The LionTree family’s hearts go out to everyone impacted by the devastating fires in Los Angeles. Many of our friends, clients, and loved ones have been personally affected or know someone facing unimaginable loss and devastation. In these unprecedented times, we remain steadfast in prioritizing humanity above all else.

Below are vetted donation platforms LionTree is contributing to financially support first responders and displaced individuals and families. We encourage everyone to unite and show compassion, care, and generosity for those in need. Thank you for standing with us as we monitor and support our community during the ongoing fires, and as we look forward to rebuilding, together.

- American Red Cross is providing shelter, food, and recovery.

- Baby2Baby is providing critical items, including diapers, food, formula and hygiene products for children and families who have lost their homes to the fires.

- World Central Kitchen is providing sandwiches and water throughout the affected regions.

- Los Angeles Fire Department Foundation has requested donations for its wildfire emergency fund which supplies firefighters with tools and supplies to contain the fires.

- California Community Foundation’s Wildfire Recovery Fund is providing immediate needs for victims including shelter, food, cash, and other basic necessities.

- Jewish Federation of Los Angeles has a wildfire crisis fund and a host of additional resources.

Thank you for your consideration.

In terms of the markets and key sector updates, it has been a volatile start to the year, The S&P and Nasdaq were down -1.9% and -2.3%, respectively this week on the back of strong economic data (especially Friday’s Payroll data) that may support the higher for longer interest rate view. Sector-wise, we focused on the below themes and developments in this edition (all clicks are clickable):

- 7th Annual LionTree Sector Themes Survey - Please Participate!

- LionTree’s Lens: Sector Insights & A Look Ahead, Winter 2024 - *NEW DECK*

- CES 2025 – The Next Round Of AI Updates…

- The Video Streaming App Consolidation Cycle Has Begun… Disney’s Hulu+ Live TV Joins Forces With Fubo

- Q4 Stock Wrap – AppLovin, Reddit, & Lemonade Come In On Top… China Internet Takes It On The Chin

- What Stocks Are Wall Street Analysts Most Bullish & Most Bearish On To Start The Year?

- Short Sellers Have A Couple Of New Top TMT Targets To Start The Year…

- US Consumers Splurged During The Holidays But With Some Caveats…

- Grab Bag: Flutter Pre-Announced Q4 Results/Netflix’s WWE Debut Was A “Mega Success”/New Streaming Stats

Best,

Leslie

7th Annual LionTree Sector Themes Survey - Please Participate!

Our 7th Annual TMT Themes survey is live, and we would love your participation. It includes ~20 quick questions about the market, sector, and company expectations. It should take ~5-8min to complete. Also, as a reminder, our rule is that we send the survey results ONLY to those who participate!

**CLICK HERE** to participate.

Last year’s survey respondents underestimated the growth of the global ad market in 2024. 54% of respondents said that the broader ad market would grow in-line with Dentsu and GroupM’s projected +4.6-7.2% range, though both companies now predict 2024 will close showing a +6.8-9.5% y/y increase. Will respondents correctly predict ad market trends for 2025?

We will also be gathering insights on the M&A & regulatory environment, the AI CapEx trajectory, the ARPU impact from a super-premium music subscription tier, a Tik Tok ban, autonomous vehicle penetration, Take-Two’s GTA launch, ESPN’s flagship DTC adoption, and more!

For reference, HERE are last year’s survey results.

LionTree’s Lens: Sector Insights & A Look Ahead, Winter 2024 - *NEW DECK*

Before the holiday’s we published the Winter edition of our LionTree’s Lens: Sector Insights & A Look Ahead which highlights what we thought were the most important themes in Q4 and outlines some of our key expectations for 2025.

If you missed it and are interested…**

CLICK HERE for access to the ~25-minute video narration of the deck and access to the standalone slides as well **

Table of Contents

Macro & Markets

- The Market’s Hot Streak Has Continued… But Valuations Are High

- Investors Have Been Diversifying Beyond Big Tech

- Recent KPIs Point To A More Resilient Than Expected Macro Picture

- Holiday Shopping Reports Also Reflect Consumers’ Willingness To Spend

- Expect Select Large IPOs To Define The 2025 Market

- The Low Hanging Fruit For Cost Cutting Is Getting Harder To Find

- Growing Profitability Looks To Remain A Priority In 2025

Top-Down Themes

- The Upcoming TRUMP 2.0 Era Likely Brings Opportunities & Challenges

- M&A Speculation & Chatter Is On The Rise

- Regulatory Pressure On Big Tech Has Been Mounting Across The Globe

- How Much Longer Can The AI Frenzy Last?

- 2025 Should Reflect A Broadening Of Gen AI Use Cases

- Big Tech & Last-Mile Are Revving Up Efforts W/ Autonomous Vehicles

- Music Has Several Chords Of Growth In 2025

- The Digital Audio Advertising Opportunity & TAM Is Under-Appreciated

- Sports Streamers Are Stacking Up Better In The Battle Between Reach & Monetization

- Anticipate More Milestones & Strong AVOD Growth In 2025 But Off A Small Base

- Pay-TV Provider Are Repositioning To Adapt To The Times

- Cable Made A Comeback In Q3, But The Telcos Are Reloading FWA & Fiber Initiatives

- Wireless Business Customers Will Be A Targeted Growth Area In 2025

- Live Entertainment – Premium & International Will Be Key Drivers In 2025

- New Theme Parks & Experiences Are Expected To Drive A Turnaround

- OTAs – Competition Is Picking Up In Alternative Accommodations

Wall Street Sentiment

- Wall Street’s Top TMT Picks & Pans

- Wall Street Sees A Lot Less Upside To Company Share Prices Vs In August

-> We are more than happy to arrange calls with company executives or investment teams to delve deeper into any of these themes. All feedback and thoughts are always welcome and greatly appreciated.

CES 2025 – The Next Round Of AI Updates…

With 138k+ attendees and 4,312 exhibitors, including 323 of the Fortune 500 companies, CES 2025 continues to be the world’s preeminent technology show, bringing together visionaries and thought leaders from across the globe to share their latest innovations and ideas. Last year’s conference was notable for a nearly universal focus on AI, and the trend continued this year, with exciting new updates from NVIDIA and AMD on the next generation of chips to support emerging AI-powered use cases as well as announcements pertaining to what some of those use cases could look like. In particular, we highlighted how AI is being incorporated into the next-generation of smart TVs and also included some color on some exciting new developments in the world of electric vehicles. See below for more details on what we thought were some of the most incremental updates from the show.

Chipmakers Annc’d New Hardware Optimized Specifically For AI Use Cases

- NVIDIA CEO Jensen Huang introduced a new generation of GPUs, the RTX 5000 Blackwell series (link): Huang provided a first look at the GeForce RTX 50 Series, including the RTX 5090, RTX 5080, RTX 5070 Ti, and RTX 5070; The new series is “equipped w/ a massive level of AI horsepower” and incorporates DLSS 4 tech

- The GeForce RTX 5090 ($1999) is “the most powerful GeForce GPU ever made”: The RTX 5090 succeeds the RTX 4090 and will have 32GB of GDDR7 memory; It will be available starting on Jan 30

- The RTX 5090 Founders Edition is compatible w/ NVIDIA’s SFF-ready program: This means the RTX 5090 will be suitable for mini ITX cases; The card is small enough to be compatible w/ the smallest gaming PC cases available

- The RTX 5080 ($999) is “built for game-changing experiences”: The RTX 5080 has 16GB of GDDR7 memory and can run the most graphically-demanding games and creative applications; The card will be available on Jan 30

- The RTX 5070 ($549) will perform similarly to the RTX 4090 in certain titles: However, a Co representative caveated that “this does not mean a 5070 can beat a 4090 in every single way”; The RTX 5070 will have 12GB of GDDR7 memory and will come out later in 2025

- The GeForce RTX 5090 ($1999) is “the most powerful GeForce GPU ever made”: The RTX 5090 succeeds the RTX 4090 and will have 32GB of GDDR7 memory; It will be available starting on Jan 30

-> On a separate but related note, NVIDIA also annc’d at CES that it’s releasing a personal AI supercomputer called Project Digits in May; Project Digits incorporates the new GB10 Grace Blackwell Superchip, which contains enough processing power to run sophisticated AI models while being compact enough to fit on a desktop and operate using a standard power outlet; The system will be ~1,000x more powerful than the best PCs and laptops currently available, will handle AI models w/ up to 200bn parameters and is designed for AI research, data science, and high-performance computing tasks; Project Digits will start at $3,000 (link)

-> NVIDIA CEO Jensen Huang also caused a stir earlier this week during an analyst Q&A session at CES w/ his declaration that useful quantum computers are still many yrs away – “If you said 15 yrs for very useful quantum computers, that would probably be on the early side… If you said 30, it’s probably on the late side. But if you picked 20, I think a whole bunch of us would believe it”; Following this statement, Rigetti Computing, IonQ, D-Wave Computing, and Quantum Computing’s shares fell ~-40% on Jan 8 (link)

- AMD unveiled new CPUs and GPUs at CES (link): Along w/ revealing the Ryzen 9 9950X3D and Ryzen 9 9900X3D top-end gaming CPU cores, which feature Team Red’s 3D V-Cache tech, AMD execs also annc’d the Co’s latest mid-range GPU lineup, the RX 9070 series

- AMD’s new CPU cores will be up to +54% faster than the last-gen AMD Ryzen 9 7950X3D: The new processors will also provide up to +64% better gaming performance than the Intel Core Ultra 9 285k, offering more cores, more cache, and a higher clock rate than the AMD Ryzen 7 9800X3D that launched back in Nov

- The Ryzen 9 9950X3D and Ryzen 9 9900X3D will be available within the next few months: However, AMD still hasn’t annc’d any details on pricing for the processors

- The RX 9070 series of GPUs will have two variants – the RX 9070 XT and the RX 9070: The chips are intended to compete w/ NVIDIA’s new RTX 5070 Ti and RTX 5070, respectively; The new GPUs will exclusively feature AMD’s latest AI-enhanced upscaler, the FSR 4

- AMD’s new CPU cores will be up to +54% faster than the last-gen AMD Ryzen 9 7950X3D: The new processors will also provide up to +64% better gaming performance than the Intel Core Ultra 9 285k, offering more cores, more cache, and a higher clock rate than the AMD Ryzen 7 9800X3D that launched back in Nov

No details on the release date or pricing have been released yet

The Next-Gen Of Electric Vehicles Will Incorporate Some Groundbreaking Features

- Sony provided more details on its Afeela 1 EV (link): The four-door Afeela EV was developed as part of a JV between Sony and Honda and was initially introduced in 2023 w/ a focus on luxury and entertainment; The Origin model will start at $89,900 and debut in 2027

- The Afeela leverages expertise from both Cos: The EV combines the reliability and manufacturing know-how of Honda w/ the infotainment and software capabilities of Sony; The interplay between software and hardware, such as sensors and screens, is integral to the car’s design

- A higher-tier version w/ more expensive trim will start at $102,900: The Signature model includes 21-inch wheels, a rear entertainment system that provides access music, movies, and video games, as well as a central camera monitoring system

- The Signature model will be available in 2026

- Both models come w/ a complimentary 3-yr subscription: The subscription includes Afeela Intelligent Drive, a Level 2+ driver assistance system that utilizes 40 sensors, as well as Afeela Personal Agent, which is a voice assistant that can control in-car functions and carry convos w/ users

- The subscription also incorporates a variety of addt’l features: Such as an array of entertainment content, customizable digital themes for the screens, and 5G data connectivity

- Pre-orders can be made for a refundable $200 fee: However, only customers in California are currently eligible to make a reservation

The Sony Honda Afeela 1 will be offered w/ three exterior paint options

- Hyundai Mobis revealed the “world’s first” full-windshield holographic display (link): The tech, which uses a specialized holographic optical element film, was developed in conjunction w/ the German Co ZEISS, and allows drivers and passengers to access essential info through the front windshield

- The tech eliminates the need for a traditional display: The holographic windshield shows driving data, navigation, and music playlists, and other important data without the need for addt’l display devices; The crystal-clear visuals are visible even in bright outdoor lighting conditions

- The windshield looks like standard traditional glass from the exterior

- BUT the holographic windshield isn’t yet available for mass production: Hyundai and ZEISS are aiming to complete pre-development by mid-2026 and plan to commercially launch the product in the global auto mkt by 2027

- The tech eliminates the need for a traditional display: The holographic windshield shows driving data, navigation, and music playlists, and other important data without the need for addt’l display devices; The crystal-clear visuals are visible even in bright outdoor lighting conditions

- Aptera Motors debuted a production-ready solar-powered EV (link): The three-wheeled EV eliminates the need for traditional charging for most daily usage, providing up to 40 miles of range per day from sunlight alone; This equates to up to ~6,200 miles of solar-powered driving annually

- Aptera’s EV is purpose-built for modern commuting: The car offers a maximum range of 400 miles on a single charge and can fully recharge in less than an hour using standard charging infrastructure

- A lightweight build also enhances durability and lowers production costs: The design incorporates one-tenth of the parts of a conventional car

- The EV already has close to 50,000 reservations: This suggests there is strong global demand for zero-emission vehicles

- Aptera’s EV is purpose-built for modern commuting: The car offers a maximum range of 400 miles on a single charge and can fully recharge in less than an hour using standard charging infrastructure

AI Is Becoming An Integral Feature In Smart TVs

- Samsung’s 2025 lineup of TVs are coming w/ a host of new AI features (link): These new AI-powered experiences, dubbed Vision AI, will deliver better picture quality, optimized sound, and other quality of life improvements; Microsoft Copilot will be part of Vision AI

- Click to Search can provide tailored info in real-time: By pressing the new AI button on their SolarCell remote, users can use Click to Search to identify people, places, and products on their screen

- Samsung Food also leverages AI to provide recipes and create shopping lists: Samsung TVs will now be able to show users how to make dishes from movies or TV shows; Samsung Food can also analyze what’s in their fridge and build a shopping list of missing ingredients

- Users can purchase groceries or takeout from their TV using provider apps

- AI will also support security and accessibility features: Samsung TVs can be transformed into smart security hubs using Samsung AI Home Security, which can analyze video feeds from connected cameras and audio from a TV’s microphone, detecting unusual sounds and movements

- Upgrades to existing features: Include AI Upscaling, Auto HDR Remastering, and Adaptive Sound Pro

- Samsung’s new TV models for 2025 –

- The Frame Pro: The upgraded model, which is designed to blend in w/ home décor and show art pieces when not in use, now comes w/ a Neo QLED display, a boosted refresh rate, and improved brightness to showcase more details than the existing Frame model

- QN990F and QN900F Neo QLED 8K TVs: These ultra-premium TVs feature the Wireless One Connect Box, which can wirelessly transmit up to 10m away

- A new QLED 4K TV lineup: Along w/ incorporating Vision AI, these TVs come in larger sizes, offer higher frame refresh rates, and a better visual experience

The Frame Pro

- LG showcased its new OLED Evo line of 4K TVs (link/link): The M5 and G5 models come w/ new AI and connectivity features as well as improvements to picture quality and brightness; The models also feature a new AI remote as well as a processor optimized for sports viewing and gaming

- The M5 and G5 models mostly offer the same capabilities –

- BUT the M5 offers a more futuristic and wireless design w/ a Zero Connect Box capable of wireless transmitting at up to 144Hz without latency or quality loss; While the previous M4 iteration required line-of-sight signaling, the new M5 provides more flexibility in positioning

- The G5 has a better native refresh rate, offering 165Hz, which should reduce input lag and disruptions to gameplay

- Addt’l enhancements offered by both models include –

- Better upscaling of low-resolution content: Given that LG’s latest α11 AI processor Gen2 is running the WebOS

- Upgraded Brightness Booster Ultimate tech: This enhances light control architecture for brightness up to +3x higher than conventional OLED models; The G5 is reportedly up to +40% brighter than last yr’s G4 model

- Support for Filmmaker Mode w/ Ambient Light Compensation: This automatically adjusts picture settings to account for the viewer’s lighting conditions and to maintain the filmmaker’s original intent

- LG is also adding a dedicated AI section to its TVs that will incorporate Microsoft Copilot: Copilot will allow users to “efficiently find and organize complex info using context cues,” though the Co hasn’t demonstrated this integration yet

- The M5 and G5 models mostly offer the same capabilities –

- Google is adding its Gemini AI model to TVs running its OS (link): The Co previewed the new capabilities, along w/ the Google Assistant’s voice controlled system, at CES; The updated version of Google’s TV software, which is set to debut later this yr, includes the following capabilities –

- Users will be able to have back-and-forth convos w/ third-party TVs: To do so, they won’t have to employ the “Hey Google” trigger phrase for each command

- Content will be able to be called up more naturally: One example spotlighted was asking Gemini to view videos saved to a user’s Google Photos account

- An “always-on” mode will use sensors to tell if a user is approaching: If the TV senses that a user is in front of it, it will show them info they might find useful, including news reports or weather forecasts

The Video Streaming App Consolidation Cycle Has Begun… Disney’s Hulu+ Live TV Joins Forces With Fubo

The video streaming sector and, specifically, the vMVPD space, saw a major shakeup this week, as Fubo announced a combination of its live TV streaming service and Disney’s Hulu+ Live TV, in addition to an injection of new capital. Along with “instantly making Fubo the major player in the streaming space,” per Fubo CEO David Gandler, the merger is also expected to result in the combined company becoming “immediately” cash flow positive. By 2028, the Co is expected to generate over $7.5bn in revenue and over $550mn in adj EBITDA. While the apps won’t be immediately integrated post the deal closing and will be offered separately, Fubo will be in a better position to leverage its newfound scale to negotiate better economics on licensing agreements and potentially launch a skinnier sports, news, and entertainment bundle (the Co has negotiated new deals with Disney and Fox, which sets the stage).

Also to note, the deal settled litigation between Fubo and Disney pertaining to Venu, the sports streaming joint venture between Disney, Fox, and Warner Bros. Discovery, but interestingly, and as a surprise turn of events, at the end of the week, Disney, Fox, and WBD announced that they decided not to move forward with the JV after all.

Net-net, given the over-proliferation of video streaming services and scarce levels profitability, consolidation in the sector has been expected to emerge for some time… Now, this cycle has more clearly begun.

See below for what we thought were the most important aspects regarding the announced transaction and other related updates.

-> FUBO shares jumped +251% following the news and ended the week up +255%; Disney’s stock was ~flat in response and closed the week down -2.3% after taking a hit post the Venu update; Fubo stock is up +61% since the start of 2024, and Disney stock is up +20.3% over the same period

- Deal basics – Disney to combine the Hulu+ Live TV biz w/ Fubo into a new entity (the deal doesn’t include the Hulu streaming svs)

- Timing: The deal is expected to close in 12-18 months

- Ownership – Disney will own 70% of the combined Co…with Fubo shareholders will own the remaining 30%

- BUT the combined Co will be led by Fubo’s mgmt team: The combined Co’s new board of directors will be majority appointed by Disney

- Termination fee: If the deal falls through, Fubo will receive a $130mn termination fee

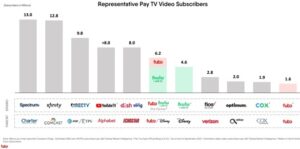

- The NewCo is better positioned in the competitive pay-TV market, given the higher scale

- 2mn North American subscribers (vs Fubo standalone 1.6mn subscribers as of Q3:24)

- $6bn+ in proforma revenue and over +10% growth

- Multi-year guidance calls for strong rev growth and margin expansion

- The combined Co is projected to be immediately CF positive

- See below for proforma revenue and adj EBITDA guidance for 2026-2028; It implies adj EBITDA margin expansion from 5.2% in 2026 to 7.3% at the mid-pt

- The expected synergy run rate is $120mn+

- Fubo drops its lawsuit regarding the sports streaming svs Venu (joint venture with Disney/ESPN, Fox & WBD)

-> But at the end of the week, Disney, Fox, and WBD announced that they decided not to move forward with the JV despite Fubo dropping their lawsuit…

- Fubo gets an injection of capital

- When the deal is signed, Disney, Fox, and Warner Bros Discovery will together make a $220mn cash payment to Fubo (this isn’t contingent on the deal closing)

- Disney will also commit a $145mn term loan to Fubo in Jan 2026 (which isn’t contingent on the deal closing) which will help Fubo close out its 2026 convertible notes without diluting equity shareholders

- Both Hulu+ Live TV & Fubo will be available separately to consumers after the deal closes: Users will still be able to stream Hulu+ Live TV through the Hulu app as well as through Disney’s bundle, which includes Hulu, Disney+, and ESPN+

- “Having two separate platforms today obviously is not ideal”: However, right now, Fubo wants to “really focus on providing consumers the choice,” and there is also “a lot of value” in the Hulu brand “w/ respect to maintaining retention”

- Fubo also entered into new carriage agreements with Disney and Fox which creates the potential to offer skinnier bundles:

- Added scale will enable the combined Co to negotiate licensing deals w/ better economics: This is the “bigger piece” contributing to the growth of the combined Co’s adj EBITDA

- Fubo has “the potential” to create skinnier sports, news, and entertainment bundles: “It will be a lower cost bundle w/ fewer networks in there,” though Fubo still hasn’t determined specifics

Q4 Stock Wrap – AppLovin, Reddit, & Lemonade Come In On Top… China Internet Takes It On The Chin

It was a volatile last couple weeks in the market at the end of the year, but the indices still ended well in positive territory in Q4, with tech making a relative comeback from Q3. NASDAQ’s +6.2% gain in Q4 (which was up from the +2.6% gain in Q3) outpaced the S&P 500’s +2.1% (which was down from Q3’s +5.4% increase).

Digging into the S&P 500, drivers of Q4’s positive performance were fairly concentrated, as just four of the sectors traded up, on average. Communication Services led the way (up +6.2%), followed by Financials (+5.1%), Consumer Discretionary (+2.2%) and Energy (+2.0%). Information Technology fell into negative territory in Q4, down -0.4%, on avg, from Q3’s +3.6%. Consumer Staples were under pressure, down -6.9%, on avg, in Q4 (from being up +5.6% in Q3). Materials was the worst performing sector, down -12.7%, on avg.

Finally, examining the performance of our LionTree Universe, made up of ~180 stocks in the TMT and Consumer sectors with $1bn+ in market cap, the percentage of stocks up vs down in Q4 narrowed vs prior quarters. While 55% of stocks traded up, it was a step down from 71% in Q3 (though still an improvement over 43% in Q2 and 52% in Q1). The magnitude of positive performance was also more modest, with 36% of stocks trading up by double digits or more in Q4, compared to 44% in Q3 and 46% in Q2.

Which stock saw the biggest gains in Q4? AppLovin. Its shares were up +148.1% in Q4 following the +56.9% rally in Q3, driven by a strong Q3 earnings print and continued growth in its AI-powered advertising offering; It was followed very closely by Reddit, up +147.9%, and Lemonade, up +122%, to round out the Top 3 best performers of Q4

On the flip side, which stock had the toughest Q4? Eutelsat Communications. Its shares were down -43.2% in Q4, followed by Oscar Health, down -36.6%, and Liberty Latin America, down -33.6%

Q4’s BEST Performers

- #1 = Payments/FinTech: After gaining +9%, on avg, in Q3, the sector accelerated and was up +40%, on avg, in Q4

- Lemonade was the best performer in the sector, up a significant +122% over Q4

- Robinhood, Affirm, Coinbase, Toast, Block, and Visa also benefitted the sector’s performance, as they all posted double-digits gains in the quarter

- PayPal and Mastercard were also up a modest +9% and +7%, respectively

- #2 = Hardware/Handsets: After rising +12%, on avg, in Q3, the sector nearly tripled its gains and was up +31%, on avg, in Q4

- Peloton was up a significant +86%

- Sonos also saw a double-digit gain of +22%, while Sony and Apple were up a more modest +10% and +8%, respectively

- #3 = Software IT Services: After a modest +5% avg gain in Q4, the sector saw a big ramp up and was up +23%, on avg, in Q4

- Palantir’s +103% gain in the quarter headlined the sector’s performance

- Elastic NV, Datadog, and ServiceNow also drove sector performance and were up double-digits in Q4

- That being said, performance in the sector was slightly weighed down by Oracle (down -2% in Q4), Microsoft (-2%), and IBM (-1%)

Q4’s WORST Performers

- #29 (last place) = China Internet/Tech: The sector saw a significant reversal of fortunes, going from a +20.1% gain in Q3 to a -17.8% loss in Q4

- Most of the names in the sector were down double-digits, with the worst performers being iQIYI (down -30% in Q4), PDD (-28%), Bilibili (-23%), Alibaba (-20%), and Baidu (-20%)

- #28 = European Media: Avg declines in the sector further accelerated from -2.1% in Q3 to -12.4% in Q4

- Both Prosiebensat 1 Media SE and Vivendi SA saw double-digit losses, down -15% and -14%, respectively, while ITV plc was also down -8%

- #27 = Out of Home Advertising: The sector also flipped from positive to negative territory over the quarter, going from +16.6% in Q3 to -12.3% in Q4

- JCDecaux SA was the worst performer in the sector, down -24.6%

- Lamar Advertising and Outfront Media’s performance also weighed on the qtr, down -9% and -4%, respectively

What Stocks Are Wall Street Analysts Most Bullish & Most Bearish On To Start The Year?

As we begin 2025, we also always like to provide an updated look at Wall Street’s research recommendations and price targets across the TMT + Consumer sector to assess where they are more bullish and more bearish at the start of each year. We analyzed data for companies in the industry that have at least 10 analysts covering the stock and a minimum market cap of $1bn.

On average, Buy ratings accounted for 57% of total ratings, Hold ratings accounted for 36%, and Sell ratings accounted for 7%. That is roughly the same distribution as at the beginning of 2023 (56% Buys, 37% Holds, 7% Sells) and is a bit more bullish than the aggregate ratings distribution for companies in the S&P 500 (54% Buys, 40% Holds, 6% Sells).

See below for more details…

MOST Loved Stock (Highest % Buy) = JD.com

- “The Most Loved Stock of 2024” = JD.com with 96% Buy ratings

- Buy ratings increased y/y from 73% Buys in Jan ’24 to 96% Buys in Jan ’25

- China Internet/Tech was the most popular sector in the Top 15: In addition to JD.com, Tencent and Tencent Music Entertainment also made the list, with 95% and 89% Buy ratings, respectively

- Similar to the same time last year, MAANG’s performance was a bit of a mixed bag (only Amazon made the Top 15)

- Amazon made the Top 15 BUT was down the most y/y amongst the MAANG group (-4ppts y/y)

- Which MOST loved stocks from Jan 2024 were also loved in Jan 2025? Microsoft, Magnite, Tencent NVIDIA, Amazon, Uber, and Bowlero

- Bowlero, which was last year’s “Most Loved Stock”, saw the largest drop amongst the group (-9ppts y/y)

LEAST Loved Stock (Lowest % Buy) = Lumen Technologies

- “The Least Loved Stock of 2024” = Lumen Technologies, which was the 2nd year in a row

- Ended both 2023 and 2024 with 0% Buy ratings

-> But note that the stock was one of the best performers of the year (+190%) so the negative rating stance didn’t work out that well for analysts

- Sector representation in the Bottom 15 was extremely diverse, with every company in the list coming from a different sub-sector (no sub-sector was represented more than once)

- Which LEAST loved stocks from January 2024 continued to lack love in January 2025? SiriusXM, Opendoor, Snap, Lumen Technologies, Lemonade, Teladoc, Peloton, and Intel

Which Stocks Had The Biggest CHANGE In Sentiment?

- Robinhood had the biggest POSITIVE swing

- Vivendi had the biggest NEGATIVE swing

How Accurate Was Wall Street in 2024?

- Has Wall Street been right over the last year? Yes… The below table shows the Most Loved and Least Loved stocks as of January 2024 – i.e., this time last year; Looking at 2024 stock price performance, stocks in the Top 10 MOST Loved group were up +32%, on average, and outperformed both the S&P 500 and NASDAQ and stocks in the Top 10 LEAST Loved group were also up +6%, on average, and underperformed the broader indices

- On the long side, the analyst community was most wrong on Pinduoduo (down -33.7% in 2024, 93% Buy ratings)

- On the short side, the analyst community was most wrong on Lumen Technologies (up +190.2% in 2024, 0% Buy ratings) and as noted above, the Street is sticking to their guns with a negative stance

Short Sellers Have A Couple Of New Top TMT Targets To Start The Year…

Finally, amongst the barrage of numbers out this week was short interest data for the period ending Dec 31, which is another gauge of market sentiment that we focus on. In regard to our LionTree Universe of ~180 stocks with $1bn+ market cap across the TMT and Consumer sectors, we looked at where the shorts have been placing their bets to start the year, where they have gotten more bearish, and where they have been covering positions.

In general, the Top 20 most shorted stock list didn’t change much overall, as 18 of the top 20 most shorted stock in Q3 were also in the Top 20 in Q4, and Lemonade remained the most shorted stock for the fifth quarter in a row (but was one of the best stock performers in Q4…see Theme #5).

The was some movement in the Top 3 most shorted as Hims & Hers saw the largest increase in short positions in Q4, while AST SpaceMobile topped the list for largest decrease in short positions.

See the bullets below and table for more detail…

Most Shorted Stocks (As % Of Float) – Lemonade

- The Top 3 Most Shorted – #1 is Lemonade, #2 is Mobileye, #3 is Hims & Hers -> Lemonade was the most shorted stock for the fifth qtr in a row, while Mobileye and Hims & Hers both ascended from the #11 and #20 positions, respectively, from last qtr;

- AST SpaceMobile and Revolve both fell out of the Top 3 from last qtr, but remained within the Top 20

- AST SpaceMobile: #2 in Q3 -> #5 in Q4

- Revolve: #3 in Q3 -> #7 in Q4

- AST SpaceMobile and Revolve both fell out of the Top 3 from last qtr, but remained within the Top 20

- Stocks that dropped out of the Top 20 most shorted: Opendoor Technologies; Redfin

- Stocks that joined the Top 20 most shorted: Fiverr; Reddit

-> Short sellers had a TOUGH Q4… only 9 of the Top 20 most shorted stocks underperformed the S&P 500’s +2.1% during the period and the Top 20 most shorted stocks traded up +23.1% on avg in Q4, significantly outperforming the S&P 500’s +2.1%

Largest Decrease in Short Interest (As % Of Float) – AST SpaceMobile

- The largest decrease in short interest was for AST SpaceMobile: The Co posted a -8.2ppt decrease in Q4 to 23.0%; It went from being the #2 most shorted stock in Q3 to #5 in Q4

- 3 of the Top 10 increases in short interest are companies in the Media Entertainment sector: Cinemark, Spotify, and Outfront Media -> Both Cinemark and Outfront Media underperformed the S&P 500’s +2.1%

Largest Increase in Short Interest (As % Of Float) – Hims & Hers

- The largest increase in short interest was for Hims & Hers: The Co was not only the third most shorted stock at the end of Q4, but it also saw the largest increase in short interest from the end of Q3 (+10.0ppt increase to 31.3%) -> The stock traded up a significant +31.3% in Q4, easily outperforming the S&P 500’s +2.1%

- 4 of the Top 10 increases in short interest are companies in the Consumer Internet sector: Revolve, Wayfair, Chewy, and Opendoor Technologies -> Both Revolve and Chewy outperformed the S&P 500’s +2.1%

US Consumers Splurged During The Holidays But With Some Caveats…

Although there was some trepidation amongst retailers heading into the 2024 holiday season due to a shortened period between Thanksgiving and Christmas, growing consumer debt levels, and surveys that showed that many shoppers were planning to spend the same or less than last year (link), these concerns appeared to be largely unfounded, as a slew of reports published this week out of Salesforce, Mastercard, and Adobe confirmed that shoppers were still willing to spend big during the holidays.

Data from Salesforce indicated that global holiday retail sales surged +3% y/y to a record $1.2tn during the period between Nov 1 and Dec 31, outpacing a forecast that the company released in August that predicted a deceleration in global holiday sales growth to +2% y/y from the +3% y/y increase over the same period last year. Strength in consumer holiday spending was particularly pronounced in the US, where Salesforce found that growth in retail sales accelerated to +4% y/y during the period after being essentially flat in 2023. Similarly, a survey by Mastercard SpendingPulse showed that growth in total US holiday retail sales improved to +3.8% y/y in 2024 (vs +3.1% y/y in 2023), and a report from Adobe Analytics revealed that US online sales increased +8.7% y/y (vs +4.9% y/y in 2023) to $241.4bn, setting a new record for e-commerce sales over the holidays. Notably, social commerce, mobile shopping, as well as AI tools and digital agents were all significant factors in the overall success of this year’s holiday shopping season.

That said, in looking deeper into the numbers, there did appear to be some caveats underneath the surface. For starters, despite the surge in overall spending, consumers “sought value at every turn this year,” with Mastercard noting that e-commerce spending was concentrated during the biggest promotional periods. Many shoppers also took on debt to fund their purchases, assuming +15% more debt, on average, than last year’s holiday season, per a recent LendingTree survey. Lastly, a spike in returns has been another cause for concern amongst retailers, with Salesforce highlighting a +28% y/y rise in global return rates to $122bn. This figure is expected to grow further to $133bn by the time the dust settles. When combined with the precipitous drop in consumer confidence seen in December (link), these data points all seem to suggest that there is still some uncertainty ahead in 2025 for the retail industry.

See below for more details:

- Global holiday retail sales were better than Salesforce predicted (link): Salesforce data showed that global holiday retail sales reached $1.2tn, growing +3% y/y (vs +3% y/y in 2023); Previously, the Co had forecasted a +2% y/y rise, accounting for fewer days between Thanksgiving and Christmas and rising consumer debt levels

- US online sales incr’d +4% y/y to $282bn, while EU online sales grew +1% y/y

- Contributing factors to the better-than-expected results –

- Social commerce has been having a growing impact: Retailers using social commerce strategies saw 20% of global holiday sales generated through platforms like TikTok and Instagram

- Social media also drove +8% y/y more traffic to e-commerce sites: Accounting for 14% of all traffic to e-commerce sites

- Mobile conversion has been improving: The percentage of orders placed grew nearly to nearly 70% (vs 67% in 2023), while the global mobile share of traffic remained the same y/y at 79%

- Social commerce has been having a growing impact: Retailers using social commerce strategies saw 20% of global holiday sales generated through platforms like TikTok and Instagram

- AI tools and digital agents influenced $229bn (19%) of global online sales: This represented a +6% y/y increase and most commonly came in the form of product recommendations, targeted offers, and conversational customer svs support

- Retail use of gen AI features incr’d by +25% during the holiday season vs Sept & Oct 2024

- BUT high returns could weigh on overall profit margins: As shoppers have already sent back $122bn worth of merchandise, a +28% y/y rise, per Salesforce; Trending consumer behaviors such as “try-on hauls” and bracketing (buying an extra size above and below your standard size” have contributed to this

- Salesforce projects that returns will top out at $133bn

-> On a separate but related note, a recent LendingTree survey found that over a third of Americans took on debt to finance gift purchases during the holiday season; Notably, only 44% of those that took on debt had planned to; On avg, consumers assumed $1,181 of debt this holiday season, a +15% y/y rise, w/ 65% of shoppers using credit cards, 24% using store cards, and 21% using BNPL svs to make purchases; 60% of consumers that took on debt said they were stressed doing it (link)

- Total US retail sales saw accelerating y/y growth during the holidays, per Mastercard SpendingPulse (link): Preliminary insights from the Co revealed that US retail sales, excluding autos, rose +3.8% y/y between Nov 1 and Dec 31, 2024 (vs +3.1% y/y in 2023)

- Growth in online sales accel’d: Online sales, including both including e-commerce as well as curbside pick-up and delivery, grew +6.7% y/y during the period (vs +6.3% y/y in 2023), as “consumers increasingly preferred digital-first shopping”

- A handful of US cities led the way in embracing e-commerce: Online sales were up double-digits in Tampa (+10.6% y/y) and Phoenix (+10.0% y/y); Minneapolis (+8.9% y/y), Dallas (+8.4% y/y), Charlotte (+7.9% y/y), Orlando (+7.8% y/y), and Houston (+7.6%) also saw strong digital sales

- In-store sales growth also stepped-up y/y: In-store sales, excluding autos, grew +2.9% y/y over the 2024 holidays (vs +2.2% y/y in 2023)

- Every category saw accel’ing growth besides restaurants –

- Apparel saw a +3.6% y/y increase in sales over the holidays (vs +2.4% y/y in 2023), driven primarily by a +6.7% y/y increase in online sales, while in-store sales were up a modest +0.2% y/y

- Electronics sales incr’d +3.7% y/y (vs -0.4% y/y in 2023)

- Jewelry sales were up +4.0% y/y during the holiday period (vs -2.0% y/y in 2023)

- Restaurant sales rose +6.3% y/y (vs +7.8% y/y in 2023)

- Growth in online sales accel’d: Online sales, including both including e-commerce as well as curbside pick-up and delivery, grew +6.7% y/y during the period (vs +6.3% y/y in 2023), as “consumers increasingly preferred digital-first shopping”

- Adobe Analytics also reported accel’ing growth in online US holiday sales (link): US consumers spent $241.4bn online between Nov 1 and Dec 31, 2024, representing a +8.7% y/y increase (vs +4.9% y/y in 2023) and setting a new record for e-commerce, per Adobe data

- The 2024 holiday season was the most mobile of all time: Smartphones drove the majority of transactions, w/ 54.5% occurring on a mobile device during the period (vs 51.1% in 2023); Mobile shopping accounted for 65% of sales of Christmas day (vs 63% in 2023)

- 1% of ‘Buy Now, Pay Later’ transactions were made through a smartphone: BNPL usage hit an all-time high, increasing +9.6% y/y and contributing $18.2bn in online spend

- 54% of online sales were driven by just three categories –

- Electronics accounted for 23% of online sales: Incr’d +8.8% y/y to $55.3bn

- Apparel accounted for 19% of online sales: Grew +9.9% y/y to $45.6bn

- Furniture/home goods accounted for 12% of online sales: Rose +6.8% y/y to $29.2bn

- Other notable growth categories –

- Grocery online sales jumped +12.9% y/y to $21.5bn (the fastest growing category)

- Cosmetics online sales were up +12.2% y/y to $7.7bn

- Toys online sales incr’d +7.8% y/y to $8.2bn

- Sporting goods online sales grew +7.4% y/y to $7.8bn

- Consumer demand was driven by strong discounts: For every -1% decrease in price, demand incr’d by 1.029% vs the 2023 season, driving an addt’l $2.25bn in online spend

- Traffic to retail sites from gen AI-powered chat bots grew by +1,300% y/y: An Adobe survey of 5,000 US consumers found that 7 in 10 respondents that have used gen AI believe it enhances their experience and that 20% turn to gen AI to find the best deals

- The 2024 holiday season was the most mobile of all time: Smartphones drove the majority of transactions, w/ 54.5% occurring on a mobile device during the period (vs 51.1% in 2023); Mobile shopping accounted for 65% of sales of Christmas day (vs 63% in 2023)

Grab Bag: Flutter Pre-Announced Q4 Results/Netflix’s WWE Debut Was A “Mega Success”/New Streaming Stats

- Flutter pre-reported disappointing Q4 results due to customer-friendly sports outcomes: After facing similar headwinds in Q3, Co cited a period of very unfavorable US sports results across the remainder of Nov and in Dec, primarily on NFL Parlay and Same Game Parlay outcomes

- The 2024-25 NFL season has been the “most customer-friendly since the launch of OSB w/ parlay outcomes”: This resulted in a ~-$438mn negative impact to gross gaming rev (GGR), a ~-$390mn reduction in rev, and a ~-$260mn negative impact to adj EBITDA

- 2024 US rev is now estimated to be ~$5.78bn (-$370mn below the prior $6.05-6.25bn range at the mid-pt)

- 2024 US adj EBITDA is now projected to be ~$505mn (~-$205mn below the prior $670-750mn range at the mid-pt): This also accounts for one-off cost mitigation

- Revised expectations for Q4 include a sportsbook net rev margin of 6.6%: This reflects structural rev margin of 14.5%, which is “broadly in-line w/ expectations” and up +100bps y/y, as well as unfavorable sports results of 390 bps (vs 240 bps of unfavorable results in Q4:23), and promo spend of 4.0% (down -20bps y/y)

- Q4 US rev is now expected to be ~$1.59bn: Given an adverse impact of from unfavorable sports results totaling -$643mn in GGR and -$550mn in rev during the qtr

- Q4 US adj EBITDA is estimated to be ~$161mn: W/ a negative impact of -$360mn in adj EBITDA from customer-friendly sports outcomes

- Outside the US, Flutter cont’d to see “good momentum” in the UK & Ireland: Favorable sports results in the English Premier League led to the Co estimating rev and adj EBITDA will be ~+1% and ~+2% higher than the guide the Co provided on the Q3 call (ex-US)

- The 2024-25 NFL season has been the “most customer-friendly since the launch of OSB w/ parlay outcomes”: This resulted in a ~-$438mn negative impact to gross gaming rev (GGR), a ~-$390mn reduction in rev, and a ~-$260mn negative impact to adj EBITDA

-> Flutter shares actually rose +1.6% in reaction to the annc’ment but ended the week down -1.1%; DraftKings shares also rose +2.6% following the news and closed the week up +5.4%; Since the start of 2024, Flutter stock is trading up +41.9%, and DraftKings stock is up +12.0%

- Netflix’s debut of WWE “felt massive” and like a “big-budget movie premiere,” per The Athletic (link): Writers from The Athletic dubbed the event a “mega success” due to the “reams of attention of from social media and conventional press that both Netflix and the WWE received

- The show was “stunning” as a pure-production play: There was an “inordinate amount of celebrity overkill,” w/ Travis Scott and Dwayne “the Rock” Johnson making appearances, and “an absurd amount of Netflix promotion,” though this was designed to appeal to a “much wider audience”

- BUT this may not necessarily be the case moving forward: As future WWE events will be held in smaller venues than the Intuit Dome on a weekly basis

- “Netflix is on the path to being a player for upcoming live sports rights”: The Athletic believes that Netflix’s WWE debut “will change the landscape of sports consumption and cause consternation for the traditional linear powers, given [the Co’s] financial might”

- The event could lay a blueprint for UFC as well: While the most prominent UFC events are typically pay-per-view, this could lay the groundwork for future events and result in a “boost in popularity” for mixed martial arts as a sport; Boxing could also benefit from this model

- The show was “stunning” as a pure-production play: There was an “inordinate amount of celebrity overkill,” w/ Travis Scott and Dwayne “the Rock” Johnson making appearances, and “an absurd amount of Netflix promotion,” though this was designed to appeal to a “much wider audience”

- Some notable streaming stats were also released this week –

- Disney has an estimated 157mn global MAUs watching ad-supported content across Disney+, Hulu and ESPN+ (link): This includes 112mn domestic users and is an avg per month over the last six months

- Disney is seeking to define a methodology for counting ad-supported users –

- The metric is derived from active accounts across Disney’s three streaming svs that have viewed ad-supported shows and movies continuously for 10+ seconds

- Each active account is then multiplied by the number of estimated users per account to estimate the total number of users

- The estimated active users are added across the apps without de-duplication, meaning users who subscribe to more than one of the platforms could be counted more than once

- Disney hasn’t historically provided metrics on its ad-supported users: Though back in Nov, the Co indicated that more than half of its new US Disney+ subscribers were choosing the cheaper, ad-supported option

- Disney is seeking to define a methodology for counting ad-supported users –

- Users watched 10bn hours of content on Fox’s Tubi svs in 2024 (link): This represents a +18% y/y increase over the 8.5bn of hours watched on the FAST svs in 2023, per a third-party analysis

- Addt’l metrics –

- 95% of viewing time on Tubi has been for on-demand movies and TV shows

- 34%+ of viewers are aged 18-34, w/ nearly half being multicultural and nearly 80% being those without cable

- Tubi’s MAUs rose +24% y/y to 97mn in 2024, per the Co

- Tubi claims to have “the largest collection of premium-on-demand content, w/ 275,000+ movies and TV episodes as well as 300+ exclusive originals

- Addt’l metrics –

- Roku has surpassed 90mn+ streaming households in the first week of 2025 alone: The Co also highlighted that it is in nearly half of all US broadband households

- The Co ended FY24 w/ 89.8mn streaming households: Roku ended Q3 w/ 85.5mn streaming households but also plans to stop reporting qtrly streaming households data beginning in Q1:25

- Disney has an estimated 157mn global MAUs watching ad-supported content across Disney+, Hulu and ESPN+ (link): This includes 112mn domestic users and is an avg per month over the last six months

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Clear Channel Outdoor (CCO) annc’d it will sell its Europe-North segment to Bauer Radio Limited, a subsidiary of Bauer Media Group, for $625 mn. The all-cash deal, expected to close in Q2 2025, will help CCO focus on its America and Airports segments. The sale aligns w/ CCO’s strategy to optimize its portfolio and reduce leverage. The proceeds will be used to prepay $375 mn in term loans and for other debt-related purposes. (Yahoo Finance)

Artificial Intelligence/Machine Learning

- Apple Intelligence, currently available on iPhones, iPads, and Macs, is not yet on Apple TV or Apple Watch. Google’s Gemini AI, announced at CES 2025, is coming to Google TV and Wear OS. Apple Intelligence features, like Writing Tools and ChatGPT integration, are being rolled out in phases. The third phase, expected by spring, will enhance Siri’s capabilities. However, these features may not be immediately useful for Apple TV and Apple Watch (9to5Mac)

- Microsoft has rolled back its Bing Image Creator model after users complained about degraded image quality. The new model, PR16, was supposed to deliver images twice as fast and with higher quality but failed to meet expectations. Users reported that images looked cartoonish and lifeless. Microsoft will revert to the previous model, PR13, until the issues are resolved. The rollback process, which began over a week ago, will take 2-3 more weeks to complete (TechCrunch)

- AI startup funding hit a record $97 bn in 2024, driven by megarounds from OpenAI and xAI. OpenAI raised $6.6 bn, while xAI secured $5.5 bn. The surge in investment reflects growing confidence in AI tech and its potential to transform various industries. Despite economic uncertainties, investors are betting on AI’s long-term impact. The funding boom highlights the increasing importance of AI in the global tech landscape. (Bloomberg)

- Google is set to bring its Gemini AI to TV sets running its software, as annc’d at CES 2025. This integration aims to enhance user experience w/ advanced AI capabilities, offering personalized content recommendations and improved voice recognition. The move reflects Google’s strategy to expand its AI ecosystem and provide seamless tech across devices. The Gemini AI will be available on select TV models later this yr, marking a significant step in smart home tech. (Bloomberg)

Audio/Music/Podcast

- Spotify has reached 55 mn US subscribers, impacting podcasters, authors, and musicians. This milestone, annc’d on Jan. 9, 2025 (Thursday), highlights Spotify’s dominance in the audio streaming mkts. The platform’s growth offers creators more opportunities for rev and audience engagement. Spotify’s investment in exclusive content and tech innovations continues to attract diverse creators, enhancing the overall user experience (Bloomberg)

- Google has introduced “Daily Listen” to its Discover feed, offering personalized audio content. This feature, announced on Tuesday (Jan. 7, 2025), curates news, podcasts, and other audio based on user preferences. It aims to enhance the Discover experience by providing a hands-free way to stay informed. Daily Listen is rolling out gradually and will be available to all users by the end of the month. (9to5Google)

Broadcast/Cable Networks

- Comcast and Paramount Global struck a new multi-year carriage deal on Monday (Jan. 7, 2025). This agreement ensures that Paramount-backed networks like CBS, BET, Comedy Central, MTV, Nickelodeon, and Paramount Network remain on Comcast’s cable systems. Comcast subscribers will also retain access to Paramount+, Pluto TV, and BET+. Additionally, Comcast can offer Paramount+ w/ Showtime to qualifying Xfinity customers. Financial terms were not disclosed (Variety)

Cable/Pay-TV/Wireless

- Free Mobile has confirmed its pledge not to increase prices until 2027 and has achieved 95% 5G coverage in France. The Co aims to maintain affordable svs while expanding its network. This commitment aligns w/ Free Mobile’s strategy to provide competitive pricing and extensive coverage. The Co’s focus on customer satisfaction and network investment supports its goal of becoming a leading telecom provider in the French mkts. (Telecompaper)

- Nexfibre’s network has reached 2 mn premises across the UK, marking a significant milestone in its expansion efforts. The Co aims to provide high-speed broadband svs to underserved areas, enhancing connectivity and digital inclusion. This achievement supports Nexfibre’s goal of becoming a leading broadband provider in the UK mkts. The Co plans to continue its network rollout, targeting 5 mn premises by 2027, aligning w/ its long-term strategy for growth and customer satisfaction.

- (Telecompaper)

- The German telecom market is forecasted to grow by 18% in 2025, driven by increased demand for high-speed internet and 5G svs. The growth is attributed to significant investments in network infrastructure and the expansion of digital svs. Telecom cos are focusing on enhancing customer experience and expanding their 5G coverage. This positive outlook reflects the ongoing digital transformation and the rising importance of connectivity in the German mkts.

- (Telecompaper)

- Nokia and stc Group achieved a record-breaking 1Tbps data center connectivity in the MEA region. Utilizing stc Group’s live DWDM terrestrial network, the trial showcased Nokia’s PSE-6s tech, enabling high-capacity, efficient, and scalable connectivity. The trial transported 6 x 100GE and 1 x 400GE high-speed svs over 1Tbps single wavelength across 850km. This milestone supports Saudi Vision 2030’s digital transformation goals and positions the kingdom as a leader in digital innovation and sustainability.

- (The Fast Mode)

- The planned merger between Hulu + Live TV and Fubo, announced on Monday (Jan. 7, 2025), will not immediately affect subscribers. Both services will continue independently, with no changes to pricing or channel lineups. The merger aims to create a stronger platform to compete with YouTube TV and Sling TV. Disney, the majority owner, is investing $365 mn in cash and loans to support Fubo. The combined company will operate under the Fubo brand (Cord Cutter News)

- Openreach’s broadband network traffic surged by 105% in 2024, driven by increased demand for high-speed internet svs. The rise reflects the growing reliance on digital platforms for work, education, and entertainment. Openreach’s continued investment in fiber infrastructure has enabled this growth, ensuring robust connectivity across the UK. The company aims to further expand its network to meet the escalating needs of consumers and businesses. (Telecompaper)

- SKT has annc’d it will launch its AI agent beta svs in North America by Mar. The AI agent, designed to enhance user experience through advanced tech, will initially be available to select users for testing and feedback. This move is part of SKT’s strategy to expand its AI capabilities and market presence globally. The beta launch aims to gather insights and refine the svs before a wider rollout. (Telecompaper)

Capital Market Updates

- Global venture funding in 2024 reached ~$314 bn, a 3% increase from 2023’s $304 bn. AI was the standout sector, attracting over $100 bn, an 80% rise from 2023. Nearly a third of all global venture funding went to AI-related fields. The fourth quarter saw a significant push, with $93 bn raised, marking the highest quarterly total since Q3 2022. Notable billion-dollar rounds included Databricks, OpenAI, and xAI. Despite economic uncertainties, late-stage funding surged, while early-stage and seed funding remained flat (Crunchbase)

Cloud/DataCenters/IT Infrastructure

- Quantum computing stocks, including IonQ, dropped significantly on Wednesday (Jan. 8, 2025) after Nvidia CEO Jensen Huang stated that practical applications of quantum computing are still years away. Huang emphasized that while quantum tech holds promise, it is not yet ready for mainstream use. This cautious outlook led to a market reaction, reflecting investor concerns about the immediate viability of quantum computing investments (Bloomberg)

- Micron Technology plans to invest $7 bn in a new memory chip plant in Singapore, announced on Monday (Jan. 8, 2025). This facility will enhance Micron’s production capacity and support the growing demand for memory chips in AI and data centers. The plant is expected to create thousands of jobs and strengthen Micron’s position in the global semiconductor market. Construction will begin later this year, with operations slated to start by 2028 (Bloomberg)

- Microsoft has annc’d a $3 bn investment in cloud and AI infrastructure in India. This initiative aims to enhance its data center capacity and support the growing demand for cloud svs in the region. The investment will also focus on advancing AI capabilities, fostering innovation, and supporting local businesses. Microsoft’s commitment underscores the strategic importance of India in its global tech strategy. (Telecompaper)

- Emirati billionaire and Former President Trump has annc’d a $20 bn investment in US data centers. This initiative aims to enhance the nation’s tech infrastructure, creating jobs and boosting the economy. The investment will focus on building new data centers and upgrading existing ones, ensuring robust and secure data storage capabilities. This move is part of a broader strategy to strengthen the US’s position in the global tech mkt. (Reuters)

Crypto/Blockchain/web3/NFTs

- SEC Chair Gary Gensler reflected on his tenure and the SEC’s crypto enforcement efforts ahead of his departure on Jan. 20, 2025 (Monday). He emphasized the SEC’s success in addressing misconduct in the digital asset sector, noting over 100 crypto-related enforcement actions during his term. Gensler described the crypto industry as “rife with bad actors” and stressed the need for continued regulation. His successor, Paul Atkins, is expected to adopt a more lenient approach.

- (Yahoo Finance)

- The article reveals that ~68% of crypto advice on TikTok is misleading, w/ many influencers prioritizing personal gain over audience welfare. Analysis of 1,000+ videos found 61% lacked disclaimers, and 58% promoted specific coins w/o context. Popular coins included Bitcoin (BTC), XRP, and Ethereum (ETH). ~35% of videos promised unrealistic returns, targeting novices. Only 0.3% of influencers had relevant qualifications. The report urges responsible content creation and consumption to prevent financial losses. (news)

Cybersecurity/Security

- Japan’s National Police Agency (NPA) linked over 200 cyberattacks from 2019 to 2024 to Chinese hacker group MirrorFace. These attacks targeted Japan’s national security and tech data, including the Foreign and Defense ministries, JAXA, and private cos. MirrorFace used malware-laden emails w/ subjects like “Japan-U.S. alliance” and “Taiwan Strait.” The NPA urges enhanced cybersecurity measures as attacks continue (AP News)

- 2024 was the worst yr on record for commercial cyberattacks, w/ UK businesses encountering ~753,341 malicious attempts each to breach their online and IT systems. This attack level was 4% higher than in 2023, making last yr the worst ever for attempted cyberattacks. The attack rate peaked at 2,192 per day in Q3 2024 before declining to 2,063 per day in Q4. (Total Telecom)

eCommerce/Social Commerce/Retail

- Wayfair annc’d on Jan. 10, 2025 (Friday) that it will lay off 730 employees as it exits the German market to focus on core biz investments. This restructuring will result in charges of ~$102mn to $111mn, including employee-related costs and non-cash charges for facility closures. Shares of the U.S.-based Co rose ~4% in premarket trading. The decision comes amid slower traffic and weaker demand from cost-conscious consumers, impacting Wayfair’s overall performance (Reuters)

- Nordstrom has partnered w/ SkinSpirit to offer Botox and filler treatments at its New York flagship. Starting in Feb., SkinSpirit will operate a shop-in-shop in Nordstrom’s Beauty Haven, providing facials, chemical peels, microneedling, and injectables. This collaboration aims to enhance customer experience by offering unique svs. SkinSpirit, recognized as a top provider of medical aesthetics, will expand to Nordstrom’s Chicago store later this yr (WWD)

- Target annc’d on Jan. 9, 2025 (Thursday) the launch of 2,000 new wellness products, w/ over 50% priced under $10. The assortment includes 600 Target-exclusive items across beauty, personal care, tech, food, and beverages. Notable products feature functional beverages, hair health, and wellness tech. Celebrity-backed brands like Kourtney Kardashian Barker’s Lemme and Ashley Tisdale’s Being Frenshe are included. This expansion aims to offer affordable wellness options for all customers (WWD)

Electric & Autonomous Vehicles

- The National Highway Traffic Safety Administration (NHTSA) has opened a probe into Tesla’s “Actually Smart Summon” feature, impacting 2. 6 mn vehicles. Annc’d on Jan. 9, 2025 (Thursday), the investigation focuses on safety concerns related to the feature, which allows drivers to summon their cars via a mobile app. Multiple crash allegations have been reported, highlighting risks associated w/ Elon Musk’s plans to roll out unsupervised Full Self-Driving this yr (Fortune)

- Germany’s EV sales have crashed as buyers abandon electric cars in droves. The decline is attributed to reduced subsidies and increased competition from cheaper Chinese models. Tesla and Volkswagen are among the hardest hit, facing significant drops in sales. The shift highlights challenges in the EV mkt, w/ consumers seeking more affordable options. The German govt is considering new incentives to revive the sector and support domestic manufacturers. (Fortune)

- Uber annc’d a partnership w/ Nvidia to accelerate autonomous driving tech. Uber will use Nvidia’s Cosmos simulation tool and DGX Cloud AI platform to develop self-driving vehicles. Cosmos generates realistic driving environments, while DGX Cloud provides high-performance AI infrastructure. This collaboration aims to enhance Uber’s autonomous vehicle capabilities and expand its market presence. (TechCrunch)

Film/Studio/Content/IP/Talent

- Due to ongoing wildfires in Los Angeles, several TV series have paused production. Universal Studio Group’s Hacks, Happy’s Place, Loot, Suits LA, and Ted will not film on Wednesday (Jan. 8, 2025) as NBCUniversal closed the lower lot at Universal Studios and the theme park. Events like the premiere of The Pitt and a press event for Shifting Gears were also canceled. Prime Video’s Fallout delayed its production restart in Santa Clarita by a few days for safety (Deadline)

Handheld Devices & Accessories/Connected Home

- Google announced on Monday (Jan. 8, 2025) that its Home hubs, Chromecasts, Google TV devices on Android 14, and some LG TVs can now control Matter devices locally. This integration, enabled by Home Runtime, allows for more reliable and responsive smart home setups. Matter, a universal standard for smart home devices, ensures compatibility across different brands. This update aims to simplify and enhance the user experience by reducing reliance on cloud services (The Verge)

Investor & Market Sentiment

- Venture capital (VC) funding in Saudi Arabia and the UAE has significantly declined, according to a report by Magnitt. The report highlights a 40% drop in VC investments in 2024 compared to the previous year. This decline is attributed to global economic uncertainties and a cautious approach by investors. Despite the slump, both countries remain committed to fostering innovation and supporting startups, with various government initiatives aimed at revitalizing the VC landscape (Bloomberg)

Last Mile Transportation/Delivery

- NYC’s new congestion pricing, effective Jan. 8, 2025 (Wednesday), impacts Uber, Lyft, and taxi fares. Taxis, green cabs, and black cars now have a $0.75 surcharge per trip, while Uber and Lyft rides incur a $1.50 fee for trips starting, ending, or passing through Manhattan’s Congestion Relief Zone (CRZ). This toll aims to reduce gridlock, encourage public transit, and fund ~$15bn in transit infrastructure improvements (Fox5 Network)

- Delta Air Lines will link its SkyMiles loyalty program to Uber, ending its eight-year partnership w/ Lyft. Starting this spring, SkyMiles members can earn miles for Uber rides: one mile per dollar on UberX airport rides, two miles per dollar on premium rides like Uber Comfort and Uber Black, and three miles per dollar on Uber Reserve trips. For Uber Eats, members will earn one mile per dollar on orders over $40. (CNBC)

Macro Updates

- US companies added 122,000 jobs in Dec. 2024, according to ADP data. This growth was driven by the leisure and hospitality sectors, which saw significant hiring increases. The rev in job creation reflects a steady recovery in the labor mkts, despite economic uncertainties. ADP’s report also highlighted strong gains in small and medium-sized businesses. The data suggests a positive outlook for the US job mkts as the economy continues to rebound. (Bloomberg)

- VC investments in emerging mkts, such as MENA, plummeted by over 40% compared to 2023. The total raised across surveyed mkts was $9.1 bn in 2024, a 41% YoY decline. Deal activity also dropped by 20%, w/ the number of deals falling to 1,5271. However, there are signs of recovery as global interest rates decline1. Fintech remains strong, attracting $3.9 bn in funding. The report suggests that 2024 might be the bottom of the funding downturn curve. (TechCrunch)

- The US job market showed resilience in Dec. 2024, w/ job openings rising to 8.1 mn, surpassing expectations. The ISM svs index indicated continued expansion, though at a slower pace. The S&P 500 and 10-year Treasury yield reacted to these mixed signals, reflecting investor uncertainty. Despite the increase in job openings, hiring eased, suggesting businesses remain cautious amid economic uncertainties. (Investor’s Business Daily)

- US job openings reached to a six-month high, driven by biz svs. The increase reflects a strong labor mkt, w/ employers adding ~300,000 jobs in Dec. The unemployment rate remained steady at 3.5%. The tech sector saw significant growth, contributing to the overall rise in job openings. Despite economic uncertainties, the labor mkt continues to show resilience, w/ employers actively seeking workers to meet demand. (Bloomberg)

Media Conglomerates

- NBC and Nexstar Media have renewed their TV affiliate agreement, covering 33 mkts in the US. The multi-year pact includes 29 stations owned by Nexstar, 3 by Mission Broadcasting, and 1 by White Knight Broadcasting, reaching over 14 mn US TV households. This renewal ensures the continued broadcast of popular NBC shows like “Law & Order” and “Chicago” franchises. The deal highlights the ongoing importance of traditional TV networks in the evolving media landscape.

- (Variety)

- The Golden Globes 2025, hosted by Nikki Glaser, drew 9. 3 mn viewers on CBS, down 2% from last yr, per Nielsen. Paramount initially reported 10.1 mn viewers using VideoAmp data, marking a 7% increase. The discrepancy arises from a contract dispute between Paramount and Nielsen. The show achieved a 1.8 rating among adults 18-49, consistent w/ 2024. The event, held on Jan. 5, 2025 (Sunday), benefitted from an NFL lead-in but competed w/ NBC’s Vikings-Lions game.

- (Variety)

- Sony Group annc’d at CES on Monday (Jan. 6, 2025) its deepened investments in anime, forecasting the sector to become a $60 bn biz by 2030. Sony’s Crunchyroll grew from 3 mn subscribers in 2020 to over 15 mn by last July. The Co will release Demon Slayer: Kimetsu no Yaiba Infinity Castle later this yr, aiming to surpass the $473 mn earned by the previous film. Sony’s bullishness on anime is driven by the global surge in interest in Japanese pop culture (The Hollywood Reporter)

- Getty Images and Shutterstock have agreed to merge, forming a $3. 7 bn stock photo giant. Getty Images shareholders will own ~54.7% of the new entity, while Shutterstock shareholders will own 45.3%. The combined co will be called Getty Images. This merger aims to strengthen their financial foundation, enhance content offerings, and invest in new tech. Shutterstock shareholders can choose cash, Getty shares, or a mix of both. (TechCrunch)

- Fubo has settled its lawsuit w/ Disney, FOX, and Warner Bros. Discovery, allowing Venu Sports to launch. The settlement, part of the Fubo-Hulu + Live TV merger, includes a $220 mn payment to Fubo. The lawsuit had alleged anti-competitive practices, arguing that Venu Sports would limit consumer choice. The resolution ends a heated legal battle and positions Fubo for growth in the streaming mkt. (Cord Cutters News)

- As cord-cutting grows, more Americans are expected to listen to the radio than watch traditional TV in 2025. The shift is driven by the increasing popularity of streaming svs and on-demand content, which offer more flexibility and variety. Traditional TV viewership has been declining, while radio remains a popular medium for news, music, and talk shows. This trend highlights the changing landscape of media consumption and the growing preference for digital platforms. (Cord Cutters News)

Regulatory

- Elon Musk’s lawyer has urged California and Delaware attorneys-general to compel OpenAI to auction a large stake in its biz, escalating tensions w/ CEO Sam Altman. In a letter dated Jan. 9, 2025 (Thursday), Musk’s attorney, Marc Toberoff, represented AI investors seeking an open bidding process. OpenAI, initially a non-profit, restructured as a for-profit to raise capital, including $13bn from Microsoft. OpenAI aims to become a public benefit corporation, balancing profit w/ societal good. (Financial Times)

- In a landmark ruling on Wednesday (Jan. 8, 2025), the EU General Court fined the European Commission for breaching its own data protection laws. The court found that the Commission transferred a German citizen’s personal data to the U.S. without proper safeguards, violating GDPR. The citizen had used “Sign in w/ Facebook” on the EU login page. The Commission was ordered to pay 400 euros ($412) in damages. This ruling underscores the importance of compliance w/ data protection regulations (Reuters)

Satellite/Space

- Telstra has partnered w/ SpaceX to trial satellite-to-mobile texting svs in remote areas of Australia. This initiative aims to enhance connectivity in regions lacking traditional mobile coverage. The trial will utilize SpaceX’s Starlink satellites to provide reliable texting svs, supporting emergency communications and everyday use. This collaboration aligns w/ Telstra’s strategy to expand its network reach and improve svs for customers in underserved areas.

- (Telecompaper)

- United Airlines has annc’d it will begin testing SpaceX’s Starlink satellite internet svs on flights as early as Feb. , w/ plans to equip its entire fleet by yr-end. This move aims to revolutionize in-flight connectivity, offering passengers seamless online access at 35,000 feet. United will provide Starlink internet for free to all MileagePlus members, enhancing the passenger experience and opening up new partnership opportunities. (Cord Cutters News)

Social/Digital Media

- Project Liberty has renewed its bid for TikTok’s US assets ahead of a Supreme Court hearing. The bid aims to address national security concerns and ensure TikTok’s compliance w/ US regulations. The Supreme Court hearing, scheduled for Jan. 15, 2025 (Wednesday), will determine the future of TikTok’s operations in the US. Project Liberty’s proposal includes a comprehensive plan to safeguard user data and enhance transparency, aligning w/ the US government’s objectives.

- (Telecompaper)

- Bluesky, a social media platform rivaling Elon Musk’s X, is nearing a $700 mn valuation in a new funding round led by Bain Capital Ventures. The platform’s user base surged from 3 mn to 25.9 mn in 2024, driven by users migrating from X after Donald Trump’s presidential victory. Bluesky plans to introduce a payment platform and subscription svs to find a profitable model. The Co aims to position itself as a safer, more idealistic alternative to X (Business Insider)

- Mark Zuckerberg’s decision to ditch factcheckers on Facebook and “prioritise free speech” weeks before Donald Trump returns to power was condemned as a “major step back” for public discourse. Mark annc’d multiple changes to his platforms including Facebook and Instagram in an attempt to “dramatically reduce the amount of censorship”. He said that, starting in the US, independent factcheckers would be replaced in the US by a system of “community notes” similar to that used on X. (The Guardian)

- X has hired John Stoll, a former editor and Detroit bureau chief at The Wall Street Journal, to lead its news group and partnership team. This strategic move aims to enhance the platform’s news offerings on a global scale. X Corp. CEO Linda Yaccarino emphasized the Co’s vision to make X a home for the future of news and journalism. The announcement was made during X Corp.’s keynote at CES 2025 in Las Vegas. (TechCrunch)

- Former President Trump praised Meta, stating it has “come a long way” after CEO Mark Zuckerberg ended fact-checking on its platforms. This decision is seen as a significant shift in Meta’s approach to content moderation, potentially impacting how information is shared and consumed on Facebook and Instagram. The move has sparked discussions on free speech and the role of tech companies in regulating content. (FOX News)

- Reddit has introduced new trends tools for businesses and an AMA ad format. The trends tools will help businesses identify and leverage popular topics on the platform, enhancing their marketing strategies. The AMA ad format allows companies to host sponsored “Ask Me Anything” sessions, engaging directly with the Reddit community. These features aim to provide businesses with more effective ways to connect with users and promote their products or svs. (TechCrunch)

- Meta will test showing eBay listings on Facebook Marketplace in Germany, France, and the US. Buyers can browse eBay listings on Marketplace and complete transactions on eBay. This test follows a $840 mn fine by the European Commission over Facebook Marketplace practices. Meta aims to address the Commission’s concerns while giving eBay sellers exposure to Facebook’s audience and expanding Marketplace’s offerings. (Yahoo Finance)

Software

- Chip designer Arm is considering acquiring Ampere Computing, a server chip company backed by Oracle. Ampere, valued at $8 bn in 2021, designs chips for cloud providers like Microsoft and Google. The potential acquisition comes as Ampere faces increased competition and shifts in the semiconductor market. Ampere had previously filed for an IPO in 2022 but is now exploring a sale. The acquisition would strengthen Arm’s position in the AI-driven semiconductor sector (Bloomberg)

Sports/Sports Betting

- The NFL has moved the Rams’ playoff game against the Vikings from SoFi Stadium to State Farm Stadium in Arizona due to the ongoing wildfires in Los Angeles. The decision, made on Jan. 9, 2025 (Thursday), prioritizes public safety. The game will still be played on Monday night at 8 p.m. ET. The wildfires have significantly impacted the LA area, and the NFL, in consultation w/ public officials, deemed it unsafe to hold the game in Southern California (Front Office Sports)

- The NHL annc’d plans to host two outdoor games in Florida in 2026. The first game will feature the Florida Panthers hosting the New York Rangers at LoanDepot Park on Jan. 2, 2026 (Friday). The second game will see the Tampa Bay Lightning face the Boston Bruins at Raymond James Stadium on Feb. 2, 2026 (Monday). These events aim to attract ~100,000 fans and highlight Florida’s growing hockey culture. The NHL will use innovative tech to maintain ice quality in the warm climate.

- (CNBC)

- The FCS Championship between North Dakota State and Montana State on Jan. 8, 2025 (Monday) drew 2.4 mn viewers on ESPN, making it the second most-watched FCS title game ever. This viewership was up 132% from the previous yr’s game, which faced NFL competition. The peak audience reached 3.1 mn viewers. The move to Monday night proved beneficial, surpassing the 2020 title game viewership of 2.69 mn. The FCS semifinals also saw impressive numbers, averaging 1.48 mn viewers.

- (Awful Announcing)

- The Pohlad family is open to selling the Minnesota Twins, but the process is expected to be gradual, similar to the sale of the Minnesota Timberwolves. The Twins are unlikely to have new owners before Opening Day, and the sale might not be completed by the end of the season. The Pohlads aim to avoid financial instability during the transition, maintaining a payroll around $127 mn for 2025. (The Athletic)

- The debut of WWE on Netflix felt massive, drawing significant viewership and engagement. The event showcased WWE’s ability to adapt to streaming platforms, offering a mix of live and on-demand content. Netflix’s investment in WWE highlights its strategy to diversify content and attract a broader audience. The collaboration is expected to bring more wrestling events to the platform, enhancing its sports entertainment offerings. (The Athletic)

Tech Hardware