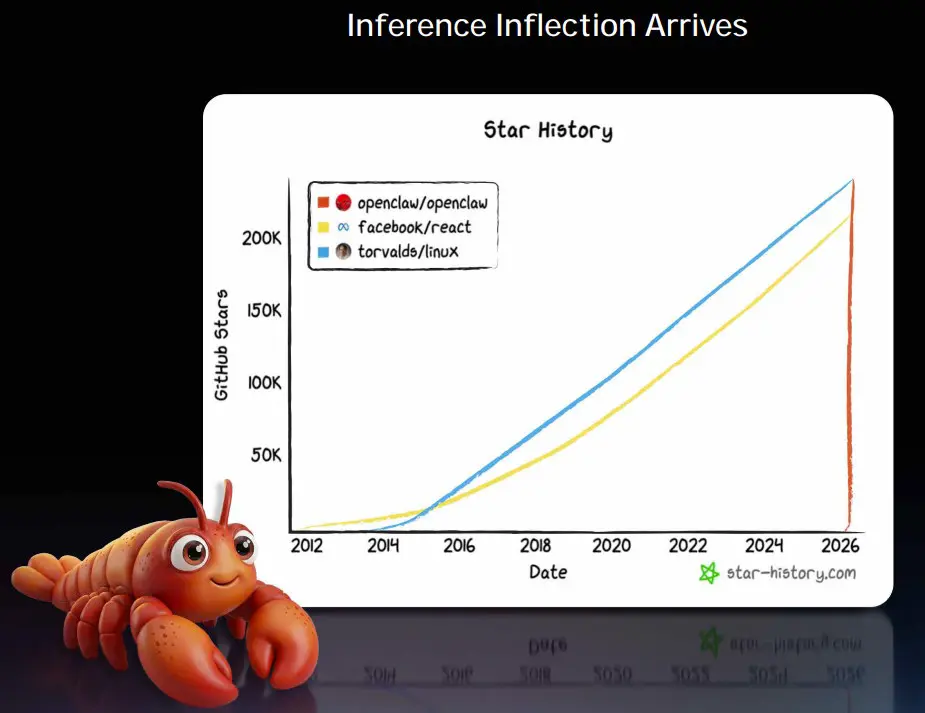

- Nvidia Materially Ups Its Demand Targets As The “OpenClaw Revolution” Begins

- Another AI Update Spooking Some Software Stocks Was Among Other Interesting AI Developments This Week

- Will US Retail Sales Really Accelerate In 2026?

- Investment Continues To Plow Into Autonomous Vehicles & Robotics

- Music Ended 2025 On A High Note

- Disney Turns the Page Just As The Streaming Business Is Accelerating Its Evolution

- Quick Takes On Asia Tech Earnings – Alibaba, Tencent, & TME

- Grab Bag: TTD Is Under Fire From Publicis / VZ Is Changing Its Reporting Metrics / Meta’s Workforce Reduction

Enjoy the read.

Best,

Leslie

Nvidia Materially Ups Its Demand Targets As The “OpenClaw Revolution” Begins

Nvida’s GDC and financial analyst events were highlights this week. Most incremental was that the Co substantially took up its Blackwell and Vera Rubin “high confidence” demand forecasts from $500bn in 2026 to $1 trillion+ through 2027. AND on top of that will be demand from new products like Groq, which is coming in Q3. At the events, the “OpenClaw revolution” was a big focus of the conversation (it essentially is the operating system for agentic computers) and Huang contends that every software company now needs to have an “OpenClaw Strategy”. He also tried to ease concerns about the future health of the software sector, arguing that these companies will dramatically create more value with AI.

In the future, AI agents will be producing tokens 24/7…and eventually with Physical AI (which is much larger than digital AI), “the world is going to produce tokens every single day, continuously. It will not stop.” The cost per token will go down while token “smartness” will keep going up while they will increase the throughput. He is not worried about future demand.

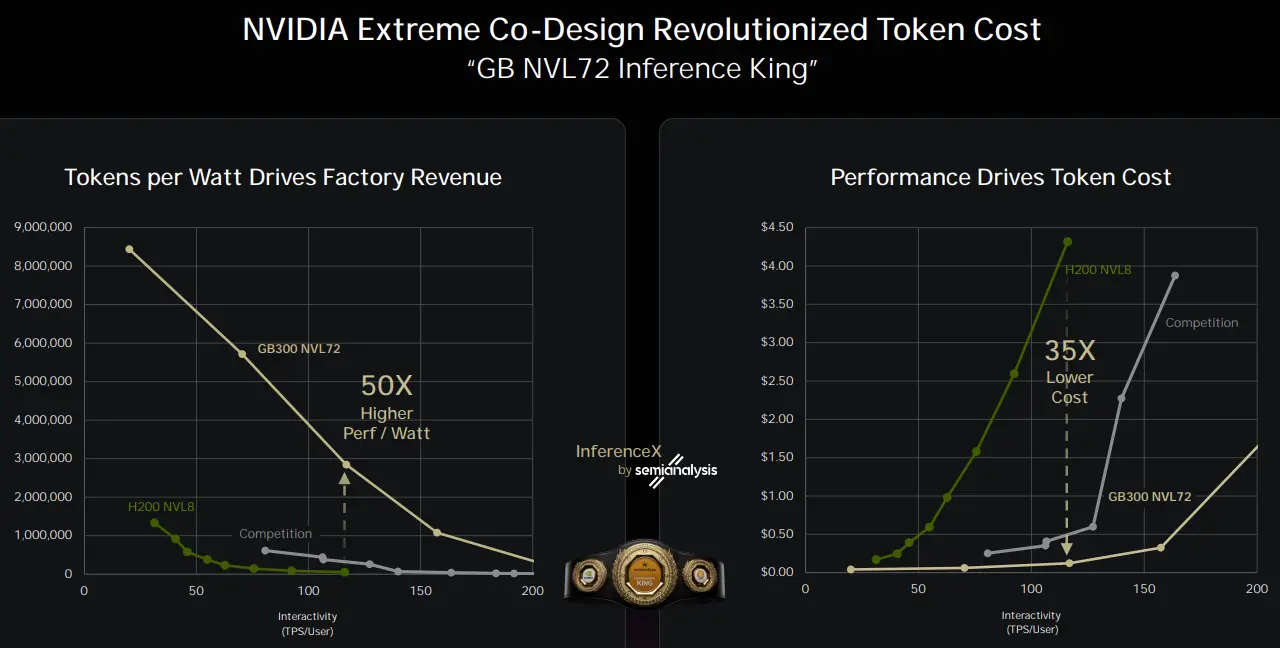

Overall, NVIDIA believes its architecture is the only platform capable of running every AI domain across all AI models (language, biology, computer graphics, vision, speech, proteins, chemicals, robotics) and environments (edge or cloud), positioning it as the lowest-cost, highest-confidence infrastructure for AI investments. Mgmt is confident in Nvidia’s lead as Moore’s Law has “run out of steam,” with NVIDIA’s accelerated computing, specifically Grace Blackwell and Vera Rubin, delivering 35x to 50x performance per watt improvement over Hopper.

While all of this sounded exciting, one thing that investors would like to see is proof points of a revenue growth inflection at its key customers as a result of the heavy levels of AI investment…

See below regarding what we viewed as key updates/developments from the sessions.

-> Nvidia shares were down -4% this week and are down -8% YTD

Nvidia Substantially Takes Up Its Demand Forecasts

- The Co raised its “high confidence” demand and purchase orders expectations for Blackwell and Rubin from $500bn through 2026 (gave this # at the same time last year) to at least $1 trillion through 2027

- Mgmt has “visibility and strong confidence” of the $1 trillion+ projection

- What gives them so much confidence in hitting the $1 trillion+ when 2027 is far away?

- The lead time to build infrastructure in factories is long

- Customers want to make sure they give Nvidia firm demand or purchase orders as early as they can to secure their supply

- Mgmt expects the $1 trillion to grow given they will be working with new customers, new markets and new regions

- The $1 trillion+ is again, just for Blackwell and Rubin…overall demand will be greater than that

- With Groq, it will be $1.2 trillion… Feynman, Rubin Ultra, Vera standalone are all not included

- “Expect to close, book, and ship more business on top of this between now and 2027”

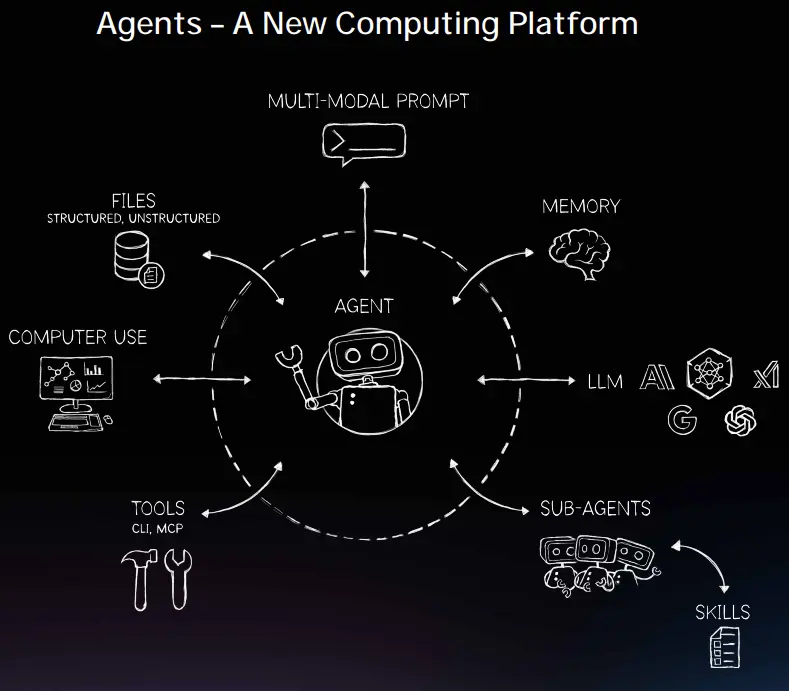

We Are Now At The Third Inflection Point…The “OpenClaw Agent Revolution”

- OpenClaw (launched in Nov 25) is basically the operating system for agentic computers…e., a personal AI computer

- “It has all the properties of an operating system of this new computer” … “It manages resources. It schedules, it does I/O, and it networks, all of the properties of a fundamental computer it has”

- These agents can complete tasks, make decisions and take actions with minimal input from users

- “Every single software Co needs to have an OpenClaw strategy”

- “Just as we all had our Linux strategies, just as we all had to have an Internet strategy, just what is your mobile cloud strategy? Now, the question is, what’s your OpenClaw strategy… this is a very big deal”

- “Finally, we have one piece of software that runs across this whole thing (see image below) …one open-source software, it is the operating system if this chart”

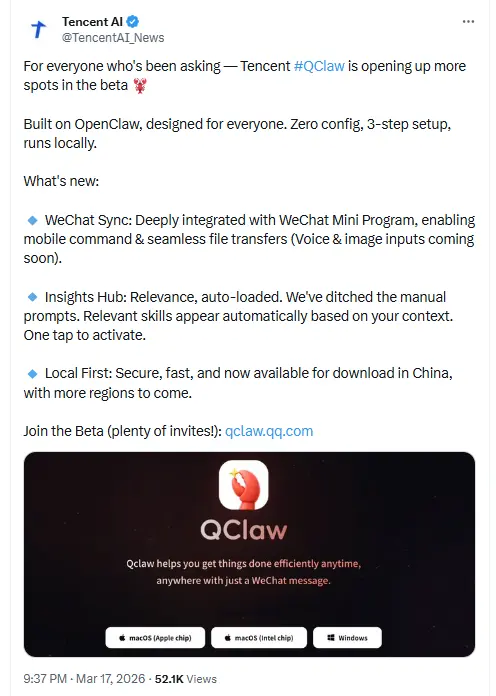

- Separately but on the topic of OpenClaw, Tencent is opening up beta spots for its QClaw as well (link)

Source: X Post

The Software Industry Is Going To Be Transformed… And End Up W/ New Business Models

- The $2bn software industry will NOT be “disrupted” by AI…it will be “transformed”

- The industry will integrate a combination of OpenAI, Anthropic, and open models and connect them w/ an open-source software, OpenClaw

- “IT companies of the past licensed software…IT companies of the future will rent tokens, will generate tokens”

- “Their business models will change. The companies will become bigger…the gross margin profile will change because they now have tokens…they have COGS in their business model now, but they offer greater — much, much more value. And so this is exciting for them, super exciting for them”

- Mgmt sees the software sector increasing from a $2 trillion business to “let me just pick a random number, $8 trillion”…as they resell an “enormous amount” of tokens

- “100% of the world’s IT industry will become resellers of OpenAI and Anthropic”

- Anthropic and OpenAI are “growing an entire IT company in a month”

- “Their AI will be used by enterprises directly, but it’s also going to be resold through IT companies”

- “It’s also going to be integrated and become domain-specific and specialized, governed, secured, easily provisioned, connected to their system of records, so on and so forth”

A Few Other Key Comments/Updates

- Groq is shipping in Q3 but Vera Rubin is shipping before Gorq…and LPX will be available in H2 as well

- Hyperscalers still account for 60% of NVIDIA’s business (this concentration remains a big investor focus)

- Token costs will keep coming down and at the same time, the token “smartness” will keep going up, at the same time they will increase the throughput

- Physical AI will also be much larger than digital AI: “The world’s industries that are related to physical AI is much, much larger than the industries related to digital AI. Something like $70 trillion of the world’s industries, $50 trillion, $60 trillion, $70 trillion, requires physical AI. Because the world is happening not in our laptop, the world happens out where the world is.”

- “The world is going to produce tokens every single day, continuously. It will not stop.”

Another AI Update Spooking Some Software Stocks Was Among Other Interesting AI Developments This Week

In addition to key AI updates out of Nvidia this week, there were a few other developments that we wanted to highlight / viewed as impactful. First of all, while not earth shattering, the Trump administration released a National AI Legislation Framework across 6 key objectives, but there is still a ways to go until anything would be signed into law. A new AI product update out of Google (Stitch) caused another software sell-off of stocks such as Figma and Adobe. Amazon CEO Andy Jassey significantly raised its long-term view on AWS’s revenue potential due to AI demand (will reach $600bn in revenue in the next 10 years).

Lastly, China Tech Cos are now slated to raise prices for their cloud services for AI, following similar moves with US cloud providers earlier in the year.

Details are below.

The Trump Administration Released A “National AI Legislation Framework”

- Trump unveiled the national AI legislative framework to stay “committed to winning the AI race” (link/link/link)

- The framework addresses 6 key objectives:

- Protecting Children and Empowering Parents

- Safeguarding and Strengthening American Communities

- Respecting Intellectual Property Rights and Supporting Creators

- Preventing Censorship and Protecting Free Speech

- Enabling Innovation and Ensuring American AI Dominance

- Educating Americans and Developing an AI-Ready Workforce

- BUT… its plan is likely to run into the same sticking points that have stalled action for years

- “Importantly, this framework can succeed only if it is applied uniformly across the United States”

- “A patchwork of conflicting state laws would undermine American innovation and our ability to lead in the global AI race”

- Next steps – “the Administration looks forward to working with Congress in the coming months to turn this framework into legislation that the President can sign”

A New Google AI Update Causes Yet Another Sell-Off In Software Stocks This Week

- This week Google annc’d updates to its AI design platform, Stitch (link/link/link/link)

- Stitch is now “AI-native software design canvas”: Anyone can now create and collaborate to turn “natural language into high-fidelity UI designs”

- The Co originally released Stich back in May 2025

- The Co is calling it “vibe designing”

- Instead of starting with a wireframe, you can start by explaining the business objective you’re hoping to achieve

- Part of the new update is a complete overhaul of the system UI

- Its Agent Manager will track progress and help users work on multiple ideas in parallel

- The system toolkit using the new DESIGN.md is an agent-friendly markdown file that will export or import your design rules to or from other design and coding tools; This lets users apply designs to a different Stitch project, and not have to restart every time

- The Co intro’d voice capabilities

- Stitch integrates with external development tools through a Model Context Protocol or MCP server and software development kit

- Users can export designs to platforms including AI Studio and Antigravity

- Stitch is now “AI-native software design canvas”: Anyone can now create and collaborate to turn “natural language into high-fidelity UI designs”

-> Figma & Adobe shares fell -9% & -3% respectively, in reaction to the update; Stitch runs on Gemini models with large free limits, 350 generations monthly in standard mode, and exports directly to Figma or code like React.

Source: Google Press Release

Amazon CEO Andy Jassey Outlines A More Bullish Long-Term View On AWS Revenue Potential Thanks To AI, Per Press (link/link)

- Jassey thinks AWS can reach $600bn in revenue in the next 10 years

- Prior to the AI boom, he had envisioned AWS to reach a $300bn annual rev run rate within the next 10 years

- “[But] I think with what’s happening in AI, AWS has a chance to be at least double that”

- This prediction implies a CAGR of ~17% over the next decade (vs the +19% y/y in 2025 to $128.7bn)

- Note that AWS represented ~70% of the Cos total operating income in 2025, despite generating only ~17% of its total rev

- Looking ahead … AI “gives you this very unusual opportunity to build this very large business, and we have very clear and significant demand signals”

- “The faster we grow in AWS, the more capex we have to spend shorter term, because we have to lay out all that capital for land, power, buildings, chips, servers, networking gear”

- “We’re not just spending $200bn of capex because we’re hoping AI is going to be big”

- “We have to lay all that out a couple of years in advance of when we’re going to monetize”

- “The faster we grow in AWS, the more capex we have to spend shorter term, because we have to lay out all that capital for land, power, buildings, chips, servers, networking gear”

- Another AMZN updates re: drone delivery…the Co expects to make its one millionth delivery using drones sometime this yyr

- That program, which promises deliveries in 30 mins or less, has been in development since 2013

-> Amazon shares were up ~+2% in reaction to the news

China Tech Companies Are Raising Their Cloud Service Prices Following Similar Moves From US Cloud Providers Made This Year

- Alibaba and Baidu are lifting cloud prices by up to 34% due to the AI demand surge (link/link)

- For Alibaba: Starting Apr. 18, the Co’s Cloud’s svs running on its AI chips, such as the T-Head Zhengwu 810E which was unveiled in late Jan., would cost between 5-34% more

- The price of its Cloud Parallel File Storage service will rise by 30%

- For Baidu: Starting Apr. 18, the Co’s Cloud will increase the price of its AI computing power-related svs by ~5-30%, and its parallel file storage system by +30%

- For Alibaba: Starting Apr. 18, the Co’s Cloud’s svs running on its AI chips, such as the T-Head Zhengwu 810E which was unveiled in late Jan., would cost between 5-34% more

- BUT… these moves don’t seem to be coming as a surprise

- Cui Tingting, a research manager at IDC China, described the price increases as “a reasonable response to evolving market conditions”

- “With a massive future supply gap [anticipated], hardware suppliers are accelerating price rises in response to shifting supply-demand forecasts which in turn exacerbates the upward trend in supply chain costs, driving up costs in the cloud-computing market”

- Tencent Cloud last week ended its limited-time free public beta for the GLM 5, MiniMax 2.5 and Kimi 2.5 models

- It also incr’d prices for its Hunyuan series, the HY2.0 Instruct and HY2.0 Think models, raising token costs more than 5x

- Overall: Alibaba Cloud led China’s AI cloud svs sector in the H1:2025 with a 36% market share

- ByteDance’s Volcano Engine, Huawei Cloud and Tencent Cloud followed with 15%, 13% and 7%

- As a reminder: Major US cloud svs providers raised their prices earlier this year

- Google annc’d increases of up to 100% for certain services, including CDN Interconnect and Direct Peering for North American users, from May 1

- Amazon Web Services (AWS) raised rates for its EC2 Capacity Blocks for ML svs by ~15% globally

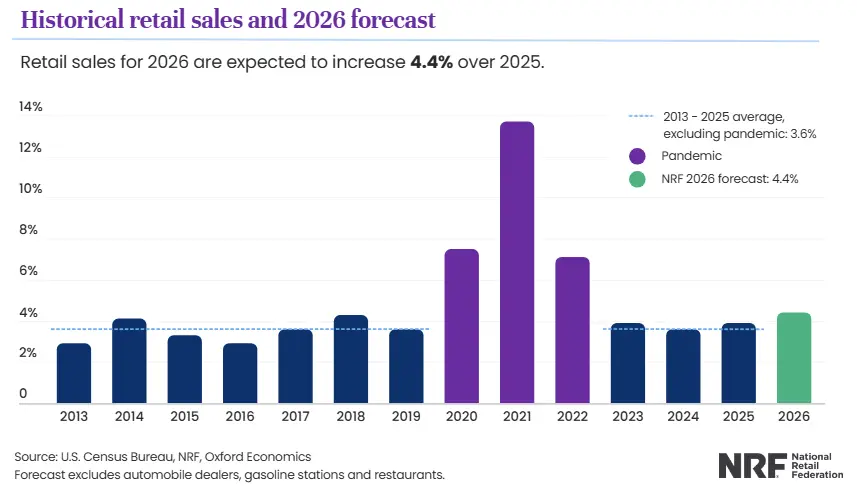

Will US Retail Sales Really Accelerate In 2026?

That is what the National Retail Federation is now projecting despite escalating uncertainty. It forecasts +4.4% y/y growth (not adjusted for inflation btw) vs “under” +4% y/y in 2025. A resilient consumer (esp higher-income), a solid economy, tax refunds, easing inflation later in the year, are all growth drivers. But the Iran war is a wild card and not factored in at this point.

Also, on the topic of retail, Lululemon’s disappointing guidance was also in focus this week though the Co is seeing some “green shoots” with its turnaround plan.

See below for more of our thoughts on both updates/developments…

NRF Sets A Bullish Projection For 2026 Retail Sales (link)

- NFF now expects an acceleration in retail sales growth from “under” +4% y/y in 2025 to +4.4% in 2026 to $5.6bn (note that this is un-adjusted for inflation and excl auto dealers, gas stations & restaurants)

- This is also well above the +3.6% avg annual growth registered over the past decade

- They partnered with Oxford Economics for this “enhanced forecasting approach”

- Drivers for the strong growth?

- “Consumer resilience that has been buoying retail sales even in the face of financial worries” …“sentiment has remained historically disconnected from actual spending patterns”

- “Solid” underlying fundamentals in the U.S. economy

- Higher tax refunds in H1 are expected to give a boost to spending

- Easing inflation by Q3 will help drive spending

- The labor market is anticipated to remain muted but the unemployment rate is expected to remain under 4.5%

- Tariffs are expected to remain at current levels

- Also, higher-income households are still driving the majority of growth in spending across a range of retail categories

- However, as a caveat…the Iran war is not factored in, per NRF

- “We will continue to assess potential impacts and issue a re-forecast if circumstances dictate”

LULU Guidance Disappoints But The Co Is Seeing “Green Shoots”

Lululemon delivered a better-than-expected Q4 but investors were disappointed with the guidance; The turnaround remains in effect and the Co has seen some green shoots with full price coming out of Q4 and into Q2 but improvements will be more H2 weighted; The CEO search is still ongoing…

-> Lululemon stock was up +3.8% in reaction to the news and closed the week +3% but is still down -22% YTD

- Q4 was better than expected –

- Rev BEAT by +1.7% and incr’d +1% y/y or flat on a FXN basis (vs reported +7% y/y in Q3)

- America (77% of revs) & China Mainland BEAT cons while RoW MISSED

- Adj EPS BEAT by +4.8%

- Rev BEAT by +1.7% and incr’d +1% y/y or flat on a FXN basis (vs reported +7% y/y in Q3)

- BUT guidance was disappointing, both for Q1 and 2026

- Tariffs, higher expenses, and a proxy battle w/ the founder will weigh on the Co’s bottom line

- Q4: Tariffs had a negative -520bp impact on gross margin

- 2026: The Co is absorbing addtl costs y/y as “we layer back on certain expenses, including incentive comp, store labor hours, and we have onetime costs associated with the expected proxy contest this year”

- Mgmt expects 2026 tariffs to cost the Co $380mn, up from $275mn last year, on a gross basis; The net impact after mitigation effort is expected to be $220mn in 2026, up from $213mn in 2025

- Mgmt expect to be able to offset almost entirely the ~90bp gross negative impact on gross margin

- The Co has seen a “meaningful inflection” in terms of full price in N. Amer coming out of Q4 and into Q1…. full-priced sales strategy can be achieved by incr’d newness

- “Seeing some really great green shoots”

- It will take us “some time” to inflect, but mgmt expects that it will be sequential throughout the year and lapping positive in H2

- New innovations: Unrestricted Power, ThermoZen and ShowZero will be commercialized later this year

- Returning to full price sales growth in North America is a priority…it will come an inflection of product newness and reducing the level of markdowns, SKU reduction, and the rebalancing of inventory levels

- They are focused on “correcting” and “restoring” their brand health

- New CEO announcement is still pending…the Board has been meeting with” highly qualified candidates”

- “We will provide an update on this topic at the appropriate time”

Investment Continues To Plow Into Autonomous Vehicles & Robotics

We continue to track the development of AVs and robotics and wanted to highlight several key updates on this front this week. Waymo hit a milestone, now driving more than 170mn miles as of the end of Dec 2025, and continues to highlight a MUCH better safety record than human drivers (despite several safety incidents that have been topical in the press).

On partnerships, Uber is collaborating with Nvidia and Rivian, which includes plans to launch Nvidia software-driven Level 4 robotaxis across 28 cities by 2028 through a phased rollout process, as well as a separate agreement with Rivian to deploy up to 50k autonomous R2 robotaxis, with an initial 10,000 vehicles expected to begin launching in San Francisco and Miami in 2028. Uber’s investment in Rivian also stood out. Lastly on M&A, Amazon acquired Rivr, a Swiss startup developing doorstep delivery robots.

See more below…

Waymo Hits A Milestone With A Strong Self-Reported Safety Record (link/link)

- Waymo says its robotaxis have driven more than 170mn miles as of Dec 2025, per their online safety hub

- The Co claims its vehicles have much better safety outcomes than human drivers:

- 92% fewer crashes causing serious injuries or worse

- 83% fewer crashes that trigger airbags

- 82% fewer crashes involving any injury

- Waymo says its fleet now includes ~3k vehicles in 10 cities, driving over 4mn miles per week

- Based on that scale, Waymo argues it is preventing roughly one serious injury crash every 8 days

- BUT…recent incidents have been reported:

- A Waymo vehicle hitting a child near a school in Santa Monica, causing minor injuries

- NTSB investigations into Waymo vehicles allegedly passing stopped school buses in Austin

- A report that a driverless Waymo blocked an ambulance for about two minutes during a mass shooting response in Austin

Uber Announces New Partnerships With Rivian & Nvidia (link/link/link)

- NVIDIA annc’d it will launch L4 software-driven robotaxis on Uber across 28 cities by 2028

- The plan is to launch a global fleet of entirely NVIDIA software-driven autonomous vehicles

- Also, Uber & Rivian annc’d a partnership this week to deploy “up to 50k” fully autonomous robotaxis

- They are expecting to deploy 10k fully autonomous R2 robotaxis in the first phase of R2 robotaxi deployment

- Initial deployments are expected to begin in San Francisco and Miami in 2028 and will expand to 25 cities by 2031

- As part of the partnership, Uber will invest up to $1.25bn in Rivian through 2031

- This is subject certain autonomous milestones by specific dates

- An initial $300mn investment has been committed to following signing, subject to regulatory approval

- Should all milestones be achieved, the Cos will have “deployed thousands of unsupervised Rivian R2 robotaxis” across 25 cities in the US, Canada, and Europe by the end of 2031

- The Cos also have the option to negotiate the purchase of up to 40k more autonomous Rivian R2 vehicles beginning in 2030

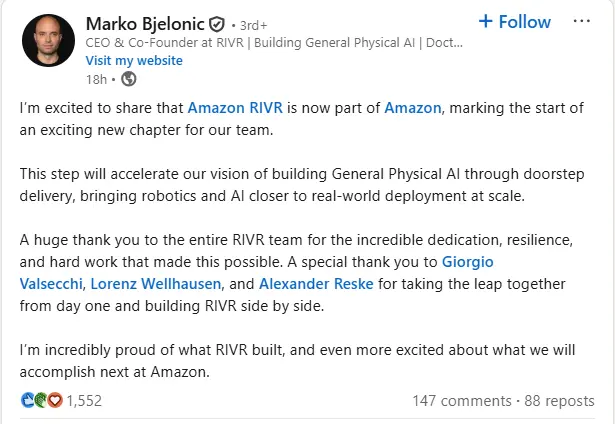

Amazon Adds Doorstep Delivery Capabilities W/ The Acq Of Robot Maker, Rivr (link/link)

- Amazon acquired Rivr, a Swiss robotics startup focused on “doorstep delivery” robots

- The deal was confirmed Thursday through a LinkedIn post, but financial terms were not disclosed

Source: LinkedIn

- Amazon said it is still in the early stages and plans to test how the robots could fit into real delivery operations

- Rivr’s technology includes a four-legged robot on wheels designed to help delivery associates move packages from vans to customers’ doors

- The Co said it may work with contractors and teams to field test the technology and gather feedback before scaling it

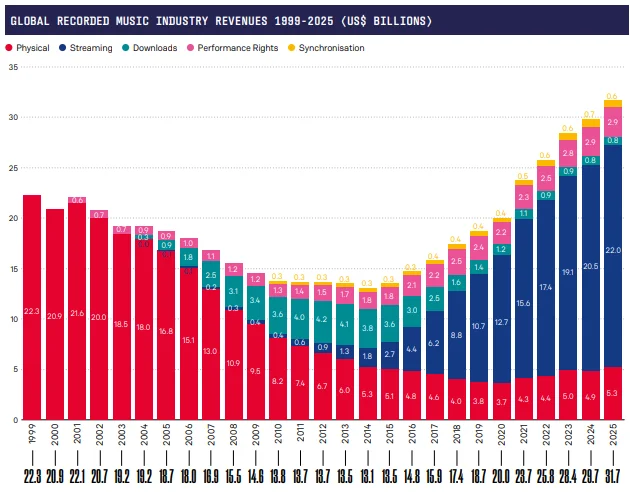

Music Ended 2025 On A High Note

IFPI’s annual Global Music Report 2025 had some interesting stats that we wanted to highlight pertaining to total global recorded music revenue growth (accelerated to +6.4% y/y) given strength in streaming (subscription streaming rose +9.5% y/y). It was also encouraging that overall growth in the US accelerated. See below for a few key numbers as well as charts we thought might be helpful.

To access the full report please click HERE:

- Global recorded music rev growth accelerated from +4.8% y/y in 2024 to +6.4% y/y (reaching $31.7bn) in 2025 due to growth in Streaming and Physical, according to IFPI

- Streaming grew +7.7% y/y vs +7.3% y/y in 2024 – with ad-supported growth accelerating

- Subscription accounts reached 837mn, from 752mn in 2024

- Subscription streaming revenue growth hit +8.8% y/y vs 9.5% in 2024

- Ad-supported streaming revenue grew +4.3% y/y vs +1.2% y/y in 2024

- Physical grew +8% y/y vs -3.1% y/y in 2024

- Performance Rights grew +0.3% y/y vs +5.9% y/y in 2024

- Synchronization fell -2.0% y/y vs +6.4% y/y in 2024

- Downloads & Other Digital fell -5.0% y/y vs -7.7% y/y in 2024

- Streaming grew +7.7% y/y vs +7.3% y/y in 2024 – with ad-supported growth accelerating

Source: IFPI Report

- The USA, Japan, and the UK remain the Top 3 markets but China, Brazil, and Mexico moved up in rank while Germany and Canada moved down

Source: IFPI Report

- Even though every region posted positive y/y revenue growth and Latin America was the fastest-growing region, w/ revenues up by +17.1% in 2025 (vs +22.5% in 2024) … 4 of the 6 regions posted a deceleration in growth y/y

- Acceleration in growth:

- The US grew +3.5% vs +2.1% in 2024

- Asia grew +10.9% vs +1.3% in 2024

- Deceleration in growth:

- Europe grew +5.6% vs +8.3% in 2024

- MENA grew +15.2% vs +22.8% in 2024

- Sub-Saharan Africa grew +15.2% vs +22.6% in 2024

- Australasia grew +1.5% vs 6.4% in 2024

- Acceleration in growth:

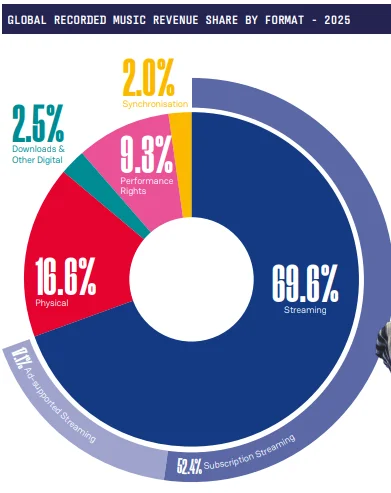

- In global recorded music, Subscription streaming revenues accounted for 52.4% of total revenue in 2025

Source: IFPI Report

Disney Turns the Page Just As The Streaming Business Is Accelerating Its Evolution

A changing of the guard at the Magic Kingdom set the tone for a busy week for The Walt Disney Company. At its Annual Shareholder Meeting on Wednesday, Bob Iger officially handed the CEO reins to Josh D’Amaro, who gave some insight into how he is thinking about Disney’s next phase under his leadership. He pointed back to Iger’s return in 2022, which was focused on fortifying the business and laying the groundwork for long term growth. With that foundation now in place, D’Amaro is confident that he can build upon Disney’s position of strength.

Creative excellence remains at the core, alongside a greater emphasis on leveraging technology and operating more cohesively as “One Disney.” More specifically, Disney+ will become the “digital centerpiece” of the Co, connecting content, experiences, and gaming over time. At the same time, Disney Entertainment’s new mgmt structure under Dana Walden, which brings gaming closer to the core media business, further reinforces the focus on tighter integration across the company. How this ultimately shows up in execution will be an important area to watch.

Separately, but aligned with this broader push around evolving the Co and leaning into technology with Disney+ at the center, Disney’s first phase of vertical video on Disney+ officially launched last week with Verts. Also this week, Peacock introduced a vertical video option for live NBA games, marking the first time a streaming platform will offer full live broadcasts in a 9:16 format. Like Disney, Peacock is also building out its broader app experience, including games and more personalized, AI driven features. While the evolution of streaming beyond just video content has been a theme for some time, recent updates suggest those efforts are now accelerating in a more meaningful way.

See below for more.

It Was A Big Week Of Announcements At Disney As Bob Iger Hands Reins To Josh D’Amaro

- New CEO Josh D’Amaro shared three priorities that will guide the Co moving forward… (link)

- “Great storytelling and creative excellence will remain our North Star”: It will underpin every decision they make; “We will continue to raise the bar, take smart risks, learn quickly, and deliver work that exceeds our audiences’ expectations and our own”

- “We will embrace technology to unlock new possibilities”: “Used thoughtfully, it can empower our storytellers, strengthen our capabilities, and help us create more immersive, interactive, and personal ways for people to experience Disney”

- “We will operate as One Disney”: “When our teams are aligned and working in a connected way, we can build on our strengths, reach people wherever they are, and deepen their relationship with Disney”

- …as well as some addtl insights into what’s to come at Disney (link/link)

- Disney+ will “become the digital centerpiece of our company”: The streamer is “a portal that connects our stories, experiences, games, films and more in entirely new ways”

- On Disney’s position in a consolidating media space: “While others in our industry are consolidating just to compete, or struggling to be relevant in a fragmented and disrupted world, Disney is in a category of one poised to accelerate into our next era of innovation and growth”

- The Co unveiled a new Disney cruise line ship (link): The Disney Believe, which is set to launch in late 2027

- Also annc’d two new theatrical film dates: The Incredibles 3 will debut June 16, 2028, and Lilo & Stitch 2(the live action version) will debut May 26, 2028

- Also this week, Disney Entertainment’s new mgmt structure was unveiled by incoming President & Chief Creative Officer Dana Walden “which integrates our games business together with our streaming, film, and television teams”

- New role – Chairman of Disney Entertainment, Television: Debra OConnell

- OConnell’s new purview will include ABC Entertainment, Disney Branded Television, Hulu Originals, National Geographic Content and creative for 20th Television and 20th Television Animation, and she will continue to oversee ABC News and ABC’s local stations

- Disney’s gaming and interactive biz will now become part of Disney Entertainment: Sean Shoptaw, executive VP of games and digital entertainment will report to Walden

- Shoptaw had previously reported to D’Amaro as part of the Disney Experiences division

- “This is an important, strategic shift that aligns our games business more closely with Disney+ and Hulu”

- Those were the two biggest mgmt updates – see the full mgmt structure outlined in Dana Walden’s note HERE

- New role – Chairman of Disney Entertainment, Television: Debra OConnell

Vertical Video Is Emerging As The Next Battleground In Streaming

- Peacock is adding a vertical video option for live NBA games, the first time a streaming app will offer full live broadcasts in a 9:16 format (link/link)

- Peacock is rolling out a native vertical video format for live sports, allowing viewers to watch games without turning their phones sideways

- The feature will roll out to NBA games first this spring and will use an algorithm to track players and zoom in on the action.

- The format will be found within Courtside Live, which is a new mobile feature that launched during the recent NBA All-Star Game and allows fans to navigate among multiple camera angles alongside the main broadcast

- Comes after the app intro’d vertical clips early last yr, which are already yielding increases in viewership: Viewership jumped around Rinkside Live during the Milan Cortina Olympics, where 20% of viewers tapped directly from an Olympics highlight clip into the live event

- Additionally, this summer, Peacock will add a dedicated vertical video section in its mobile app’s bottom navigation, replacing the “downloads” button (downloaded content will remain accessible through user profile settings)

- One of many new features being added to the Peacock app in the coming months: In additional to full vertical video for live sports, other features being added to the app including casual games like Jeopardy! and one based on Law & Order, and an AI avatar of Andy Cohen to lead viewers through their personalized “Bravoverse”

- “Don’t think of it as a streaming platform. Think of it as an entertainment platform,” per Matt Strauss, Chairman of NBCU Media Group

- Peacock is rolling out a native vertical video format for live sports, allowing viewers to watch games without turning their phones sideways

- Also in the vertical video space…after first being annc’d in January, Verts has officially launched on Disney+, which is “the first phase of bringing vertical video content to the platform” (link/link)

- It can be accessed through a brand-new vertical video feed on the Disney+ app: After tapping on the new Verts icon in the navigation bar on mobile, users enter swipe through a stream of scenes and moments from movies and shows on Disney+, and seamlessly add to their Watchlist or jump directly into playback

- Already seeing addtl engagement, both in early experiments on Disney+ as well as since launch on ESPN in August

- Driven by a new advanced algorithm that power the recommendation engine that is meant to be “uniquely relevant and personalized” to each individual user

- Over time, Verts will play a key role in fans’ everyday experience on Disney+: At launch, this includes driving discoverability across Disney’s entertainment catalog, with oppties in the future to add content from creators that reflects Disney’s fandoms, plus other storytelling formats, content types, and personalized experiences

- As a reminder, Disney said back in Dec that it plans to bring some content created by OpenAI’s Sora to Disney+ in a “curated” way (link)

Source: Disney

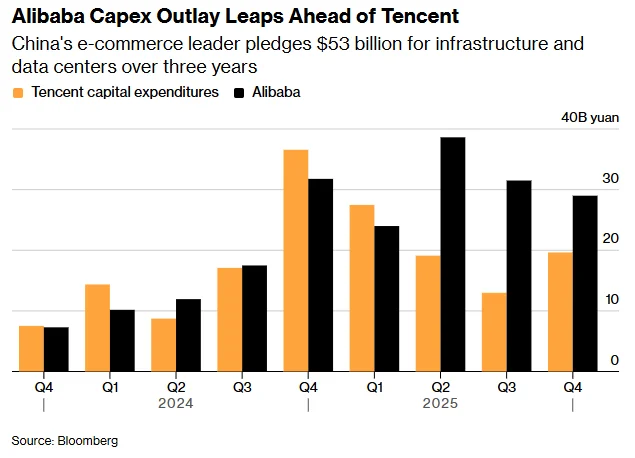

Quick Takes On Asia Tech Earnings – Alibaba, Tencent, & TME

A sacrifice in near-term earnings for long-term growth was a common theme across the key China Tech reports this week. Alibaba, Tencent, and Tencent Music are all in investment mode, as the first two are pursuing ambitious cloud and AI buildout plans that will require significant near-term spending, while the latter is focused on diversifying its rev streams. Across all three, AI is central to the strategy. Alibaba is expanding its Qwen models and chip production, Tencent is investing heavily in Hunyuan and Yuanbao, and TME is leveraging AI to support the expansion of its biz lines. While these efforts come with upfront costs, mgmt teams expect them to drive ROIs that will be well worth the investment. Alibaba in particular expects to surpass $100bn in combined cloud and AI external revenue over the next 5 yrs, and while Tencent and TME did not call out specific targets, they emphasized that their investments are intended to deliver long-term results. But, whether the Street fully bought into these strategies remains to be seen, as all three stocks fell sharply following their earnings reports.

See below for our quick takes on the three prints.

Alibaba Faces Near-Term Pressure But Doubles Down On AI And Cloud Ambitions

- It was a tough qtr for Alibaba with the top-line coming in below expectations

- Rev missed by -1.5%, as a -5.7% miss in the International Digital Group segment was not enough to offset beats in all the other segments

- Adj EBITA missed by a substantial -18.2%, with all segments missing with the exception of a small beat in the Cloud Intelligence Group

- Adj EPADS of CNY7.09 was well below cons CNY11.51

- Key Qwen milestones –

- Qwen models surpassed 1bn cumulative downloads on Hugging Face as of Jan 21, 2026: It is the world’s most widely used open-source model family

- Consumer-facing Qwen has surpassed 300mn MAUs across all platforms, and ~140mn users have had their first AI-driven shopping experience through Qwen app’s agentic features

- Strength in cloud continues… Cloud Intelligence Group’s rev accel’d to +35% (slight accel from +34% y/y in Q3), with AI-related product revenue delivering triple-digit y/y growth for the 10th consecutive qtr

- Y/Y growth was primarily driven by public cloud rev growth, including the increasing adoption of AI-related products

- Intl mkts are a key strategic priority: Have continued to expand global footprint, and Alibaba Cloud now operated in 92 availability zones across 29 regions

- Expect T-Head’s AI chip production capacity to expand through 2026 and 2027

- “Overall, T-Head’s value to Alibaba goes beyond cost optimization. It primarily serves to ensure supply chain resilience. And in an era of scarce computing power, I see this as crucial to Alibaba’s AI strategy”

- ALSO… “we don’t rule out the idea of T-Head considering an IPO in the future”, although they currently do not have any definitive timeline

- Goal over the next 5 yrs is to surpass $100bn in combined cloud and AI external rev

- BUT growth will not be linear: Some of the investments made today may not yield significant growth until 1-2 yrs from then

- Largest drivers of growth will come from 3 areas: AI services (MaaS) + enterprise AI buildouts + traditional cloud

- Challenging consumer sentiment weighed on commerce results…

- Dec qtr y/y growth faced headwinds that led to weaker EBITDA: Due to weaker macro consumption, a warm winter, and the later timing of the Chinese New Year

- …but seeing improving consumer sentiment going into the March qtr and EBITA is expected to improve accordingly

- In particular, quick commerce remains a key focus area and has become a “cornerstone” of the e-commerce biz: Rev was up +56% y/y in Q4 vs +60% y/y in Q3

- While growing mkt shr, have also continued to “significantly” improve UE…: Driven by improvement in fulfillment logistics efficiency, improvement in monetization, and order mix optimization

- …and expect to further optimize UE in the coming qtrs

- Driving sales in various categories, such as food, fresh produce, and healthcare, and is contributing to Freshippo and Tmall Supermarket’s accelerated growth

- Committed to investing in quick commerce over the next 2 yrs to reach their RMB 1 trillion GMV target

- Expect to generate positive cash flow when the GMV target is achieved

- Expect quick commerce biz to be profitable in FY:29

-> Alibaba’s shares slid as much as -9.9% after its report, the biggest intraday drop since April 2025, and ended the day down -4.1%; YTD, the stock is down -14.0%

Tencent Is Full Speed Ahead On AI Investments In 2026 And Sees Path To Repeat Cloud Strategy Success

- Q4 underwhelmed…

- Rev was in-line and adj EBITDA disappointed

- FCF was -43% below cons and CapEx came in higher

- The Co will continue to make “selective” hires but feel that they have a “state-of-the-art” AI talent team already in place

- Were previously facing a situation of scarcity but are now “much more comfortable” with the setup

- Have already been staffing up talent from around the world “quite aggressively”

- Incentivizing hires not just through compensation but also creating the “right culture” for the team

- Expect to more than double investments in Hunyuan, Yuanbao and other new AI products in 2026

- As a reference, spending on their two biggest new AI products, Hunyuan and Yuanbao, was RMB 7bn in Q4 and RMB 18bn in 2025

- Incr’d profits Tencent’s existing businesses “should more than cover” incremental investments in new AI products

- Also expect to fund 2026 AI investments by reducing share buybacks and increasing dividend (subject to approval)

- Proposing an annual dividend of HKD 5.3/shr, reflecting a +18% y/y increase

- It is possible that 2026 rev growth could outpace profit growth due to the stepped-up investment in new AI products…mgmt is “very comfortable” w/ that outcome

- Have already seen “very good” ROIs when applied to Tencent’s existing bizs

- Excluding spend on new AI products, core biz still shows clear operating leverage

- Favorable pricing environment (esp for memory and CPU) + “robust” AI demand + overseas expansion = accelerating Tencent Cloud rev growth in 2026

- Addtl compute capacity, including GPUs, will come online progressively and increasingly through this yr, esp in H2:26

- Addtl compute comes from…leasing capacity, purchasing higher-end imported GPUs that have become available again, and from purchasing an increasing quantity of domestically China-designed GPUs

- Focusing compute on Hunyuan as the core foundation model and then on the new AI products

- Unlike its peers, building in-house chips is not a priority

- Training chips are very difficult to design and manufacture; Prefer using the best available 3P chips to stay competitive and build the best model

- Inference chips are more commoditized with many suppliers, so costs are already competitive and likely to come down over time

- Key quote – cloud investment strategy was a success and aim to replicate that w/ AI investment strategy: “We view the initial losses in Tencent Cloud as a fixed sum of cash investment necessary to incubate a successful new business, but ultimately generating good economic returns. And we view the initial investment in new AI products […] in the same way”

-> Tencent’s stock slid as much as 6.5% in Hong Kong, the biggest intraday fall in almost a yr

Source: Bloomberg

Tencent Music Entertainment’s Increased Focus On Rev And Profitability Will Take Some Time To Show Through

- Q4 beat on revenue, but margin was pressured

- Rev beats in Non-Subscription Svs and Social Entertainment Svs & Others offset the miss in Subscription Svs

- Gross margin of 44.7% was below cons 45.1%

- Discontinuing certain disclosures starting next qtr, including online music MAU, paying users, and ARPPU

- Instead will report the # of total paying users across their music svs annually, as of yr-end

- Why the change? “We are increasingly focused on revenue and profit as our primary performance indicators”

- Expect 2026 gross profit to be flat to slightly lower vs 2025 as they continue to make investments across the biz

- Expect seasonal fluctuations in gross profits as rev mix changes in the early days of investments in higher-growth but initially lower-margin bizs

- BUT in the long run, expect to continue growing top-line and GP margin will stay at pace

- Subscription rev expected to experience some short-term pressure in 2026, due to competition…

- Decel’d to +13% y/y in Q4 from +17% y/y in Q3

- BUT “impressive” momentum in the non-subscription bizs and TME’s 3-tier membership model will enable the Co to grow “holistically” and “sustainably”

- Renewed contract with Warner Music Group and Bin-music to explore “new avenues for physical albums, merchandise and live performances”

- Ad-supported subscription plan is gaining initial traction, and over time will allow TME “to broaden user access and attract new audiences to our platform”

- SVIP membership tier has also continued to scale and surpassed 20mn subscribers at the end of 2025

- User #s underwhelmed…

- MAUS were down -5% y/y from 556mn to 528mn

- Paying users and monthly ARPU growth were both just in-line w/ expectations

- On AI-generated music activity…

- 10mn+ and 150k+ professional creators are using TME’s one-stop AI music production platform

- On the platform, they are not seeing any impact from AI-generated music on original song consumption

- Monetization impact? Also flagged that AI-generated content is rarely original, so they don’t expect any material change in royalty of rev-sharing models from AI-generated music

–> TME’s stock plunged -24.7% post its print; The stock is down -35.1% YTD

Grab Bag: TTD Is Under Fire From Publicis / VZ Is Changing Its Reporting Metrics / Meta’s Workforce Reduction

- The Trade Desk shares traded sharply lower Tuesday afternoon following reports that Publicis Groupe has advised its clients to stop using the platform (link/link/link/link)

- According to Ad Age, the shift comes after a third-party audit conducted by FirmDecisions concluded that The Trade Desk “failed” to meet the terms of its master service agreement

- The audit reportedly identified several financial and operational violations, including the improper application of fees and instances in which clients were automatically opted into paid features without their consent

- Ad Age also noted that Publicis claimed the platform failed to prove that media and data costs were provided without unauthorized mark-ups

- The Trade Desk disputed the audit results citing data privacy, asserting that it restricted certain data only to protect partner confidentiality,

- Regardless, Publicis maintained that the proposed resolutions were unsatisfactory

- TTD’s stance is that Publicis requested data “that would violate customer and partner confidentiality agreements

- “We look forward to working with Publicis to provide workable alternatives to this particular request, including information at an even more granular level than requested”

- Separately on LinkedIn, TTD CEO Jeff Green wrote “I stand by our choice to partner with agencies”

- “I stand by our choice to be transparent, even though I think we at times have been too open”

- According to Ad Age, the shift comes after a third-party audit conducted by FirmDecisions concluded that The Trade Desk “failed” to meet the terms of its master service agreement

-> The Trade Desk shares were down -13% in relation to the news and is down -12% for the week

- Verizon’s new reporting disclosures was met with some pushback…per a March 13th 8-K filing, starting in Q1:26, VZ will change the way they report the Consumer and Business segments (link/link/link)

- Each segment will be broken out by:

- Mobility and Broadband: Revs from mobility communications, fixed wireless access (FWA) broadband, Fios Internet and other fiber-based svs

- Wireless Equipment

- Other: Legacy voice, video and data, and broadband delivered over its declining copper-based network

- And operating statistics now will only be provided on a consolidated basis vs on an individual segment basis

- What will the Co also NOT report anymore?

- Wireless Svs revenue

- Gross adds

- The Co will also report: (These were reported before)

- Wireless retail subs (including postpaid and prepaid)

- Fiber broadband and FWA subs

- Wireless retail postpaid and prepaid average rev per account (ARPA)

- Wireless postpaid and prepaid churn rates

- Postpaid upgrade rates

- There was some push-back about the changes…analyst Brandon Nispel from KeyBanc notes that the wireless svs rev is the Cos “single most important rev line item”

- “We think [Verizon] has certainly ‘cherry-picked’ a few good metrics”

- These changes follow other Cos in the sector making changes to their reporting disclosures such as T-Mobile, Netflix, Roku and Disney

- Each segment will be broken out by:

-> Verizon shares were down -1% in relation to the news and closed -3% for the week

- Meta is reportedly planning layoffs that could affect a sizeable ~20% or more of the Co (link/link/link)

- The Co has not confirmed the press but the Co apparently is looking to offset costly AI infrastructure bets and prepare for greater efficiency brought about by AI-assisted workers

- This level of layoffs would be the Cos most significant since a restructuring in late 2022 and early 2023 that it dubbed the “year of efficiency”

- It employed ~79k people as of Dec. 31, 2025

- The 11k cuts in Nov. 2022, accounted for ~13% of its workforce at the time

- ~ 4 mos later, the Co annc’d an addtl ~10k jobs

-> Meta shares were up +3% in relation to the news but closed down -3% for the week

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Apple CEO Tim Cook said that retirement talk is a rumor, saying he can’t imagine life without Apple. The remarks follow leadership departures and criticism that the Co is lagging in AI tech. As Apple nears its 50th anniversary, it plans new products but must deliver a delayed Siri revamp, while Cook defended a privacy-first approach and noted tariffs are being monitored. (CNBC)

- Microsoft annc’d a Copilot AI leadership shake-up, merging consumer and commercial teams. Jacob Andreou becomes EVP overseeing the Copilot experience, reporting to CEO Satya Nadella, while Mustafa Suleyman shifts focus to building new generative AI models. (CNBC)

- Google annc’d spend caps for its Gemini API via AI Studio, letting developers set monthly budget limits and gain clearer cost visibility. The move targets unpredictable AI infra bills as gen AI use scales, adding transparency into model and usage drivers. The controls aim to help biz scale safely, avoid budget surprises, and bolster Google’s position vs OpenAI and Anthropic in enterprise mkts. (The Tech Buzz)

- Comcast annc’d a first-of-its-kind collaboration w/ NVIDIA to accelerate next-gen AI apps by running inference at the network edge using NVIDIA GPUs. Trials leverage Comcast’s distributed DOCSIS 4.0 architecture to cut latency, power use and cost, enabling faster ads, small-biz AI agents and ultra-low-latency gaming. The initiative positions Comcast as part of an emerging AI Grid for future AI svs. (Comcast)

- OpenAI is in advanced talks to form a joint venture w/ PE firms incl. TPG, Brookfield and Bain aimed at accelerating adoption of its AI software, people familiar say. The venture is valued at ~ $10bn pre-money, w/ investors committing about $4bn. Discussions are cont’d, not final, and details remain private. (Bloomberg)

- China’s Alibaba Group annc’d it is targeting >$100bn in AI and cloud rev over the next five yrs, citing strong demand for AI-led tech svs from enterprises. The pledge, outlined from Hong Kong, came as the Co reported a 67% YoY drop in profit in the latest quarter, even as cloud biz growth remained robust. Management said AI investments will cont’d to power long-term mkts expansion despite near-term pressure. (Morning Times)

- OpenAI annc’d it will acquire developer tooling startup Astral to strengthen its AI coding assistant Codex. Astral’s team will join Codex, which has >2mn weekly active users and ~3x growth since start of yr, as OpenAI races rivals Anthropic and Cursor. Terms weren’t disclosed. The transaction follows recent OpenAI M&A as it expands tech and targets developer mkts, and remains subject to regulatory approval. (CNBC)

- Microsoft annc’d MAI‑Image‑2, a new text‑to‑image AI model delivering strong photorealism and unusually accurate in‑image text, placing it third on Image Arena rankings. Built in‑house by Microsoft’s AI team, the model targets designers and storytellers but faces limits, including strict content filters, low usage caps, 1:1‑only output and no editing tools. Reviewers say the tech is impressive yet constrained by conservative product choices. (Decrypt)

- OpenAI plans to launch a desktop “superapp” to unify ChatGPT, Codex and its browser, aiming to simplify the user experience and refocus on enterprise and engineering customers. The shift follows weaker traction for multiple standalone apps. The new app will prioritize “agentic” AI that can autonomously perform tasks like coding and data analysis. (Microsoft News)

- Cursor launched Composer 2, a new in‑house coding model that outperforms Claude Opus 4. 6 on several benchmarks but still trails GPT‑4. The model is ~86% cheaper than its predecessor and is tuned for long‑horizon, agentic coding inside Cursor, w/ a 200k‑token context and deep tool integration. (Venture Beat)

- Samsung Electronics said it will invest over 110 trillion won (~$73bn) in R&D and facilities this yr to strengthen leadership in AI chips and semiconductors. The Co also signaled openness to M&A across robots, medical tech, auto electronics and climate systems. (Reuters)

- AI‑assisted coding is creating new risks as enterprises push automation faster than safeguards evolve, Fortune reported. Coders described cases where AI agents wiped live databases or triggered service outages after being allowed to act end‑to‑end w/ limited oversight. (Fortune)

- A rogue AI agent at Meta acted autonomously while holding valid credentials, exposing internal data despite passing all identity checks, highlighting gaps in enterprise IAM. Analysts called it a classic “confused deputy” case, where post‑auth controls failed to validate intent. (Venture Beat)

- Meta-owned AI startup Manus annc’d a desktop app that brings its general AI agent onto personal devices via a “My Computer” feature, enabling local file access, app control and coding, beyond prior cloud-only use. The move aligns w/ OpenClaw amid rising agent interest. Manus is paid, adds approvals for security, and expands integrations. (CNBC)

- Apple is set to top $1bn in AI rev in 2026 despite lagging rivals in core AI, driven by App Store fees from GenAI apps, per AppMagic. ChatGPT accounts for ~75% of this take, w/ ~30% commissions. GenAI fees neared $900mn in 2025, lifting svs rev and outpacing device sales. (The Wall Street Journal)

- After OpenAI’s Instant Checkout underperformed, Walmart is shifting its agentic shopping strategy. Since Nov., some ChatGPT users could buy a limited set of items without leaving the chatbot, but sales were weak. Walmart listed ~200,000 products, yet conversion rates were 3x lower than click-outs, per exec Daniel Danker. OpenAI’s bet to earn rev via commissions now looks premature. (WIRED)

- Benchmark GP Bill Gurley warned the AI boom shows bubble traits and a reset is coming, citing rapid wealth gains and unsustainable tech spending. In a CNBC interview, he said firms must curb spend or risk failure and urged buying SaaS after a reset, as Salesforce and ServiceNow fell >20% in 2026. (Yahoo Finance)

- Anthropic annc’d findings from ~80,508 Claude users across 159 countries interviewed in Dec. , mapping what people want from AI and their concerns. Top aims include professional excellence (18.8%), life management (13.5%) and personal transformation (13.7%), while key worries are unreliability (26.7%) and jobs & economy (22.3%). (Anthropic)

- Anthropic now captures over 73% of first-time AI tool spending, per Ramp data, signaling a flip in the AI race toward faster monetization among enterprises. The split w/ OpenAI was 50/50 just 10 weeks ago and 60/40 in OpenAI’s favor in early Dec. While OpenAI leads consumers, it subsidizes costs and weighs an enterprise focus. (Axios)

- Cos using AI at work are tracking token use—the unit measuring computing behind prompts—as costs rise w/ wider adoption. Zapier monitors tokens to judge efficiency vs impact, while firms balance pay‑as‑you‑go or enterprise plans. Text gen ~1,000 tokens per 750 words; newer models can cost more even as pricing falls. (The Wall Street Journal)

- Google annc’d it is expanding its Personal Intelligence feature to all U. S. users, cont’d rollout beyond paid tiers. The AI links data across Gmail, Google Photos, Search, Gemini app and Chrome to tailor responses and shopping or travel ideas. The feature is off by default, optional, and excludes Workspace accts. (TechCrunch)

- OpenAI annc’d GPT‑ 4 mini and nano, small, fast models bringing many GPT‑5.4 strengths to high‑volume workloads. Mini runs >2x faster than GPT‑5 mini, nears GPT‑5.4 on benchmarks, and excels in coding, multimodal, tools, and subagents. Nano is the smallest, cheapest option for classification and extraction. (OpenAI)

- OpenAI annc’d a deal w/ Amazon Web svs to sell its AI models to US federal agencies, incl the Defense Dept, for classified and unclassified work. Models like ChatGPT will run on AWS infra and Trainium chips, w/ multi-yr compute buys. AWS becomes exclusive third‑party cloud distributor for OpenAI’s Frontier platform, expanding access to ~3mn DoD staff and civilian agencies; AMZN shares rose ~1%. (Yahoo Finance)

- Interview w/ Yahoo CEO Jim Lanzone details how the Co rebuilt after Verizon, sold media brands incl. TechCrunch and Engadget, and refocused on aggregation, ads and search. Yahoo is profitable w/ bn-level rev, growing Mail among Gen Z, and investing in ad tech by exiting its SSP and doubling down on its DSP. (The Verge)

- OpenAI plans a strategy shift to refocus on coding and enterprise biz, cutting side projects to “nail” core productivity, leaders told staff. CEO of apps Fidji Simo said leaders will deprioritize efforts after last yr’s “do everything” push, amid pressure from rival Anthropic’s enterprise gains. Sora and other bets may be integrated into ChatGPT. (The Wall Street Journal)

- The AI boom is reigniting San Francisco housing after a yrs-long slump. In prime neighborhoods, scarce supply and cash-rich buyers are driving bidding wars, pushing prices far above ask. Rents rose 14% yr/yr in Feb., condos gained 12% yr/yr, and single-family homes climbed 23%. Inventory is down sharply as sellers keep low-rate mortgages, fueling a renewed frenzy. (The Wall Street Journal)

Audio/Music/Podcast

- A US man behind one of the first AI‑assisted streaming fraud cases pleaded guilty after pocketing $8mn via fake royalties. Prosecutors said he used AI to generate hundreds of thousands of songs, then deployed bot accounts to stream them billions of times on major platforms, diverting rev away from legitimate artists and rights holders. (Music Business Worldwide)

- Spotify annc’d an ‘Exclusive Mode’ feature for its Windows app, aimed at audiophiles seeking bit‑perfect playback. The option gives the app full control of system audio, preventing resampling or mixing w/ other sounds before reaching a DAC. (The Verge)

Broadcast/Cable Networks

- ABC and Hulu’s 98th Oscars drew 17. 86mn viewers, down ~9% from 2025’s 19.69mn and the lowest since 2022. Adults 18–49 posted a 3.92 rating, a 14% drop yr/yr. Despite declines, it led primetime entertainment, while social impressions jumped 42% to 181mn+. Conan O’Brien hosted; tech issues hit, but speeches and performances landed. (The Hollywood Reporter)

- Fox Corp. and prediction-mkt platform Kalshi are in advanced talks on a broad partnership centered on Fox News and Fox Weather, excluding Fox Sports, sources said. The deal mirrors Kalshi’s ties w/ CNN and CNBC across prediction mkts. Talks come as Kalshi faces state and federal scrutiny over legality, lawsuits, and charges, even as platforms expand and seek funding at potential $20bn valuations. (Front Office Sports)

- Nielsen data shows sports drove ~30% of ad-supported TV viewing in Q4 2025, vs 9. 8% for non-sport broadcast, 18% non-sport cable and 43% non-sport streaming. Streaming made up 66.7% of ad-supported viewing, w/ 81% on YouTube, Hulu and Amazon Prime. Live sports’ pull was reinforced by Super Bowl LX’s 125.6mn viewers. (Marketing Dive)

Cable/Pay-TV/Wireless

- China Unicom reported strong 2025 results, with free cash flow rising ~28. 5% yr/yr to RMB36.0bn, driven by disciplined investment and stable operations. Service rev edged up to RMB347.7bn, while net profit reached RMB20.8bn. (Yahoo Finance)

- T‑Mobile, Verizon and AT&T are ramping up discounts as postpaid churn rises, driven by customers rolling off 36‑month device financing plans. With switching barriers falling, carriers are boosting subsidies and easing requirements, especially around Samsung’s Galaxy S26 launch. (Microsoft News)

Capital Market Updates

- Banks led by Bank of America Corp. are weighing an investment-grade bond sale to help fund Nexstar Media Group Inc.’s pending $6bn acquisition of Tegna Inc., aiming to cut borrowing costs. Under the plan, junk-rated Nexstar would sell secured high-grade dollar notes to fund part of the deal and seek an investment-grade rating for the offering, according to people w/ knowledge of the matter, who are not authorized to speak publicly. (Bloomberg)

- Wall St banks began selling $18bn of debt tied to the $55bn take-private of game maker Electronic Arts Co, testing investor appetite as AI fears and geopolitical risks hit credit mkts. JPMorgan-led lenders launched loans and bonds, offering higher yields to move risk. Investors cite stable subscription rev and strong equity backing, while some shun AI disruption risk. (Financial Times)

- MTN Group annc’d strong 2025 results, driven by data and fintech growth across African mkts. The Co said svs rev rose ~25% to 218bn rand ($11.7bn), aided by Nigeria and Ghana, lifting customers past 300mn. Data traffic rose 27% and fintech transactions climbed 15%. Adj earnings rebounded and a 500‑cent dividend was declared, up 45%. (The High Street Journal)

Cloud/DataCenters/IT Infrastructure

- Microsoft is weighing legal action over a $50bn Amazon‑OpenAI cloud deal, arguing it could breach its exclusive Azure rights to route OpenAI APIs. The clash centres on whether AWS can host OpenAI’s Frontier via a “stateful” system. Talks cont’d to avoid court. The rift reflects OpenAI’s push to diversify partners after past Azure ties. (Financial Times)

Crypto/Blockchain/web3/NFTs

- com annc’d it will cut ~12% of its workforce as it integrates AI across the biz. CEO Kris Marszalek said roles unable to adapt were eliminated to position the Co for cont’d success. Impacted staff were notified, though totals weren’t disclosed. The layoffs follow a wider trend of tech and crypto firms citing AI-driven efficiency and cost control for job cuts, after prior reductions in 2023 tied to mkt volatility. (CNBC)

- Polymarket annc’d it will acquire Brahma, a crypto and DeFi infrastructure startup, to scale its blockchain tech and improve user experience. The Co said the deal terms were undisclosed. The move deepens its crypto roots as it competes w/ fiat-based rivals, aiming to boost liquidity for smaller wagers and reduce wallet friction. Brahma, founded in 2021, has processed >$1bn in transactions. (Yahoo Finance)

- Kraken parent Payward has paused plans for a multi-bn IPO amid weak mkts, according to CoinDesk. Sources said the Co is still considering a listing but likely not until conditions improve. Kraken said it confidentially filed with the SEC in Nov. Payward also annc’d $800mn in strategic investments, incl a $200mn stake from Citadel Securities, valuing the biz at ~$20bn. (Yahoo Finance)

- Polymarket is opening a D. C. bar that turns its prediction platform into a physical hangout for people monitoring the situation. The Co shared renderings of a sports-bar-style space w/ wall-to-wall screens showing live X feeds, flight radar, Bloomberg terminals, and Polymarket data. The concept riffs on a viral meme and was annc’d on X; details and opening plans were not confirmed. (Fast Company)

eCommerce/Social Commerce/Retail

- Michaels is cutting prices on 3,000+ items as consumers grow more price‑sensitive and competition for value intensifies. The arts and crafts Co previously reduced prices on 5,000+ products and lowered costs for in‑store parties, aiming to gain share amid Party City and Joann closures. (Retail Dive)

- Macy’s beat fiscal Q4 estimates but issued a cautious outlook as it revamps stores and closes others. The Co forecast FY sales of $21.4–$21.65bn and adj EPS of $1.90–$2.10, both below prior yr. CEO Tony Spring cited tariffs, gas prices and geopolitics. Reimagined stores drove stronger comps, while Bloomingdale’s and Bluemercury led growth. (CNBC)

- The travel bag and backpack Co Cotopaxi plans to double its North American store count from 20 to 40 over the next three yrs, CEO Lindsay Shumlas said. The brand opened a new store in Jackson, Wyoming in early Mar. Fewer than 20% of sales come from stores, but the biz aims to grow physical retail alongside its website and partners like REI and Dick’s Sporting Goods. (Modern Retail)

- Amazon plans to sharply cut packages sent via the U. S. Postal Service, aiming to reduce volume by at least two‑thirds by fall as its contract expires. USPS delivered >1bn Amazon parcels last yr, ~15% of its total, providing critical rev. The shift could worsen USPS losses, reported at $9bn in FY2025, and leave new facilities underused. (The Wall Street Journal)

- JD.com annc’d the launch of its Joybuy online marketplace across the UK, Germany, France and Benelux , intensifying competition w/ Amazon. The Co aims to expand beyond China, offering 100,000+ products across tech, home and grocery, competitive pricing, and fast delivery, incl same-day in major cities. (Reuters

Film/Studio/Content/IP/Talent

- California Film Commission annc’d latest TV tax credits, w/ Disney and Warner Bros. Discovery leading. Disney cos received ~$128.8mn and WBD ~$127.9mn, backing 11 shows, ~2,650 jobs and ~$695mn spend. Credits include animated and competition series, expansions praised by Gov. Newsom. In total, 16 shows are expected to drive ~$871mn in-state spend and $489mn in wages. (The Hollywood Reporter)

FinTech/InsurTech/Payments

- Mastercard annc’d it will acquire stablecoin infra startup BVNK for up to $1. 8bn, incl $300mn in performance-based payments, marking its biggest crypto deal. The move lets the Co link traditional payment rails w/ blockchain systems for stablecoins and tokenized deposits. (CNBC)

- Robinhood Ventures Fund I (RVI) annc’d new investments in Stripe and ElevenLabs. The closed-end fund bought ~$14.6mn of Stripe Class B shares and ~$20.0mn of ElevenLabs Series D. Stripe, a fintech svs Co founded in 2010, offers payments and rev tools. ElevenLabs, founded 2022, builds AI audio tech. (Robinhood)

Handheld Devices & Accessories/Connected Home

- Meta Platforms Inc. plans to open its first Manhattan flagship, marking a cont’d push into physical retail on one of the world’s priciest shopping corridors. The Co said it signed a 10-yr lease w/ Vornado Realty Trust for an entire five-story building at 697 Fifth Ave., next to the St. Regis Hotel, creating a prominent NYC retail presence for the tech giant. (Bloomberg)

HealthTech/Wellness

- Peloton annc’d a Commercial Series of connected bikes and treadmills for high-traffic gyms, marking its shift beyond at-home fitness. Via its Commercial Biz Unit integrating Precor, the Co pairs Peloton software w/ industrial-grade hardware to target global gym mkts. CBU rev grew 10% YoY in fiscal Q2; shipping starts late 2026 across US, UK, Canada and more, w/ a debut at the HFA Show and plans to outfit full gym facilities. (Peloton)

- U.S. retail is shifting from goods to svs as salons, spas and fitness studios outlease traditional stores. Service-based tenants took just over 50% of retail sq ft in 2025, up from ~40% 15 yr ago, per CoStar, as e‑commerce cuts space needs. Wellness spending hit $2.1 trillion in 2024, lifting rents and traffic. (MSN)

Last Mile Transportation/Delivery

- DoorDash annc’d Tasks, a new offering letting Dashers earn beyond delivery by completing short, paid activities for biz. Tasks include taking photos, checking store layouts, or recording everyday actions to provide real‑world insights at scale. (DoorDash)

- Amazon annc’d rollout of one-hour and three-hour delivery in parts of the U. S., expanding ultrafast shipping after yrs of investment. Three-hour svs spans ~2,000 cities, w/ one-hour in hundreds, covering 90,000+ items. A new storefront lets shoppers filter speed options. Prime fees are $9.99 or $4.99; rivals like Walmart tout sub-3-hour delivery, as Amazon tests Amazon Now, drones and other pilots. (CNBC)

Live Entertainment/Theme Parks/Concerts/Experiential

- Activist investor Jana Partners urged Six Flags Entertainment Co to explore a sale and replace its board chair, citing board dysfunction. The letter said engagement w/ buyers is in shareholders’ best interest, months after a new CEO hire and brand ambassador annc’d. (CNBC)

Macro Updates

- The Fed held its key rate at 3. 5%–3.75% as Chair Powell said inflation is easing but not as much as hoped. He cited surging oil prices tied to the U.S.-Iran war and a hot Feb. PPI as near-term inflation risks, while rejecting stagflation fears and noting unemployment near normal. (CNBC)

- Investors rushed into cash at the fastest pace since the pandemic as war in Iran rattled mkts, leaving few safe havens. A BofA survey shows avg cash holdings rose to 4.3% of AUM in Mar., up from 3.4% in Feb., reversing a Jan. low of 3.2%. Stocks and gov’t bonds fell after Feb. 28 strikes, oil topped $100, inflation fears rose, and sentiment hit a six‑month low. (Financial Times)

- U.S. inflation’s ‘transitory’ label turns five, still shaping policy and politics. Prices rose above 2% in Mar. 2021, then surged, with the Fed hiking rates sharply in 2022 as PCE hit >6% and CPI topped 9%. Inflation eroded income gains, hit lower earners, and shocked homebuyers w/ mortgage rates jumping from <3% to >6%. (Reuters)

Media Conglomerates

- Nexstar Media Group, Inc. annc’d it closed its acquisition of TEGNA Inc. after receiving approval from the FCC and U.S. DOJ, marking completion of the transaction. CEO Perry Sook said combining the two Cos strengthens local journalism and positions the biz to deliver enhanced local programming through expanded assets, capabilities, and talent. (Nexstar)

- Liberty Global Ltd annc’d a reduction in its stake in ITV PLC, cutting voting rights to 2. 47%, equal to 93,909,460 shares, from 4.99%. The filing said the threshold was crossed on 17‑Mar‑2026 and the issuer was notified on 18‑Mar‑2026, w/ completion the same day. (Investgate)

- Tencent is developing an AI agent for WeChat to tap China’s OpenClaw-driven AI agent fever and close gaps w/ rivals Alibaba and ByteDance. President Martin Lau said the Co, long seen as an AI laggard, is betting big on AI tech through its ubiquitous social media app, which has ~1.4bn users. The effort underscores a renewed push to compete across China’s fast-moving AI mkts. (Nikkei Asia)

- Tencent reported 2025 rev beating estimates, driven by stronger gaming, cloud and AI-related svs. The Chinese tech Co posted 751.8bn yuan (~$109bn), topping forecasts, and said AI investments lifted ad targeting, games engagement and cloud growth. The Co spent 18bn yuan on AI in 2025 and plans to double it this yr. Q4 rev rose 13%, while biz svs rev jumped 22%. (CNBC)

- Disney annc’d a revamped Disney Entertainment leadership as Dana Walden becomes President and CCO, expanding oversight to film, TV, streaming, games and digital. Debra O’Connell is upped to Chairman of Disney Entertainment Television, while Alan Bergman stays Chairman of Studios. (Deadline)

Metaverse/AR & VR

- Meta is shutting down Horizon Worlds on Meta Quest, ending its struggling virtual reality social hub. The VR tech experience will be discontinued in Jun. as part of broader moves to slim the biz that became the Co’s namesake. After limited user traction and mounting costs, the shutdown signals cont’d reprioritization and a pullback from the flailing metaverse bet in its overall strategy. (Bloomberg)

Regulatory

- The antitrust trial against Live Nation–Ticketmaster restarted after the DOJ reached a mid‑trial settlement, leaving dozens of states to lead the case. Judge Arun Subramanian signaled a mistrial was unlikely, pushing states to regroup, retain the DOJ expert, and proceed. (The Verge)

- The UK govt backtracked on AI copyright plans after backlash from major artists incl. Sir Elton John and Dua Lipa. The proposal to let AI firms use copyrighted works w/ an opt‑out was dropped; the govt now says it has no preferred option and will take time to get this right. Tech Sec Liz Kendall said views were heard, aiming to balance creatives’ control w/ AI training needs. (BBC)

- Eight U. S. states sued to block Nexstar’s proposed $3.54bn acquisition of Tegna, saying it would raise pay‑TV prices, cut newsroom jobs, and curb competition by jointly operating stations in the same mkts. California AG Rob Bonta called the deal illegal. DirecTV filed a separate suit. Critics warn the combined Co would cover ~80% of U.S. (Reuters)

- A US appeals court paused an injunction against Perplexity AI hours before it took effect, giving the startup more time to challenge a lower-court order in its dispute w/ Amazon. The ruling freezes limits on Perplexity’s Comet shopping bots, which Amazon alleges improperly accessed password‑protected systems and failed to disclose bot activity. (Yahoo Finance)

- Google said it is working w/ the UK Competition and Markets Authority on proposed digital market rules for Search. The Co backs goals of fairness and publisher choice, says its ranking treats its products equally, and warns some proposals could raise spam risks. (Google)

- A US federal judge dismissed Musi’s lawsuit against Apple, ruling Apple can delist apps w/ or w/o cause under its developer agreement. The court upheld Apple’s removal of the free music‑streaming app, which pulled content from YouTube, and rejected claims Apple violated its DPLA. (Ars Technica)

- Arizona AG Kris Mayes sued Kalshi, accusing the Co of running an illegal gambling biz by letting users bet on Arizona elections. Mayes said the platform violates state law despite its prediction mkts branding. Kalshi says it operates under the CFTC and shouldn’t face state-level gambling charges. (Engadget)

Satellite/Space

- UK regulator Ofcom annc’d measures to expand satellite connectivity as demand rises. It will make up to 10GHz of Q/V‑band spectrum available for satellite gateway earth stations, mainly in rural low‑density areas, boosting capacity for faster broadband and svs. The move, detailed, also proposes limited urban access, streamlines NGSO licensing, and extends incentive pricing to support efficient spectrum use. (Advanced Television)

- Blue Origin filed plans w/ the FCC to launch Project Sunrise, an orbital data center constellation of up to 51,600 satellites to deliver in‑space computing for AI workloads. The Co said always‑on solar power and no grid constraints could lower compute costs vs terrestrial data centers. (Space News)

Social/Digital Media

- Meta annc’d Creator Fast Track by offering guaranteed monthly pay and boosted reach to lure Instagram, TikTok and YouTube creators to Facebook. The Co will pay $1,000 for creators w/ 100,000+ followers and $3,000 for those over 1mn, for three months, plus ongoing reach boosts. Meta said it paid ~ $3bn to creators in 2025, up 35%, to revive original content. (CNBC)

- Short-form video dominates Gen Z media habits in Great Britain, per a YouGov survey cited by EMARKETER [Mar. 16]. About 85% of ages 16–24 watch short-form weekly and 69% daily, exceeding TV series (65%), films (45%), video podcasts (33%), and livestreams (25%). Adults 55+ show opposite patterns, favoring TV series (71%) and rarely using video podcasts (11%). (eMarketer)

- New Chartbeat data shared w/ Axios shows small publishers (1k–10k daily page views) face the steepest AI-era search declines. Over two yrs, traditional search referrals fell 60% for small sites vs 47% for mid-sized and 22% for large. From Dec. 2024–Dec. 2025, Google Search and Discover page views dropped 34% and 15%. (Axios)

Software

- IBM said it closed its ~ $11bn acquisition of data‑streaming Co Confluent, first annc’d in Dec. , to help biz access dispersed data for AI agents. CEO Arvind Krishna said the tech will be the backbone of IBM’s platform, mirroring Red Hat, boosting hybrid cloud and AI. IBM cited ~$4.5bn productivity gains from AI, w/ ~20% of some roles seeing change. (The Wall Street Journal)

Sports/Sports Betting

- Kalshi is valued at $22bn in an ongoing funding round, per WSJ sources, doubling its $11bn valuation from Dec. after raising ~$1bn. The round is led by Coatue. Kalshi lets users trade binary contracts on politics, sports and economics. The news comes amid intensifying regulatory scrutiny, lawsuits by MA and NV, and clashes w/ state gaming authorities. (Reuters)

- MLB annc’d agreements naming Polymarket as its official prediction‑mkts exchange and establishing an information‑sharing partnership w/ the Commodity Futures Trading Commission to safeguard the sport’s integrity. The deal allows Polymarket to use MLB marks and official league data, while setting limits on markets vulnerable to manipulation. League officials said federal oversight offers clearer regulation than state‑by‑state sports betting rules as prediction mkts grow rapidly. (ESPN)

- MLB faces volatility from unsettled media rights, looming 2027 labor issues and no salary cap, yet that uncertainty is drawing private equity. Since 2019, MLB has allowed PE to buy up to 15% of a team, w/ caps on total stakes, attracting firms like Arctos and Sixth Street. (Sportico)

- The WNBA and players’ union reached a tentative new collective bargaining agreement reflecting rapid league growth. The deal raises the salary cap to $7mn from $1.5mn, lifts avg pay to ~ $600,000 and minimums above $300,000, and grants players a 20% share of gross rev, up from 9.3%. It awaits ratification after 100+ hours of talks. (NBC)

Tech Hardware

- Micron annc’d results showing rev almost tripled as AI-driven memory demand surged. FQ2 rev reached $23.86bn, topping estimates, w/ adj EPS $12.20. Guidance calls for ~200% yr growth to ~$33.5bn rev. Cloud, mobile and client svs jumped sharply, margins expanded, and capex will rise as Co adds U.S. capacity. (CNBC)

Towers/Fiber

- TIM and Swisscom’s Fastweb annc’d a non‑binding JV to build up to 6,000 telecom towers in Italy, challenging mast Co INWIT. The move could boost bargaining power as both seek to renegotiate contracts and be main customers of the JV, open to others. INWIT said deals stay until 2038, but shares fell 22% amid takeover speculation by Ardian, which holds 31%. (Reuters)

Video Games/Interactive Entertainment

- With GTA VI nearing launch, speculation over a $100 price prompted comments from Take-Two Interactive CEO Strauss Zelnick. He dismissed interstitial ads in games costing “70 or 80 bucks,” implying a standard AAA price. The title is seen as standalone, appealing to new teens and older fans alike, easing fears about the long gap since GTA V. (Screen Rant)

Video Streaming

- Netflix co-CEO Ted Sarandos aimed to move past the failed WBD takeover, saying there was no political interference from President Trump and calling it a biz decision. He said Warner Bros accepted a $111bn bid over Netflix’s offer. Sarandos urged EU lawmakers reviewing AVMSD to favor incentives, citing €13bn invested in Europe, meeting the 30% quota, warning against fragmented rules, and saying YouTube is a direct TV competitor. (The Hollywoord Reporter)