It felt a little bit like a seesaw this week in the markets, but the major indices closed relatively flat (Nasdaq falling -0.5% and the S&P 500 closing up +0.1%). Treasuries were weaker across the curve, with yields up 5-6 bp. The 43-day government shutdown finally ended with a stopgap bill through January 30, and while it had limited market impact, attention is now shifting back to the return of official economic data, with some October reports potentially skipped, and September payrolls slated for release on November 20. Uncertainty about the outcome of the Fed’s December rate cut meeting again drove headlines.

In the sector, the earnings storm is winding down but we didn’t focus on updates across the legacy media, China Tech, last-mile, and AI infrastructure sectors and next week companies including Nvidia and Warner Music Group will close us out.

The key themes/developments that we focus on this week are below:

- Earnings Scorecard – Week 5

- Disney’s Growth Story Is Intact BUT Pushed To H2

- Paramount’s Streaming Profitability Takes Center Stage, But Strategic Questions Loom

- Some Mixed Signals Pertaining To Holiday Shopping Expectations Emerge This Week

- Temporary Data Center Delays Put A Damper On CoreWeave's Results

- More & More Players Are Making A Bet On The Prediction Markets

- A Handful Of Other Key Media Entertainment Updates Across Studios, Streaming, Sports, Games, Experiential, And More...

- Competition Isn't Emptying Instacart's Cart As Feared

- China Tech Is Investing For Growth, Which Is Pressuring Margins

- Valve's New Hardware Devices Put The Video Game Sector Into Focus This Week

- Grab Bag: Waymos Are Coming To Freeways / AI Shots In House Of David S2 / Google Faces New EU Probe Over News Publisher Rankings

Have a nice weekend.

Best,

Leslie

P.S. If this email has been forwarded to you and you would to join our distribution list, please email me. Thanks!

Earnings Scorecard – Week 5

After a record-breaking 91 companies in our LionTree Universe reported earnings last week, the pace slowed significantly this week, with just 18 companies reporting. Stock reactions were neutral, with an equal number of companies trading up and down. The worst performer was WEBTOON, which fell -25% after its report, and the best performer was PubMatic, up +43%.

The last of the legacy media names reported this week, though stock reactions diverged, with Disney falling -7.7% post its print (see Theme #2), while Paramount Skydance jumped +9.8% (see Theme #3). China Internet/Tech names also posted their quarterly results, but had a tough week with Tencent Music down -8.4%, JD.com down -1.7% and Tencent down -0.8% (see Theme #9).

On the AI infrastructure side, CoreWeave’s stock fell -16.3% (see Theme #5), while Instacart rounded out the last-mile earnings reports and was up +1.6% (see Theme #8).

The table below includes select mid- and large-cap TMT and consumer companies in our LionTree stock universe that reported this week.

Disney’s Growth Story Is Intact BUT Pushed To H2

Disney is juggling multiple moving parts across its media and entertainment portfolio, and this quarter’s results and outlook largely disappointed investors. FQ4 was mixed: total revenue missed, operating income landed in line, and adj. EPS beat (but still declined -3% y/y). Mgmt reiterated its double-digit adj. EPS growth targets for FY26 and FY27 (after closing FY25 up +19%), but the heavy back-end weighting across certain divisional op income growth tempered near-term enthusiasm.

First of all, the core Entertainment segment remains in transition. Streaming underperformed relative to Street expectations, despite subscriber and ARPU trends surprising to the upside. Looking ahead, mgmt’s guides of $375mn DTC SVOD operating income in FQ1 is a sequential improvement vs the $352mn in FQ4 and the 10% margin target for fiscal 2026 was reiterated. As a reminder, this was the last qtr that Disney will disclose subscriber numbers. On the linear side, declines were steeper than anticipated though profitability beat and the Co reaffirmed FY26 Entertainment segment operating income growth guidance at double digits but flagged a H2 weighting. Near-term headwinds in FQ1 include a $400mn hit to film operating income, weaker political ad revenue, and tough comps against last year’s Star India contribution. Front-end loading of film costs (higher marketing spend for Avatar: Fire and Ash) adds further pressure.

Sports was a bright spot…ESPN DTC is off to a strong start, bundling looks sticky, and live sports viewership remains robust. However, FY26 sports operating income y/y growth will skew to FQ4 given rights expense timing. Experiences missed estimates, but mgmt downplayed NBCU’s Epic opening as a major factor, instead citing that other parks felt more of that increased competition vs them. Forward bookings and cruise demand remain solid, and FY26 Experiences guidance for high-single-digit operating income growth stands, but again, will be weighted to H2 amid pre-opening and dry dock costs.

Overall, the near-term visibility is clouded by back-end weighting and cost headwinds leaving the narrative hanging on execution. It was good timing that the Co also annc’d a doubling of the buyback for F2026 and, coupled with increasing its annual dividend by 50%, are certainly signs of long-term confidence, at least from the mgmt. point of view.

-> Disney’s stock closed down -4.5% on the week and is down -4.6% YTD

FQ4 Was A Mixed Bag And While F2026 Guidance Was Largely Reiterated, It Will Be More H2 Weighted

- Total FQ4 revs disappointed, while op income was in-line and adj EPS beat (but fell -3% y/y)

- Experience – MISSED: Both revs & op income were below cons

- Entertainment – MIXED: Revs were worse than expected especially as it related to Linear revs declines while op income was better than expected

- Linear – Mixed: Revs were -3.7% below cons but op income was ahead by +9.8%

- DTC – Missed: Both revs and op income were below cons

- CSLO – Beat: Both revs and op income topped projections

- Sports – BEAT: Better performance in both revs and op income

- Maintained double digit adj EPS guidance for F2026

- Expect $24bn in content investment across Entertainment and Sports ($1bn increase y/y)

- Expect $19bn in cash provided by operations, +7% y/y

- Expect $9bn of CapEx ($1bn increase y/y)

- Increasing cash returns:

- Doubling share repurchase target y/y to $7bn

- Declared a cash dividend of $1.50/shr

- Maintained double digit adj EPS guidance for F2027

Entertainment Segment: Reiterated F2026 Op Income Growth Guidance But It Will Be Weighted To H2

- Entertainment – FQ4 headline results were mixed vs consensus (see chart above)

- Revs fell -6% y/y (decel from +1% y/y in Q2)

- Op income fell -35% y/y (decel from -15% y/y in Q2)

- Due to lower results at Content Sales/Licensing and Other (film slate comps) and Linear Networks, partially offset by an increase at DTC

- Reiterated F2026 guidance for double digit % segment op income growth y/y, BUT will be weighted to H2

- The Co will face headwinds in FQ1…

- Film will have a -$400mn neg impact to op income

- The Co will have lower political advertising rev of $140mn vs prior yr period

- They have an unfavorable comp to $73mn of Star India op income in prior yr period

- Linear networks op income decline was negatively impacted by Star India transaction (contributed $84mn to Intl Linear Networks in FQ4 last year

- Lower results at Domestic Linear Networks were due to declines in advertising driven by lower viewership and lower political advertising (adverse impact of ~$40mn versus the prior-yr qtr), partially offset by a decline in programming and production costs

Film: Will Be Pressured In FQ1 But Mgmt Remains Optimistic About The Forward Content Slate

- Tough Film comps and higher costs will weigh on FQ1 results – expect -$400mn negative impact in Entertainment op income

- More theatrical releases in FQ1 of this year

- Comping against Moana 2 and Mufasa: The Lion King in the prior yr qtr

- Also expect FQ1 to include higher costs, including marketing, for Avatar: Fire and Ash

- Despite higher FQ1 costs, “very encouraged” by the studio slate coming up…“the slate is as strong as it has been in a while and that goes into F27 and 28”

- Films into the holidays: Zootpia 2 and Ash

- Cal26 Films: The Devil Wears Prada 2, Lucasfilm’s The Mandalorian and Grogu, Pixar’s Toy Story 5, Disney’s live-action Moana, and Marvel Studios’ Avengers: Doomsday

- Have a long list of other content drivers

- FQ4 TV content drivers: and Season 34 of ABC’s Dancing with the Stars

- Other highlighted upcoming content: New seasons of Paradise, The Secret Lives of Mormon Wives, Percy Jackson & the Olympians, American Idol, and the revival of the comedy Scrubs; Also Taylor Swift’s End of an Era docuseries, as well as the concert film Taylor Swift: The Eras Tour: The Final Show

- FQ1 overall is what drives the guidance

Direct-To-Consumer: Fell Short Of FQ4 Expectations But Mgmt Still Thinks They Can Get To 10% Streaming Op Margin in F2026

- Total FQ4 DTC revenue and op income fell short of consensus estimates (see chart above)

- Revs grew +8% y/y vs +6% y/y in FQ3 and included an adverse impact of 2ppts as Disney+ Hotstar was included in Q4 last year

- Op income incr’d +39% y/y due to higher subscription revenue driven by growth in ARPU and subscribers, partially offset by higher programming and production, marketing, and technology and distribution costs

- Guided for FQ1 DTC SVOD operating income of ~$375mn (up vs $352mn in FQ4)

- Reiterated guidance for driving op margin to 10% for Entertainment DTC SVOD in F2026

- “Beyond 2026, we’re certainly looking to gain margin in chunks, not in basis points”

- This is the last qtr that the Co will disclose subscriber figures but FQ4 DTC subscriber trends generally outpaced Street estimates(total subs reached 195.7mn, +12.4mn seq driven by wholesale Hulu subscriptions and D+ ended the qtr w/ 131.6mn subs)

- ARPU was also generally ahead of projections though Domestic APRU was more ~inline

- Increasing the streaming app experience and feature set –

- Creating a unified app experience

- In Oct, Hulu became the global gen entertainment brand w/in D+ in international mkts

- Working to consolidate all Entertainment content domestically in a single app

- Continue to enhance user experience and personalization on D+ – began rolling out experiential and navigational improvements

- Expanding exclusive perks program globally

- Expanding intl reach by investing in originals and working with local studios to license content – taking a disciplined approach to markets they are prioritizing

- Overtime, with AI, can use D+ as a portal to all things Disney, with commerce and engagement engines for theme parks, hotels and cruise ships and there are “huge oppties” for games as well: Can integrate game like features into D+; Can provide D+ users with more engaged experience and create short form UGC

Sports Segment: ESPN DTC Is Off To A Strong Start…But Expect Sports Op Income Growth Y/Y To Be Weighted To FQ4

- FQ4 Sports segment topped estimates (see chart above)

- Revs grew +2% y/y (accel from -5% y/y in Q2)

- Advertising rev growth due to an increase in impressions and higher rates

- An increase in sub and affiliate rev reflecting higher effective rates and the comparison to the temporary suspension of carriage with an affiliate in the prior-year quarter, partially offset by fewer subscribers

- Op income fell -2% y/y (up from -7% y/y in Q2)

- Higher marketing costs due to the August 2025 launch of the ESPN DTC service

- An increase in programming and production costs due to contractual rate increases and costs for new sports rights

- Revs grew +2% y/y (accel from -5% y/y in Q2)

- Maintained F2026 guidance of low-single digit % segment op income growth y/y, BUT with growth WEIGHTED to FQ4, reflecting the timing of rights expenses, which adversely impacts y/y comparability in Q2 and Q3

- Q4 Domestic ESPN op income was down -3%, as higher marketing / programming & production costs were partially offset by higher advertising, subscription and affiliate revs

- The increase in marketing costs in the quarter was due to the launch of ESPN DTC

- Higher programming and production costs were driven by contractual rate increases and new sports rights

- Q4 Domestic ESPN advertising revenue was up +8% y/y, driven by strong viewership for U.S. Open tennis, NFL, and college football programming, as well as higher rates

- Q4 Domestic ESPN op income was down -3%, as higher marketing / programming & production costs were partially offset by higher advertising, subscription and affiliate revs

- “Thrilled” by the response to the EPSN DTC launch

- It has been a “real success”

- It has done well with attracting new users

- It is increasing engagement with existing users

- Signed up a substantial # of cord nevers to the premium product

- The product is “working for advertisers” as well

- Later in the call Iger say something else I missed – can you find?

- ESPN app now includes –

- Multiview

- Vertical short form video (“Verts”)

- SportsCenter For You

- Catch Up to Live

- Other tools

- Live game stats

- Betting (will also be integrating DraftKings per recent agreement)

- Fantasy sports

- commerce integration

- Bundling has been an effective strategy for ESPN DTC and expect to do more

- 80% of all the subscribers to the new ESPN service are actually buying the Trio or the Triple bundle, “That’s a very positive sign for us in terms of lowering churn into the future”

- Bundling externally has also been successful

- D+ with Max also shows lower churn

- WBD has also benefitted from the bundle

- “We’ve expressed the desire to do more bundling with other companies and have been in discussions on and off with other companies about doing just that”

- Live sports viewership remains strong w/ Q4 ratings across ESPN networks, incl ESPN on ABC, up +25% y/y

Experiences Segment: Maintained F2026 Op Income Growth Guidance But It Will Be Back End Weighted

- Experiences – FQ4 growth was relatively steady despite incr’d competition but modestly missed consensus expectations (see chart above)…

- Revs rose +6% y/y (decel from +8% y/y in FQ3)

- Op income grew +13% y/y (same as FQ3)

- Domestic

- Revs rose +6% y/y vs +10% y/y in FQ3

- Op income rose +9% y/y vs +22% y/y in FQ3: Driven by growth at Disney Cruise Line reflecting the launch of the Disney Treasure in Q1 F2025

- Margins: 15.7%

- International

- Revs rose +10% y/y vs +6% y/y in FQ3

- Op income rose +25% y/y vs a decline of -3% y/y in FQ3: Due to growth at Disneyland Paris

- Mgmt believe NBCU’s EPIC opening is impacting the rest of the competition in Florida as opposed them

- The impact was as expected on their end

- Demand fundamentals remain intact – bookings are up +3% in the first qtr and are up for the yr

- Demand for cruises is very strong despite incr’d supply

- Maintained F2026 segment op income guidance of high single digits y/y but WEIGHTED to H2: Included in the guidance…

- $160mn in pre-opening expenses (~$90mn in FQ1), driven by Disney Adventure and Disney Destiny

- $120mn in higher dry dock expenses for Disney Cruise (~$60mn in FQ1)

- Excited about new growth drivers –

- Two new cruise ships – Disney Destiny’s maiden voyage (Nov 20) and Disney Adventure (Mar); Brings total ships to 8

- World of Frozen at Disneyland Paris

- Have expansion projects underway at all their theme parks, five addtl cruise ships scheduled for launch beyond F2026, and a new theme park planned for Abu Dhabi

Other – YouTube Feud, M&A and Advertising

- Limited updates were given on YouTube

- Not much was said about YouTube as the Co is currently still in “ongoing negotiations”

- BUT… in terms of EPS guidance a hedge was built in already

- In terms of dollar impact there are two pieces:

- The piece that they are not getting paid for

- The piece that they are picking up by subs moving elsewhere

- Bob Iger said “we are not trying to break any new ground here”

- Interested in M&A? “Don’t comment on deals” but “have a great portfolio and don’t need to do anything”; Will see how the moves play out with other players but “don’t expect Disney to participate and make any significant moves” -> there were some updates on the media consolidation front this week, see more in Theme #7

- Advertising seems to be trending the right way going into 2026:Still expecting growth going into 2026, despite tough political comps in FQ1(ad rev grew +5% y/y in 2025)

- Sports has been “particularly strong”, DTC has had supply coming into the market, and CPMs have been improving over the last two qtrs’ Linear is driven by what happens with subs

Paramount’s Streaming Profitability Takes Center Stage, But Strategic Questions Loom

The date of Paramount’s Q3 earnings call marked 96 days since the start of the “new Paramount” (the Skydance deal officially closed Aug 7th) and CEO David Ellison is “more confident than ever”. The company has been in the midst of a fundamental transformation, and this quarter’s results and guidance provided a clearer picture of the new Co’s strategic plans and priorities.

Big picture, profitability is now the major headline theme. Paramount’s Q3 adj OIBDA beat cons by +14% and 2026 adj OIBDA guidance topped cons by +13%. This 2026 profitability outlook will be underpinned by higher than originally expected efficiency targets (raised from $2bn to $3bn+) but also absorbs a significant ramp in content investment across film, TV, and streaming (plans an incremental $1.5bn in content spend). The UFC deal is part of the spend and despite the high-ticket price (and some pushback from analysts), mgmt is very confident in the returns they will generate from being the exclusive home to the league. Mgmt makes a good point that the cost of an annual subscription to Paramount+ is less than just one UFC pay-per-view event under the prior distribution. They see more subscribers, more engagement and more retention on the way.

The much better profitability in the Co’s Direct-to-Consumer (DTC) biz was a key standout as Q3 adj OIBDA reached $340mn vs cons $112mn and on a full year basis, the Co expects DTC to be profitable in 2025, followed by further “growth” in 2026. The streaming business is and (and will) benefit from price increases and several operational changes are underway that will help with profitability, though they will be a headwind to subscribers in the near term (see details below).

The Film business is a work-in-progress, and the Co is now ramping to 15 movies year, up from 8 when they bought the Co. With that said, 2026 Film Entertainment revenue is expected to decline as they work to recalibrate their film slate and have tough comps vs Mission: Impossible -The Final Reckoning in 2025.

Lastly, while mgmt acknowledged the pressure faced by its cable networks and is working on creating more value from these assets (and has no plans to spin off these assets), it also contends that its CBS b-cast business is more resilient than people are giving it credit for and ratings remain strong.

Overall, Paramount set a new narrative this quarter, but there is still a lot of execution ahead and a potential deal with WarnerBrosDiscovery remains a key question (mgmt reiterated there are “no must-haves” and they will be evaluating options based on how much they can help accelerate reaching the Co’s goals).

See below for more details on what we thought were the most important themes from Paramount’s results.

-> Paramount shares rallied almost +10% in reaction to earnings but is still down -20% from the highs in late September on the back of deal speculation

High Level Strategic Direction / Updates

- Mgmt highlights its 3 “North Stars”

- 1 – “Investing in our growth businesses anchored by our creative engines and exceptional storytelling”

- 2 – “Scaling our direct-to-consumer business globally”

- 3 – “Driving efficiency enterprise-wide with a focus on long-term free cash flow generation”

- Layoffs: At the end of Oct, the Co implemented a significant workforce reduction of ~1k employees across the Co

- Intend to re-segment their financials starting w/ Q1 2026 results

- Studios: Will house all production and IP, including almost all licensing rev

- TV Media: Will be comprised of the broadcasting and the cable businesses

- There will be no impact to reporting for their DTC segment

MUCH BETTER Streaming Profitability Was The Key Driver To Q3

- While total revenue MISSED by -2.3% (and was down -0.4% y/y)…adj OIBDA BEAT by a significant +14.1% (and was up +11% y/y vs -5% y/y in Q2)…DTC was the key positive

- TV Media – MIXED: Revs were -2.4% below cons while adj OIBDA was +4.2% ahead (down -12% y/y vs -15% y/y in Q2)

- DTC – STRONGER: Revs beat by +3.2% (up +17% y/y vs +15% y/y in Q2) and adj OIBDA beat by +203% (up +590% y/y

- Film – WEAKER: Revs missed by -12.1% while adj OIBDA missed by -187%

- FCF at $15mn significantly MISSED cons $296mn but incls payments for restructuring, transaction-related items, and transformation initiatives which total $309mn

While Q4 Guidance Is A Mixed Bag, 2026 Guidance Topped Estimates & The Co Raised Efficiency Targets…

- Q4 guidance was a mixed bag

- Revenue BEAT cons by +4.6%, given the $8.10-$8.30bn range (growth of +1-4% y/y)

- Led by strength in DTC, offset by declines in TV Media and Filmed Entertainment

- Adj OIBDA MISSED cons by -9%, given the $500-$600mn range (6.7% margin)

- Expect restructuring charge of ~$500mn

- Revenue BEAT cons by +4.6%, given the $8.10-$8.30bn range (growth of +1-4% y/y)

- FY 2026 guidance was above consensus – especially on profitability

- Revenue slightly BEAT cons by +1.2% and reflects +4% y/y growth

- Led by healthy DTC revenue acceleration partially offset by declines in TV Media affiliate and advertising w/ cont’d headwinds from the pay TV industry on affiliate rev and lower advertising revenue y/y

- Adj OIBDA BEAT cons by +12.9%, which implies a 11.7% margin

- Driven by progress against their $3bn+ efficiencies plan, and includes incremental investments across content and technology (see below)

- Revenue slightly BEAT cons by +1.2% and reflects +4% y/y growth

- Incr’d the run rate efficiency target from $2bn to “at least” $3bn

- Of the anticipated $3bn+ run rate –

- More than $1.4bn will have been executed btw the deal announcement and YE

- With an addtl $1bn+ anticipated for 2026

- Expect to complete their transformation program by the end of 2027

- Achieving this will requires ~$800mn in transformation costs in 2026 and $400-$500mn in 2027

- Of the anticipated $3bn+ run rate –

- These transformation costs will negatively impact FCF but there is oppty w/ working capital and taxes

- Q4 FCF: Negatively impacted by several hundred million from transformation costs

- 2026 FCF: Including the $800mn transformation costs, FCF will be negative in 2026, but ex those costs, it would be positive

- There is a lot of opportunity to improve working capital which has been a big negative

- Need to get better payment terms

- Need to get better systems in place

- Need to get more visibility into accumulating receivables by customer and by area

- Cash tax rates will also be a focus

- Also, expect to achieve investment grade debt metrics by the end of 2027

The Better Than Expected 2026 Guidance Also Factored In A Lot More Spend In Content & Technology

- “Storytelling will be the heart and soul of everything they do”

- Expect to make incremental programming investments of more than $1.5bn in 2026 (globally) …“Investing a lot more in content than envisioned earlier and what they put in the investor deck”

- Across theatrical and DTC: Includes their DTC investments in the UFC, Paramount+ Originals, and 3P catalog licensing and the ramp in their film slate

- Aiming to have a slate of year-round programming

- Global: Ramping investment in local content in key regions – incl Latin America, Canada, and parts of EMEA

- Questions arose about whether Paramount can get a return on its UFC deal? Mgmt is very confident they will

- “Couldn’t be more excited about the TKO partnership and also zuffa boxing

- UFC is a “bit of a unicorn for us”

- P+ is now the home for combat sports (rights in US, Latam, Australia)

- And UFC is the largest sport that is not split across properties

- UFC’s 100mn fans base in the US has grown +25% since 2019 to date

- AND they did that behind a double paywall

- Eliminating the double paywall will drive strong engagement

- “The cost of an annual subscription to Paramount+ [is] less than just one UFC pay-per-view event under prior distribution”

- Other recent content investments/platform drivers

- Exclusive 50year deal for South Park (a top acq driver on Paramount+ in Q3)

- 4-year exclusive deal w/ Duffer Brothers for feature films, TV, and streaming projects starting in 2026

- An overall film deal w/ 5x Oscar-nominated filmmaker James Mangold

- A first-look TV deal w/ Jessica Biel and Michelle Purple’s Iron Ocean Productions

- Renewed partnership w/ The Conjuring franchise’s Walter Hamada

- New horror/thriller label for Paramount Pictures in collaboration w/ Weapons producers J.D. Lifshitz and Raphael Margules

- Signed a film partnership with Activision to produce Call of Duty

- Other key upcoming exclusive streaming releases –

- Season 3 of Tulsa King (most watched title so far in Q4)

- Season 4 of Mayor of Kingstown (launched late Oct)

- Season 2 of Landman (November 16th premiere)

- Also, annc’d renewals of Dexter: Resurrection, Yellowjackets and The Chai

- The Co is also making upgrades to the backend to drive efficiency and a better user experience

- BET+, P+, Pluto are all on different platforms…they are transitioning to the same on by mid-2026

- That will improve user experience and discovery & ad tech

- The Co is exploring how to best build and deploy AI across personalization and recommendations

- And unifying the Co under a single ERP system by early 2027 which will give real time info for managers

On A FY Basis the Co Expects Direct-To-Consumer To Be Profitable In 2025 And With “Growth” In 2026

- DTC was stronger than expected….revs grew +17% y/y vs +15% y/y in Q2 and adj OIBDA up +590% y/y to $340mn

- Paramount+ (P+) revenue (80% of DTC biz) rose +24% y/y vs +23% y/y in Q2

- P+ subs grew +10% y/y to 79.1mn (but a decel from +14% y/y in Q2): Note that this includes 1.2mn on free trials but starting in Q4, free trials will not be included in P+ subs #s

- Importantly, now expect that on FY basis, DTC will be profitable in 2025 and will show “growth” in 2026

- Q4: Expect adj. OIBDA losses on an absolute basis due to seasonally weighted content costs

- Key operational shifts in DTC strategy include –

- Shifting away from certain hard bundles and low-margin subscriptions

- Reducing investment in select international markets w/o a clear path to sufficient scale

- Retiring free trials

- Reviewing discount practices

- Price increases and elimination of hard bundles are helping ARPU but Q3 net adds will be down seq

- Q4: Expect similar y/y increase in P+ ARPU (+11% y/y in Q3) but also expect net adds to be below Q3

- Recent price increases is a tailwind (Canada and Australia)

- And terminated two low-ARPU international hard bundles (expect more terminations in 2026)

- Q1 2026: Plan to implement price increases in the US

- Q4: Expect similar y/y increase in P+ ARPU (+11% y/y in Q3) but also expect net adds to be below Q3

- Believe that investment in content in the back-end (see section above) will drive incremental subs and profitability

Recalibrating The Underperforming Film Business

- Film business underperformed expectations w/ most films missing lifetime profit targets in 2025

- Segment Q3 revs grew +30% y/y but due to the consolidation of Skydance licensing and other rev

- Segment Q3 adj OIBDA fell to -$49mn from -$89mn in Q3:24

- Recalibrating and increasing investments…

- Will make more films: Ramping to ~15 annually beginning in 2026 (vs the 8 being made when they acquired the studio)

- Will “significantly” expand TV studio output over the coming yrs: The titles will be on their own platform and licensed to third parties

- …But it will take some time: The Co expects rev to be down y/y in 2026 as they work to recalibrate their film slate and as they compare against Mission: Impossible – The Final Reckoning in 2025

Legacy Media Remains Under Pressure But Mgmt Believes B-Cast Is Much More Resilient Than Expected

- TV Media business is still under pressure w/ revs down -12% y/y (accelerating from -6% y/y in Q2) but the Co posted a modest seq improvement in adj OIBDA to -12% y/y from -15% y/y in Q2

- Advertising declines of -12% y/y, incl an 8ppt headwind from political spending and from the comparison to the recognition in 2024 of rev that had been previously underreported by an international sales partner

- CBS is a “cornerstone asset” and is off to a “great start this season”…momentum in CBS Sports

- The NFL on CBS had its best October in a decade, averaging more than 19mn viewers

- Set to broadcast the Thanksgiving Day game (traditionally the most viewed season game of the yr)

- They have a full slate of NFL playoffs, highlighted by the AFC championship game on CBS and Paramount+

- Regarding linear TV, mgmt differentiates between broadcast & cable nets: While b-cast is declining, the declines are modest vs cable and content on b-cast side is a huge driver on DTC subs and engagement

- Mgmt believes they are in a good spot w/ dollars coming from streaming and reach coming from CBS

- Cable declines are accelerating but streaming is a replacement for that

- BUT mgmt will NOT spin off its cable assets…they think they can still drive value as part of Paramount

Another Growth Driver Is Digital Advertising…Signs New Deals W/ Ad Agencies

- Digital advertising has not had the “growth potential we know it can achieve”…partnered with IPG and Publici, across both ad sales and media buying

- They are getting significant savings on the cost of buying marketing across the Co

- They got “significant revenue commitments” over 3 years with both Publicis and IPG

- Most of this advertising will be in the digital area, “should see numbers over the next couple of yrs”

- Brought on Jay Askinasi as the head of the advertising business

- He came from Roku, but before that he was the head of digital for Publicis

- 2026 linear advertising guidance

- Expect a more moderate decline versus 2025 due to the combined effects of –

- Expected political spending in 2026

- New ad agency partnerships

- The sale of Telefe and the planned sale of Chilevision

- Expect a more moderate decline versus 2025 due to the combined effects of –

There Are No “Must Haves” M&A Wise

- When asked about potential M&A the Co said there is no “must haves” for them

- They evaluate buying vs building, and they have what they need to build

- They believe they can hit all their goals in streaming and enterprise efficiency through building

- But they have the balance sheet to be opportunistic when thinking about M&A

- It is a question as to whether a deal will accelerate their goals

- But are also long-term disciplined owner operators

- Separately, the Co is also looking to divest smaller assets(reduces their workforce by an addtl ~1,600 employees)

- They have divested Televisión Federal, or Telefe, in Argentina

- They are in the process of divesting Chilevision in Chile, which they expect to complete in Q1 2026

- “You will periodically see us divest smaller assets”

- The Co is also focused on becoming investment grade across all three agencies

Some Mixed Signals Pertaining To Holiday Shopping Expectations Emerge This Week

Holiday spending forecasts for 2025 (at this stage) are sending mixed signals as retailers and consumers gear up for the critical November–December period. The National Retail Federation (NRF) is projecting the strongest holiday season on record, with sales expected to surpass $1 trillion for the first time, growing between 3.7-4.2% y/y. However, this is down from the +4.2% y/y growth rate in 2024 and spend per person is expected to be down. The Conference Board’s latest survey also shows that shoppers are planning to “tighten their belts,” with intended holiday spending falling across both gifts and non-gift categories and inflation-adjusted budgets hitting multi-year lows. Sentiment has also weakened amid ongoing tariff pressures, a government shutdown, and rising job-loss expectations.

Against this backdrop, major retailers such as Amazon, Nintendo, and Target are preparing by rolling out early discounts, expanding low-cost assortments, and introducing new AI shopping tools to capture demand even if consumers ultimately lean toward value-driven spend.

While the holiday spending picture is up for debate, we will carefully track additional data points on shopping trends and consumer behavior as we progress into this important period…

See more color on the need to knows from this week on this theme.

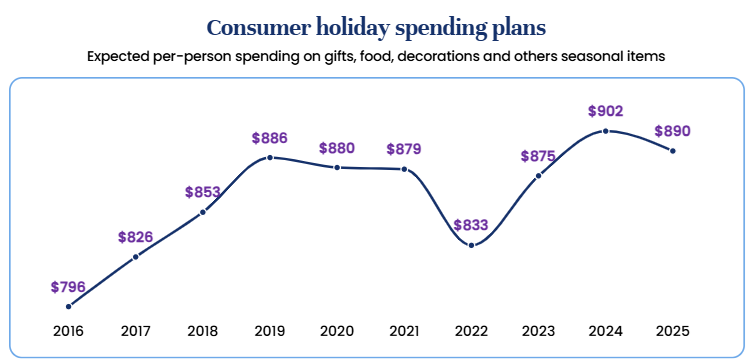

The NRF Predicts Holiday Sales To Top $1 Trillion For The First Time But Y/Y Growth Is Down & Consumers Are Expected To Individually Spend Less

- NRF’s holiday forecast is based on economic modeling using indicators including consumer spending, disposable personal income, employment, wages, inflation and previous monthly retail sales releases

- The calculation excludes automobile dealers, gasoline stations, and restaurants to focus on core retail

- NRF defines the holiday season as Nov 1-Dec 31

- Consumers are expected to spend ~$890 each, the 2nd highest amount in the surveys 23-yr history

- But this is down from 2024 spending of $902 per person

- It is predicted that sales in Nov-Dec will grow between +3.7-4.2%, which translates to $1.01-1.02 trillion

- Last yr’s holiday sales rose +4.3% to reach $976.1bn

- Some key consumer stats include –

- 42% plan to begin browsing and buying for the holiday season before Nov

- The leading reason they shop early is to spread out their budget (54%) or to avoid the stress of last-minute shopping (41%)

- Even with the early start, the majority (60%) anticipate they will finish shopping in Dec

- 85% anticipating higher prices due to tariffs

- 63% plan to wait until Thanksgiving weekend to do most of their holiday shopping (up from 59% last yr)

- 55% plan to make purchases digitally

- That is followed by grocery stores (46%), department stores (44%) and discount stores (42%)

- 42% plan to begin browsing and buying for the holiday season before Nov

- NRF predicts retailers will hire 265-365k seasonal workers, in-line with a slower-paced labor market

- By comparison, there were 442k seasonal hires in 2024

- NRF Chief Economist and Executive Director of Research Mark Mathews added that while seasonal hiring normally supports the job market this time of year, the ongoing tariff situation could be making retailers wait to make staff additions

- At the same time…through Oct, there have been 88,664 layoffs in the industry, up +145% y/y

- By comparison, there were 442k seasonal hires in 2024

The Conference Board Study Also Points To Consumers “Tightening Their Belts” & The Gov’t Shutdown Is A Headwind

- The Conference Board stated that the avg US consumer intends to spend $990 on holiday-related purchases in 2025

- That’s down -6.9% from $1063 in 2024 and close to holiday spending intentions in 2023 ($985), but lower than in 2022 ($1,006) and 2021 ($1,022)

- Consumers intend to spend $650 on gifts this year, down -3.9% from $677 last year and the lowest since 2022

- Meanwhile, budgets for non-gift items (including food, decorations, and wrapping paper) are down -12% at $340

- After adj for inflation, these figures are at $513 for gifts and $268 for non-gift items in constant 2017 dollars, both multi-year lows

- Consumers under 35 are driving reduced spending on gifts in 2025, while those aged 35-45 and 55-64 are driving declines in spending on non-gift items

- Only consumers over 65 are planning to spend more on both gifts and non-gift items this year vs last year

- Consumers earning $75–100K and those earning over $125K

- Plan to reduce holiday spending this year

- Consumers earning less than $50K

- Plan to spend a bit more on gifts and non-gift items this year

- Most holiday shopping is planned for Nov to capture Black Friday deals after Thanksgiving: But almost 40% of consumers will continue to shop in Dec

- Less than 10% of consumers started their holiday shopping in the first half of 2025, suggesting little evidence of advance purchases ahead of tariffs

- Buying gifts online remains widely popular

- 43% of consumers expect to purchase at least half of their gifts online this yr, unchanged from 2024

- 54% for consumers earning over $125K

- 9% do not plan to buy any gifts online

- 43% of consumers expect to purchase at least half of their gifts online this yr, unchanged from 2024

- The federal govt shutdown may also be a headwind this year

- According to the University of Michigan, consumer sentiment fell this month to the lowest level since June 2022

- Consumer sentiment fell ~6% this Nov, led by a -17% drop in current personal finances and a -11% decline in year-ahead expected biz conditions

- For the 3rd consecutive month, consumers’ expectations of losing their job within the next year rose to 43% in Oct

Amazon, Nintendo & Target Are Preparing For Lower Price Points In Several Cases

- Nintendo’s upcoming Black Friday sale includes up to $30 off Switch games: As well as temporary price cuts on its amiibo figures, and a $20 off discount on microSD Express cards that are only compatible with the Switch 2

- If shopping on the Switch or Switch 2, deals start Nov 20th – Dec 3rd

- Physical retailers will offer deals starting Nov 23rd

- Finally, starting November 30th, Nintendo stores in New York and San Francisco, along with select retail stores, will offer $20 off Samsung microSD Express cards

- Amazon on Friday said it expanded its low-cost e-commerce service Amazon Bazaar (known as Haul in the US) to 14 additional markets

- Amazon Bazaar, which launched in Mexico last yr, will deliver most products priced under $10 and some as low as $2 to its newest markets, ranging from home goods to fashion

- Some of the newer markets include:

- Hong Kong

- Philippines

- Nigeria

- Taiwan

- Since launching in Mexico, Bazaar expanded to Saudi Arabia and the UAE

- Shein and Temu have also ramped up expansion outside the US

- Shein operates in ~160 countries including the U.S., Brazil, Ireland, and Southern China

- Temu ships to ~70 countries

- Target is slashing prices on 3,000 items for the holiday season

- The price savings are coming to food and beverage and household goods

- Also brought back its Thanksgiving meal, with a complete holiday dinner for less than $5 per person

- Separately, they launched a new AI-powered tool to help with holiday shopping

- Called the “Target Gift Finder” the mobile app providing tailored recs based on shoppers typing a few details about the recipient into the app

- The retailer also has added list-to-cart scanning, allowing shoppers to scan handwritten lists into the Target app

- The app also includes Smart navigation, which helps guide guests through the aisles, and if an item isn’t available, Store Mode connects to alternate fulfillment methods, including same-day or next-day delivery in eligible markets

- Though Target is not the first, Walmart also released their new AI experiences to help shoppers this holiday season: Some features include in-store savings locator, wish lists, navigation and 3D product visualization

- The price savings are coming to food and beverage and household goods

Sources: Retail Dive (11/10), The Verge (11/10), PR Newswire (11/10), Retail Dive (11/10), NFR Press Release (10/16), Yahoo Finance (10/12), Target Press Release (11/11), Touch Points (11/7)

Temporary Data Center Delays Put A Damper On CoreWeave's Results

Sometimes, it takes just one bad apple to spoil the bunch. Or in CoreWeave’s case, one data center delay to overshadow progress at all its other data centers. At least that was the sentiment from analysts in reaction to CoreWeave’s Q3 report this week. The Co reported a temporary delay at a third-party data center developer, which led to them lowering FY25 guidance for revenue, operating income, and CapEx. Mgmt tried to mitigate investor concerns by noting that the impacted customer has agreed to extend their contract, preserving the full value, and that the majority of the delay is expected to be resolved by Q1 of next yr. They also highlighted several steps they have already been working on to manage the “challenging” environment, including diversifying data center providers (no single provider represents more than ~20% of contracted power) and expanding self-build efforts to gain operational control. Overall, the delay is par for the course of building out capacity, and as CoreWeave continues to scale, delays at any single site will have less impact. This is an industry issue, not specific to just CoreWeave, and will likely persist in the foreseeable future as the Co continues to build out infrastructure to meet the overwhelming demand it it seeing.

Outside of the delay, Q3 top-line growth was strong, with revenue and adj EBITDA above estimates, though margins were slightly lighter (61.4% vs consensus 62.9%). CoreWeave continues to diversify its customer base, and as of Q3, no single customer represents more than ~35% of revenue backlog, down from ~50% last quarter and ~85% at the start of the yr.

On the data center and capacity front, growth also continues. Their active power footprint expanded +120 MW q/q to ~590 MW, and contracted power capacity grew +600 MW to 2.9 GW, with 1 GW expected to come online in the next 12–24 months. They also added 8 new data centers in the US, with further expansions in Europe underway. Self-build projects are progressing in parallel, providing addtl operational control, though mgmt emphasized that it is “an additional piece of the puzzle” and is supplemental, not a replacement, to their partnerships with third-party providers.

Mgmt also briefly touched on the terminated Core Scientific deal, saying that they will continue to work closely with them, though when asked if the Q4 delay was related to the deal termination, they sidestepped the question.

While investors were certainly spooked by the delay, mgmt tried their best to explain that it is part of scaling what is a highly supply-constrained biz and that they are taking steps, including diversification, self-build, and fungible infrastructure, amongst others, to help mitigate. See below for more.

-> CoreWeave plunged -16.3% in reaction to its print and ended the week down -26%; That said, since its IPO back in March, the stock is up a massive +93.4%

Q3 Mostly Beat On The Top-Line, Though Adj EBITDA Margins Were A Bit Below Expectations

- Rev grew +134% y/y (vs +207% y/y in Q2)

- Rev backlog grew +271% y/y (a huge accel from +86% y/y in Q2)

- Adj. EBITDA beat by +3.2% BUT margins came in light at 61.4% vs cons 62.9%

- EPS of -22c came in well ahead of cons -40c

- Cash from operations was a strong +84.3% ahead of estimates

CoreWeave Continues To Operate In A “Highly Supply-Constrained Environment”

- Demand for CoreWeave’ cloud platform “far exceeds” available capacity

- Added $25bn+ in rev backlog in Q3, bringing them to $55.6bn in rev backlog at the end of Q3 (almost double Q2 and approaching 4x YTD)

- Also reached $50bn in RPO (remaining performance obligations) faster than any cloud in history

FY25 Guidance Lowered Across The Board Due to A Temporary Data Center Delay

- Now expect LOWER rev for FY25…: $5.05-5.15bn vs prior guidance of $5.15-5.35bn

- …and LOWER op income for FY25: $690-720mn vs prior guidance of $800-830mn and cons $802.8mn

- …as well as LOWER CapEx for FY25:$12-14bn vs prior guidance of $20-23bn

- “Vast majority” of the remaining CapEx previously anticipated to land in Q4 will now be recognized in Q1

- Looking ahead – expect 2026 CapEx to be “well in excess of double that” of 2025: Given the “significant” growth in their backlog and continued “insatiable” demand for their cloud svs

- Q4 will be negatively impacted by temporary delays related to a 3P data center developer that has fallen behind schedule

- BUT the impacted customer has agreed to extend the contract: Customer has agreed to adjust the delivery schedule to preserve their capacity for the full duration and the total value of the original agreement

- Mgmt sidestepped the question when asked if the delay was related to termination of Core Scientific deal: “I’m not going to speak to any specific one of our data center providers. We’re working with all of our data center providers to do everything we can to facilitate the ultimate delivery of the infrastructure that they’re going to deliver to us”

- The ~40% cut in FY25 CapEx is due to this provider’s delay

- Delay will have NO impact on ability to bring on more clients and the is Co is “parallelizing” the build of the rest of their infrastructure: Have 32 other data centers in their portfolio, all of which are “progressing to one extent or another”

- “This one data center will catch up and then we will move forward from there”

- Have taken “a number of steps” to manage the “challenging” environment and minimize infrastructure delivery delays –

- Diversifying data center providers

- Created a “significant” portion of the Co dedicated to being able to facilitate and assist with the operational component of delivering infrastructure

- Set up their own self-build efforts

- But the problem at the “powered shell level” is an issue across the industry (not just at CoreWeave): “There’s plenty of power right now and we believe that there will be ample power for the next couple of years, but really where the challenge is, is the powered shell”

- “This is a systemic problem that the industry is going to have to deal with for the foreseeable future”

- Also in Q4, will be bringing online some of their largest-scale deployments in Co’s history, which will have a near-term impact on adj op margin

- Due to the timing difference between when data center costs are first incurred and when they start recognizing rev

Focused On Both Expanding And Diversifying CoreWeave’s Rev Base

- As of Q3, have reduced customer concentration “significantly” – no single customer represents more than ~35% of rev backlog, down from ~50% last qtr and ~85% at the beginning of the yr

- Also, 60%+ of rev backlog is now tied to investment-grade customers

- In Q3…

- Executed large-scale compute contracts with “many” of their largest customers, including Meta and OpenAI

- “Each represents a meaningful expansion of existing relationships and a diversification away from any single customer”

- Expanded their relationship with a “leading” hyperscaler, their 6th contract with this customer to date

- Executed large-scale compute contracts with “many” of their largest customers, including Meta and OpenAI

- Overall, 9 of their 10 largest customers have now executed multiple agreements with them, the only exception being a new customer that was onboarded in Q3

- “Our exceptional growth illustrates just how quickly AI adoption is progressing beyond the frontier AI labs and hyperscalers”

- # of customers that exceeded $100mn of rev over the LTM tripled y/y

Their Power and Data Center Footprint Expands As Self-Build and Fungible Infrastructure Diversify Offerings and Boost Capacity

- On the capacity front in Q3…

- Expanded their active power footprint by +120 MW q/q to ~590 MW

- Grew contracted power capacity by 600+ MW to 2.9 GW

- “Well-positioned” for future growth, with 1 GW of contracted capacity available to be sold to customers that is expected to largely come online within the next 12-24 mos

- No single data center provider represents more than ~20% of their contracted power portfolio

- As the Co grows and operates more data centers, delays at any single site will matter less and less to the overall biz: I.e., when they’re managing 2.9 GW of capacity, a delay at one 100-MW site won’t really affect results

- On the data center side in Q3…

- Added 8 new data centers across the US w/ addtl expansions underway across Europe

- Continue to embark on self-build projects to further accelerate their footprint and provide greater operational control

- Self-build strategy is another way to de-risk delivery across their broader portfolio: Will continue to work with their partners who provide data center capacity, but self-build will be an “additional piece of the puzzle”

- “We just think that you need to be on both sides of this fence in order to be as effective as you can be de-risking what is a complicated supply chain environment”

- Can AI customer capacity be reused if demand shifts? Building out infrastructure so it is fungible and can be transferred from one client to another

- Infrastructure is built to the “most demanding” specs, so it supports both training and inference workloads, while maintaining as much optionality and flexibility as possible

- NVIDIA deal is an example of mitigating overcapacity risk: Allows for the capacity contracted and reserved for NVIDIA to be interrupted and resold to different customers, particularly smaller customers, such as high-growth AI labs that prefer shorter and lower upfront commitments

- “The interoperability here is an incredibly powerful tool for the resiliency and opportunities for new companies to become part of CoreWeave’s broader offering”

Continue To Expand AI Capabilities Through Strategic M&A And Partnerships

- “…we are expanding our addressable market and growing with our customers. We are fundamentally evolving the capabilities of CoreWeave, which is creating beachheads and expansion opportunities into new markets”

- On previously proposed acq of Core Scientific, which was terminated in October:Made sense “strategically” for both Cos BUT the valn Core Scientific wanted was not a price that was “appropriate” for CoreWeave

- “Particularly because the outcome of the transaction in no way adversely impacts our ability to achieve our growth ambitions in the coming years”

- But NOT the end of the relationship w/ Core Scientific: Will continue to work “closely” w/ them on the ~590 MW of capacity they have already leased

- Have been expanding beyond building and training AI models to helping Cos actually put AI to work, and using M&A to do that, including the recently announced acquisitions of OpenPipe, Marimo, and Monolith.

- Also leveraging strategic partnerships to drive growth and enter new mkts

- CrowdStrike partnership will “unlock and accelerate” partner-driven growth

- Storage product and partnership with VAST Data both broadens their offerings and enables entry into markets where they previously had limited/no presence

More & More Players Are Making A Bet On The Prediction Markets

The flood of activity in the prediction markets shows no signs of slowing down and is entering the main stage as major players across sports, media, and fintech prepare U.S. launches and announced high-profile partnerships. The flood of updates this week include 1) Polymarket, FanDuel, and PrizePicks all unveiling significant moves that signal growing acceptance and accelerating competition in the event-contracts space; 2) Polymarket gearing up for a formal U.S. return with live beta testing and a landmark partnership with TKO’s UFC and Zuffa Boxing; 3) FanDuel pushing into the sector with a new standalone app built in partnership with CME Group; 4) PrizePicks becoming the first sports entertainment operator registered as an FCM, enabling a broad rollout of Kalshi-powered markets; and 5) Fanatics exploring an entry into the space via talks with Crypto.com. Together, these developments underscore how prediction markets are rapidly evolving from niche use cases into a federally regulated, multi-platform consumer product.

See below for more on what we thought was important this week along these lines…

Polymarket Is Preparing For Its Reentry Into The United States With Its Beta Testing & A New TKO Deal

- The Co began live testing its US exchange, onboarding a slice of users and matching real trades

- A limited group of users are onboarding as part of a beta phase, Bloomberg reported Wed

- The exchange is fully functional for select accounts

- A limited group of users are onboarding as part of a beta phase, Bloomberg reported Wed

- Outside of beta testing the Co signed a “first-of-its-kind” deal with TKO

- TKO annc’d a multi-yr partnership in which Polymarket will become the Official and Exclusive Prediction Market Partner of UFC and Zuffa Boxing

- The agreement makes UFC and Zuffa Boxing the first sports orgs to integrate prediction market technology directly into the live fan experience

- Polymarket will create a new storytelling metric, visualizing fan sentiment that “complements, not competes” with, regulated sports betting

- Polymarket will power the first-ever real-time Fan Prediction Scoreboard within UFC broadcasts

- UFC and Polymarket will also collaborate on a new custom social series entitled Matchup Predictions – who’s next?

- It will run across official UFC Facebook, Instagram, Threads, and X channels following UFC events

- Who’s Next? will highlight potential matchups for top UFC fighters

- The speculative nature of these posts will “spark social debate and engagement”

FanDuel Has Also Been Active, Launching Their New Predictions Market Platform With CME Group

- FanDuel Predicts will launch in Dec as a standalone mobile app

- The app will provide access to sports event contracts across baseball, basketball, football, and hockey

- In states where online sports betting is not yet legal, customers will be able to trade event contracts on the outcome of sporting events

- As new states legalize online sports betting, FanDuel will cease offering sports event contracts in those states

- In addition to sports, event contracts will be offered on benchmarks such as the S&P 500 and Nasdaq-100, prices of oil and gas, gold, cryptocurrencies, and key economic indicators such as GDP and CPI

Finally, PrizePicks Launched Their Offering With Kalshi

- PrizePicks annc’d the launch of its prediction markets offering through its subsidiary, Performance Predictions II and a multi-yr partnership with Kalshi

- Customers on PrizePicks are now able to make predictions on sports, entertainment, and pop culture directly within the PrizePicks app through Kalshi’s library of event contracts

- All event contracts listed on PrizePicks are Kalshi markets

- At launch, PrizePicks will offer Team Picks and/or Culture Picks in 38 states and Washington, D.C.

- Team Picks: For the first time on PrizePicks, customers can predict team outcomes, from individual matchups to season-long futures like win totals, playoff chances and championship winners

- Culture Picks: For the first time, PrizePicks is also expanding beyond sports, allowing customers to predict the outcomes of the biggest cultural events and pop culture storylines

- From who will win Best Picture or Album of the Year to the outcome of the next election

- Additionally, PrizePicks recently became the first sports entertainment operator to be registered as a Futures Commission Merchant (FCM) by the National Futures Association (NFA)

- This allows PrizePicks to offer prediction markets in partnership with federally regulated Designated Contract Markets (DCM), ensuring customers can engage with confidence in a safe, compliant environment

-> Fanatics is also reportedly in talks to partner with Crypto.com to make a push into prediction markets but talks “are in early stages and could still change”

Sources: TKO Press Release 11/13, Yahoo Finance 11/12, PR Newswire 11/12, New York Post 11/13, SBJ 11/14, PR Newswire 11/14

A Handful Of Other Key Media Entertainment Updates Across Studios, Streaming, Sports, Games, Experiential, And More...

It seems like the news coming out of the media entertainment sector refuses to let up with a plethora of announcements, launches, milestones, and speculations hitting the tape this week. Discussions around the future of Warner Bros Discovery’s appear to be advancing, though the Co still seems to be moving ahead with day-to-day operations, including a newly announced partnership with WEBTOON for webcomic adaptations. Sports’ growing importance in streaming was underscored by new Parks Associates data, and MLS will now be getting more reach on AppleTV. Advertising, also another key pillar of streaming, continues to scale, w/ Amazon reporting 315mn monthly viewers on its ad-supported tier. And rounding out the week, Netflix continues to broaden its offerings and announced the release of Netflix Party Games and the opening of its first Netflix House in Philadelphia.

See below for the quick updates.

While Buyers Circle, WBD Keeps Expanding Its Content Pipeline

- An update on the WBD saga…Paramount, Comcast, and Netflix are reportedly preparing bids for Warner Bros Discovery, per The Wall Street Journal

- Reported timeline –

- The initial deadline to submit nonbinding first-round bids is Nov. 20, some of the people said

- WBD is holding the auction process in the hopes of having it completed by the end of the yr, the people said

- What Cos are reportedly interested in what parts of WBD?

- Paramount remains committed to buying the entire Co

- Comcast and Netflix are primarily interested in the Warner Bros. movie and television studios and the HBO Max streaming svs, but not its cable network holdings

- Reported timeline –

- WEBTOON Entertainment and Warner Bros. Animation annc’d a strategic partnership to co-produce 10 webcomic adaptations for global distribution

- Projects are to be selected from the Co’s Korean- and English-language platforms, with development support from WEBTOON Entertainment’s U.S.-based Webtoon Productions and Japanese IP biz teams

- Plans are still in early stages: The projects could be films or series, and no release dates have been targeted yet

- How will deals w/ creators be structured? The creators of the original WEBTOON webcomics will own the IP and, under their agreements with the Co, will receive a share of rev generated from the animation projects

- Not the first adaptation deal WEBTOON has made: Other WEBTOON Entertainment adaptations are available on Netflix, Amazon’s Prime Video, Sony’s Crunchyroll and some other platforms

MLS Looks To Get More Reach… Apple TV Brings All MLS Matches Into Its Core Svs

- Apple TV will include all Major League Soccer (MLS) matches for no extra cost worldwide starting in 2026

- Under a revision to the 10-yr deal Apple and MLS made in 2022, beginning in 2026, all MLS matches will be available to stream for Apple TV subscribers at no addtl cost

- Viewers will be able to access all regular-season matches, Leagues Cup tournament, the MLS All-Star Game, Campeones Cup and MLS Cup Playoffs with a standalone Apple TV subscription

- Dropping the MLS Season Pass: The MLS Season Pass as an addtl package within Apple TV will officially conclude at the end of the 2025 season

- As a reminder, the MLS Season Pass was most recently priced at $14.99/mo or $99/season (which was in addition to Apple TV’s subscription price of $12.99/mo)

- Also as part of the revised deal, MLS club season ticket members will receive a full Apple TV subscription as part of their 2026 full-season ticket membership (one per paid season ticket account).

- MLS will be joining Formula 1 and Major League Baseball as offerings within the overarching Apple TV catalogue of sports that are available at no addtl cost

- Under a revision to the 10-yr deal Apple and MLS made in 2022, beginning in 2026, all MLS matches will be available to stream for Apple TV subscribers at no addtl cost

Ad-Supported Video Streaming Continues To Grow

- Amazon’s Prime Video w/ Ads reach 315mn monthly viewers

- That is up from 200mn back in April 2024, according to self-reported data from Amazon

- How is viewership measured? Represents the unduplicated avg monthly active ad-supported audience across original and licensed series and films, live sports and events, and free, ad-supported live channels on Prime Video

- As a reminder, Prime Video has now launched in 16 countries

- Amazon annc’d the #s just a few days after Netflix shared it has 190mn monthly viewers on its ad-supported tier

Netflix Continues To Broaden Offerings W/ Two Non-Video Streaming Related Launches This Week

- Netflix releases Netflix Party Games, which lets users play casual games on their TV using just their phone and a Netflix subscription; It currently includes five games (LEGO Party!, Boggle Party, Pictionary: Game Night, Tetris Time Warp, and Party Crashers: Fool Your Friends) that groups can easily play on their TV screen

- First-ever Netflix House is now open in Philadelphia: The 100,000-sq-ft venue has a mini-golf course, restaurants, a movie theater, and lots more, in addition to immersive experiences inspired by Netflix’s TV shows and movies; Netflix House is free to enter and explore, though the venue does have some ticketed experiences, which start at $15

- The next Netflix House is set to open in Dallas in December

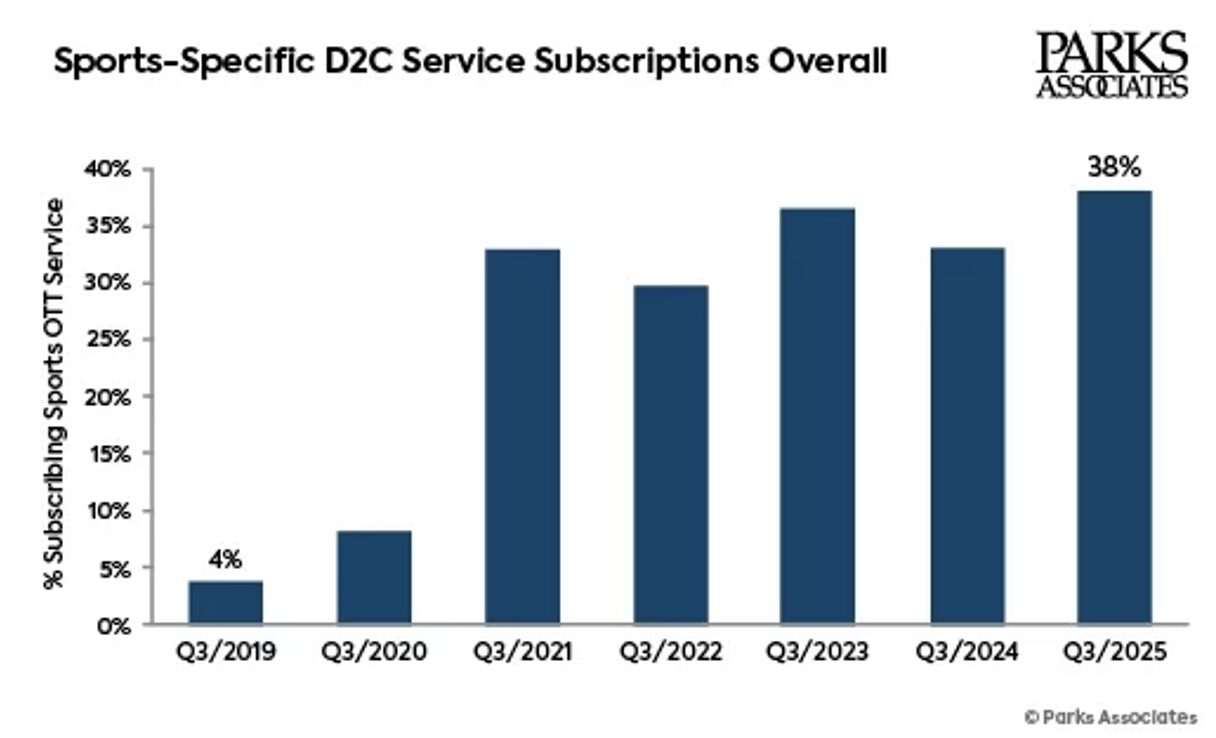

New Data On Sports Streaming Service Uptake…

- Quick stat spotlight – 38% of US internet households subscribe to at least one sports-specific streaming service, per Parks Associates

- This is up from just 4% in 2019

- The NFL is the most popular sport, with 82% of sports viewers in US internet households regularly watching NFL content during the season

- Pure-play streaming platforms, + hybrid agreements w/ platforms now account for b/w one-qtr to one-third of the NFL’s total broadcast rev

Sources: The Wall Street Journal (11/13), Netflix (11/13), ESPN (11/13), Variety (11/13), Variety (11/12), Deadline (11/11), Parks Associates (11/11), Deadline (11/5)

Competition Isn't Emptying Instacart's Cart As Feared

Rounding out the last-mile delivery names this earnings season was Instacart, which reported results this week in its first earnings call under new CEO Chris Rogers. Having spent six yrs at the Co, most recently as Chief Business Officer, he emphasized that he does not plan to make major changes to Instacart’s core strategy. Instead, he outlined three focus areas that will guide the company into its next chapter: affordability, accelerating enterprise growth, and continued investment in advertising and data.

The Co delivered Q3 results that were largely in-line with expectations, with a modest beat on the top-line, though Advertising & Other was a bit of a drag. Mgmt expects some continued pressure on ad growth in Q4 as large brands adjust spend in response to macro uncertainty, but he did flag that October trends so far have been “strong”. Despite potential near term headwinds, he is confident in the long-term goal of advertising reaching 4–5% of GTV.

Competition was a big focus amongst analysts on the call given Amazon’s recent launch of same-day fresh food delivery and DoorDash’s expanded partnership with Kroger, among other competitive moves. Instacart maintains that it is playing a different game, continuing to lead in large basket grocery orders above $75, which account for ~75% of the online grocery market (vs Amazon and DoorDash, which tend to focus on smaller baskets). They have not seen a shift in basket mix and highlighted that unit economics remain positive across ALL order sizes. Additionally, on retail partnerships, they stressed that retailer exclusivity is not essential to its strategy, but rather the depth of those partnerships.

All in all, mgmt was largely able to abate investor concerns around competition and the business seems to be moving along as expected. See below for more on the above, as well as addtl color on the oppty in international, AI strategy, regulatory happenings, and more.

-> Instacart was down as much as -5% as a knee jerk reaction to earnings but ended the day up +1.5%; The stock is down -1% YTD

-> Separately, but related, Airbnb is testing a new svs w/ Instacart that will let guests at some US rentals order groceries through its app ahead of and during their stay; The 3-mo pilot program (starting Jan. 5th) is open to select hosts with available listings in Phoenix, Orlando and Los Angeles, and guests will be allowed to place an Instacart order within the Airbnb app up to 3 weeks before their stay (Source: Bloomberg 11/12)

Q3 Beat On The Top-Line, Though Advertising Was Slightly Weaker Than Expected

- Q3 rev beat by +0.6%: Grew +10% y/y (vs +11% y/y in Q2)

- Transaction rev beat, while Advertising & Other missed

- Q3 Adj EBITDA margin of 29.6% was ahead of cons 28.7%

- Q3 GTV, Orders, and AOV were all in-line/slightly ahead of cons

- AOV fell -4% y/y due to restaurant orders and lowered basket minimums to $10 for Instacart+ members to get waived delivery fees

- The Co also authorized $1.5bn increase to their share repurchase program

Q4 Guidance Was ~ Where The Street Expected

- Q4 GTV – modestly BEAT by +0.5%: $9.45-$9.6bn vs cons $9.48bn

- Implies y/y growth of +9-11% (vs +10% in Q3), with orders growth expected to outpace GTV growth

- Puts and takes: Reflects “strong” performance in October, and continued momentum w/ enterprise partnerships, partially offset by the expected impact of EBT SNAP funding scenarios on their biz

- Q4 adj. EBITDA – ~in-line: $285-$295mn vs cons $289mn

- Q4 Advertising & Other rev expected to grow +6-9% y/y

- Reflects ongoing strength from emerging and mid-sized brands, partially offset by some large partners adjusting spend as they manage macro uncertainty and changing consumer trends

- Expected impact from EBT SNAP? EBT is a “relatively small” part of the overall biz and mgmt. expects to achieve guidance regardless of how things play out

There Were Some Uncertainties Around How The Brand Advertising Landscape Will Shape Up In Q4

- “Not satisfied” with the Q4 guide and “focused” on reaccelerating Advertising & Other rev

- Called out some puts and takes –

- Have been seeing “real ongoing strength from mid-market and emerging brands” all yr

- BUT some of their large brand partners are moderating spend as they navigate a tougher macro environment

- ALSO in Q4, they’re up against some brands that “leaned in heavily” towards the end of last yr

- Looking ahead – the Co is “confident” in its ability to return to double-digit advertising growth next yr (was up +10% y/y in Q3 and +12% y/y in Q2) and ability to achieve long-term target of 4-5% of GTV

- How will they get there? Constant innovation across the platform to attract increasingly larger budgets

- This includes new ad formats, enhanced optimizations (such as ad relevance systems powered by LLMs), cont’d expansion of the ads ecosystem and partner pipeline, new in-store surfaces like Caper Carts, and growing off-platform partnerships

Mgmt Outlined 3 Focus Areas That Will “Accelerate” The Biz Into Its Next Chapter

- Affordability

- #1 reason people churn off the platform and also a barrier to customers placing their first order

- Working with “almost all” of their retail partners on the pricing strategy

- i.e., surfacing deals more aggressively, reducing the markup or offering sale pricing, same as in-store pricing, etc.

- Price parity retailers are growing 10pp faster vs marked-up retailers

- Accelerate enterprise “even more”

- Already in 350+ e-commerce storefronts, but there is room to launch “a lot more” retailers across N. America

- Also an oppty to expand outside of N. America for the first time in a “real way”

- Once they’ve landed w/ a retail partner, oppty to cross-sell (i.e., Caper Carts w/ FoodStorm)

- Ads and data

- Ads biz is “very strong and highly performant” and plan to continue to invest to build an ad ecosystem that “really innovates”

- Includes on-platform, off-platform (through partnerships w/ Google, Meta, TTD, Pinterest, and TikTok), and w/ Carrot Ads

Not Worried About Increased Competitor Activity – “It’s Clear That We’re Playing A Different Game”

- Instacart remains the leader in big baskets ($75+), which still represents 75% of the online grocery mkt

- It’s an area of the mkt that their competitors “don’t really touch” (competitors tend to focus on small baskets)

- NOT seeing a shift in basket composition between small and large baskets / Not seeing any “meaningful” change in AOV

- While large baskets continue to play a “critical role” and growth remains consistent, the Co has also found that by reducing basket size, they’re adding incremental use cases

- “Think about it more as capturing the full set of needs of the consumer”

- Have also been converting small basket users to large basket users “at multiple times higher than others”

- Looking at Amazon specifically – Instacart continues to expand both overall and in mkts where it overlaps with Amazon

- “We’ve proven that we can compete and win in a highly competitive space and we haven’t seen anything in the short term that would change that”

- Also flagged that exclusivity isn’t critical to their strategy – “what matters is the depth of our relationships”

- 80%+ of their business is nonexclusive

- And of the remaining that is exclusive, the majority of those have an enterprise relationship w/ Instacart

“Doubling Down” On Instacart+ Memberships B/c Those Are Their “Best Customers”

- Instacart’s most active customers are Instacart+ members

- Have not seen any competitive impacts in growing Instacart+ members

- Instacart+ members continue to represent a majority of activity on the platform

- And are more engaged and have higher retention that non-Instacart+ members

- Continuing to enhance the value of Instacart+ to drive further membership growth: By extending family accts to 3 members, adding subscriptions (i.e., NYT Cooking), adding restaurants that are eligible for free delivery, etc.

Right Now Is The “Right Moment In Time” To Start Exploring Mkts Outside Of N. America

- See “tremendous” oppty to grow intl

- Have already started to make inroads in Europe and Australia with Wynshop and Caper

- But NOT building new suite of technology specific to these mkts

- Will need to invest in go-to-mkt, but for the most part will take existing technologies (i.e., Storefront Pro, Caper, and FoodStorm) and extend those to intl retailers

- Making sure “we do this in a way that’s aligned with our profitability objectives and our ability to deliver annual EBITDA progression”

Still “Early Days” On AI But Accelerating Innovation And Offerings Across Instacart’s Ecosystem

- Launched AI Solutions in Q3 which is “a collection of enterprise offerings that bring AI-powered capabilities” to their retailers

- “It’s going to connect every part of the shopping journey from how products are discovered online to how shelves are stocked in stores”

- What will drive the monetization oppty? “Smarter operations…better product visibility with the in-store view …[a] more personalized shopping experience” for customers, etc.

- Have had a “very promising start out of the gate” and “believe that this is going to be something we can monetize over time”

- Will also be building out agentic experiences directly on Instacart: Leveraging data from 1.5bn+ orders to date and catalog of 17mn unique items to understand people’s preferences; Also have “the best UX”

- Will extend these capabilities to retail partners through Cart Assistant,enabling them to scale agentic experiences on retailers’ owned and operated websites at the same pace as Instacart’s own marketplace

- Example use cases: Can build a party cart for 10 based on budget or review a basket for allergens

- “We do think we can deliver the most relevant agentic experience for grocery with a great user interface directly on Instacart”

- Will extend these capabilities to retail partners through Cart Assistant,enabling them to scale agentic experiences on retailers’ owned and operated websites at the same pace as Instacart’s own marketplace

- Have also started to surface other AI-driven experiences…

- Smart Shop, which analyzes customer behavior and dietary preferences to surface the most relevant products faster

- Virtual Aisles, which tailor product selections to specific household needs such as baby care, pet items, or dietary preferences

- Personalized Replacements, which recommends alternative products based on dietary needs, pricing, and past purchase preferences

- … “and you’re just going to see that continue to accelerate into the future”

Too Early To Gauge The Impact Of NYC Delivery Wage Changes, Though Instacart Opposes The Regulation

- For some background… NYC Council overrode Mayor Adams’ veto to pass a bill extending minimum earnings standards to grocery delivery workers; Instacart is now engaging with the city in the rulemaking process

- Not supportive of the regulation b/c it comes “at the detriment” of customers, shoppers and retailers in NYC

- Customers could see increased fees

- Shoppers could see fewer earning oppties and could lose the flexibility to choose when and where they shop

- Retailers will likely see fewer orders given the cost increase to consumers

- “To be clear, this is not an outcome that we want to believe is good for stakeholders in New York City” …

- … BUT have dealt with “many” regulatory changes in the past and are “confident” in ability to navigate it and still deliver on their profitability objectives on a Co level

- New York represents “a pretty small percentage” of overall GTV

China Tech Is Investing For Growth, Which Is Pressuring Margins

China Tech was in focus this week as Tencent, JD.com, and TME all reported earnings that delivered mostly strong rev momentum but came in light on margins, which weighed on post-results stock performance. Across the board, the three Cos continued to lean into investment mode, particularly in AI and new biz lines, which is weighing on profitability.

Key quick takes are below, plus the latest on Singles Day (China’s biggest annual shopping event) and Baidu’s new AI product rollouts.

Tencent – Modestly Beats Street Expectations

- Q3 results beat across the board, with the exception of op margin

- CapEx also came in much lower than expected

- Domestic games rev growth decel’d seq (22% of total rev): Q3 rev grew +15% y/y (vs +17% y/y in Q2), primarily reflecting contributions from recently released games such as Delta Force, growth in revenues from evergreen games such as Honour of Kings and Peacekeeper Elite, and the expansion of VALORANT from PC to mobile

- Delta Force: Ranked among top 3 games industry-wide by gross receipts in 3Q; Achieved 30mn+ DAUs in Sept, including 10mn+ million on PC

- HoK: Gross receipts grew y/y in Q3 and DAUs reached 139mn on the game’s 10th anniversary in Oct

- VALORANT: Mobile version released on Aug 19 and became China’s most successful mobile launch YTD by first month DAU and gross receipts; After mobile launch, VALORANT franchise MAUs more than doubled from Jul to Oct, exceeding 50mn; PC DAU and gross receipts reached record high in Sept

- International games rev growth accel’d seq (11% of total rev): Q3 rev grew +43% y/y (vs +35% y/y in Q2) or +42% FXN, due to higher revs from Supercell’s games, recognizing rev upfront on copy sales of new game release, and to consolidation of recently acquired studios

- Clash Royale: Monthly DAU and gross receipts in Sept achieved all-time highs since launch in 2016; Gross receipts increased 400%+ y/y in Q3:25

- PUBG Mobile: Gross receipts increased y/y in Q3

- Dying Light: The Beast: Received “Very Positive” user review scores on Steam since launch in Sept

- Social Networks rev growth of +5% y/y decel’d seq (17% of total rev): Grew +5% y/y (vs +6% y/y in Q2) driven by growth in Video Accounts live streaming rev, music subscription rev and Mini Games platform service fees

- Marketing Svs revs were up +21% y/y(slight accel from +20% y/y in Q2), due to higher ad impressions, benefitting from increased user engagement and ad load, coupled with higher eCPMs, driven by AI-powered ad targeting

- Ad spend increased across all major industry categories in Q3

- FinTech and Business Svs rev were up +10% y/y (in-line w/ Q2)