During this shortened holiday week, the markets continued to climb higher with the S&P 500 increasing another +1.7% and Nasdaq rising +1.6%, both hitting fresh new record highs. Positive news on trade deals helped boost optimism and the GOP’s One Big Beautiful Bill Act was in the spotlight. All in all, Q2 ended with a bang as the major indices dramatically rallied (the S&P 500 rose +11% and Nasdaq rose +18% for the qtr).

Note that this is a light edition of the Weekly Update and our focus is on:

The full edition of our LT Weekly Update will resume next week.

Enjoy 4th of July!

Best,

Leslie

Quarterly Stock Performance Wrap…Q2 Ends With A Bang

After a tough start to the year, with both the S&P 500 down -4.6% and NASDAQ down a more substantial -10.4% in Q1, both indices posted a strong rebound in Q2, with the S&P 500 up +10.6% and the tech-heavy NASDAQ up an even stronger +17.8%.

Within the S&P 500, the Information Technology sector was the best performer, up +19.6%, which was a considerable reversal from down -8.5% last qtr. While Consumer Discretionary staged a rebound in Q2, up +6.6 after falling -6.3% in Q1, the same couldn’t be said for Consumer Staples, which fell -3.1% in Q2 after the sector was up +2.3% in Q1. The Energy sector performed the worst in Q2, down -9.1%, after being the best performing sector in Q1, up +7.5%.

Looking at performance across our LionTree Universe of ~180 stocks in the TMT and Consumer sector with $1bn+ market caps, stock performance was much stronger with 73% of stocks trading up in Q2, a big increase from 40% in Q1, and 48% trading up double-digits, which was also meaningfully up from 23% in Q1. On the other end, 11% of stocks traded down double-digits, which was a lot lower than the 34% that traded double double-digits in Q2.

Which stock saw the largest gain in Q2? It was CoreWeave, which surged +340% in the quarter after an initial tough start after going public at the end of March. It was followed by Robinhood, up +125%, and Magnite, up +111%, to round out the Top 3 best performers in Q2.

Which stock had the toughest Q2? It was Criteo, which fell -32% in Q2, followed by Compass, down -28% and Stagwell, down -26% to make up the Bottom 3 worst performers.

- How did the “Magnificent 7” do in Q2? They all rebounded from very weak performances in Q1 and were up double-digits in Q2, with the exception of Apple

Our Top 10 List Of Most Interesting/Impactful Headlines This Week

Also see our Other Curated News Section for the full list of news updates that we found most interesting this week.

- Warner Music Group & Bain Capital are launching a $1.2bn joint venture to acquire “legendary” music catalogs across both recorded music and music publishing (link)

- WMG and Bain will together source and acquire the catalogs, while WMG will manage all aspects of marketing, distribution, and administration

- As part of the partnership, Warner Music is in talks to acquire the catalog of the Red Hot Chili Peppers for more than $300mn, according to a person with knowledge of the matter (link)

- Netflix is pushing harder into “live”

- The Co reportedly held talks with Spotify about collaboration on music-related shows, including live ones (link)

- Netflix is adding live NASA programming this summer: Subscribers a real-time look at rocket launches, astronaut spacewalks, mission coverage, and live feeds from the International Space Station (link)

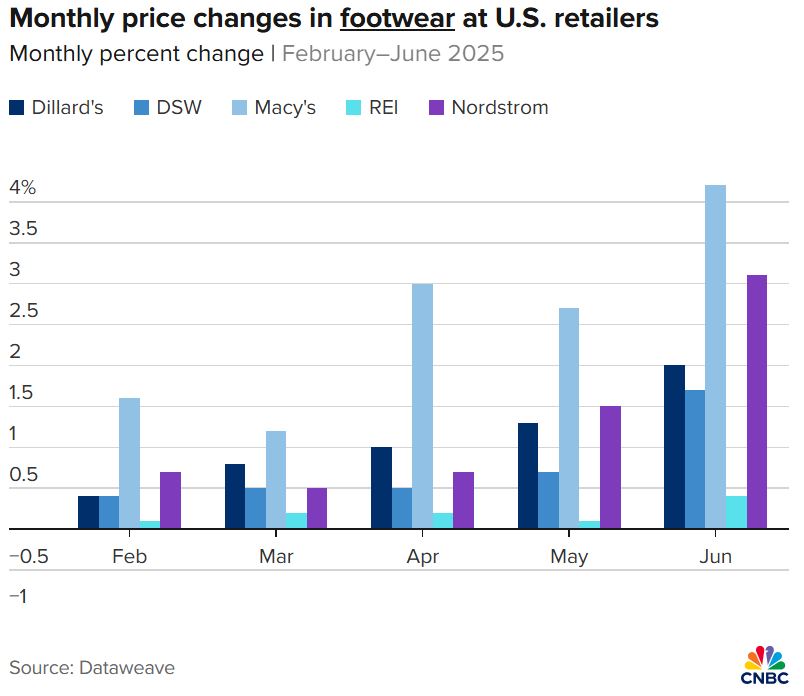

- “Inside America’s department stores, tariff price hikes pick up”…per data from analytics firm DataWeave, recent U.S. tariffs are driving up prices at major department stores like Macy’s, Nordstrom, & Dillard’s (link)

- May marked a noticeable shift when prices began to rise more sharply

- Footwear prices have incr’d the most with prices up as much as 4% above Jan levels at some banners

- Apparel prices are rising more slowly b/c of longer design cycles and more diversified sourcing

- Consumers are likely to feel more of the impact as the summer progresses…

- Apple is reportedly considering a major shift in its strategy for Siri by exploring the use of external AI technologies to boost the virtual assistant’s capabilities (link)

- Sensor Tower data this week shows how Chinese AI models are gaining momentum, with DeepSeek achieving 125mn global downloads despite US tech export restrictions; However, OpenAI’s ChatGPT still has much bigger scale at 910mn global downloads (link)

- Trump says he’s found a buyer for TikTok (link)

- While he didn’t say who the buyer is, according to sources, it is the same investor consortium including Oracle, Blackstone, and venture capital firm Andreessen Horowitz, whose bid for the app had stalled amid

- “I think I’ll need probably China approval and I think President Xi will probably do it…It’s a group of very wealthy people,” Trump said in an interview

- Amazon is nearing a tipping point in automation, with over 1mn robots now operating in its warehouses, which is the most it has ever had and near the count of human workers at the facilities (link)

- Now some 75% of Amazon’s global deliveries are assisted in some way by robotics, the Co said

- Anthropic has reportedly hit a $4nm annualized revenue run rate, quadrupling its top line since January(link)

- The Co is now valued at $61.5bn

- Microsoft is cutting ~9,000 jobs, its second major wave of layoffs this year, to control costs and increase spending on artificial intelligence (link)

- The layoffs will affect less than 4% of the company’s total workforce, across teams, geographies, and tenure, and aim to streamline processes and reduce management layers

- The terminations follow an earlier round of layoffs in May that hit 6,000 people and fell hardest on product and engineering positions

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- OpenAI CEO Sam Altman, in a leaked memo, criticized Meta’s AI hiring spree as “distasteful”. He claimed Meta missed top targets, settling for lower-tier hires, and warned of cultural fallout. Altman reaffirmed OpenAI’s mission-driven ethos, stating “missionaries will beat mercenaries,” while hinting at comp adjustments to retain talent amid escalating AI talent wars. (Wired)

- Musk’s xAI has raised $10bn—$5bn in debt & $5bn in equity—to fund AI infra incl its Memphis-based Colossus supercomputer & Grok platform, per Tech in Asia. Morgan Stanley led the oversubscribed deal. The raise positions xAI to compete w/ OpenAI & Anthropic amid rising AI infra costs & talent wars. xAI’s valuation now exceeds $120bn, w/ some investors pegging it at $200bn. (Tech in Asia)

- Microsoft has scaled back its AI chip roadmap after delays in its Maia chip (Braga), now expected in 2026. Originally aimed at reducing reliance on Nvidia, Braga faced setbacks due to design changes, OpenAI’s late feature requests, and high attrition (~20% in some teams). Microsoft now plans less ambitious chips through 2028, impacting partners like Marvell. The delay may widen the gap w/ Nvidia’s Blackwell chips and force Azure to depend longer on 3rd-party hardware (The Information)

- Tesla has paused Optimus robot production due to a leadership shakeup and unresolved design flaws. Milan Kovac’s exit led to Ashok Elluswamy taking over, aiming to fix overheating joints, weak hand durability, and short battery life. By May, ~1,000 units were built, but the 2025 target of 5,000 is now unlikely. Procurement halted mid-Jun., and redesign may take 2 months. Musk still envisions 50K units in 2026, w/ Grok-powered voice AI. (AInvest)

- China’s Baidu annc’d it will open source its Ernie gen AI LLM, marking the biggest AI move since DeepSeek. Experts say this could disrupt both US & Chinese mkts, pressuring closed models like OpenAI’s. While some doubt it’ll match DeepSeek’s impact, others see it as a major shift in global AI. (CNBC)

Broadcast/Cable Networks

- Paramount Global and Mediacom renewed their multi-yr distribution deal, ensuring continued access to CBS, BET, MTV, Nickelodeon & more across Mediacom mkts. The pact also enables qualifying customers to access Paramount+ Premium. Both cos emphasized flexibility, combining linear TV w/ streaming to meet evolving consumer needs. (Street Account)

Cable/Pay-TV/Wireless

- T-Mobile completed a $2bn multi-yr network expansion across Florida, boosting 5G speeds, coverage & resilience. The upgrade added/retained 1,282 sites, upgraded 1,350+, & hardened 1,375 for disaster readiness. Avg. 5G speeds rose 216% since 2021 to 266.7Mbps, now covering ~100% of Floridians. The move supports smart cities, emergency svs & biz innovation statewide. (T-Mobile Newsroom)

- Bouygues Telecom and Free are in early talks to jointly acquire and split SFR’s assets, including mobile subscribers, fixed-line boxes, antennas, and retail stores. Discussions follow Altice’s plan to divest SFR amid €60bn debt. The split would give Bouygues SFR’s mobile biz and Free the fixed-line segment. The deal could reshape France’s telecom landscape, pending regulatory scrutiny and valuation alignment (BFMTV)

Capital Market Updates

- Ultra-unicorns—private cos valued at $5bn+—now dominate the private mkts, per Crunchbase. Though just 13% of unicorns by count, they hold over 50% of the board’s $6tn value and raised half of its $1tn funding. In H1’25 alone, 17 cos joined the club, incl. Thinking Machines Lab (raised $2bn seed at $10bn val), Glean, Abridge & Groww. U.S. leads w/101 such cos. OpenAI ($40bn) & Scale AI ($14.3bn) drew 73% of 2025’s funding. (Crunchbase News)

Cloud/DataCenters/IT Infrastructure

- Google signed a 200MW PPA w/ Commonwealth Fusion Systems (CFS) to offtake power from its ARC fusion plant in Virginia, expected online in early 2030s. ARC aims to be the 1st grid-scale fusion plant; SPARC, its demo reactor, will test net fusion by 2027. Google, a CFS investor since 2021, is increasing its stake. The deal marks the largest corporate fusion offtake, supporting clean, 24/7 energy for data centers amid rising AI-driven demand (DataCenterDynamics)

Crypto/Blockchain/web3/NFTs

- Visa & Mastercard are adapting to a $253bn stablecoin threat, per Business Times. Stablecoins offer lower fees & faster settlement, bypassing card networks. In response, both cos are integrating stablecoin tech, investing in infra (e.g., Visa’s BVNK stake, Mastercard’s USDG via Paxos), & promoting fraud protection/tokenization. (Business Times)

eCommerce/Social Commerce/Retail

- Tariff-driven price hikes are accelerating across US dept stores like Macy’s, Nordstrom & Dillard’s, w/ May marking a turning point. Dataweave tracked ~15K SKUs from Jan.–Jun., showing footwear prices rose up to 4.2% (Macy’s), apparel ~2% (DSW), & bags ~2.6% (REI). Private-label goods made in China are hit hardest. (CNBC)

- Amazon’s Prime Day (Mon, Jul. 8) will run 96 hours—twice as long as last yr—w/ BoA projecting $21bn+ in GMV, up ~60% YoY. 1P sales may hit $11.5bn (+55%), 3P $10bn (+67%). Analysts cite improved logistics, AI tools (e.g., Rufus), & inventory mgmt. Ad rev & Prime signups expected to rise. Risks include margin pressure, tariff impact, & lower-margin category mix. (Yahoo Finance)

- Alibaba annc’d a $7bn subsidy plan via Taobao’s Shangou to intensify China’s instant e-comm war vs JD. com & Meituan. Over 12 months, consumers get cash vouchers, free coupons & discounts; merchants receive store launch aid, delivery subsidies & lower commissions. The move aims to boost offline traffic, counter “involution,” and defend turf amid rising competition. Deliveries are fulfilled by Ele.me, Alibaba’s food delivery arm (South China Morning Post)

- Temu’s US monthly users plunged 51% to 40. 2mn and Shein’s fell 12% to 41.4mn (Mar–Jun) after Trump closed the “de minimis” tax loophole and imposed tariffs up to 90% on Chinese goods. Both cos slashed US ad spend—Temu by 87%, Shein by 69%—and shifted focus to Europe, where Temu’s app usage surged 64–76% and Shein’s rose 13–20%. EU/UK may soon end similar exemptions, posing new risks. (Financial Times)

EdTech

- Google annc’d over 30 new AI tools for educators under “Gemini in Classroom” at ISTE 2025, incl. lesson planning, quiz generation & personalized content. A new Gemini for Education app, built on Gemini 2.5 Pro, offers AI chatbots (“Gems”) trained on class materials. NotebookLM now creates video overviews; Google Vids is open to all education users. Gemini Canvas enables students to generate quizzes. All tools are free for Google Workspace for Education users. (TechCrunch)

- McGraw Hill, backed by Platinum Equity, filed for a US IPO aiming to capitalize on demand for ed content and tech. The Co, known for textbooks and digital learning tools, seeks to expand its digital footprint. IPO proceeds will support debt reduction and growth. No pricing details disclosed yet (Reuters)

Film/Studio/Content/IP/Talent

- AMC struck a Transaction Support Agreement w/ creditors to resolve litigation, refinance 2026 debt & boost liquidity via $223. 3mn new financing. It’ll convert $143mn of notes into equity (up to $337mn possible) & dismiss lawsuits tied to 7.5% notes. CEO Aron cited a resurgent box office since Apr. & projected 2025 as strongest in 5 yrs, w/ 2026 momentum expected to continue. (The Hollywood Reporter)

- CMX Cinemas filed for Chapter 11 bankruptcy for the 2nd time since 2020, per Bisnow, citing mounting pressure on theater ops. The chain, w/ 28 locations, aims to restructure, reduce obligations & emerge stronger by early Q3. Despite ~$100K–$500K in assets & <$50K liabilities, CMX plans to keep ops running. Industry-wide, U.S. screens have dropped ~14% since 2019 amid shifting consumer habits. (Bisnow)

- AMC is increasing the number of ads shown before movies, per Variety, aiming to boost rev amid $4bn+ debt. The move follows a new deal w/ National CineMedia to run “platinum spot” ads just before films start. Critics argue it cheapens the moviegoing experience, especially as ticket prices rise. Surveys show 67% of viewers want shorter ads, though 81% still enjoy trailers. (Variety)

- Apple & Warner Bros’ “F1” revved to a $144mn global debut ($55. 6mn domestic), marking Apple’s biggest theatrical opening. The Brad Pitt-led film blended high-octane racing w/ emotional storytelling, earning strong reviews and an “A” CinemaScore. Meanwhile, Universal’s “M3GAN 2.0” underperformed at $10mn+, far below its 2023 predecessor. (Deadline)

Live Entertainment/Theme Parks/Concerts/Experiential

- Six Flags United Parks saw a sharp drop in foot traffic due to extreme heat and severe weather across key US regions. CEO Selim Bassoul revealed that ~400K fewer visitors came in recent weeks. Record temps in the South and heavy rainfall in the Northeast disrupted attendance. CFO Gary Mick noted rev losses are hard to recover, prompting plans for more indoor, air-conditioned venues. Despite challenges, pass sales remain strong (Bloomberg)

M&A

- Global M&A hit $2. 14tn in H1’25, up 26% YoY, fueled by a surge in $10bn+ deals—esp. in Asia, which doubled to $583.9bn. Despite early headwinds from tariffs & high rates, optimism is rising as mkts stabilize. Bankers expect more megadeals in H2, citing easing antitrust rules & IPO momentum. (Reuters)

Macro Updates

- Fed’s Bostic reaffirmed his forecast for one rate cut in 2025, citing solid labor mkts & tariff-related inflation uncertainty. Speaking at a Market News Intl. event, he said the Fed can afford to be patient, w/ 3 more cuts penciled in for 2026. Bostic warned that tariff pricing hasn’t fully hit the economy & policy volatility could unsettle mkts. (Reuters)

- US manufacturing contracted in June for the 4th straight month, w/ ISM index at 49, below the 50 threshold. Orders & jobs fell sharply amid tariff-driven uncertainty, weak demand & rising input costs. Backlogs shrank for a record 33rd month, while employment dropped to a 3-mo. low. Despite this, production edged into growth. Import gauge rose 7.5 pts—most in 5 yrs—after prior slump. (Bloomberg)

- US job openings rose by 374K to 7. 77mn in May, highest since Nov, per BLS data on Tues (Jul.1). Gains were led by leisure & hospitality (~75% of increase), while hiring fell, esp. in health care & manufacturing. Layoffs dropped to 188K, quits rate edged up, and vacancies per unemployed rose to 1.1. Despite headline strength, economists flagged mixed sectoral trends & cautious hiring amid tariff uncertainty. (Bloomberg)

Media Conglomerates

- Paramount agreed to pay $16mn to settle Trump’s lawsuit over a 2024 “60 Minutes” interview w/ Kamala Harris, which he claimed was deceptively edited. The funds will go to Trump’s future presidential library, not to him directly. The deal includes no apology but requires CBS to release transcripts of future candidate interviews. The move comes as Paramount seeks approval for its $8.4bn Skydance merger. (CNBC)

- Warner Bros Discovery stock fell 4. 9% on Tue (Jul 1) after Advance/Newhouse sold 100mn shares for $10.97 each (~$1.1bn), reducing its stake below 5%. The sale, finalized Sun (Jun.30), was for estate planning & investment flexibility. The Newhouse family, early Discovery investors, now owns ~3.97% of WBD. The move comes as WBD plans to split into two cos by 2026: Global Networks & Studios/Streaming, w/ the former taking most of its $37bn debt (Yahoo Finance)

Regulatory

- Google has proposed a revised search layout—Option B—to avoid a potential EU antitrust fine. Under scrutiny for favoring its own svs like Shopping & Flights, Google now suggests a VSS box atop search results linking to rivals, plus a second box w/ free supplier links (e.g., hotels, airlines). The proposal, revealed Mon (Jun.30), precedes a key EU workshop (Jul.7–8). Critics argue changes may still fall short of DMA compliance, risking fines up to 10% of global rev (Reuters)

- Canada has suspended its planned digital svs tax after the US walked out of trade talks, citing concerns over unfair targeting of US tech cos. The Canadian govt said it remains committed to fair taxation but paused the levy to avoid escalating trade tensions. The US had warned of retaliatory tariffs. Talks may resume if both sides agree on a global tax framework (Telecompaper)

Social/Digital Media

- Meta has launched DMs on Threads, enabling private 1-on-1 chats for users aged 18+ across Android, iOS & web. Rolled out on Tues (Jul.1), the feature supports text, emoji reactions, muting & spam reporting. However, it lacks end-to-end encryption, raising privacy concerns. Meta plans to add group chats, inbox filters & message controls soon, aiming to evolve Threads into a standalone social platform. (The Verge)

- Reddit shares surged after app downloads spiked 77. 98% in Apr. and 47.92% in May, signaling renewed user growth. The stock rose 44% in 3 months and 127% YoY, aided by short covering (16.3% float short). Analysts like Citigroup ($163 PT) and Guggenheim ($165 PT) cited monetization potential. Reddit plans to expand ad tools, partnerships & personalization. (Benzinga)

- Trump claimed a buyer is ready to acquire TikTok but declined to name the party, raising speculation amid ongoing legal and political scrutiny. He emphasized the deal would keep TikTok operational in the US and suggested it could be a “great American Co.” The statement comes as ByteDance faces a looming divest-or-ban deadline. (Bloomberg)

Software

- Figma filed for IPO on July 1, aiming to list on NYSE under ticker “FIG. ” The move follows Adobe’s failed $20bn acquisition in 2023. Figma, last valued at $12.5bn, has 1,000+ clients paying $100K+ annually. CEO Dylan Field said public listing will enable “big swings,” incl. acquisitions. (NBC New York)

Sports/Sports Betting

- ESPN and MLB have resumed media rights talks after both opted out of their $550mn deal in Feb. , ending a 35-yr partnership after 2025. Discussions, revealed Sun (Jun.30), focus on local rights and parts of ESPN’s former package (e.g., Sunday Night Baseball, Home Run Derby). ESPN seeks lower fees; MLB eyes broader reach via ESPN+ or its upcoming DTC app. NBC, Apple & Fox also expressed interest. A deal is expected before the All-Star Game (SportsPro)

Tech Hardware

- A US judge denied Apple’s motion to dismiss a DOJ-led antitrust suit, allowing the case to proceed. The gov’t alleges Apple monopolizes the U.S. smartphone mkts—holding 65% of the broader segment and 70% of the “performance smartphone” segment—by restricting five key techs: super apps, cloud-streaming, messaging, smartwatches & digital wallets. Internal Apple emails allegedly show intent to block user switching. Remedies could include biz practice changes or divestitures. (Reuters)

Towers/Fiber

- Google Fiber (GFiber) is exploring slice-enabled svs plans using Nokia tech, aiming to offer real-time customization for home internet. The demo showed how network slicing can carve a home network into “lanes” optimized for uses like gaming or secure banking. GFiber envisions “transactional slices” that activate briefly for sensitive tasks. No commercial rollout date yet, but Nokia collab continues. (Telecompaper)

Video Games/Interactive Entertainment

- Nintendo pulled its Switch 2 and other products from Amazon’s US site due to a dispute over unauthorized third-party sales. Sellers were reportedly bulk-buying in Southeast Asia and undercutting Nintendo’s U.S. prices. Amazon offered authenticity labels, but Nintendo opted to halt direct sales. Both cos deny Bloomberg’s claims, though Switch 2 remains unavailable on Amazon US, unlike in other mkts. (Bloomberg)

Video Streaming

- Disney+ has secured exclusive rights to stream UEFA Europa & Conference League matches in Sweden & Denmark from the 2024/25 to 2026/27 seasons. The 3-yr deal covers 342 games across 19 match weeks at no extra cost to subs. It marks Disney’s 1st major live sports push in Europe, aiming to broaden reach & engage new fans via ESPN’s sports heritage. (Cord Cutters News)