What a week! The DeepSeek AI reverberation came out of nowhere during an incredibly busy earnings week! We did our best to dig in and provide perspective on what we thought was most incremental but we had to pick our spots. The major indices pulled back a bit (S&P 500 down -1% and Nasdaq -1.6%, dragged down by some big tech names like NVIDIA -16% and Microsoft -7%). The Jan FOMC meeting was as expected though Trump’s potential tariff moves were front and center.

This is a dense edition so you may need the extra cup of coffee.

Have a nice weekend and prepare for what should be another exciting week ahead.

- Earnings Scorecard – Week 1 & 2

- Meta’s Core Business Out-Delivered, Though 2025 Will Be An Intense Year

- DeepSeek Sinks Big Tech…What’s Next?

- Telcos Shine With AT&T & T-Mobile Following Verizon’s Lead

- Comcast & Charter Faced Tougher Competitive Headwinds, But M&A Optionality Remains In Place

- The TikTok Tug-Of-War Seems To Be Shaping Up Into A Bidding War… Potential Buyers Come Out Of The Woodwork

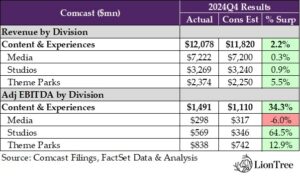

- First Look At Media Trends…Comcast’s Theme Parks Are Back On Track & Peacock Losses Improve

- Robotaxis Get The Next Green Light

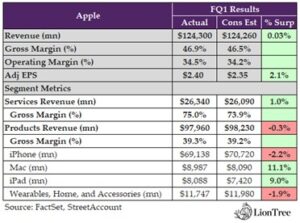

- Quick Takes On Apple & Microsoft As Well…

- One Small Step For Satellite Providers And Potentially A Giant Leap For The Connectivity Industry

Best,

Leslie

Earnings Scorecard – Week 1 & 2

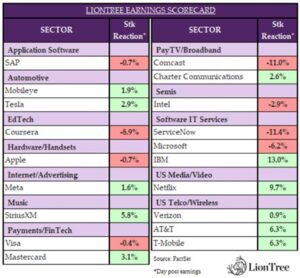

The first earnings season of 2025 is officially underway, with 19 companies in our LionTree Universe reporting their fourth quarter results over the last two weeks. It has been somewhat of a positive start to the year, as stock price reactions were biased to the upside – 11 companies (58%) trading up on their prints and 8 companies (42%) traded down. IBM led the pack, up +13.0%, while ServiceNow was the biggest laggard, down -11.4%.

The telco connectivity and cable names took over the earnings circuit this week. The big 3 telcos had a strong quarter – after Verizon’s results last week, with the stock up +0.9% in reaction, AT&T and T-Mobile followed suit this week with +6/3% gains post-earnings (see Theme #4). Cable was more mixed, as while Charter was up +2.6% after its results, Comcast plunged -11.0% (see Theme #5 for more details).

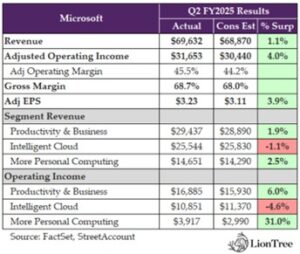

Big Tech also took center stage this week. Meta’s stock was up +1.6% in reaction, (see Theme #2 for all the updates), while it was tougher going for both Microsoft and Apple, which fell -6.2% and -0.7%, respectively (see Theme #9).

Finally, we got out first look into the media and theme parks space, with NBCU results out from Comcast (see Theme #7).

There were a whole host of updates across the sector, and its just getting started…The table below includes select mid- and large-cap TMT and consumer companies in our LionTree Stock universe.

Meta’s Core Business Out-Delivered, Though 2025 Will Be An Intense Year

The pressure is on at Meta, as CEO Mark Zuckerberg called out that the next 48 weeks are going to be instrumental for the Co to “get on the trajectory that we want to be on.” And what exactly is that trajectory? Starting big picture, 2025 is going to be a “big year” for “redefining” Meta’s relationship with the government, especially with the goal of establishing a “national advantage” through a US-led open-source standard in light of DeepSeek’s entry into the market. Additionally, 2025 is poised to be the year Meta AI emerges as the leading AI assistant, driven by a focus on personalizing the agent for each user’s interests and needs and it will be the year that the sophistication of AI engineering agents will reach new highs. Over at Reality Labs, while details on Horizon were sparse, there was mention that several of the metaverse investments will “really start to land” by year-end. Similarly, 2025 will be a “defining” year for AI glasses as Meta gauges whether the shift in focus from holographic-driven adoption to AI-powered glasses will maintain its momentum.

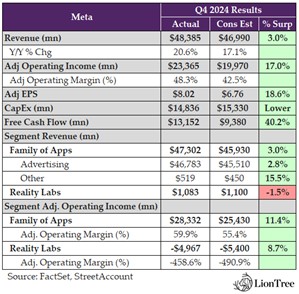

While at the same time, in the here and now, the Co’s core advertising business, which continues to drive the bulk of revenue, posted a very strong qtr, with total rev growth accelerating seq and beating expectations. The business is certainly benefitting from AI-driven improvements and within its Family of Apps, the average price per ad increased +14% y/y in Q4 vs cons +6.1% y/y. However, total revenue guidance for Q1 disappointed and implied decelerating growth sequentially. On top of that, while the Co has been priming investors for 2025 to be a big infrastructure investment year, the 2025 capex outlook of $60-65bn still came in materially above expectations of $52.6bn and mgmt. doesn’t have a sense for long term capital intensity given the magnitude of unknowns.

Engagement on the platform remains favorable and newer services like Threads now has 320mn+ MAUs and is expected to reach 1bn users “over the next several years”. Ads will begin to be tested on Threads this qtr, though monetization Is still some ways off. Reels is also growing, with several initiatives underway to continue to drive that growth. Interestingly, Zuckerberg mentioned going back to the “OG Facebook” or, in a sense, reviving the platform to grow its “cultural influence.” Concrete details on what that means weren’t shared outside of it being a “a fun and interesting goal that will take our product development in some interesting directions.”

Overall, it was a strong qtr and while investment levels remain high (and might for some time), Meta is showing fruits of some of those investment in its core advertising business in the meantime and 2025 will be a pivotal year for many new future growth drivers.

See below for our key takeaways from Meta’s results …

Q4 Was A Very Strong Qtr, But Q1 Rev Guidance Was A Disappointment

- Q4 total revs beat cons by +3.0% and grew +21% y/y (an accel from +19% y/y in Q3): Family of Apps beat by +3.0%, while Reality Labs missed by -1.5%

- OUTLOOK – Q1 rev disappointed: Midpt of Q1 rev guidance ($39.5-$41.8bn) was -2.5% below cons and implies seq decel of +8-15% y/y growth

- Did not provide FY25 revenue outlook, but expect investments in core biz will enable them to deliver “strong” rev growth throughout 2025

- Q4 adj. op income beat by a significant +17% (much stronger margin of 48.3% vs cons 42.5%)

- Q4 EPS beat by +18.6%

- FCF was a notable +40.2% beat

Investing “Aggressively” In Infrastructure But Still Too Early To Determine When It Will Peak

- While Q4 CapEx came in lower than expectations…: $14.8bn vs cons $15.3bn, driven by investments in servers (largest portion of overall CapEx), data centers, and network infrastructure

- … 2025 CapEx OUTLOOK of $60-65bn is well above consensus $52.6bn (and 2024 CapEx of $39.23bn), driven by increased investment to support both genAI efforts and core biz

- Looking further out, still too early to determine what long-term capital intensity will look like, given the many different factors at play (i.e., pace of advancements in underlying models, efficiency, adoption and use cases of genAI products, etc.)

- “I continue to think that investing very heavily in CapEx and infra is going to be a strategic advantage over time. It’s possible that we’ll learn otherwise at some point, but I just think it’s way too early to call that. And at this point, I would bet that the ability to build out that kind of infra is going to be a major advantage for both the quality of the service and being able to serve the scale that we want to”

- OUTLOOK – 2025 expenses: Total expenses to be in the range of $114-119bn (vs $95.1bn in 2024), driven by –

- Infrastructure costs, driven by higher OpEx and depreciation (will be the “single largest driver”)

- Employee compensation (“second largest” factor) as they add technical talent in “priority areas” of infrastructure, monetization, Reality Labs, genAI, as well as regulation and compliance; Head count growth in biz functions will remain “relatively limited”

- Several buildouts in progress –

- 2025: Expect to bring online ~1 gigawatt of capacity this year

- In progress: Building a 2 gigawatt and “potentially bigger” AI data center big enough to cover “a significant part” of Manhattan is it were placed there

- Implementing efficiency initiatives to optimize costs and productivity across infrastructure, operations, and talent

- Infrastructure optimization: Extending server lifespan to 5.5 years and improving workload efficiency to reduce CapEx and depreciation

- Hiring and productivity: Prioritizing technical hires while leveraging AI tools to boost engineering efficiency

- Custom MTIA (Meta Training and Inference Accelerator) Silicon: Deploying MTIA to lower compute costs, with broader adoption planned in 2025

- Timeline for moving to custom MTIA silicon from 3P chips?

- Expect to continue to purchase 3P silicon and are “certainly committed to those long-standing partnerships”

- But also “very interested” in developing their own custom silicon for “unique” workloads, “where off-the-shelf silicon isn’t necessarily optimal”

- Will continue ramping adoption of MTIA over the course of 2025 as they use it for both incremental capacity and to replace some GPU-based servers when they reach the end of their useful lives

Taking The Lead With Llama 4 (And DeepSeek Reinforces The Need For A US-Led Open-Source Standard)

- Update on model progress –

- Llama 4 is making “great progress” in training

- Llama 4 mini is done with pretraining

- Reasoning models and larder models are “looking good too”

- “Our goal with Llama 3 was to make open source competitive with closed models. And our goal for Llama 4 is to lead”

- Llama 4 will be natively multimodal, will have agentic capabilities, and will “unlock a lot of new use cases”

- View on DeepSeek and impact on Meta? Its advancements are part of the natural evolution of the industry

- “Think that there’s a number of novel things that they did that I think we’re still digesting”

- Still too early to whether it will impact Meta’s trajectory around infrastructure and CapEx

- Expects shift in how compute is used, with more focus on inference models alongside pretraining, which may require more compute to enhance intelligence and service quality

- Open-source AI strategy drives industry adoption, lowers costs, and strengthens US leadership amid global competition

- DeepSeek highlights the need for a US-led open-source standard: Sees growing global competition, including DeepSeek from China, as reinforcing the importance of ensuring an open-source AI standard led by the US

- Also expect that “2025 will be the year when it becomes possible to build an AI engineering agent that has coding and problem-solving abilities of around a good mid-level engineer”

- First-mover advantage: “Whichever company builds this first, I think, is going to have a meaningful advantage in deploying it to advance their AI research and shape the field”

- “And this is going to be a profound milestone and potentially one of the most important innovations in history, like as well as over time, potentially a very large market”

“This Is Also Going To Be A Big Year For Redefining Our Relationship With Governments”

- “We now have a US administration that is proud of our leading companies, prioritizes American technology winning and that will defend our values and interests abroad and I am optimistic about the progress and innovation that this can unlock”

The Core Advertising Business Outperformed As Initiatives To Drive Higher Per Ad Yielded Results

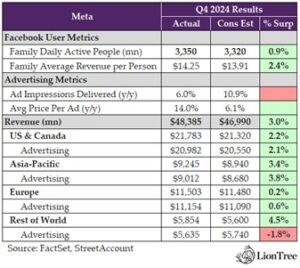

- Family of App ad rev grew +21% y/y (accel from +19% y/y in Q4) and beat cons by +2.8%: FOA adj op margins of 59.9% came in higher than cons 55.4%

- Online commerce vertical was the largest contributor to y/y growth (similar to last qtr)

- RoW led y/y ad rev growth (similar to last qtr)

- ROW +27%

- APAC +23%

- Europe +22%

- Amer +18%

- Delivered fewer impressions but MUCH higher growth in avg price per ad

- Total impressions incr’d +6% (vs cons +10.9%), mainly driven by APAC

- Avg price per ad incr’d +14% (which was a lot better than cons 6.1%), benefitting from incr’d ad demand, in part driven by improved ad performance, partially offset by impression growth, particularly from lower monetizing regions and surfaces

- Focused on driving “efficient” ad supply growth to optimize ad volume w/ organic engagement

- Continue to grow supply on lower monetizing surfaces…: Like video

- …while optimizing ad supply on each of their services: To deliver ads at the time and place they will be most relevant to users (i.e., continuing to optimize ad placement by personalizing when and where ads appear in a user’s feed to maximize both user experience and revenue)

- Improving marketing performance through ongoing enhancements to ads ranking system

- Andromeda (ML system in partnership w/ NVIDIA) has driven a +8% increase in the quality of ads that people see on objectives they’ve tested

- Adoption of Advantage+ shopping campaigns continues to scale with revs surpassing a $20bn+ annual run rate and growing +70% y/y in Q4

- Testing a new streamlined campaign creation flow in which all campaigns optimizing for sales, app or lead objectives will have Advantage+ turned on from the beginning

- Plan to expand to more advertisers in the coming months before fully rolling out later in the year

- Advantage+ Creative is also seeing momentum: 4mn+ advertisers are now using at least on genAI ad creative tool, up from 1mn six months ago; Have seen “significant” early adoption of their first video generation tool rolled out in October, Image Animation, with “hundreds of thousands” of advertisers using it monthly

- “Overall, we are seeing healthy cost per action trends for advertisers for whatever is the action that they are optimizing for. And we believe we’ll continue to get better at driving conversions for advertisers”

- Threads is ramping strongly but is NOT expected to be a “meaningful” driven of overall impression or rev growth in 2025: Introduction of ads on Threads will be “gradual”, with tests beginning this qtr

Continue To Invest In Growing IG Reels And Threads, While A Revival Of The “OG Facebook” Is In The Works

- Making “several” product bets on Instagram Reels to drive “longer-term success”

- Video continued to grow in Q4: Global video time grew “double-digit %ages” y/y on Instagram

- Looking into 2025 – see “continued opportunities” to drive growth

- Creators are a “central focus”: Prioritizing original posts and recommendations to boost smaller creators, including a new feature that lets creators share Reels with non-followers first to test performance and expand reach

- Investing in creative tools: Launching new standalone app called Edits that provides a full suite of creative tools to make it easier for creators to make reels on their phone

- Making it easier for people to connect over content: Reels are reshared 4.5bn+ times a day; In the US, a new Reels destination featuring content liked or noted by friends has shown strong early results, with plans for global expansion soon

- Ongoing optimizations of ranking systems

- Limited commentary on TikTok: “We’re going to learn what’s going to happen with TikTok”

- Expect Threads “to continue on its trajectory to become the leading discussion platform and eventually reach 1 billion people over the next several years”

- Reached 320mn+ MAUs in Q1 (up from ~265mn in Q4)

- Have been adding 1mn+ sign ups per day (in-line w/ Q4)

- Making “a number of updates” to make Threads “the place people come to keep up with what they care about”

- Prioritizing more recent posts

- Surfacing content from “top” creators

- Ensuring people see more of the content from accounts they follow

- Continue improving custom feeds so people can build personalized feeds on topics they’re interested in

- Want to get back to the “OG Facebook” this yr – “we’re focused on growing its cultural influence” (but mgmt. provided limited color on what this really means)

- US is a key growth market focus for WhatsApp: “I expect WhatsApp to continue gaining share and making progress towards becoming the leading messaging platform in the US like it is in a lot of the rest of the world”

- WhatsApp now has 100mn+ MAUs in the US

Expects 2025 To Be The Year Meta AI Becomes The Leading AI Assistant, Driven By A Focus On Increased Personalization

- “Meta AI is already used by more people than any other assistant” … road to 1bn? “I expect that this is going to be the year when a highly intelligent and personalized AI assistant reaches more than 1 billion people, and I expect Meta AI to be that leading AI assistant”

- Meta AI now has 700mn monthly actives (up from 500mn in Q4)

- How is Meta AI being used across platforms?

- WhatsApp has the strongest Meta AI usage: Used most frequently for information seeking and educational queries, along with emotional support use cases

- Facebook is the second-largest driver of Meta AI engagement: Seeing “strong” engagement from feed deep dives integration that lets people ask Meta AI questions about the content that is recommended to them

- Introducing updates that will enable Meta AI to deliver “more personalized and relevant responses” by remembering certain details from people’s prior queries and considering what they engage with on Facebook and Instagram to develop better intuition for their interests and preferences

- Monetization is not a focus at the moment: Initial focus is “really about building a great consumer experience”;

- But expect there to be “pretty clear” monetization oppties over time, including paid recommendations and a premium offering; It’s just “not where we are focused in terms of the development of Meta AI today”

- Looking ahead… “we have some fun surprises that I think people are going to like this year”

Reality Lab’s Q4 Operating Loss Was Not As Negative As Expected & More To Come With The Product In 2025

- Reality Labs grew +1% y/y to $1.1bn (-1.5% below cons), and operating loss was $5bn (which was better than cons $5.4bn)

- “The number of people using Quest and Horizon has been steadily growing”

- By end of the year, “think we’re going to know a lot more about Horizon’s trajectory”

- “This is a year when a number of the long-term investments that we’ve been working on that will make the metaverse more visually stunning and inspiring will really start to land”

2025 Will Be The Year “When We Understand The Trajectory For AI Glasses As A Category”

- Glasses are the “ideal form factor for an AI device”, enabling an AI assistant to understand context by seeing and hearing what the user experiences

- “Glasses are going to be a very important computing platform in the future” …

- “It’s kind of hard for me to imagine that a decade or more from now, all the glasses aren’t going to basically be AI glasses”

- …and this year will be a “defining year” that determines “if we’re on a path towards many hundreds of millions and eventually billions of AI glasses…or if this is just going to be a longer grind”

- “We still don’t know what the long-term trajectory for this is going to be. And I think we’re going to learn a lot this year”

-> Press, citing an internal memo circulated by Meta CEO Mark Zuckerberg, reported that the Co sold 1mn units in 2024… (link)

DeepSeek Sinks Big Tech…What’s Next?

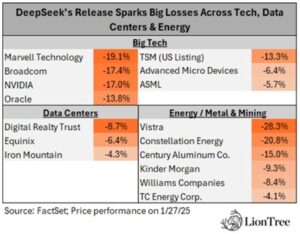

It was quite a tech scare out of the gate this week following press that DeepSeek was the #1 free Apple iOS app download in the US over the weekend and approached the top 10 in the Google play store. DeepSeek’s new open-source AI model called R1, which mimics human reasoning, created a panic that reverberated across the industry due to its impressive performance while reportedly costing a fraction of traditional foundational models. This innovation was also achieved despite AI chip export restrictions in place. This all raises questions about chip oversupply, high levels of AI investment, competitive moats, etc. NVIDIA alone lost -$600bn in market cap on Monday, but the carnage was far reaching across the tech sector as well as energy/power related companies and REIT data centers.

This development was also interesting timing, given that it was barely over a week after Project Stargate (JV to spend $500bn to building data centers and fund AI R&D) was announced at the White House (see last week’s edition for more).

There is still a lot to learn about DeepSeek’s R1 and the impact of further trade restrictions, for example, but we think this was a wake-up call for the sector and will actually help to spark further and faster innovation. Driving down the AI cost curve will help the general proliferation of the technology.

There will be more to come in the weeks ahead but see below for what we view as the need-to-knows thus far on DeepSeek (and see Theme #2 and Theme #9 for more on Meta, Apple, and Microsoft’s response). (link/link/link/link/link/link/link)

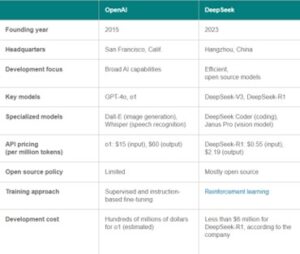

Who developed DeepSeek?

China based, 40-year-old Liang Wenfeng created DeepSeek in 2023 as an offshoot of the AI division of his quant hedge fund called High-Flyer

What was the product release timeline?

- Nov 2023 – DeepSeek Coder: the Co’s first open-source model designed specifically for coding-related tasks

- Dec 2023 – DeepSeek LLM: the first version of the Co’s general-purpose model

- May 2024 – DeepSeek-V2: the second version of the company’s LLM, focusing on strong performance and lower training costs

- July 2024 – DeepSeek-Coder-V2: a 236bn-parameter model offering a context window of 128k tokens, designed for complex coding challenges

- Dec 2024 – DeepSeek-V3: uses a mixture-of-experts architecture, capable of handling a range of tasks

- The model has 671bn parameters w/ a context length of 128k

- Jan 2025 – DeepSeek-R1: this model is based on DeepSeek-V3 and is focused on advanced reasoning tasks directly competing with OpenAI’s o1 model in performance, while reportedly maintaining a significantly lower cost structure

- Like DeepSeek-V3, the model has 671bn parameters w/ a context length of 128k.

- Jan 2025 – Janus-Pro-7B: is a vision model that can understand and generate images

What is all the hub bub?

- DeepSeek asserts that R1 performs better than OpenAI’s o1… Last week, DeepSeek released a report that showed its model matching or exceeding o1’s performance on several critical benchmarks

- …While also being DRAMATICALLY cheaper to train: DeepSeek cites a sub $6mn number to train its AI (~3% to 5% of what it reportedly cost OpenAI to develop its next-generation o1 counterpart) which raised questions about how much US Big Tech has been spending to develop their AI efforts; This also raised concerns about Nvidia chip demand and the potential for an oversupply of AI investments

- BUT note that there has been a lot of debate about what other costs were also incurred by DeepSeek and not included in the $6mn figure

- Semiconductor analyst Dylan Patel calculated that DeepSeek spent over $1 billion on its compute cluster per President Trump’s AI czar, David Sacks on X on Friday. “The widely reported $6M number is highly misleading, as it excludes capex and R&D, and at best describes the cost of the final training run only”

Source: TechTarget link

- DeepSeek was able to develop this AI tech despite restrictions on the highest performance AI accelerator and GPU chips

- There has been some debate about what AI chips DeepSeek used to train its model; It has been reported that they obtained 10k+ Nvidia GPUs before U.S. export restrictions kicked in, and then expanded to 50k GPUs through alternative supply routes despite trade barriers but other press cites that they used Nvidia H800’s, which are compliant with the barriers.

- DeepSeek’s R1 release called into question US Big Tech’s dominance in AI and business models but at the same time, the performance and efficiency of DeepSeek is also seen as a boost for AI adoption overall

- R1 also shows that AI models can self-improve by learning from other models released by OpenAI, Anthropic, and others—which puts those companies’ existing business models, cost structures, and technological assumptions at risk

- DeepSeek is also being offered to consumers for free, while OpenAI charges $20/mo for its Plus subscription, and $200/mo for its Pro subscription

- Given DeepSeek’s model requires a lot less power, it also shows that AI could have a smaller climate impact than originally thought

- This called into question the AI power demand projections given that AI represents ~ 75% of overall US power demand forecasts through 2035 in most projections per Jefferies research

- But on the flipside, more competition and innovation in AI may also spur greater power demand, something known as the Jevons paradox

Does this get us closer to artificial general intelligence (AGI)?

Some industry experts believe R1 takes us one step closer

- AGI arriving sooner than expected would drive more demand for compute power

What was the reaction of key constituents / players in the space?

- Nvidia: “DeepSeek is an excellent AI advancement and a perfect example of Test Time Scaling. DeepSeek’s work illustrates how new models can be created using that technique, leveraging widely-available models and compute that is fully export control compliant. Inference requires significant numbers of NVIDIA GPUs and high-performance networking. We now have three scaling laws: pre-training and post-training, which continue, and new test-time scaling.” (link)

- Microsoft & OpenAI: While Sam Altman out of the gate said that “DeepSeek’s R1 is an impressive model” and that “we will obviously deliver much better models and also it’s legit invigorating to have a new competitor!”…Microsoft & OpenAI are investigating whether DeepSeek obtained its training data in an unauthorized manner to train its own AI (called distillation)

- DeepSeek says that it did distill data but from only open-source models (which OpenAI is not)

- Marc Andreessen called the product “AI’s Sputnik moment”

- President Trump: DeepSeek’s R1 release “should be a wake-up call for our industries that we need to be laser-focused on competing to win” …The model is a “positive development” that could allow for less expensive AI advancements across the board

- Trump also this week reportedly is considering additional curbs on the sale of Nvidia AI chips to China so that remains a wild card

- Howard Lutnick, President Trump’s Commerce Secretary pick: Suggested that the DeepSeek evaded US export controls and pledged a “very strong” response if he is confirmed as commerce secretary

- Anthropic co-founder Jack Clark: “DeepSeek means AI proliferation is guaranteed.”

- Amazon AWS CEO Matt Garman: “DeepSeek R1 is the latest foundation model to capture the imagination of the industry”

- AWS followed by added DeepSeek R-1 on Amazon Bedrock, SageMaker

Carnage was felt across several sectors… See notably big stock moves across tech and power related stocks

Telcos Shine With AT&T & T-Mobile Following Verizon’s Lead

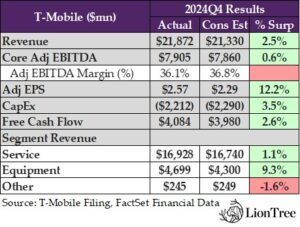

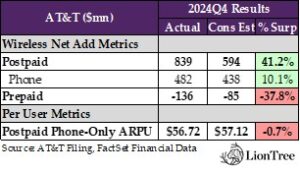

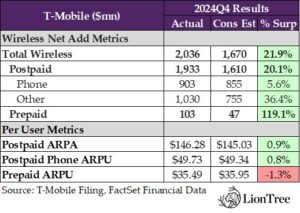

Following Verizon’s strong print last week, AT&T and T-Mobile kept the hot streak going for the telcos this week with earnings that were well-received by the market. AT&T and T-Mobile’s headline numbers were solid, though the former missed on adj EBITDA, and both came up a bit short on margins. Nonetheless, the real highlight from the two telcos’ results were stronger than anticipated performances on net add metrics. On the wireless side, AT&T’s postpaid phone net adds finished a comfortable +10.1% ahead of consensus forecasts and T-Mobile’s closed +5.6% above estimates. Similar to commentary from previous quarters, the telco’s Business segment was cited as a key contributor to their outperformance on postpaid phone net adds, and both anticipate that market share gains will drive growth in postpaid phone net adds throughout 2025. That said, it was notable that AT&T and T-Mobile’s postpaid phone net adds did take a step down on a y/y basis in Q4, which was in-line with AT&T’s prognostication of an ongoing normalization in the wireless market, though T-Mobile believes it can continue taking market share to drive growth.

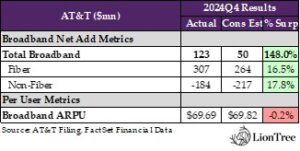

Trends were equally robust in the two telcos’ broadband businesses in Q4. T-Mobile touted that it once again led the industry with +428k high-speed internet net adds during the quarter, which beat the Street’s expectations by +5.2% and was driven primarily by “strong demand” from existing customers as well as switching activity from other broadband providers. For its part, AT&T’s +123k total broadband net adds topped expectations by a wide +148.0%, as sequential improvements in the company’s Fiber and Internet Air net adds offset continued declines in its legacy copper subscriber base. Notably, AT&T’s Fiber net adds benefited from pent-up demand related to a Southeast work stoppage that weighed on the segment’s Q3 performance, though management reassured that the impact was “not substantial.”

Looking ahead, the telcos expect to maintain momentum into 2025. AT&T reaffirmed guidance that was initially provided during its Investor Day last December, calling for an acceleration in consolidated service revenue growth as well as relatively similar levels of adj EBITDA growth in FY25 compared to the previous year. T-Mobile’s FY25 outlook implied an improving trajectory in top-line growth with the company’s “highest ever” postpaid net adds guidance. However, T-Mobile also anticipates a step down in core adj EBITDA growth to a ~+msd% cadence after increasing +9.1% y/y in FY24. All said, there was a lot for investors to like in the two telcos’ Q4 print – see below for more details:

-> AT&T shares rose +1.1% in reaction to the print and finished the week up +4.4%; T-Mobile shares jumped +6.3% in response to earnings and ended the week up +6.6%; YTD, AT&T stock is trading up +4.2%, and T-Mobile stock is up +5.6%; Notably, T-Mobile shares (+194%) have grown at nearly the same pace as Apple shares (+205%) over the last 5 years

The Telcos’ Headline Results Reflected Strength On The Top-Line, Though Adj EBITDA Margins Fell Short

- AT&T – Q4 headline results were MIXED, as rev BEAT while adj EBITDA MISSED: Rev incr’d +0.9% y/y in Q4 (vs -0.5% y/y in Q3) and topped cons by +0.9%; Adj EBITDA was up +2.2% y/y (vs +3.4% y/y in Q3) but closed a slight -0.4% below cons; Adj EBITDA beat cons by +8.0%; FCF finished +4.8% ahead of cons

- Mobility (~74% of Communications rev) – IN-LINE TO ABOVE: Q4 rev rose +3.3% y/y (vs +1.7% y/y in Q3) and beat cons by +1.5%; Adj EBITDA grew +6.1% y/y (vs +6.7% y/y in Q3) and was ~in-line w/ cons; Svs rev and equipment rev were both up +3.3% y/y

- Business Wireline (~15% of Communications rev) – MIXED: Rev was fell -10.0% y/y in Q4 (vs -11.8% y/y in Q3) and beat cons by +1.5%; Adj EBITDA was down -22.0% y/y (vs -20.0% y/y in Q3) and missed cons by -1.9%; Cited lower demand for legacy voice and data svs as well as product simplification for rev declines

- Consumer Wireline (~11% of Communications rev) – MIXED: Q4 rev grew +3.4% y/y (vs +2.6% y/y in Q3) but ended -1.3% below cons; Adj EBITDA rose +9.8% y/y (vs +8.6% y/y in Q3) and beat cons by +5.9%; Growing fiber revs offset declines in legacy voice and data svs

- T-Mobile – Headline numbers BEAT, but margins came in below estimates: Q4 rev grew +6.8% y/y (vs +4.7% y/y in Q3) and beat cons by +2.5%; Core adj EBITDA was up +10.1% y/y (vs +8.9% y/y in Q3) and closed +0.6% ahead of cons; Adj EPS topped cons by +12.2%; FCF ended +2.6% above cons

- Service rev (~77% of total rev) – BEAT: Rev rose +5.5% y/y in Q4 (vs +5.1% y/y in Q3) and beat cons by +1.1%

- Equipment rev (~21% of total rev) – BEAT: Q4 rev incr’d +12.6% y/y in Q4 (vs +4.3% y/y in Q3) and topped cons by +9.3%

Both AT&T And T-Mobile See Momentum From Q4 Carrying Into 2025

- AT&T reiterated FY25 guidance from its Investor Day last Dec –

- Consolidated svs rev growth in the ~+lsd% y/y range (vs +0.5% y/y in FY24)

- Mobility svs rev growth at the higher end of the +2-3% y/y range (vs +3.5% y/y in FY24)

- Consumer fiber broadband rev growth in the ~+mid-teens% y/y (vs +17.9% y/y in FY24)

- Consolidated adj EBITDA growth of ~+3% y/y or more (vs +3.1% y/y in FY24)

- Mobility adj EBITDA growth at the higher end of the +3-4% y/y range (vs +6.3% y/y in FY24)

- Consumer Wireline adj EBITDA growth in the ~+hsd-ldd% y/y range (vs +10.0% y/y in FY24)

- Business Wireline adj EBITDA to decline ~-mid-teens% y/y (vs -18.0% y/y in FY24)

- Adj EPS (excluding DIRECTV) between $1.97-2.07 (vs $1.95 in FY24)

- AT&T still expects the sale of its entire 70% stake in DIRECTV to TPG to close in mid-2025; This is estimated to result in an addt’l $5.4bn in after-tax cash payments this yr

- Consolidated svs rev growth in the ~+lsd% y/y range (vs +0.5% y/y in FY24)

- T-Mobile’s FY25 outlook included its “highest ever” postpaid net adds outlook: Notably, the Co significantly beat its initial FY24 postpaid net adds and adj EBITDA guidance

- Postpaid net customer adds guidance was5-6.0mn (vs 6.1mn in FY24): This is the Co’s “highest ever beginning of the year guide” for postpaid net adds (it initially guided for 5.0-5.5mn postpaid net adds at the start of FY24)

- Postpaid phone net adds are expected to comprise ~half of overall postpaid net adds in FY25: Implies +2.8-3.0mn postpaid phone net adds this yr

- Raised svs rev growth guidance from +4% to ~+5% y/y (and compare to +4.6% y/y in FY24)

- Postpaid ARPA growth guidance was ~+3% y/y

- Core adj EBITDA guidance of $33.1-33.5bn, represents a +5% y/y increase but slightly missed cons by -0.1% at the mid-pt

- Postpaid net customer adds guidance was5-6.0mn (vs 6.1mn in FY24): This is the Co’s “highest ever beginning of the year guide” for postpaid net adds (it initially guided for 5.0-5.5mn postpaid net adds at the start of FY24)

The Telcos’ Postpaid Phone Net Adds Were Lower Y/Y But Still Handily Outperformed The Street’s Forecasts / Strong Performance In Business Was A Common Thread

- AT&T – Q4 postpaid phone net adds were down y/y but better than anticipated: Fell -8.4% y/y to +482k (vs +403k in Q3) but still topped cons by +10.1%

- The Co has cont’d to see “a bit of moderation going on” in the postpaid phone mkt: Moving forward in 2025, AT&T expects a “healthy wireless mkt w/ further normalization of net adds and overall activity levels”

- BUT Business Solutions was an area of strength: This was particularly true for AT&T at the mid- to low-end of the mkt, which was mainly due to the improvements the Co has made in its distribution structure and how it’s working w/ partners

- FirstNet also remains a “consistent growth category”: FirstNet’s wireless connections grew by ~+300k seq, ending Q4 w/ 6.7mn+ in total

- AT&T’s Q4 postpaid upgrade rate was in-line w/ cons: It was 4.6%, down -10bps y/y (vs -40bps y/y in Q3), matching cons’ estimates; The Co is “not seeing anything out of pattern” in terms of customers’ desire to upgrade handsets, based on the devices & offers in the mkt in Q4

- Q4 postpaid phone churn was slightly up y/y and more than expected: Postpaid phone churn incr’d +1bps y/y to 0.85% (vs 0.78% in Q3), which was a touch above cons’ 0.84%; Customers reaching the end of end of their device promos returned to a more normalized level on a seasonal basis in Q4

- Looking ahead, gross add performance should “get a little better” relative to the Co’s mkt share: That said, the Co is not going to be seeing “outsized numbers… given the overall pool of growth is getting smaller,” w/ lower immigration being one potential factor

- The Co has cont’d to see “a bit of moderation going on” in the postpaid phone mkt: Moving forward in 2025, AT&T expects a “healthy wireless mkt w/ further normalization of net adds and overall activity levels”

- T-Mobile – Q4 postpaid phone net adds fell on a y/y basis but surpassed expectations: It was down -3.3% y/y in Q4 (vs +1.8% y/y in Q3) and beat cons by +5.6%; The Co once again led the industry in postpaid phone net adds and achieved its target of 3mn+ across FY24

- The Co delivered its “highest ever postpaid phone gross additions” in Q4…

- T-Mobile led the industry in postpaid switching share: The Co grew its share of households on a y/y basis across both the top 100 mkts as well as smaller mkts in rural areas, the latter of which represents 40%+ of the country

- T-Mobile for Business is also “gaining share rapidly”: Driven by multiple factors, including the Co’s T-Priority offer and other related 5G advanced svs, such as network slicing; For the tenth straight qtr, T-Mobile saw positive port trends across every part of the biz group

- The Co won a big contract w/ New York City: T-Priority, which provides +40% more capacity and 2.5x the speeds for first responders, was a significant factor

- Q4 upgrade rates ticked up both on a seq and a y/y basis: The device upgrade rate of 3.6% incr’d +40bps y/y in Q4 (vs -10bps y/y in Q3)

- Q4 postpaid phone churn was lower than anticipated: Q4 postpaid phone churn was down -4bps y/y to 0.92% (vs 0.86% in Q3) and below cons’ 0.97%

- The Co sees no weak spots in its biz moving through 2025: Indicated that it was “time to tune up” its postpaid net add guidance after seeing that “there’s just not an area that’s doing anything other than outperforming prior expectations”

- The Co delivered its “highest ever postpaid phone gross additions” in Q4…

AT&T And T-Mobile Saw Growth In Wireless Svs Rev Move In Different Directions Seq

- AT&T – Q4 Mobility svs rev growth decel’d seq: Incr’d +3.3% y/y (vs +4.0% y/y in Q3), driven by subscriber gains and postpaid phone ARPU growth

- Business Solutions wireless svs rev grew faster than overall Mobility svs rev: Was up +3.5% y/y in Q4; In addition to improving the distribution structure, growth in Business Solutions is “highly correlated” to economic growth

- AT&T also saw “some success” in the resell mkt: The Co has benefited from being a provider to DISH’s migration and has also seen that other MVNO reseller accounts “are now starting to generate some volume”

- T-Mobile – Q4 svs rev growth accel’d seq: Svs rev was up +5.5% y/y in Q4 (vs +5.1% y/y in Q3); FY24 svs rev rose +4.6% y/y (vs +3.1% y/y in FY23)

- Postpaid svs rev maintained a consistent rate of growth: Q4 postpaid svs rev rose +8.3% y/y (similar to Q3’s rate), which was more than twice the rate as the Co’s peers

- Prepaid svs rev growth improved seq: Prepaid svs rev incr’d +10.5% y/y in Q4 (vs +9.8% y/y in Q3)

- Wholesale and other svs rev reversed declines: Q4 wholesale and other svs rev fell -35.1% y/y to $738mn (vs $701mn in Q3), marking the first qtr in the last eight that wholesale rev has incr’d seq

- 2025 is still expected to be the low point for wholesale service rev: Given that Dish and TracFone are both in the process of building their own networks and offloading from T-Mobile’s network

Rate Plan Optimizations Have Been Major Contributors To ARPU/ARPA Growth

- AT&T – Q4 postpaid phone ARPU fell short of expectations: At $56.72, grew +0.9% y/y in Q4 (vs +1.9% y/y in Q3) and missed cons by -0.7%; As signaled exiting Q3, postpaid phone ARPU growth was mostly driven by targeted actions and changes in plan mix

- Segmentation of the customer base will drive future ARPU gains: AT&T has been looking at “pockets of [its] base” where it can get more value from moving customers to different plans or finding where it’s priced differently in the mkt”

- T-Mobile – Q4 postpaid ARPA growth accel’d seq and outperformed estimates: At $146.28, rose +4.3% y/y (vs +4.1% y/y in Q3) and finished +0.9% ahead of cons; The Co grew its postpaid ARPA at the highest rate in 7+ yrs due to the cont’d deepening of customer relationships and optimizations of rate plan structure

- Other drivers of ARPA growth –

- Many customers are “taking the oppty to self-select up the rate card”: T-Mobile cont’d to see 60%+ of new customers choose its premium plans during the qtr

- Higher sell-through of converged bundles: Cited fewer standalone fixed wireless net adds and more bundled customer growth

- Restructuring legacy rate plans could drive further ARPA growth in FY25: This effort was initiated in 2024 but wasn’t completed, as there are still “very outdated” legacy plans that the Co “can address at scale”

- Q4 postpaid phone ARPU was better than expected: At $49.73, was up +1.7% y/y in Q4 (similar to Q3’s increase) and topped cons by +0.8%

- Other drivers of ARPA growth –

The Telcos Reported Divergent Trends In Prepaid Net Adds

- AT&T – Q4 prepaid net losses were ~flat on a y/y basis but were worse than the Street forecasted: Net losses of -136k (vs -135k the prior yr qtr and -45k in Q3) were worse than cons’ -85k; Prepaid churn was down -24bps y/y to 2.73% (flat vs Q3), w/ Cricket phone churn being “substantially lower” during the qtr

- T-Mobile – Q4 prepaid net adds finished well ahead of estimates: Adds of +103k jumped +94.3% y/y in Q4 (vs +24k in Q3) beat cons by a wide +119.1%; The Co recorded +258k prepaid net adds across FY24 (vs +282k in FY23)

- The Co’s prepaid biz is “very insulated” from immigration trends: Immigration didn’t result in huge inflows of prepaid customers for the Co in 2022 and 2023 b/c its prepaid biz revolves around “the very highest premium monthly prepaid subscriptions”

- Prepaid churn took a slight step down y/y but was still higher than anticipated: Q4 prepaid churn of 2.85% was down -1bps y/y (vs -3 bps y/y in Q3) but was above cons’ 2.84%

- Prepaid to postpaid conversion dropped both on a seq and y/y basis: Q4 saw 160k prepaid to postpaid conversions (vs 175k in Q3), representing a -5.9% y/y decline

There Weren’t Many Major Changes In Competitive Positioning

- AT&T’s go-to-mkt strategy was “consistent” and “pretty disciplined” w/ promos in Q4: The approach “continues to resonate, as more customers are choosing and staying w/ AT&T”; Moving forward, the Co expects that upgrade rates won’t materially change “any time in the near future,” given that its strategy will remain the same

- T-Mobile’s story is “simple and it’s consistent”: The Co remains focused on leveraging its “sustainable, long-term structural advantages” by offering a “unique combination of best network, best value, and best experience”; Emphasized that T-Mobile is “not chasing growth for growth’s sake”

- “Rapidly growing” digital distribution capabilities are a “big part of [the Co’s] growth trajectory”: The Co highlighted its flagship digital platform T-Life, which saw 50mn+ downloads by the end of the yr (vs the 40mn that was originally expected) as well as “some incredible engagement numbers”

Broadband Was A Bright Spot For Both AT&T And T-Mobile

- AT&T – Q4 broadband net adds improved seq and BEAT estimates by a wide margin: Came in at +123k in Q4 (vs the prior yr qtr’s +19k and Q3’s +28k) topped cons by a wide +148%

- Broadband rev growth accel’d seq: Rose +7.8% y/y (vs +6.4% y/y in Q3); This propelled 2024 consumer broadband rev to close at a +7.2% y/y increase, which was above the initial FY24 guidance of +7% y/y

- Fiber net adds were the Co’s highest Q4 result ever and exceeded expectations: Grew +12.5% y/y to +307k in Q4 (+226k in Q3) and beat cons by +16.5%; The Co’s “incr’d pace” of expanding customer locations contributed to “solid subscriber growth”

- Net adds benefited from pent-up demand after a one-month Southeast work stoppage in Q3, though the impact was “not substantial”

- Fiber ARPU growth accel’d seq: Q4 Fiber ARPU of $71.71 was up +4.7% y/y (vs +3.2% y/y in Q3), w/ the “improved trend” being driven by pricing actions and favorable plan mix, including transitioning customers onto fiber vs copper legacy products

- Internet Air FWA “continues to perform well,” w/ net adds stepping up seq: Incr’d +158k (vs +135k in Q3 and +139k in Q2) brought the Co’s total 2024 FWA net adds to 0.5mn+; The Co continues to believe that selling Internet Air to bizs is a “great oppty” w/ “plenty of room to run”

- “Lower price shoppers are probably migrating more towards fixed wireless” compared to Fiber

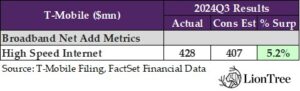

- T-Mobile – High speed internet (HSI) net adds incr’d seq and topped estimates: Fell -20.9% y/y to +428k in Q4 (vs +415k in Q3) and beat cons by +5.2%; T-Mobile once again led the industry in broadband growth, closing 2024 w/ 6.4mn HSI customers

- HSI growth was driven by “strong demand” from existing customers: Caveated that the “relative mix changes q/q” and that the Co “still had lots of new to T-Mobile customers come in,” of which the “vast majority” were “switching from something else”

- The biz segment continues to be a “great growth oppty” for FWA: The Co sees “a lot of oppties” for FWA to serve as the primary connection for multi-unit retail operations, pharmacies, insurance agencies, and other bizs w/ thousands of buildings across the country

- The Co’s 5G broadband pricing construct is “very competitive”: T-Mobile made some changes to its pricing construct in Q4 that allowed it to compete for “the most price-discerning customers” as well as create oppties for customers to “self-select up the rate card to more feature-packed plans”

- T-Mobile is “settling into a pattern at this level of growth on HSI”: Implies that HSI net adds will in the +400s per qtr moving forward; This cadence would enable the Co to reach its target of 12mn HSI customers by the end of 2028

- HSI growth was driven by “strong demand” from existing customers: Caveated that the “relative mix changes q/q” and that the Co “still had lots of new to T-Mobile customers come in,” of which the “vast majority” were “switching from something else”

AT&T Continues To Double Down On Converge, While T-Mobile Remains Skeptical

- AT&T’s fiber investment has helped drive the Mobility biz: The Co has been adding more converged customers, w/ AT&T Fiber at 40% penetration and 4 out of every 10 AT&T Fiber households are choosing AT&T as their wireless provider; These metrics improved by ~+100bps y/y, reflecting “strong demand” for fiber and 5G svs together

- The Co’s long-term target is 50% converged penetration: This was set at the Co’s Investor Day last Dec; Some mkts have already achieved this goal

- AT&T’s Guarantee program is a “truly converged full Co effort”: Introduced earlier in Jan, it spans across both wireless as well as fiber and covers both consumers and SMBs, providing bill credits for svs outages over a certain period of time, better deals on handsets, and prompt customer svs

- T-Mobile – “Americans are already operating in a converged world”: Pointed out that customers in the US have already had the option to purchase wireline and wireless from the same provider 80%+ of the time for 5+ yrs

- BUT a wireless-wireline bundle “doesn’t seem to be a core motivator of purchase in either category”: Highlighted that T-Mobile also experiences higher wireline attach rates in areas where its competitors have converged offers, suggesting “some selection bias” rather than causality, in competitors’ claims

Investment Targets From Each Co’s Most Recent Investment Day Were Reiterated

- AT&T remains focused on investing in 5G and fiber to drive “sustained growth” –

- The below targets are from the Co’s Investor Day last Dec –

- ~45mn owned and operated fiber passings by the end of 2029: This includes 6.5mn biz locations passed w/ fiber before the end of the decade; The Co 2024 w/ ~29mn total passings

- 5mn+ addt’l fiber passings from Gigapower and other commercial open-access agreements

- 50% fiber penetration in the longer-term

- Recent developments in Washington DC could also drive higher levels of network investment –

- Tax reform could free up more financial flexibility: The delta between AT&T’s current level of investment ($22bn) and its peak levels a couple yrs ago ($24bn) is equal to the increase in its current tax bill; Indicated the first place it would use “a little bit of latitude” is in accel’ing the fiber build

- The below targets are from the Co’s Investor Day last Dec –

- T-Mobile will “bolster investments across [its] network” to extend its network leadership in 2025: Emphasized that the Co already has “more available capacity per customer than anyone else” and was deemed the top provider in 46 out of 50 states by Ookla

- The fiber JVs will be “very efficient”: Leverages T-Mobile’s strengths in customer sales, svs, and mkting, while its partners are “some of the best in the US at laying fiber”; Won’t be a CapEx burden on T-Mobile

- The Co is gradually applying AI into its RAN to create AI-RAN: This will drive an evolution into 5G-advanced and “eventually even sixth generation” tech, though details remain vague

- T-Mobile’s Customer-Driven Coverage AI model enables its network to “self-heal”: This enables the Co’s network to “borrow” capacity from other sectors to “make sure nobody goes unconnected” when another portion of the network goes down

- AI will provide a “nice tailwind” for the Co’s biz on the consumer side: It’s still “early days,” but new AI use cases will enable T-Mobile to “increasingly showcase” its differentiation and its network advantages to customers

- T-Mobile isn’t concerned about FWA capacity constraints: Given that the Co only approves customers for 5G broadband when its algorithm says that it will have excess capacity in a particular sector for yrs to come

- Runing limited beta for Satellite service: “Satellite density is rapidly improving,” paving the way for commercial svs; The launch and monetization of its satellite connectivity partnership w/ Starlink in a “phased” manner; T-Mobile is now running a limited beta launch and then will begin offering to customers on its highest value plans

- There also oppties to sell satellite connectivity on an à la carte basis

Both Telcos Finished FY24 W/ Material Reductions In CapEx Levels

- AT&T – Q4 CapEx came in higher than consensus: Was up +48.7% y/y in Q4 (vs +14.1% y/y in Q3) and finished -12.8% higher than cons; But FY24 CapEx totaled $20.3bn, which was -14% y/y decline

- FY25 CapEx is expected to be ~similar to FY24 levels (at ~$22bn)

- T-Mobile – Q4 CapEx was lighter than anticipated: Rose +39.4% y/y (vs -19.1% y/y in Q3) but was still -3.5% below cons; FY24 CapEx of $8.8bn was down -9.8% y/y

- FY25 CapEx is still projected to be ~$9.5bn

Free Cash Flow Was A Bright Spot For Both Cos

- AT&T – Q4 FCF was better than projected: Was $4.8bn, down -24.2% y/y (vs -1.7% y/y in Q3) but still closed +4.8% above cons

- Q4 FCF included ~$1.1bn in pre-tax DIRECTV distributions…

- …BUT starting in Q1:25, all cash received from DIRECTV will be excluded from reported FCF

- FY25 FCF, excluding DIRECTV, is forecasted to be $16bn+: Assumes lower cash interest from lower debt balances, the absence of network termination fee payments in 2024, and lower y/y working capital balances

- FY25 FCF will also have a “more ratable profile”: Though also highlighted FCF will be seasonally lower in Q1, primarily driven by the timing of device payments and annual incentive compensation payout; DIRECTV also contributed $500mn+ to Q1:24’s FCF

- Q4 FCF included ~$1.1bn in pre-tax DIRECTV distributions…

- T-Mobile – Q4 FCF also surprised to the upside: At $4.1bn, fell -5.1% y/y in Q4 (vs +29.0% y/y in Q3) but still beat cons by +2.6%

- FY25 FCF, incl payments for merger-related costs, is projected to be $17.3-18.0bn (vs $17bn in 2024): Includes an expectation of ~$700mn in cash income tax payments and ~$3.9bn of incr’d cash interest payments

- Net cash provided by operating activities is expected to range from $26.8-27.5bn

- Repurchases will resume in H2:25: As part of the Co’s $14bn buyback authorization by the end of 2025 and under its broader plan of returning up to $50bn to shareholders over the next 3 yrs

- Recent transactions have all been contemplated in the authorization: Including USCellular, Metronet, Lumos, as well as other acquisitions and JV partnerships

- FY25 FCF, incl payments for merger-related costs, is projected to be $17.3-18.0bn (vs $17bn in 2024): Includes an expectation of ~$700mn in cash income tax payments and ~$3.9bn of incr’d cash interest payments

Other Highlights

- AT&T will soon make detailed fillings w/ the FCC to stop selling legacy products in ~1,300 wire centers: This represents ~25% of the wire centers across the Co’s footprint; The Co looks forward to working w/ the newly appointed FCC chair Brendan Carr

- T-Mobile sees the Vistar acquisition as an “oppty to transform” the Out of Home ad industry: The Co wants to combine Vistar’s tech platform and w/ its own customer intelligence to bring “new features into outdoor advertising that can transform the industry and bring things like measurability and impact to an advertising platform that hasn’t had them before”

- T-Mobile is adding a COO position to its roster: Srini Gopalan will start as T-Mobile’s on March 1 so that CEO Mike Sievert can focus more of his time on longer-term oppties and strategy; This comes as the Co gets “deeper into its challenger to champion plan”

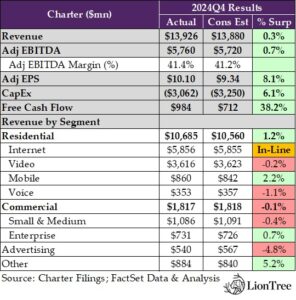

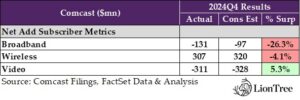

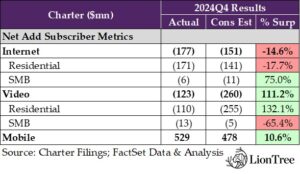

Comcast & Charter Faced Tougher Competitive Headwinds, But M&A Optionality Remains In Place

Joining the telcos (see Theme #4) in an earnings-packed week for the connectivity industry, cable companies Comcast and Charter jumped into the fray this week with their own Q4 prints, though these didn’t necessarily provoke the same response from the market. Despite broad headline beats, the cable companies continued to struggle in their core broadband segments during the quarter, with Comcast losing a net -131k broadband accounts (vs cons’ -97k) and Charter reporting -177k net Internet losses (vs cons’ -151k). In addition to a housing market that has remained “sluggish,” both cable companies contended with “potentially the most competitive environment” that they have faced in broadband, per Comcast CFO Jason Armstrong. Similar to previous quarters, Comcast and Charter acknowledged “significant competition” from fixed wireless providers and fiber overbuilders, but to note, competition from satellite was added to the list this qtr. Although the impact from satellite broadband was “de minimis,” Comcast is “not being dismissive of it” and will monitor it “very closely” moving forward. Additionally, Charter faced headwinds from the hurricanes in early October as well as from lingering ACP-related churn that combined resulted in ~-160k net losses.

In contrast, there was more room for optimism in the cable companies’ wireless businesses. While Comcast’s +307k wireless net adds fell -4.1% short of the Street’s expectations, it plans to “lean into wireless more than ever before” moving forward, highlighting that the industry has a TAM of $200bn compared to broadband’s more modest $80bn TAM. Consequently, the company will make additional investments in its wireless segment on the road ahead, though details on what this may entail were vague. Compared to Comcast, Charter’s mobile business fared better in Q4, as its +529k net adds finished a wide +10.6% ahead of estimates. The company’s investments in marketing, Spectrum One promotion, and efforts to reprice and repackage its converged offerings appear to have paid dividends in terms of brand recognition. Charter touted that Spectrum Mobile is now “widely recognized, both from a brand and capability standpoint,” and it intends to leverage this advantage to create more attach opportunities for broadband in 2025.

Lastly, a bright spot of the cable companies’ Q4 results came from the respective performances of their video businesses. The two continued to experience net video account losses during the quarter; however, these were less severe than anticipated. While Comcast didn’t have much to say regarding its video segment, Charter’s management believes that “video can become an asset again,” particularly within bundles that combine broadband, mobile, and video. Furthermore, the H1:25 launch of Charter’s seamless entertainment offering, which will provide TV Select customers with up to $80 of retail app value at no additional cost, is expected to further enhance the company’s video business in the coming year, though it isn’t necessarily expected to return to growth.

Looking ahead, it sounds like the cable companies don’t expect an immediate rebound in their core broadband businesses, but both will make investments to drive a recovery to the medium- to longer-term. Continuing to enhance their networks will be a key part of this strategy, as Comcast has already started to leverage network upgrades to create new broadband packages for consumers and Charter upped the amount of capital that it intends to spend on its ongoing network evolution initiative. FCF growth and returns to shareholders are important KPIs as well. See below for more details:

-> Comcast shares dropped -11.0% in reaction to the print and ended the week down -10.5%; Charter shares were up +2.6% in response to earnings (after falling -6.3% the previous day following Comcast’s earnings release) and finished the week down -6.0%; YTD, Comcast stock is trading down -10.3%, while Charter stock is up +0.8%

The Cable Cos’ Headline Numbers All Surpassed The Street’s Forecasts…

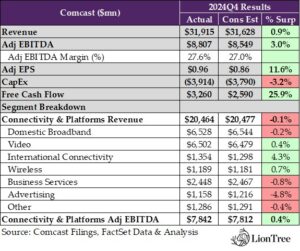

- Comcast – Q4 headline results broadly BEAT expectations: Consolidated rev incr’d +2.1% y/y in Q4 (vs +6.5% y/y in Q3) and closed +0.9% above cons; Consolidated adj EBITDA rose +9.9% y/y (vs -2.3% y/y in Q3) and topped cons by +3.0%; Adj EPS beat cons by +11.6%; FCF finished +25.9% ahead of cons

- Connectivity & Platforms (~64% of total rev) – MIXED: Q4 rev grew +0.2% y/y (vs +0.1% y/y in Q3) but fell a slight -0.1% short of cons; Adj EBITDA was up +3.5% y/y (vs +0.9% y/y in Q3) and beat cons by +0.4%; Residential Connectivity rev topped cons by +0.5%, but Business Services rev missed cons by -0.8%

- Broadband and wireless net adds MISSED, while video net adds BEAT

- Charter – Q4 headline numbers BEAT across the board: Q4 rev grew +1.6% y/y (similar to Q3’s rate) and beat cons by +0.9%; Adj EBITDA rose +3.4% y/y (vs +3.6% y/y in Q3) and closed +3.0% ahead of cons; Adj EPS topped cons by +8.1%; FCF ended +38.2% above cons

- Residential rev (~77% of total rev) – BEAT: Residential rev was down -0.4% y/y in Q4 (vs +0.3% y/y in Q3) but still topped cons by +1.2%; Residential customer relationships fell -2.2% y/y (vs -1.8% y/y in Q3), while monthly rev per customer was up +1.7% y/y (vs +1.8% y/y in Q3)

- Commercial rev (~13% of total rev) – SLIGHT MISS: Q4 Commercial rev incr’d +1.9% y/y (vs +2.0% y/y in Q3) and finished a slight -0.1% below cons; SMB rev was up +0.3% y/y (vs +1.0% y/y in Q3), while Enterprise rev rose +4.4% y/y (vs +3.7% y/y in Q3)

- Internet net adds MISSED, while wireless and video net adds BEAT

BUT The Cable Cos Dealt W/ “Potentially The Most Competitive Environment” That They’ve Faced In Broadband

- Comcast – “Competitive conditions remain intense… in all segments”: Highlighted that competition was “dynamic and varied across [Comcast’s] footprint and customer segments”; The Co “see[s] no signs of this changing in the near-term”

- Fixed wireless has “leveled” but is “still out there aggressively mkting”: Comcast believes that fixed wireless will “continue to sell into remaining excess capacity” in the near-term and carve out a “permanent part of the market” in the longer-term, despite being “capacity constrained”

- Fiber remains Comcast’s primary competition in most of its footprint: This effectively means that there will be two multi-gig symmetrical broadband providers for the “vast majority” of homes in the Co’s footprint; Will “settle into fairly equal mkt share amongst providers in the medium- to long-term”

- Fiber overbuilds are expected to continue in the shorter-term: Resulting in “early mkt share wins” for fiber providers

- Satellite was also mentioned as a competitor: Although the competitive impact from satellite has been “de minimis” and immaterial, Comcast is “not being dismissive of it” and will “watch it very closely”; So far, the Co sees satellite being more active in rural areas vs suburban and urban ones

- Charter – “The environment for broadband, mobile, and video remains competitive”: Flagged “significant competition from wireline overbuild, cell phone Internet, and satellite across all of [the Co’s] products”; Still, the Co has “better visibility than this time last yr”

- “Cell phone Internet net additions appear to have peaked or stabilized” …: Acknowledged “a little bit of competition” in rural mkts from FWA but believes this doesn’t impact wireline terminal penetration b/c demand for wired broadband “is still quite high”

- Competition from FWA has weighed on the early penetration of new passings: “There’s a little less jump at the very beginning than what [Charter] had seen previously”

- … And “there will be a declining base of fiber overbuild”: Highlighted that Charter “continue[s] to do well against new fiber overlap”

- “The housing mkt remains sluggish”: That said, this “hasn’t meaningfully reduced” the Co’s passings growth outlook

- “Cell phone Internet net additions appear to have peaked or stabilized” …: Acknowledged “a little bit of competition” in rural mkts from FWA but believes this doesn’t impact wireline terminal penetration b/c demand for wired broadband “is still quite high”

Comcast & Charter’s Broadband Net Adds Left Some Room To Be Desired

- Comcast – Q4 broadband net losses were worse than indicated last Dec: Net losses of -131k (vs -34k the prior yr qtr and -87k in Q3) were -26.3% worse than cons and worse than the “just over” -100k net losses predicted by the Co in mid-Dec; Comcast lost a net -131k residential customers (vs -79k in Q3) and -8k biz ones (similar to Q3)

- Total FY24 broadband net losses totaled -411k (vs -66k in FY23): Q4 marked the seventh consecutive qtr of broadband net losses for the Co and the worst amount over that timeframe

- The Co “may have been a little too optimistic” w/ the Q4 forecast provided in Dec: Indicated that this was particularly true in the price-conscious segment in the earlier part of the qtr in Dec; Heavy competition was cited as the main reason for this

- The SMB mkt faced similar dynamics as residential broadband: Comcast has been “operating in the same competitive environment” within the SMB segment

Comcast still has “a lot of levers” to drive growth moving forward: The Co plans to bring new offerings to mkt in Q2 and plans to “compete aggressively in the mkts… to drive cont’d broadband growth”

- Charter – Internet net losses were steeper than expected: Q4 net losses of -177k (vs -61k in the prior yr qtr and -110k in Q3) missed cons by -14.6%; Residential net losses of -171k were -17.7% worse than cons, though SMB net losses of -6k were better than cons’ -11k

- BUT excluding the impact of one-time items, Internet losses would have been ~-17k: Outside of the impact of the hurricanes and ACP-related factors, Charter was “generally pleased” w/ its Q4 core Internet results

- Hurricane Helene and Hurricane Milton caused ~-20k disconnects

- ACP-related churn resulted in ~-140k Internet net losses: This primarily consisted of non-pay as well as some voluntary churn; Still, the Co kept ~90% of former ACP customers connected, and the impact of the program’s end is now behind it

- The Co experienced ~-450k ACP-related subscriber losses in 2024: Not having this headwind in 2025 “will be huge”

- Net adds in the subsidized rural footprint were flat seq: Added a net +41k in Q4 (vs +41k in Q3 and +36k in Q2)

- Q1 results will see some impact from the Los Angeles wildfires: The Co will provide more details on the Q1 call and is still assessing the impact but acknowledged that ~15-16k passings in the mkt are no longer inhabitable and that its footprint covers the entirety of LA

- BUT excluding the impact of one-time items, Internet losses would have been ~-17k: Outside of the impact of the hurricanes and ACP-related factors, Charter was “generally pleased” w/ its Q4 core Internet results

Forward-Looking Commentary Revealed Some Puts & Takes For The Coming Yr

- Comcast provided some directional color on trends that it anticipates for 2025 –

- Broadband rev is expected to “continue on a growth trajectory”: W/ convergence rev growth again outpacing growth in broadband rev

- Business Services is projected to have the “same framework” of growth as it did in 2024: Indicated that the overall category of Business Services has been increasing at a +~msd% rate

- Margins are expected to expand at a “slightly lower rate”: Given the investments that Comcast wants to make back into its biz, including in wireless

- Charter sees several potential tailwinds behind its biz in 2025 –

- The Co is “really confident” about its ability to grow Internet in the mid-term: A “huge benefit” will come from moving past ACP-related losses, competitive pressures from FWA and fiber should ameliorate, rural passings will start to drive more growth, and data consumption continues to rise

- Sales & mkting expense is projected to grow ~+lsd-msd% y/y: Given customer acquisition efforts and the cont’d rollout of the Life Unlimited brand

- Programming expenses and cost to svs customers will be flat to slightly down y/y

- Adj EBITDA is expected to grow…: Anticipates that growth in mobile biz, new packaging and pricing around certain offers, as well as the Spectrum One promo roll-off and other rate benefits will drive growth; The Co’s high-margin advanced Wi-Fi product is also expected to make a “significant contribution”

- … Despite some one-time headwinds: Including the impact from a lack of political advertising and 2024’s Internet customer losses

- “2025 will have a slightly higher level of investment than 2024”: 2025 will be the Co’s “key capital investment” yr, but total capital spending will be on a “meaning downward trajectory” in following yrs, even inclusive of BEAD spending (see below for more details)

Both Comcast & Charter Saw A Seq Dip In ARPU Growth

- Comcast – Q4 broadband ARPU growth decel’d seq: Domestic broadband ARPU was up +3.1% y/y in Q4 (vs +3.6% y/y in Q3); Commentary was limited but previously the Co cited the competitive backdrop as a headwind

- The Co anticipates “cont’d healthy ARPU growth” in 2025: Cited a “new packaging approach” that leverages recent network upgrades and will be “hyper-focused on the high-end” as one of a “number of levers” to drive growth

- BUT “there could be some impact to ARPU” from attaching mobile to broadband packages: Still, the Co believes this is “absolutely the right thing to do over the long-run”

- The Co anticipates “cont’d healthy ARPU growth” in 2025: Cited a “new packaging approach” that leverages recent network upgrades and will be “hyper-focused on the high-end” as one of a “number of levers” to drive growth

- Charter – Q4 residential ARPU growth was a bit slower seq: Resi ARPU incr’d +1.7% y/y in Q4 (vs +1.8% y/y in Q3), driven by promo rate step-ups, rate adjustments, and Spectrum Mobile growth, partly offset by a higher mix of non-video customers, a higher mix of non-video customers, and $34mn of hurricane-related customer credits

- There weren’t any updates on Internet ARPU: The Co previously reported that Internet ARPU rose +3.1% y/y on a non-GAAP basis in Q3 and +1.7% y/y in Q2; Still, bundling video and mobile w/ broadband subscriptions has “add[ed] value back into the broadband relationship”

Convergence Will Be An Integral Part Of The Cable Cos’ Go-To-Mkt Strategy Moving Forward

- Comcast plans to shift its go-to-mkt strategy more towards converged bundles: Specifically, the Co plans to package mobile w/ more of its higher-tier broadband products for both new and existing customers; These will address “friction points” by introducing more simplicity

- The Co is also creating new products to appeal to its key customer segments: These new offerings will also provide more flexibility w/ attractive pricing; Highlighted its new Sports & News TV package that was annc’d last week as one example, given that “sports fans want and need great broadband”

- These packages are expected to sell more Xfinity Internet: As well as lower churn for existing subs

- A new COO of Connectivity & Platforms will also help shakeup Comcast’s mkting strategy: Steve Croney, who was promoted to the position in the past month, will be responsible for the Co’s residential and commercial bizs, including product strategy, sales & mkting, and customer experience, among other areas

- The Co is also creating new products to appeal to its key customer segments: These new offerings will also provide more flexibility w/ attractive pricing; Highlighted its new Sports & News TV package that was annc’d last week as one example, given that “sports fans want and need great broadband”

- Charter remains focused on investing to create a “virtuous cycle in its business: The positive impact from the Co’s customer commitment and brand refresh investments will take time to be recognized, though benefits are already starting to be evident

- Charter continues to ramp up the rollout of its Life Unlimited brand platform: The ability to bundle “two or three sets of products between really broadband, mobile and video” has allowed the Co to offer Internet at a lower price and create more attach oppties

- “It’s only going to get better”: Over time, the Co’s selling capabilities and training to re-bundle these svs will be “enhanced

- The Co hasn’t stopped offering Spectrum One: The offer of one free mobile line still “works well,” though Charter is now more focused on using mobile to drive broadband now that Spectrum Mobile has brand recognition in the mktplace

- Investments in customer svs have led to a “competitive advantage”: The Co’s investments in improving employees’ wages, basing its sales & svs staff in the US, and in real estate are “difficult to replicate”; These ultimately improve customer satisfaction, lower churn, and increase penetration

- Charter continues to ramp up the rollout of its Life Unlimited brand platform: The ability to bundle “two or three sets of products between really broadband, mobile and video” has allowed the Co to offer Internet at a lower price and create more attach oppties

Data Usage Remains On An Upward Trajectory

- Comcast flagged that traffic has been increasing at double-digit rates: NFL streaming and large game downloads drove “the biggest consumption in Internet history” this past fall; However, the Co didn’t provide figures on the avg monthly usage of broadband-only customers this qtr (was ~700 gigabytes per month in Q3)

- Charter – “Demand for faster Internet speeds continues to grow as data usage grows”: Monthly data usage by the Co’s non-video residential Internet customers reached 800+ gigabytes in Q4 (Previously reported that non-video Internet customers were using nearly 800 gigabytes per month in Q1)

Comcast & Charter’s Wireless Net Adds Diverged Relative To Consensus Forecasts But Remain A Key Focus Ahead

- Comcast – Q4 wireless net adds decr’d seq and underperformed estimates: Q4 net adds were down -1.0% y/y to +307k in Q4 (vs +319k in Q3) and missed cons by -4.1%; The Co closed out FY24 w/ 7.8mn total domestic wireless lines, an +18.8% y/y increase (vs +24.0% y/y in FY23)

- Wireless penetration of Comcast’s residential broadband base was similar seq: Wireless penetration remained at 12% of residential broadband customers, or ~6% of total passings, in Q4

- Comcast plans to “lean into wireless more than ever before” moving forward: Given that the Co is the “challenger” in a mkt that is 2.5x the size of broadband (wireless has an estimated $200bn TAM), w/ a “capital-light strategy that does not require network trade-offs”

- “Wireless is an integral part of [the Co’s] broadband strategy”: Given that it reduces churn, is a “key acquisition tool,” and drives Comcast’s “strong convergence rev growth” that continues to be at the high-end of the industry at ~+5% y/y

- There will be “addt’l investment” in wireless ahead: Resulting in a headwind to margins in FY25

- BUT Comcast is shifting away from its buy one line, get one free approach: “This is a fundamental shift that will impact acquisition, base mgmt, and retention,” though it will also drive more converged rev

- Xfinity Mobile customers will receive automatic speed boosts at WiFi hotspots: These boosts will be up to 1 gig when Xfinity Mobile customers connect to one of the Co’s 23mn WiFi hotspots

- Q4 converged rev growth continued to track at the high-end of industry benchmarks: Converged rev grew ~+5% y/y in Q4 (similar to Q3’s rate)

- “There’s no new news in terms of MVNO approach”: Comcast is “pleased w/ [its] current position” and didn’t signal any intention of attempting to adjust its MVNO contract when it comes up for renewal later this yr

- Charter – Q4 mobile net adds declined seq but still exceeded expectations: Mobile net adds fell -3.1% y/y to +529k in Q4 (vs +545k in Q3) but still topped cons by a wide +10.6%; Charter exited FY24 w/ 9.9mn total mobile lines, representing a +27.3 y/y increase

- The Spectrum Mobile biz “cont’d to grow at a rapid rate”: Touted that Spectrum Mobile remains the fastest-growing mobile svs in the US

- Still, mobile penetration of Charter’s broadband base was ~flat seq, remaining at ~8% of total passings

- Mobile svs rev growth was ~flat seq: Q4 mobile svs rev incr’d +37.4% y/y (vs +37.6% y/y in Q3), driven by mobile line growth as well as higher svs rev per line; Commentary was sparse, but last qtr the Co cited the Anytime Upgrade offer as a driver of mobile ARPU growth

- 87% of Spectrum Mobile’s traffic is carried on the Co’s network: This number is expected to increase moving forward via addt’l CBRS deployment as well as Charter’s expanding Wi-Fi capabilities; The Co believes “there’s no pressure” to feel like it needs addt’l owner’s economics beyond this

- The Spectrum Mobile biz “cont’d to grow at a rapid rate”: Touted that Spectrum Mobile remains the fastest-growing mobile svs in the US

Efforts To Stem Video Net Losses Have Been Bearing Fruit

- Comcast – Q4 video net losses improved seq and were less steep than expected: Q4 net losses of -311k (vs -389k the prior yr qtr and -365k in Q3) were +5.3% better than cons; This also marked the Co’s best result in the last sixteen qtrs, though Q4 tends to see a seasonal reduction in net losses

- Video rev also finished ahead of the Street’s forecasts: Video rev was down -6.4% y/y in Q4 (vs -6.8% y/y in Q3) and topped cons by +0.4%, as a decline in the number of video customers was partially offset by an overall increase in avg rates

- Otherwise, commentary on the video biz was sparse: The Co didn’t provide updates on the NOW portfolio or the StreamSaver offering after highlighting them last qtr; There also wasn’t any color on the progress of Comcast’s renewal discussions around distribution agreements

- Charter – Q4 video net losses improved materially seq and much better than anticipated: Net losses of -123k (vs -257k in the prior yr qtr and -294k in Q3) beat cons by a wide +111.2%; Resi net video losses were +132.1% better than cons, though SMB video net losses of -13k were worse than cons’ -5k

- The improvement was driven by efforts to re-bundle video within the Life Unlimited platform: Notably, the Co’s video performance does not yet reflect the benefits of incorporating seamless entertainment apps in its product

- The Co’s new programming allow for more flexibility in packaging video: Charter has been able to create video packages that offer more value to customers, and this has provided the Co w/ the confidence to begin actively selling video alongside broadband subscriptions once again

- “Video can become an asset again”: Caveated that this “doesn’t mean that [Charter is] going to grow video,” but the Co views it as a “significant asset” that can be combined w/ mobile and broadband “to drive growth to a unique set of products and save customers a lot of money”

- The timing around Charter’s launch of a seamless entertainment offering in 2025 hasn’t changed: The Co still plans to fully roll out the seamless entertainment product in H1:25 and deliver up to $80 of retail app value for its TV Select customers at no addt’l cost

- The improvement was driven by efforts to re-bundle video within the Life Unlimited platform: Notably, the Co’s video performance does not yet reflect the benefits of incorporating seamless entertainment apps in its product

Lower Programming Costs Drove Upside In The Cable Cos’ Adj EBITDA Margins

- Comcast – Q4 Connectivity & Platforms adj EBITDA margin topped estimates: The segment’s adj EBITDA margin improved +120bps y/y to 38.3% in Q4 (vs 40.9% in Q3), beating cons by +17bps; Excluding severance and other factors, margins expanded by +80bps y/y

- Residential Connectivity & Platforms adj EBITDA margin expanded to a higher degree seq: Q4 adj EBITDA margin of 36.0% incr’d +120 bps y/y (vs +20 bps y/y in Q3); Lower programming expenses due to a decline in video customers was partly offset by rate increases under domestic programming contracts

- Business Services adj EBITDA margin improved on a y/y basis: Adj EBITDA margin of 55.7% rose +50bps y/y in Q4 (vs -10bps y/y in Q3)

- Hurricanes Milton and Helene had a “modest negative impact” on margins during the qtr: The hurricanes affected growth in both Residential and Business Services adj EBITDA margins

- Charter – Q4 adj EBITDA margin surprised to upside: Q4 adj EBITDA margin expanded +80bps y/y to 41.4% (vs +40.9% in Q3) and topped cons by +20bps

- A breakdown of expense items –