Summer is over and it is off to the races with an always busy September underway. It was rocky out of the gate post the Labor Day holiday, but the tech heavy Nasdaq ended closing the week up +1.1% (while the S&P 500 closed up only a modest +0.33%). Alphabet was a clear leader, up +10% for the week post the better than feared court ruling on search antitrust remedies (see Theme #1). There was a lot of macro focus on the labor market slowdown which resulted in market expectations moving to three 25bp cuts before YE. Trade headlines were also front and center.

Within the sector, see below for key themes and updates in this edition:

- The Rise of Gen AI Tools Changed the Course Of The Regulatory Hammer On Big Tech

- Data Shows That Specialty SVOD Growth Is Outpacing That Of Mainstream Svs

- The Post Summer TMT Conference Circuit Has Begun! Key Executive Soundbites This Week…

- Which Company Is Looking To Hire The Most AI Engineers? TikTok

- AI Will “Extend” SaaS Vs “Eliminate” SaaS, Per Salesforce CEO Benioff

- Grab Bag: NFL Hits Ad Rev Record / Apple’s Upcoming “Awe Dropping” Event / Lululemon Post-Earnings Plunge

Have a great weekend.

Best,

Leslie

The Rise of Gen AI Tools Changed the Course Of The Regulatory Hammer On Big Tech

It was a sigh of relief for Alphabet investors this week as the verdict regarding remedies associated with Google’s Search antitrust case was finally delivered…and the outcome was positive for the Co. There were minimal penalties and far less severe remedies than feared. Concerns about the Co having to split up and divest Chrome are now off the table. What helped change the course of the case is the rise of gen AI tools that have introduced new ways for users to retrieve information, “challenging” Google’s dominance in traditional search. Judge Amit Mehta said that these new tools “may yet prove to be game changers,” but their emergence made harsh structural remedies less necessary. Interestingly, “Generative AI” and “GenAI” was mentioned 220 times in the remedies ruling and “large language models” (LLMs) were mentioned 82 times.

The outcome of this ruling was an overhang on Alphabet’s stock, hence investors were relieved to move forward with certainty on this front. Now the focus moves purely back to fundamentals…

-> Alphabet shares rallied +9% and Apple’s rose +4% in reaction to the final ruling; YTD, the stocks are up +24% and -4%, respectively while Meta, Amazon, and Microsoft are up +15%, +6%, and +18%, respectively

A Brief History … (link)

- Oct 20, 2020: During President Trump’s first term, the US DoJ filed a lawsuit against Google, alleging it illegally monopolized online search and digital advertising markets

- Aug 4, 2023: Judge Mehta granted partial summary judgment for Google, dismissing some claims but allowing the core “default search” allegations to proceed

- Sept 12, 2023: At trial, Google defended its practices, arguing that it earned its dominant market share by offering users a high-quality service

- Aug 5, 2024: Judge Mehta found Google in violation of US antitrust law, saying that “Google has no true competitor”

- Nov 2024: DoJ proposed remedies, including divestiture of Chrome and Android

- Sept 2, 2025: The final ruling on remedies was issued whereby Google will not be required to sell its Chrome browser

Details From The Final Ruling (link/link)

- The Co won’t have to sell Chrome but it must share search data with rivals

- The court found that the plaintiffs overreached in seeking forced divestitures

- It determined that the Co did not use these assets to effect illegal restraints

- Google is allowed to continue to pay Apple for default search placement, which is obviously a plus for Apple as well

- The Co pays Apple “$20bn annually” according to Morgan Stanley Analysts

- Judge Mehta concluded that cutting off payments would impose substantial, even crippling, harm to partners, related markets, and consumers

- The court found that the plaintiffs overreached in seeking forced divestitures

- The changing competitive landscape with AI worked in Google’s favor

- Judge Mehta noted the competitive landscape for Search is changing rapidly, particularly with the advent of GenAI technologies

- “Tens of millions of people now use GenAI chatbots to gather information that they previously sought through internet search”

- The GenAI market is highly competitive, with numerous new market entrants

- Judge Mehta noted the competitive landscape for Search is changing rapidly, particularly with the advent of GenAI technologies

- While the Co remains dominant, the rise of generative AI and new entrants is already reshaping the market

- Judge Mehta had some final remarks on the matter…

- “The Court must approach the question of remedies with a healthy dose of humility”

- “Renders GenAI a potential threat to Google’s dominance in the market for general search services”

- Judge Mehta had some final remarks on the matter…

- Google is barred from entering or maintaining exclusive contracts for Google Search, Chrome, Google Assistant, and the Gemini app…the Co is prohibited from the following “conditioning” (making one business benefit contingent on another obligation, essentially tying access or payments to extra requirements that favor Google’s other apps)

- Prohibited from conditioning Play Store or other app licensing on distribution, preloading, or placement of Google Search, Chrome, Assistant, or Gemini

- Prohibited from conditioning revenue share payments for one app (e.g., Search, Chrome, Assistant, Gemini) on placement of another

- Prohibited from conditioning revenue share payments on maintaining these apps for more than one year

- Prohibiting partners from simultaneously distributing other GSE (General Search Engine), browser, or GenAI products (prevents Google from forcing exclusivity and ensures rivals can still get distribution)

- Google is subject to data sharing obligations and search syndication rules

- The Co must provide “Qualified Competitors” with certain search index and user-interaction data (but not ads data)

- This remedy is narrowed to only datasets linked to anticompetitive conduct

- The Co must offer “Qualified Competitors” search and search text ads syndication services

- Syndication to occur largely on ordinary commercial terms consistent with current practice

- The Co must provide “Qualified Competitors” with certain search index and user-interaction data (but not ads data)

- The Co will not be required to present a choice of screens or compel Android partners to do so (choice screens = a setup screen on a new device that lets users pick their default search engine like Google, Bing, DuckDuckGo, etc., rather than automatically defaulting to Google)

- Courts avoided remedies mandating product design; choice screens not proven to enhance competition

- Additional rejected provisions from the lawsuit which to Google will not be subject

- No obligation for a nationwide public education campaign

- No requirement to modify policies for publishers’ content use

- No investment reporting requirement

- No anti-retaliation, anti-circumvention, or self-preferencing provisions

While A Big Win For Google, There Are Other Regulatory Actions To Note (link/link)

- The determination on remedies associated with the other DoJ case whereby Judge Brinkema found the Co to hold illegal monopoliesin online advertising technology is still pending; The DOJ is pushing for…

- Unbundling of ad tech services

- Restrictions on data sharing

- Measures to prevent future monopolistic behavior, especially in emerging areas like AI advertising

- Also this week, Google was fined €325mn ($381mn) this week for showing ads to Gmail users and placing cookies without first obtaining proper consent from account holders

- France’s CNIL gave the Co 6 months to stop showing ads in Gmail inboxes without prior consent: Google must ask users clearly and explicitly for permission (“valid consent”) before using their account data for ads

- If not followed, both the Co and its Irish subsidiary will have to pay a penalty of 100k euros per day

- Google is reviewing the decision and counters that “users have always been able to control the ads they see in their products”: Google asserts that it has already taken steps over the past two years to address CNIL’s concerns by:

- Adding an option to decline personalized ads during account creation

- Modifying how ads are displayed in Gmail

- France’s CNIL gave the Co 6 months to stop showing ads in Gmail inboxes without prior consent: Google must ask users clearly and explicitly for permission (“valid consent”) before using their account data for ads

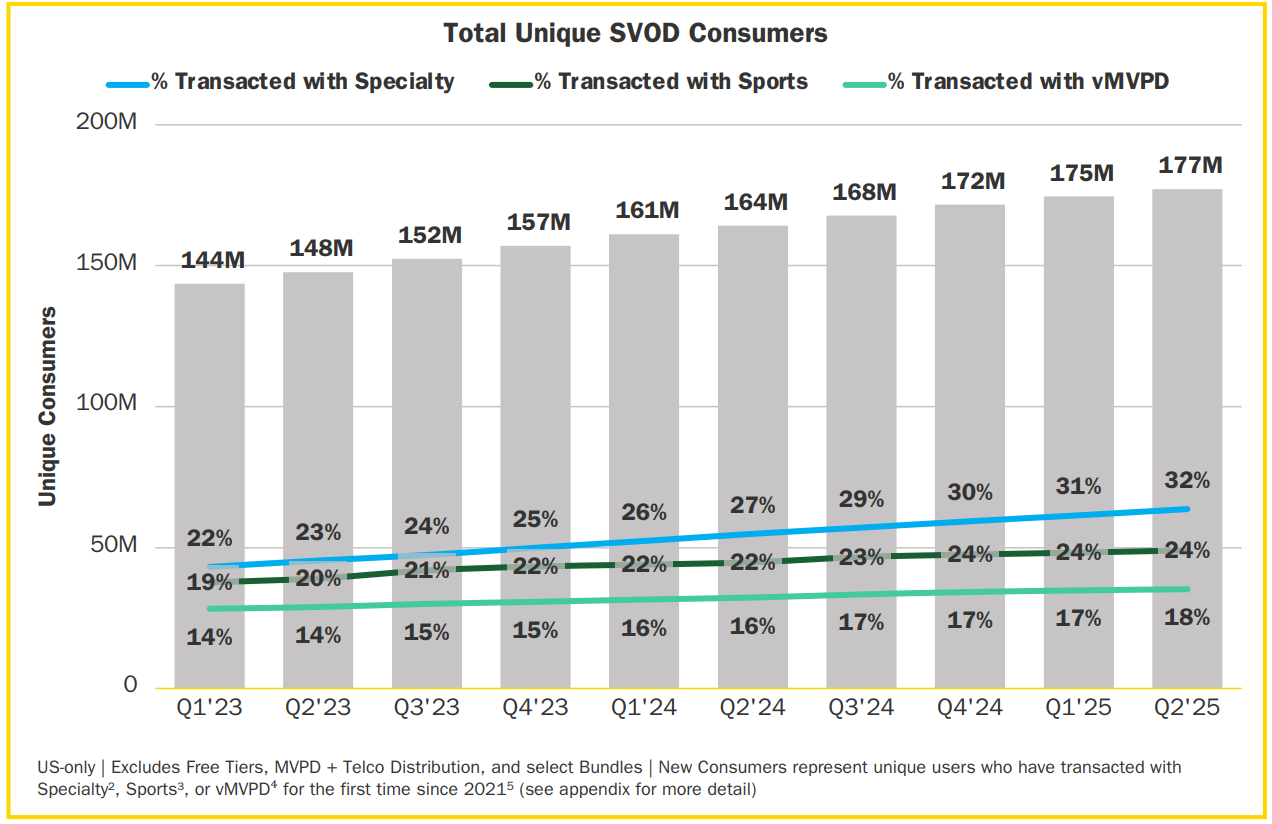

Data Shows That Specialty SVOD Growth Is Outpacing That Of Mainstream Svs

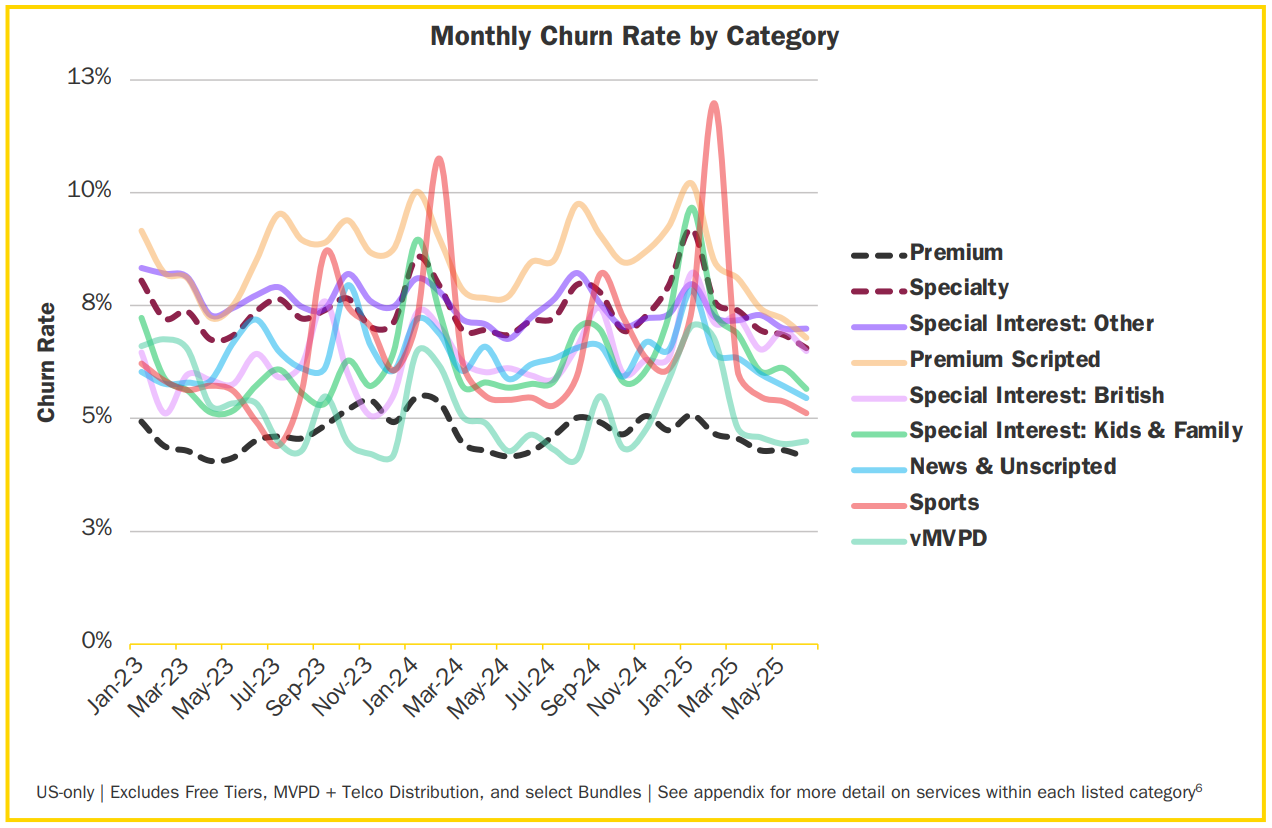

Antenna’s latest State of Subscriptions: Specialty SVOD 2025 report also made the cut this week. It examined the growth and evolving dynamics of Specialty SVOD services within the broader streaming market. Specialty SVODs continue to outpace Premium SVODs in y/y growth, though their pace is slowing, while the share of consumers engaging with Specialty, Sports, or vMVPD services has steadily increased each qtr. Churn rates remain highest in Sports and Specialty categories, though Premium SVODs benefit from a large base of long-term subscribers.

See below for what we thought were the key highlights, and click HERE for the full report.

The Report Breaks Streaming Svs Into 4 Categories –

- Premium SVOD: i.e., Apple TV+, Discovery+, Disney+, HBO Max, Hulu, Netflix, Paramount+ Peacock, Starz

- vMVPD: i.e., DIRECTV STREAM, Fubo, Hulu + Live TV, Philo, Sling TV, YouTube TV

- Sports: i.e., DAZN, ESPN+, FanDuel Sports Network, MLB TV, MLS Season Pass, NBA League Pass, NFL+, NFL Sunday Ticket, UFC Fight Pass

- Specialty SVOD: i.e., A&E Crime Central, Acorn TV, ALLBLK, AMC+, BBC Select, BET+, BritBox, Cinemax, Crunchyroll, CuriosityStream, Gaia, Hallmark+, History Vault, Lifetime Movie Club, MGM+, PBS Documentaries, PBS KIDS, PBS Masterpiece, PureFlix, Shudder, Sundance Now, UP Faith & Family, ViX Premium and Zeus Network

Specialty SVOD Growth Is Outpacing That Of Premium SVODs, But The Pace Is Decelerating

- Premium SVOD Subscriptions grew at +11% y/y in 2024 and +10% into 2025

- Specialty SVOD grew +22% y/y in 2024 and +12% y/y into 2025

The Share Of Total SVOD Consumers Who Have Transacted With Specialty, Sports, Or vMVPD Svs Is Increasing Each Qtr

Churn Rates Are Down Slightly Across Categories

- Specialty, Sports, and vMVPDs have higher churn rates than Premium…

- Premium SVOD Churn is currently 4.1% and has ranged from 4.1% to 5.5% monthly since 2023

- vMVPD Churn is currently 4.5% and has ranged from 4.1% to 7.1% monthly since 2023

- Sports SVOD Churn is currently 5.1% and has ranged from 4.4% to 12.0% monthly since 2023

- Specialty SVOD Churn is currently 6.6% and has ranged from 6.6% to 9.2% monthly since 2023

- …BUT Premium SVOD’s overall churn is reduced by its large base of long-term subscribers, particularly Netflix users

Avg Monthly Churn Rates For Different Sub-Categories Vary Significantly, But The Sports Sub-Category Exhibits The Highest Volatility

The Post Summer TMT Conference Circuit Has Begun! Key Executive Soundbites This Week…

There was quite a bit of chatter this week as companies in the sector addressed investors at a large Wall Street conference. We highlighted the key incrementals we found particularly noteworthy from Warner Bros. Discovery, T-Mobile, Publicis, and Charter which covered strategic moves around spinoffs and debt reduction, as well as synergy expectations, service performance, M&A plans, growth metrics, and more.

Warner Bros Discovery Is Considering Selling A Stake In Its Studio & Streaming Business Before The Spinoff (link/link)

- “We want to get full value for it…we’ve had some serious people asking about ways to get their hands on that,” per WBD CFO Gunnar Wiedenfels: WBD, which is splitting in two, is mulling selling a 20% stake in its studio and streaming biz (Warner Bros.) before the planned separation next yr

- Selling the stake in Warner Bros. is considered a “creative tool in the box” to help reduce debt: Warner Bros has reduced its net debt down to ~$30bn, and it will be “significantly lower at the end of the year”

- Achieving optimal value from a buyer is “definitely going to be a priority,” Wiedenfels said

- The Co has a yr to execute a sale without taking a tax hit

- “We have had some interest and some discussions earlier than that. And technically, we would be able to monetize part of it, all of it, whatever, before we even close the transaction”

- “There’s nothing specific here yet, but definitely something that I’m going to be a lot more focused on over the next few months”

-> WBD closed up +2.3% on the day the news hit the tape and ended the week up +4.0%; YTD, the stock is up +14.6%

T-Mobile Provides Updated Synergy Expectations Following The Close Of UScellular, Along With Addtl Biz Updates (link)

- The Co raised its synergy target w/ UScellular by 20%, now expecting to reach ~$1.2bn in total annual run rate cost synergies upon integration: This is comprised of ~$950mn in OpEx and ~$250mn in CapEx run rate synergies

- The integration is now expected to be achieved in ~2 ys, an acceleration from the original 3-4 yr expectation

- Costs to achieve are expected to be ~$2.6bn, within the original guidance range, and TMUS continues to plan to reinvest a portion of synergies toward “enhancing consumer choice, quality and competition in the wireless industry”

- Stronger core business performance on T-Mobile postpaid net additions is expected to offset the impacts of the initially higher-churning UScellular base

- Overall postpaid & postpaid phone customer guidance for the yr is unchanged at this time as a result

- Expected financial impacts from UScellular acq in Q3…

- Svs rev of ~$400mn

- Core adj. EBITDA of ~$125mn

- ~$100mn in costs to achieve as the Co begins an accelerated integration process, which are excluded from Core Adj. EBITDA, and ~$175mn in D&A expenses

- Acquisition of the lower postpaid ARPA UScellular base, together with postpaid accounts acquired from the Metronet joint venture also with lower Postpaid ARPA, will impact consolidated T-Mobile Postpaid ARPA by ~$1.50

- Excluding UScellular and Metronet, T-Mobile’s underlying biz continues to see “strong” postpaid ARPA growth, with ongoing expectations for full year 2025 versus 2024 growth of at least 3.5%

- Business transformation initiatives and addtl updates…

- Accelerating its move to a more “streamlined and dynamic” billing technology stack in Q3, which will result in an expected ~$350mn in predominantly non-cash costs associated with its digital technology transformation

- Including non-cash impairment expense and accelerated depreciation related to the retirement of software, and personnel costs primarily associated with technology modernization

- Expects its recent acquisitions outside of UScellular, alongside ongoing network investments, to generate an additional $120mn in D&A, integration and other expenses

- Accelerating its move to a more “streamlined and dynamic” billing technology stack in Q3, which will result in an expected ~$350mn in predominantly non-cash costs associated with its digital technology transformation

-> TMUS fell -0.2% on the day of the announcement but ended the week up +0.3%; YTD, the stock is up +14.5%

Publicis Is Bullish on H2 + Not Looking To Do Large-Scale M&A (link/link)

- “We can fairly say that we had a good summer,” CEO Arthur Sadoun said, adding “the marketing cuts that we have discussed in Q2 did not appear”

- Back in July, the Co warned that H2 would be more challenging and could result in cuts to client spending, particularly at the end of the year

- Sadoun also expressed confidence that the Co would achieve its target of 5% growth for organic revenue in 2025

- Publicis is not interested in pursuing large-scale consolidation: “We are not interested in consolidating more of the same for the sake of efficiencies. This was true a year ago, it is even truer today.”

- What they are actually interested in is AI: “With the speed of change AI is bringing, we are only interested in buying capabilities in data, technology, and AI that will enable us to continue to outperform the market and deliver immediate value to our clients”

-> Publicis shares closed up +2.7% on the day the comments were made, the highest since July 29

Charter Expects A Slightly More Challenging EBITDA Trends In Q3 Vs Q4

- Regarding EBITDA trends, “my expectation is that third quarter is actually a little more challenging than the fourth quarter. And [for] some of that is, I think, there are operational efficiencies that we’ll get more of as we get later into the year”, per CFO Jessica Fischer

- But on a full year basis, the Co continues to expect “to grow” EBITDA

- The broadband market “continues to be a competitive space,”

- Expects broadband pricing to remain “pretty resilient… I think we’ll continue to be able to grow rapidly in that space based on the unit economics we have now”

-> Charter was down -0.7% on the day the comments were made and ended the week down -1.5%; YTD, the stock is down -23.7%

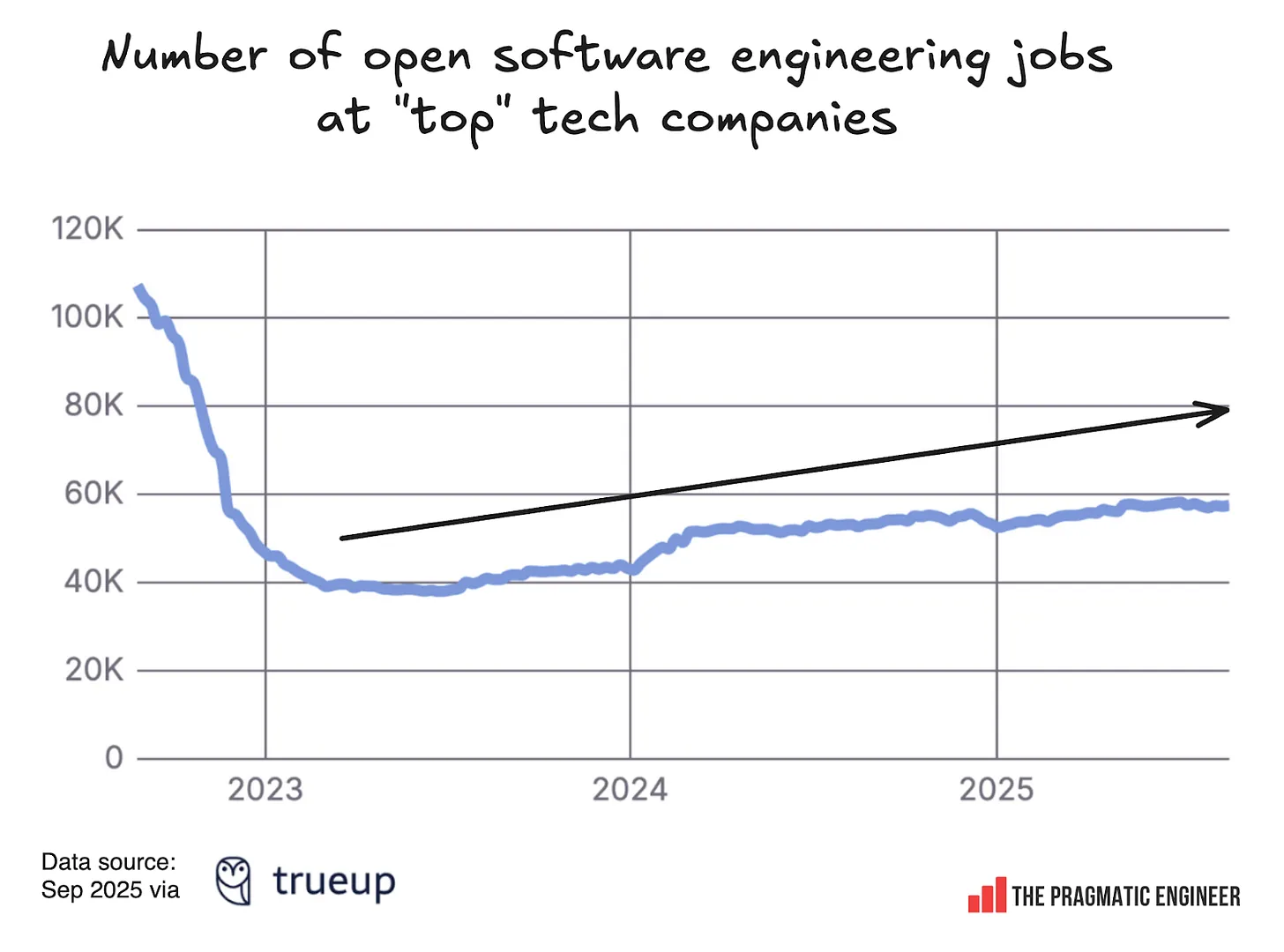

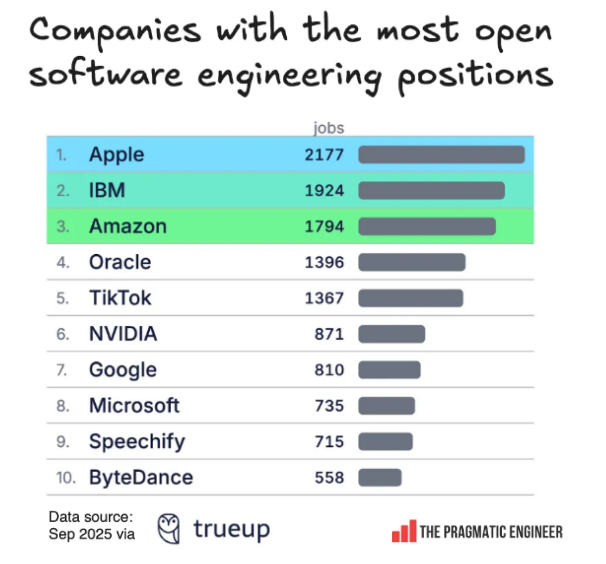

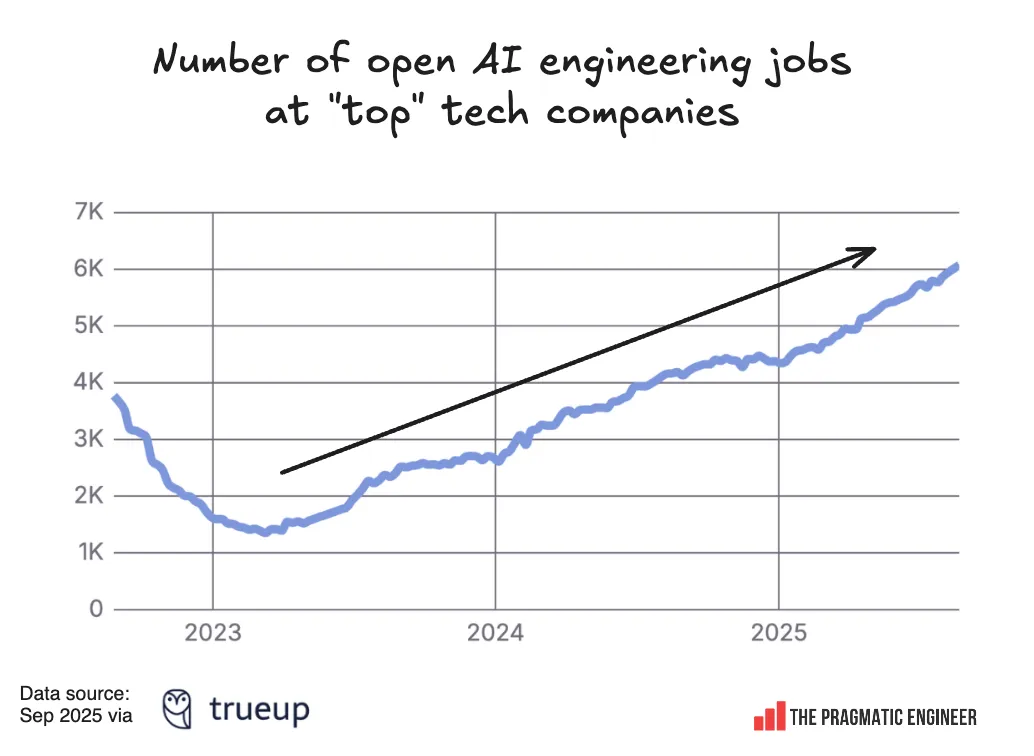

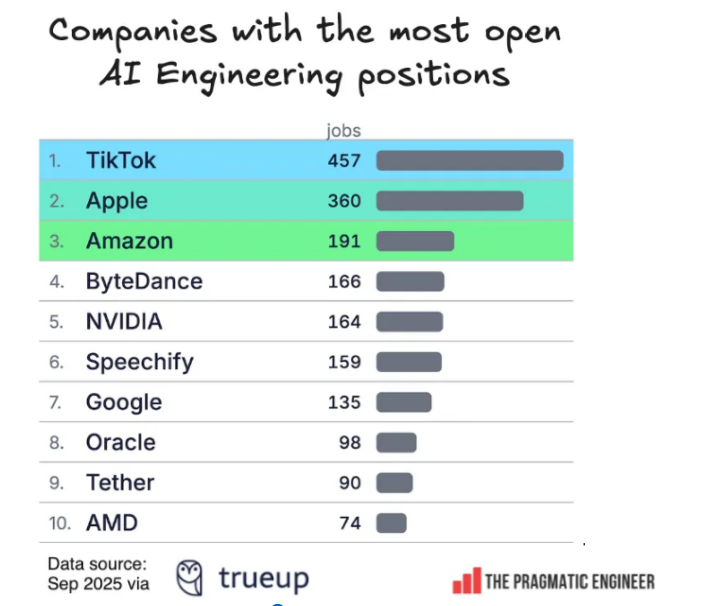

Which Company Is Looking To Hire The Most AI Engineers? TikTok

The health of the jobs market was in focus this week given the release of July job openings, which marked the lowest level in 10 months. Available positions fell to 7.18mn, which was below economists’ 7.38mn consensus estimate (per Bloomberg) and lower than the downwardly revised 7.36mn in June, per the BLS, a division of the US Department of Labor. But one area of the job market that is super hot is for AI engineers! We found an analysis by Pragmatic Engineering on open positions for software engineering had some interesting findings, which includes that TikTok and Apple have the highest number of open positions for AI engineers.

See below for more on what we thought were the top takeaways (link to the analysis).

- Following layoffs in 2022-23, there has been a “slow, steady rise in recruitment” for software engineers across Big Tech & top startups

- Which companies are hiring the most software engineers? Among the Top 5 were Apple, Amazon, Oracle, and TikTok, but perhaps the most surprising was IBM at #2

- IBM is recruiting a large # of backend and generic software engineers, and specialists like AWS DevOps engineers, and SAP/ServiceNow developers

- Surprise, surprise…there has been a massive increase in demand for AI engineers since mid-2023…

- It is interesting to see the slope of demand for AI engineers vs software engineers

- Who is looking to hire the most AI engineers? TikTok, Apple, Amazon, ByteDance, and Nvidia are the Top 5

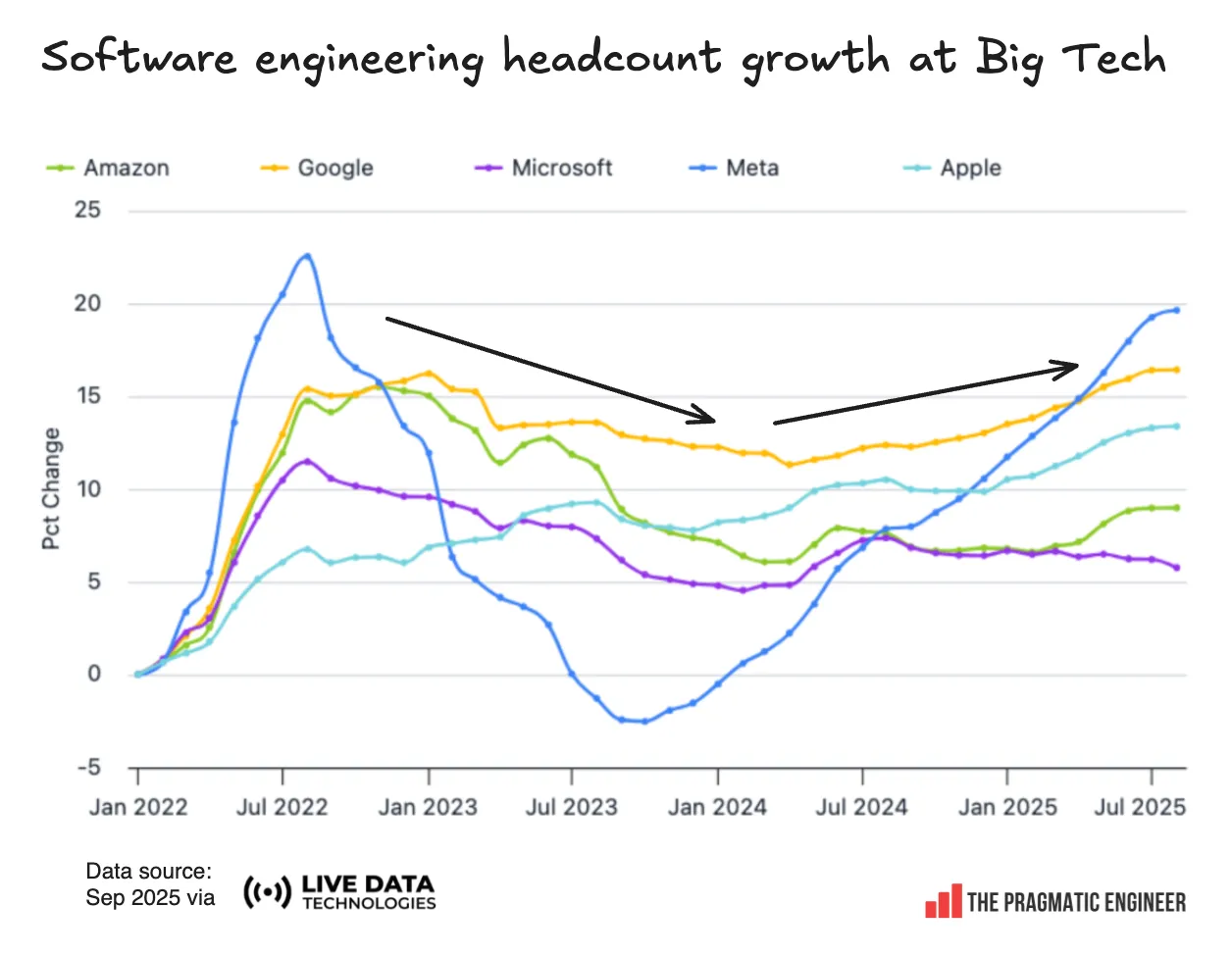

- Tenure of engineers is rising fast at Big Tech

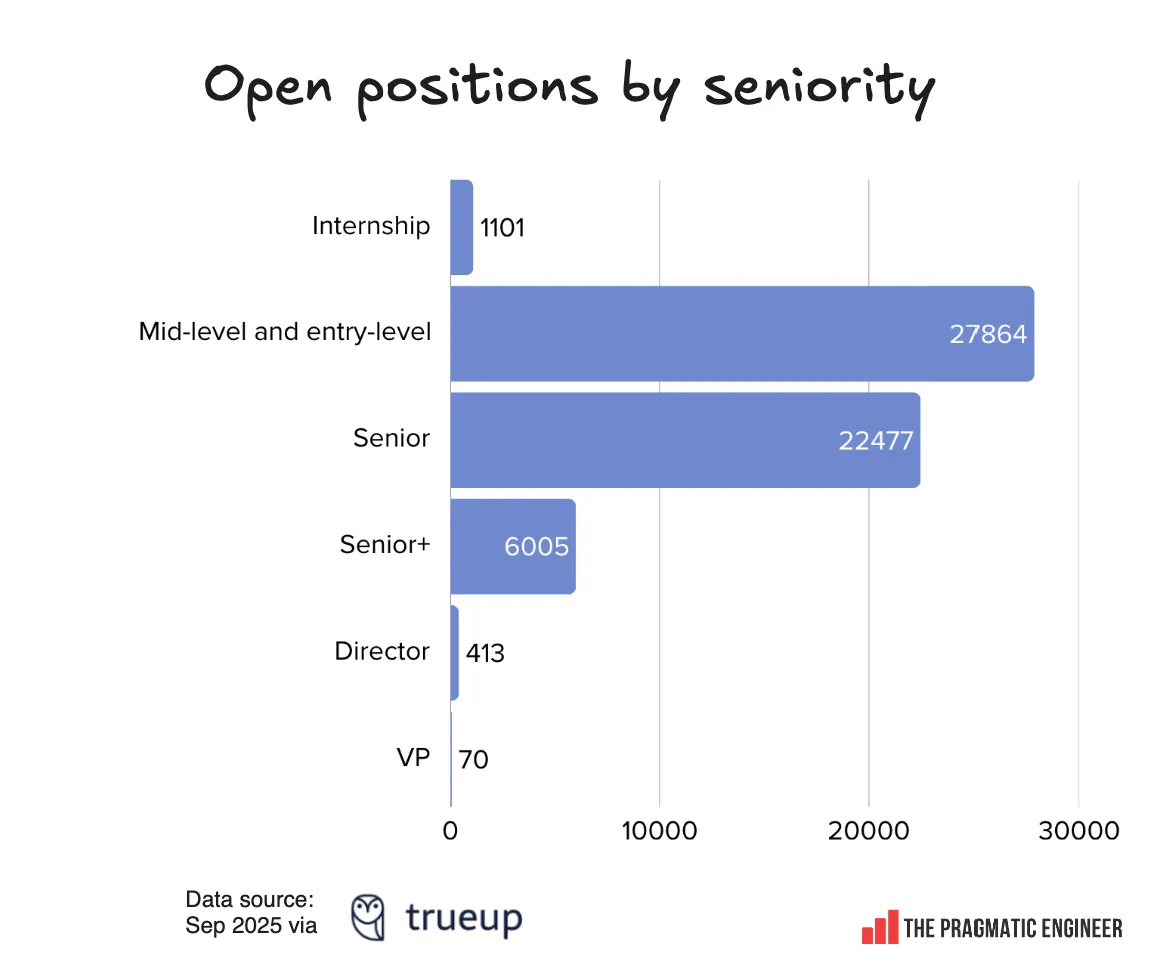

- More than half of open engineering roles are at the senior level or above

- Since 2023, the avg tenure at Big Tech companies has incr’d at a record pace and publicly-traded companies have the most high-paying vacancies

- Other observations regarding Big Tech software engineering headcount, by company –

- Meta’s software engineering headcount has bounced back the most: After the sharpest cuts in 2023 (down ~-12%), Meta now has 19% more engineers vs Jan 2022, which is the biggest recovery among Big Tech employers

- Google & Apple have had steady growth in software engineering headcount: Compared to 2022, Google’s engineering headcount incr’d by +16%, and Apple’s by +13%

- Amazon & Microsoft have had the slowest growth in software engineering headcount: Amazon’s engineering headcount is only 8% above its 2022 level, while Microsoft’s has barely grown since early 2023

AI Will “Extend” SaaS Vs “Eliminate” SaaS, Per Salesforce CEO Benioff

There has been a lot of debate on the “existential risk” that AI poses on software companies and as one can imagine, this was a point of focus as it related to Salesforce this week. Overall, CEO Marc Benioff is not worried…he believes AI will fundamentally extend SaaS vs eliminate AI.

How defensible is SaaS against the disruption from AI native apps and customer built AI? The below says it all…

- “The software industry is going through a tremendous transformation, and it’s really driven by… the fundamental acceleration of artificial intelligence”

- “These large language models only have a certain level of accuracy and it’s not 100%. It’s probably about in the 90s when it really gets well architected with our data cloud and with all the different kind of capabilities and kind of really advanced techniques that we’ve come up with to make our AI as accurate as it can”

- Agents have not “completely taken over the huge customer support channel, it’s Salesforce, it’s just not possible”

- “In the last nine months, about 1.5mn conversations happened directly with these agents and 1.5mn of these conversations happened with humans. And so it’s those apps and it’s the agents working together”

- “And so by doing that, yes, there’s a lot that we can resolve, automatically through these agents with the customers, but there’s also a lot that cannot be resolved and that has to be escalated to the humans”

- And so it’s humans and agents working together to satisfy customer success. And this is what has been extremely important”

- In addition to support, AI is also creating opportunities “for sales as well. As I mentioned with this incredible new robotic salesperson that’s out there, calling back every single one of our leads and setting appointments and even in many places closing deals. And it’s going to be true in every application we made”

- “There are very smart people in our industry and other executives who are saying absolute nonsense. And I don’t understand why they’re saying this nonsense. Maybe it’s just to create a certain level of FUD (fear, uncertainty, doubt) in the market. But I think it’s inappropriate at this point, and what it’s done for the whole enterprise software industry, I think, is crazy”

- “Over the weekend, I read that MIT study that’s becoming very popular which really goes to show that a lot of companies have thought they were on the right path with generative AI, building their own models, doing it themselves, hooking it all up and now they’re claiming about 94% of those projects have failed. Well, we’ve been saying that was going to happen for the last several years, as you know”

- “So, it’s not about the fundamental, oh, I would say elimination of SaaS. And what I would say it’s the fundamental extension of SaaS”

Separately, Microsoft’s Nadella’s 5 Key AI Prompts

On the topic of AI implementation at the workforce, we also wanted to flag Microsoft CEO Satya Nadella making headlines this week when he revealed 5 AI prompts that he uses that can ‘supercharge your everyday workflow’ (link). For those that would like to leverage or try out his prompts, see below!

- “Based on my prior interactions with [/person], give me 5 things likely top of mind for our next meeting”

- “Draft a project update based on emails, chats, and all meetings in [/series]: KPIs vs. targets, wins/losses, risks, competitive moves, plus likely tough questions and answers”

- “Are we on track for the [Product] launch in November? Check eng progress, pilot program results, risks. Give me a probability”

- “Review my calendar and email from the last month and create 5 to 7 buckets for projects I spend most time on, with % of time spent and short descriptions”

- “Review [/select email] + prep me for the next meeting in [/series], based on past manager and team discussions”

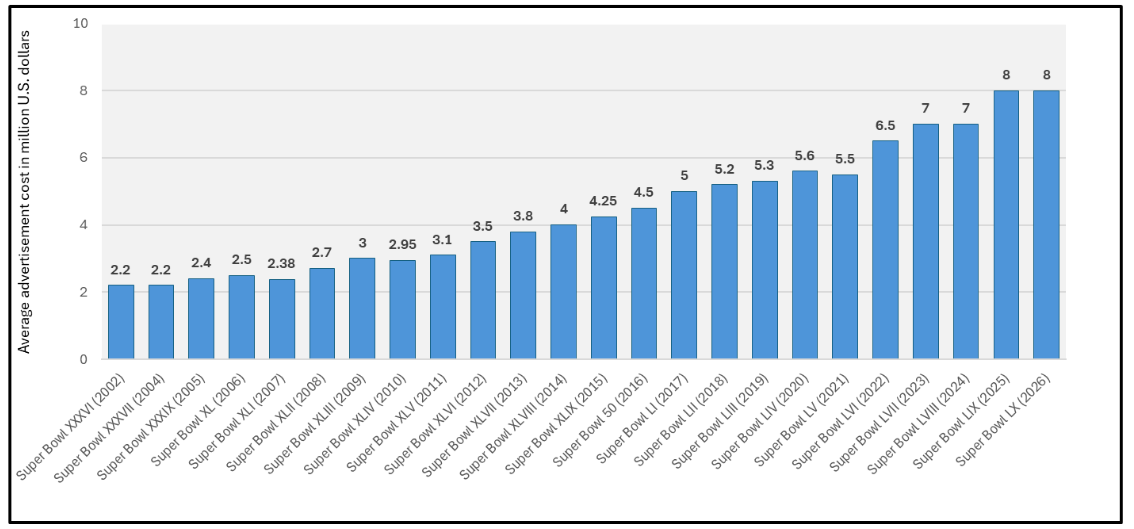

Grab Bag: NFL Hits Ad Rev Record / Apple’s Upcoming “Awe Dropping” Event / Lululemon Post-Earnings Plunge

- NBCUniversal cites record NFL season ad rev (link)

- This NFL season is its highest grossing ever in overall ad & partnerships

- Super Bowl LX ad inventory is fully sold out, earlier than ever

- Already sold 90% of “Sunday Night Football” ad slots

- Over 150 partnerships for “Sunday Night Football” in 2025-26, with ~40 new brands

- This NFL season is its highest grossing ever in overall ad & partnerships

- Ad pricing & demand

- Super Bowl ads are going for $8mn per 30-second spot which is consistent with the $8mn last Super Bowl, but up from $7mn in 2024

- High demand from consumer products, entertainment, finance, and alcohol brands

- Digital spend up +20% vs NBC’s last Super Bowl in 2022

- Speculation mounts ahead of Apple’s “Awe Dropping” event next week (link/link)

- Rumored headliners…iPhone 17 lineup, including –

- iPhone 17 Air – thinnest iPhone ever (5.5mm), A19 chip, single camera on the back

- iPhone 17 – bigger screen, 24MP front camera, ProMotion and always-on screen,

- iPhone 17 Pro / Pro Max – major camera upgrades with new camera bar design, 48MP telephoto + revamped ultra-wide

- Other rumored launches –

- Apple Watch SE, Apple Watch Series 11, and Watch Ultra 3 + health upgrades

- iPad Pro

- Vision Pro

- AirPods Pro 3

- AirTag 2

- New Apple TV 4K (2025)

- HomePod, now with display

- Event date/time: Sept 9th / 1pm EST

- Rumored headliners…iPhone 17 lineup, including –

-> Related to Apple and also notable this week… the Co is reportedly in advanced talks to use Google’s Gemini AI models to power a major upgrade to Siri, aiming to make it more conversational, context-aware, and competitive with tools like ChatGPT and Perplexity (link)

- Lululemon’s stock was a big mover this week, falling post-earnings for the third qtr in a row

- Q2 was in-line/above expectations: Rev of $5.53bn was ~in-line w/ cons $2.54bn, while EPS of $3.10 beat by +9%

- Rev beat was driven by RoW as both Americas and China Mainland missed by -1.7% and -0.9%, respectively

- Q3 guidance was well below expectations: Rev and EPS missed consensus at the midpt by -3% and -23%, respectively

- Cut FY guidance: Rev of $10.85bn- $11bn, down from prior qtr’s $11.15bn-$11.3bn; EPS of $12.77-$12.97 vs prior guidance of $14.58-$14.78

- Guidance includes an estimated reduction in gross profit of ~$240mn, net of currently anticipated mitigation efforts, including vendor savings, and pricing actions, reflecting company’s current assumptions about higher levels of tariffs on imports into the United States and the removal of the de minimis exemption

- “We are facing yet another shift today within the industry related to tariffs and the cost of doing business. The increased rates and removal of the de minimis provisions have played a large part in our guidance reduction for the year”

- Other factors impacting Co performance –

- “The overall market for premium athletic wear in the US remains challenging with declines continuing in Q2”

- “Consumers are spending less on apparel overall, spending less in performance activewear, and are being more selective in their purchases”

- “The competitive landscape is different today than it was even two or three years ago and while no single competitor is having a meaningful impact on our business, there are now many players in the market”

- Q2 was in-line/above expectations: Rev of $5.53bn was ~in-line w/ cons $2.54bn, while EPS of $3.10 beat by +9%

-> Lululemon fell -18.6% on the back of its Q2 print (had previously fallen -19.8% after its Q1 results and -14.2% post its Q4 report); The stock closed the week down -17.0% and is down -56.1% YTD

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Global linear TV ad spend will drop 11.3% to $139.1 billion in 2026, down from $201 billion in 2013, cutting its share of global media to 12.4%. Tech and electronics brands reduced TV spend 42%, while household products rose 12%. Linear still makes up 75% of TV-video investment, but CTV is growing, projected to reach $44.7 billion in 2026, with over half of advertisers planning budget increases, especially in the Americas. (Media Post)

- Warner Bros. Discovery is leaning on contextual relevancy to make its new shoppable CTV ads effective, moving beyond the QR vs. remote debate. Partnering with Kerv.ai, WBD uses machine learning image recognition to identify on-screen objects and match them to products in retailers’ catalogs, starting with Wayfair in 2024. The goal is to turn cultural inspiration from HBO content into instant shopping opportunities, with ads tailored to specific scenes and aesthetics rather than generic product pushes. (Ad Exchanger)

- WPP named Devika Bulchandani as chief operating officer, with Laurent Ezekiel succeeding her as global CEO of Ogilvy. The move follows Andrew Scott’s planned year-end retirement and comes as new CEO Cindy Rose undertakes an operational overhaul after the group lost its top spot in global advertising to France’s Publicis. (Reuters)

- US ad mkts in Jul. saw first YoY decline since Mar. 2023. Per Guideline US Ad Tracker, spend fell 5.6% vs. 2024, which had six days of Olympics and record political buys. Digital ad spend, however, rose 6% YoY, showing resilience despite overall dip. (Cynopsis)

- OOH rev grew 3% in 2Q25 to $2. 86bn, per OOAAA. 65 of top 100 OOH advertisers upped spend YoY. Digital OOH rev rose 9.2%. Transit, financial svs, and local svs led growth; tech and DTC brands expanded. Top 10 OOH advertisers included Morgan & Morgan, Apple, McDonald’s, Coca-Cola, Verizon, Disney, Universal Pictures, Indeed, T-Mobile, and Comcast. (Cynopsis)

- Dentsu is weighing options incl. selling a minority stake or overseas ops, per FT. Last month, CEO Hiroshi Igarsashi told analysts, “We’re rebuilding our biz foundation,” and re-evaluating underperforming units. He noted steady progress, signaling strategic shifts to strengthen the Co’s global position. (Cynopsis)

Artificial Intelligence/Machine Learning

- OpenAI will build its first in-house AI chip next year with Broadcom, using it internally to reduce reliance on Nvidia and diversify supply. The move follows similar efforts by Google, Amazon, and Meta to develop custom AI chips as demand surges. Broadcom, which has secured over $10 billion in AI infrastructure orders, hinted the new customer could be OpenAI. (Reuters)

- Switzerland annc’d Apertus, an open-source national LLM built by EPFL, ETH Zurich & CSCS. Trained on 15tn tokens in 1K+ languages, 40% non-English, it complies w/ Swiss data laws. Apertus aims to be public infrastructure, offering full transparency incl. training docs & datasets. Available via Swisscom & Hugging Face, it targets researchers, cos & hobbyists for chatbots, translators & training tools. (Engadget)

- Apple is set to launch “World Knowledge Answers,” an AI-powered answer engine to rival ChatGPT, Perplexity & Google. Debuting in spring 2026, it’ll integrate w/ Siri, Safari & Spotlight, enabling natural language queries. Apple may use Google’s AI models to accelerate rollout. Despite entering late, Apple aims to leverage its ecosystem for dominance, echoing past moves in music, smartphones & payments. (Tekedia)

- Mistral AI is finalizing a €2bn raise at a $14bn valuation. Known for open-source LLMs and chatbot Le Chat, this marks its first major round since Jun. 2024 (€5.8bn valuation). Backed by Andreessen Horowitz & General Catalyst, Mistral leads Europe’s AI surge, w/ 55% YoY investment growth in Q1 2025 and 12 unicorns incl. (TechCrunch)

- OpenAI ups its secondary share sale to $10. 3bn, initially targeting $6bn, letting eligible staff sell equity at a $500bn valuation. Employees w/ >2 yrs of shares have till Sept. end to opt in; deal closes in Oct. Investors include SoftBank, Thrive, MGX & T. Rowe Price. OpenAI joins cos like SpaceX & Stripe in using secondary sales to ease IPO pressure. (CNBC)

- Palantir & Lumen Tech. annc’d a collab to accelerate Lumen’s AI-driven telecom transformation. Using Palantir’s Foundry & AIP, Lumen aims to modernize ops, streamline workflows & migrate legacy infra. The AI tools will enhance decision-making across finance, tech & svs, aligning w/ customer needs. (Street Account)

- Alibaba’s HK shares surged 19% on Sept. 1 after strong cloud rev and news of a new AI chip. June qtr rev hit $34.73bn, up 2% YoY, missing estimates, but net income rose 78%. Cloud unit rev grew 26%, w/ AI svs showing triple-digit growth for 8th straight qtr. Alibaba is investing in China’s competitive “instant commerce” via Taobao, impacting adj earnings but gaining investor support. (CNBC)

- Anthropic annc’d a $13bn funding round at a $183bn valuation, tripling since Mar. Backed by Amazon, the AI Co’s rev run-rate hit $5bn in Aug., up from ~$1bn in Jan. Claude, its AI assistant, has driven rapid growth. Investors include Iconiq, Fidelity, Lightspeed, Altimeter, and more. Funds will support safety R&D, enterprise demand, and global expansion. Anthropic now serves 300K+ biz customers. (CNBC)

- OpenAI annc’d exec reshuffle and a $1. 1bn acquisition of Statsig to boost its Applications team under new CEO Fidji Simo. Statsig CEO Vijaye Raji becomes CTO of Applications, overseeing ChatGPT & Codex. Srinivas Narayanan is now CTO of B2B Apps, handling enterprise/govt biz. CPO Kevin Weil shifts to research as VP of AI for Science. (The Verge)

- OpenAI annc’d new ChatGPT parental controls, allowing linked teen accounts, age-based rules, and alerts for “acute distress. ” The move follows a CA lawsuit blaming ChatGPT for a teen’s suicide. OpenAI aims to strengthen safeguards in long chats and route sensitive cases to reasoning models. (NBC News)

- Klarna & backers aim to raise $1. 27bn via a revived NY IPO, offering 34.3mn shares at $35–$37, valuing the Co at ~$14bn. Klarna’s valuation plunged from $45.6bn in 2021 to $6.7bn in 2022. The IPO, paused in Apr. due to Trump’s tariff war, is set to price on Sept. 9. Klarna, known for BNPL, now pushes global digital banking. Sequoia to retain ~22% voting power post-offer. (Yahoo Finance)

- Tencent open-sourced two 7B-parameter translation models—Hunyuan MT 7B & Chimera 7B—that outperformed Google Translate and top AI rivals in 30 of 31 WMT2025 tests. Supporting 33 languages, incl. Chinese minority langs like Uyghur & Kazakh, the models use a 5-stage training pipeline and fusion techniques. Despite being smaller, they beat larger models by up to 65%. (The Decorder)

- Tencent Youtu Lab annc’d Youtu-Agent, a zero closed-source dependent framework enabling full-scene adaptation. Its meta-agent dialogue auto-generates YAML configs via natural language, boosting dev efficiency by 300%. Scoring 71.47% on WebWalkerQA, it empowers SMEs w/ low-cost, high-performance agent deployment across data analysis, file mgmt, academic research & wide-area investigation. (Sohu)

- Telus Corp. annc’d a deal to acquire full ownership of Telus Digital for US$539mn, reversing its 2021 spin-off. Offer of US$4.50/share—up from prior US$3.40—is payable in cash or Telus shares. Telus Digital, which went public at US$25/share, closed at US$3.88. CEO Entwistle said the move will enhance AI, SaaS, and global growth across key verticals. Deal values equity at ~US$1.3bn. (Yahoo Finance)

Broadcast/Cable Networks

- PBS is cutting about 100 jobs, or 15% of its staff, after Congress slashed $500 million in federal funding for public broadcasters. The layoffs include 34 current employees plus dozens of open roles and prior reductions. PBS CEO Paula Kerger said the cuts, along with a 21% budget reduction and lowered station dues, are meant to help the network stabilize amid the loss of support from the Corporation for Public Broadcasting, which will shut down in January. NPR has also trimmed its budget in response to the funding shortfall. (PBS)

- Scripps annc’d sale of WFTX (Fox affiliate in Fort Myers) to Sun Broadcasting for $40mn. Deal expected to close in Q4 pending regulatory approvals. Sun, a local broadcaster, will take over ops; Scripps to use proceeds to reduce debt. CEO Symson said the move aligns w/ biz strategy. In Jul., Scripps also revealed a station swap w/ Gray Media, currently under federal review. (Scripps)

Cable/Pay-TV/Wireless

- Charter expects a $26 per-share boost in free cash flow from network upgrades, while the Cox Communications deal is projected to generate $500 million in synergies and cut $1 billion in capital spending. The company plans 450,000 rural passings in 2025 and is integrating streaming services into bundles to steady its video segment. The combined entity will operate publicly as Cox Communications, with Spectrum retained as the consumer brand. (Investing)

- CableLabs’ latest DOCSIS 4. 0 interop hit 16.2 Gbit/s downstream using 8K-QAM and 16K-QAM on a high-split HFC network, up 13% from Jun. tests. Upstream reached ~2 Gbit/s. Though achieved in lab conditions, the test shows D4.0’s potential. Ten modem vendors and multiple core/RPD suppliers participated. While real-world speeds may vary, the cable industry eyes future upgrades like 3GHz spectrum and 25–50 Gbit/s to stay competitive. (Light Reading)

Capital Market Updates

- QIA joined Anthropic’s $13bn round, valuing the AI co at $183bn. It marks QIA’s deeper push into AI after past caution, following peers like MGX and Saudi funds. QIA aims to do 25 tech deals/yr, investing ~$25–100mn per deal, focusing on chips, media, and enterprise AI. Despite past setbacks like Builder.ai, QIA sees AI as strategic, backing firms like Databricks, Instabase, and xAI. (MSN)

- US IPO mkts reopened post-Labor Day as tariff fears eased. Klarna, Gemini, Figure Tech, and others launched roadshows. Analysts expect strong IPO activity through mid-Oct. amid equity optimism. High-growth tech & crypto cos like Circle & Firefly saw strong debuts. Nasdaq sees AI & digital asset cos leading. (Reuters)

- Goldman Sachs expects a major ramp up in dealmaking toward the end of the yr, with a chance that 2026 proves a record year for M&A. The bank predicts deal flow of around $3.1tn globally this yr, rising up to $3.9tn the next, according to Tim Ingrassia, Goldman’s co-chairman of global mergers and acquisitions. That would surpass $3.6tn of M&A in 2021, he added, citing numbers from research firm Dealogic. (Yahoo Finance)

Cloud/DataCenters/IT Infrastructure

- Broadcom topped Q3 estimates with $15. 96 billion in revenue and EPS of $1.69, guiding Q4 to $17.4 billion. Net income hit $4.14 billion, rebounding from last year’s tax-related loss. AI drove results with revenue up 63% to $5.2 billion, expected at $6.2 billion next quarter, and a $10 billion custom chip order secured. Shares are up 32% YTD and nearly doubled over 12 months, pushing its value above $1.4 trillion. (CNBC)

- Microsoft annc’d a deal w/ the U. S. GSA offering $6bn+ in savings over 3 yrs on cloud svs, incl. $3.1bn in yr one. Discounts apply to Office, Azure, Dynamics 365, and Sentinel. Millions of gov’t workers get 1 yr free Copilot AI. The offer supports Trump’s OneGov strategy to consolidate IT spend. GSA oversees $110bn in procurement; Microsoft seen as a key partner for civilian & defense IT needs. (CNBC)

Crypto/Blockchain/web3/NFTs

- SEC & CFTC annc’d a joint initiative to streamline crypto asset trading. Their divisions will issue guidelines for leveraged, margined, or financed spot retail commodity transactions. This aligns w/ Trump admin’s crypto-friendly stance & SEC’s Project Crypto. The CLARITY Act, proposing split oversight, passed the lower chamber. Concerns over Trump-backed ventures raise scrutiny. (Yahoo Finance)

- Crypto exchange Gemini, led by the Winklevoss twins, plans a U. S. IPO targeting a $2.22bn valuation, aiming to raise $317mn by selling 16.67mn shares at $17–$19. Backed by Goldman Sachs & others, Gemini reported $142.2mn rev in 2024, up from $98.1mn. The Co positions itself as a compliant alt to offshore exchanges. (Coindesk )

- Crypto.com & Underdog annc’d a partnership to offer sports prediction mkts in 16 states, targeting areas w/o legal sports betting. Traders buy/sell outcomes like financial assets, bypassing bookmakers. CDNA, a CFTC-registered exchange, will provide contracts hosted on Underdog’s tech. Legal ambiguity remains, but analysts expect $555mn rev in 2025. (CNBC)

eCommerce/Social Commerce/Retail

- Amazon must face a US-wide class action involving 288mn buyers over claims it overcharged for third-party goods. A Seattle judge ruled Amazon’s pricing policies violated antitrust law by restricting sellers from offering lower prices elsewhere. The Co allegedly imposed inflated fees, raising consumer costs. (Reuters)

- Amazon will end shared Prime shipping for non-household members starting Oct. 1. Users must now live at the same address to share benefits via Amazon Family. Invitees can get a discounted $14.99/yr plan for 1 yr, then $14.99/mo. The move follows weak Prime signups during July’s extended Prime Day. Amazon Family allows sharing perks like Prime Video, Music, and more, but limits apply to adults, teens, and kids. (The Verge)

- Gap Inc. posted flat Q2 net sales at $3.7bn, w/ comps up 1%. Old Navy rose 1% to $2.2bn, Gap up 1% to $772mn, Banana Republic down 1% to $475mn, Athleta fell 11% to $300mn. E-comm rose 3%, stores fell 1%. Net income rose 5% to $216mn. Tariffs raised inventory 9%, pressuring margins. CEO Dickson cited cultural momentum via Gap’s viral Katseye ad. (Retail Dive)

- Ulta’s Q2 net sales rose 9. 3% to $2.8bn, driven by its Space NK acquisition and strong fragrance demand. Comps grew 6.7% via higher transactions and avg. ticket. Gross profit rose 11.6%, net income 3.3%. Ulta raised FY outlook to $12–$12.1bn in sales. It opened 24 stores in Q2, now targeting 63 for the yr. Prestige beauty saw mid-single-digit growth. (Retail Dive)

Electric & Autonomous Vehicles

- The Trump administration plans to ease deployment of self-driving cars by removing certain safety requirements meant for human drivers, Bloomberg reports. The U.S. Department of Transportation will propose three rules in spring 2026 to modernize Federal Motor Vehicle Safety Standards for automated vehicles, relaxing mandates tied to manual controls like gear shifts, defrosting buttons, and some lighting equipment. The changes would affect companies developing autonomous vehicles, including Tesla, Google, Amazon, Uber, and GM. (Tip Ranks)

- Tesla Inc. annc’d its Robotaxi hailing app is now “available to all,” after prior limited access to investors and select users. The app is live on Apple App Store w/ a “Download to join waitlist” prompt, signaling broader rollout soon. A follow-up noted Android support is “coming in the future.” This marks a key step in Tesla’s autonomous mobility push, expanding its tech-driven svs footprint. (Baha)

Film/Studio/Content/IP/Talent

- Paramount Pictures and Legendary Entertainment finalized a multi-year global film distribution deal under which Paramount will handle marketing and distribution of Legendary’s theatrical films worldwide, excluding China. The first film in the partnership will be Street Fighter, co-produced with Capcom and filmed for Imax, set for release on October 16, 2026. The agreement follows Paramount’s merger with Skydance and positions the studio to expand its global slate alongside Legendary’s franchises. (Deadline)

- Paramount, now led by David Ellison, annc’d plans to develop a live-action film based on Activision’s “Call of Duty” franchise, which has sold 500mn copies and draws 100mn monthly players. The move follows Ellison’s takeover of the studio and aims to revitalize its legacy. The deal may expand to more films/TV. (Yahoo)

Media Conglomerates

- Paramount is in final talks to acquire Bari Weiss’ The Free Press for $100–200mn and offer her a senior editorial role at CBS News. The move follows the $8bn Skydance-Paramount merger and FCC-mandated changes at CBS, including scrapping DEI programs. Weiss, known for challenging progressive norms, may reshape CBS News amid newsroom tensions. (New York Post)

- Sphere Entertainment (SPHR) stock rose 7. 3% after it repurchased $27.5mn of Class A shares at $43.72 avg. price (Aug. 21–29), signaling mgmt’s confidence in long-term growth. ~$322.5mn remains under buyback auth. SPHR also secured trademarks for “Sphere Doha” & “Sphere Qatar,” hinting at intl. expansion. (Trading View)

- John Malone told FT he had “serious discussions” w/ Rupert Murdoch last summer on merging Fox Corp. w/ WBD. The deal might’ve cont’d if Fox News and CNN could coexist. Warner CEO Zaslav and News Corp chair Lachlan Murdoch were also involved. Malone, a WBD advisor, revealed the talks aimed at uniting major media cos under one umbrella. (Cynopsis)

Regulatory

- Trump asked Supreme Court to fast-track appeal after a Federal Circuit court ruled his tariffs illegal, saying he overstepped authority under IEEPA. The court held tariffs are a Congressional power. Treasury Sec. Bessent warned delays could disrupt $750bn–$1tn in collected tariffs. Trump seeks Nov. hearing, citing national security risks. (CNBC)

- Trump’s “No Tax on Tips” policy, part of a July megabill, lets eligible workers deduct up to $25,000 in tips from federal taxes (2025–2028), on top of the $15,750 standard deduction. Applies to 68 jobs incl. influencers, rideshare drivers, baristas, and more. Deduction phases out above $150K income. Policy may cost gov’t ~$40bn. Unclear how tips must be reported or if auto-gratuities qualify. (Forbes)

- Cox Comm. urged SCOTUS to reverse a ruling holding it partially liable for users’ illegal music downloads. Cox argued the 4th Circuit’s theory would force it to cut off homes, cafes, hotels, barracks, and regional ISPs from internet access. In its brief, Cox warned this would sever innocent users and infringers alike from vital svs integral to modern life. (Cynopsis)

Software

- DocuSign beat Q2 expectations with revenue of $800. 6 million, up 8.8% year over year and above estimates, and adjusted EPS of $0.92. Billings rose 12.9% to $818 million, while adjusted operating income of $238.7 million marked a 12% beat. The company raised full-year revenue guidance to $3.20 billion, though growth remains slower than past years, with analysts projecting just 5.4% over the next 12 months. Free cash flow margin fell to 27.2% from 29.8%. Management cited AI innovation and go-to-market changes as key drivers, with shares jumping 6.7% after the report. (Yahoo Finance)

- Figma’s first earnings post-IPO showed Q2 rev of $249. 6mn (41% YoY growth), beating est. of $248.8mn. op. income hit $11.5mn. Q3 rev guidance of $263–265mn also topped est. Stock plunged 14% post-report. AI tools like Figma Make & Sites launched, but monetization is pending. Net retention fell to 129%. (CNBC)

- Salesforce CEO Benioff annc’d 4,000 support job cuts in 2025, citing AI adoption. AI agents now handle ~50% redcutin in support staff, enabling staff reallocation to sales & svs. Revamp via Agentforce led to fewer support cases, no backfills. Benioff called the past 8 mos. “most exciting” of his career. (San Francisco Chronicle)

Sports/Sports Betting

- Shares of prediction markets continue to grow as regulators clash over their classification. Outgoing CFTC commissioner Kristin Johnson warned in her farewell speech that the agency has “too few guardrails and too little visibility” into the space, stressing the risks of retail-focused leveraged contracts and urging stronger oversight. The CFTC, which regulates event trading nationally, has largely taken a hands-off approach, while state regulators in Nevada and Ohio have moved to block operators, highlighting a widening rift. (iGaming Business)

- Julia Koch & Koch family agreed to buy a 10% stake in the NY Giants at a record $10bn valuation. Deal awaits NFL owner approval in Oct. Koch, widow of David Koch, is NY’s richest woman ($74.2bn). The Mara family retains control; John Mara stays CEO. Kochs also own 15% of BSE Global. (New York Post)

- Fubo’s auto-DVR now records all major sports events—NFL, NBA, MLB, college football, EPL, F1, etc. —by default for subscribers. Team News playlists w/ recaps, analysis, and injury reports are also auto-saved. Users can opt out via My Stuff settings. Content is accessible across devices, w/ storage managed by deleting oldest clips. (Cord Cutter News )

Tech Hardware

- Pixel 8+ phones now support Bluetooth LE Audio & Auracast, enabling audio streaming to multiple headphones. Users can share music via QR code or Fast Pair. Google expanded support to Sony models like WH-1000XM6 & LinkBuds. Pixel Buds Pro 2 get Adaptive Audio, blending noise cancellation w/ ambient awareness, plus Loud Noise Protection. (The Verge)

- Google Play Games will roll out a global update starting Sept. 23, adding public profiles that show game progress, stats, and achievements – similar to Steam. Profiles will appear directly in the Play Store, streamlining account mgmt. Users can customize visibility and connect w/ others. Google aims to boost community-building and milestone tracking across Android gaming. (The Verge)

Video Games/Interactive Entertainment

- NBA 2K26 expands WNBA integration by adding women’s players to MyTeam for the first time, enabling use alongside NBA players in online play and showcasing a deeper W mode. Chicago Sky forward Angel Reese graces the WNBA edition cover, highlighting growing commercial momentum for women’s basketball. The WNBPA, working with OneTeam Partners, has leveraged this visibility into record licensing deals, merchandise sales projected to rise 115% this year, and broader partnerships with brands like DoorDash and Aflac. (Sportico)

- Singtel & Tencent Games annc’d HoK ∙ Cloud, a global-first 5G network slicing deployment for mobile gaming. The tech enables low-latency, cloud-based play w/o heavy downloads or high-end hardware. Launching via TxStore in Nov., users get exclusive in-game credits. TxStore offers 30 titles incl. PUBG MOBILE. (Singtel)

- Roblox annc’d expansion of its age-estimation tech to all users by yr-end, using selfie scans to verify age for chat features. It’s also partnering w/ IARC to standardize content ratings globally, replacing cos labels w/ ESRB, PEGI, GRAC, etc. These moves aim to improve child safety amid lawsuits and regulatory pressure. (TechCrunch)

- Nintendo’s Switch 2, launched in Jun. , defied critics w/ record sales, selling 6mn units in 7 weeks. Despite modest upgrades, fans embraced its fun-first philosophy. The $100bn+ co, rooted in Kyoto tradition, prioritizes gameplay over tech trends. Nintendo’s success stems from originality, internal devs & a culture of creative apprenticeship. (Bloomberg)

Video Streaming

- Nielsen annc’d its Big Data + Panel system as the new standard for TV audience measurement. Combining data from 42K panel homes w/ 75mn devices, it boosts sports viewership accuracy. NFL may see ~1mn lift per game; Amazon’s TNF saw 8% gain. Though final data will take longer, cos expect more reliable metrics. Sports, key for ad rev, will benefit most from this cont’d evolution. (Front Office Sports)

- Walmart+ now lets members choose between Peacock or Paramount+ (ad-supported) for free, switching every 90 days. The perk, worth $95.88/yr, boosts value amid streaming fatigue. Walmart+ costs $98/yr or $12.95/mo, w/ added benefits like free grocery delivery, fuel discounts, and Rx savings. Upgrades to ad-free tiers are optional. (Cord Cutters News)

- YouTube TV is exploring a cheaper “broadcast-and-sports” tier incl. ABC, CBS, FOX & NBC plus key sports nets, aiming for ~$40–$50/month. Talks w/ broadcasters like Disney (ABC, ESPN) & FOX are ongoing. The plan cuts non-sports channels from the $82.99 base, targeting cord-cutters. Prototypes are in testing; launch may hinge on Disney deal. (Cord Cutters News)