Where do I start?! It was a historic week, and the rally that the Trump election sparked was the main event in the markets, with the onslaught of sector earnings in the background. The S&P 500 and Nasdaq rose +4.7% and +5.7%, respectively, reaching fresh all-time highs, while the small cap Russell 2000 rallied +8.6%. On the flipside, treasuries pulled back on the short end.

Elsewhere on the macro side, as expected, the Fed cut rates by -25bps, and the market is currently pricing in a 30% chance of a pause in December.

What does the new administration potentially mean to the TMT sector?? We offer some perspectives in Theme #2 this week! The rest of our focus is related to the extremely heavy earning cycle, where interesting updates were coming out left and right.

Separately, I wanted to highlight that LionTree acted as a bookrunner on Informatica’s secondary share offering announced this week. This follows serving as a bookrunner on the Co’s IPO in October of 2021.

Also, LionTree served as exclusive financial advisor to the Special Committee of FIGS‘ board of directors in its investment in OOG, an AI-powered peer-to-peer online learning and social platform for healthcare professionals.

Enjoy the weekend and the read – It is another intense edition!

- Earnings Scorecard – Week 4

- It Was A Historic Week With Lots Of Potential Reverberations Across The Sector

- Visibility On Take-Two’s Multi-Year Growth Trajectory Is Improving

- 10 Significant “Landscape Changes” Are Driving The Trade Desk’s Business

- Fox Continues To Pull Away From The Pack… It’s Been Good To Be In Sports & News

- WBD & PARA: The Streaming Transition Has Its Ups & Down

- DraftKings: “Hot” Customer Acquisition Trends Outweighed Setbacks From “Customer-Friendly” Sport Outcomes

- TKO Gets Through The Toughest Quarter Of The Year…

- Airbnb & Expedia: Questions Emerge Regarding More Competition In Alternative Accommodations

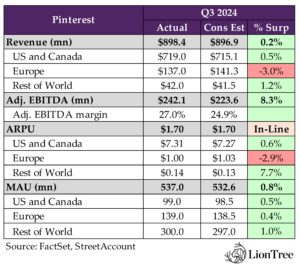

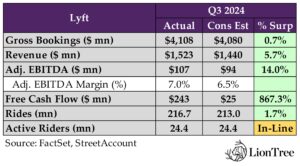

- Other Key Earnings Follow-Ups: Digital Advertising (Pinterest) & Last-Mile Transport (Lyft)

Best,

Leslie

Earnings Scorecard – Week 4

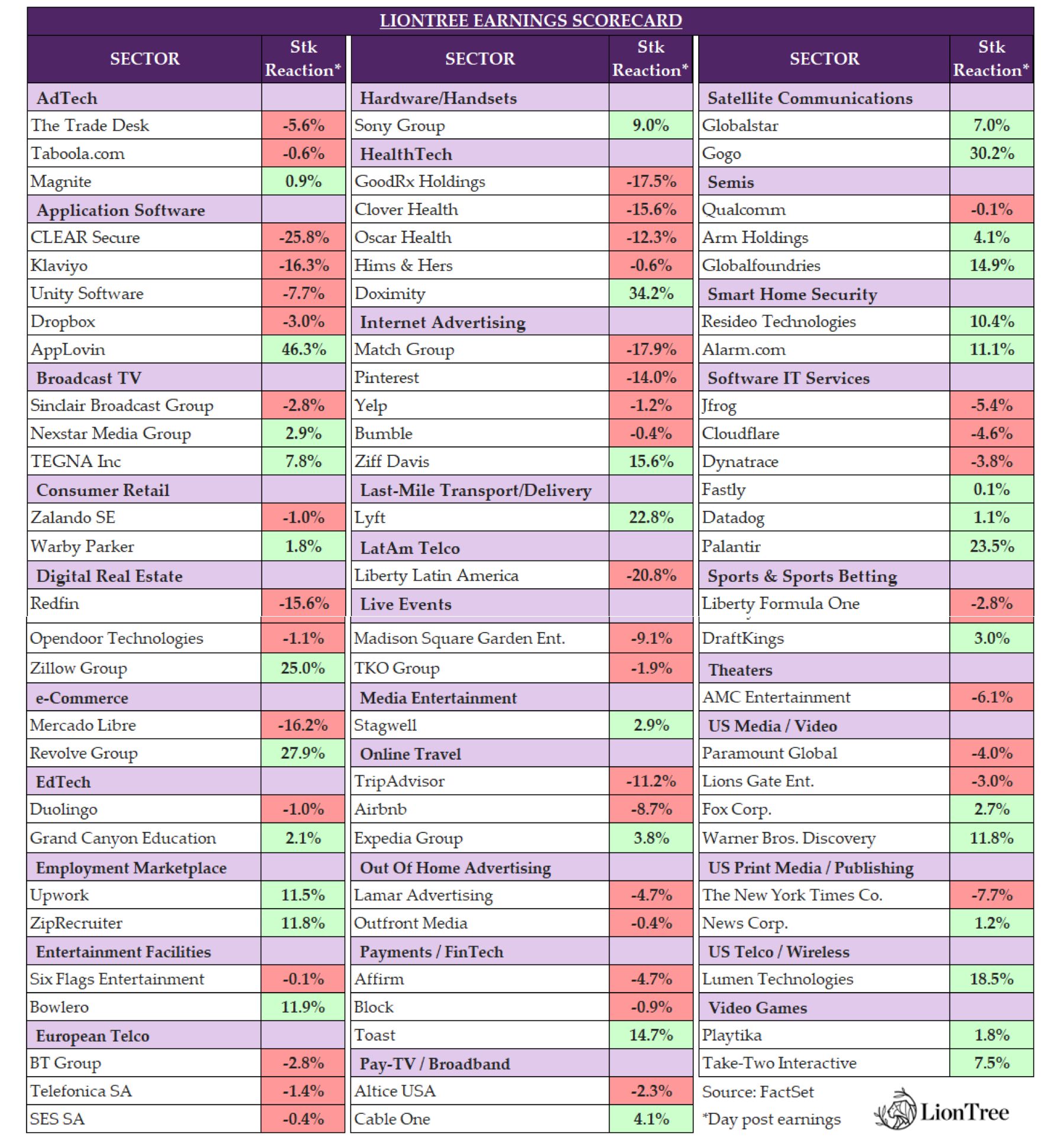

We reached peak activity in the TMT earnings circuit this week, with a record 98 companies in our LionTree TMT Universe reporting their third quarter results (more than double the 46 companies that reported last week). Similar to the last two weeks, stock price reactions were biased to the downside, as 53 companies (55.2%) traded down post their results, while 45 companies (44.8%) traded up. CLEAR Secure was the worst performer, falling -25.8% in reaction to its report, while AppLovin was the best performer, soaring +46.3%.

Companies across sub-sectors were on the docket this week. Starting with the legacy media companies, Fox’s earnings report kicked off on a good note, with the stock trading up +2.7% during the day (see Theme #5). Warner Bros Discovery and Paramount followed suit later in the week, though stock reactions diverged between the two, with WBD trading up +11.8% and Paramount trading down -4.0% (see Theme #6).

In interactive entertainment, after EA and Roblox’s prints last week that were received positively by the markets, Take-Two also saw green in reaction to its report this week, trading up +7.5% (see Theme #3). Several of the online travel reports continued into this week after Booking’s report last week, though reactions were mixed, with Airbnb trading down -8.7%, and Expedia trading up +3.8% (see Theme #9).

In the live entertainment space, TKO reported, but the stock fell -1.9% in reaction to its print (see Theme #8). Over in sports betting, DraftKings also saw a positive reaction and was up +1.9% (see Theme #7). And in AdTech, The Trade Desk received a tough reaction from the Street, closing down -5.6% (see Theme #4).

Finally, we also took a quick look at Pinterest, which fell -14.0%, as well as Lyft, which jumped +22.8%, post their respective reports (see Theme #10).

The table below includes select TMT and consumer companies in our LionTree stock universe with $1bn+ market caps that reported this week.

It Was A Historic Week With Lots Of Potential Reverberations Across The Sector

The historic re-election of President Donald Trump this week sent ripples, and in some cases tidal waves, across many sectors far and wide, as investors assessed implications and tried to determine potential winners and losers. Close to where we live, Jeff Bezos, Sam Altman, Tim Cook and other tech leaders were quick to congratulate Trump on the heels of his election win, given that the Tech Sector is one that has been in Trump’s scope in various forms and fashions. Big picture, there is optimism about a more business-friendly administration and what this could mean for taxes, deregulation, and consolidation (among other things). However, there is also concern about potential challenges related to trade policies and immigration.

See below for some more detailed thoughts and perspectives (link /link/link/link/link/link).

- Trump’s administration is likely to favor deregulation, which could lead to incr’d M&A across the sector

- WBD CEO David Zaslav on the Co’s earnings call…“It’s too early to tell, but it may offer a pace of change and an opportunity for consolidation that may be quite different, that would provide a real positive and accelerated impact on this industry that’s needed. These are great companies. If the best content is going to win, there needs to be some consolidation in order to have these businesses be stronger and have a better consumer experience”

- There is some mixed opinion about Trump’s impact on antitrust enforcement

- It is widely expected that Trump will replace FTC Chair Lina Khan, who has had an aggressive stance on antitrust (Brendan Carr is seen as a potential front runner)

- Trump has a history of critical comments towards Google, but has also more recently expressed reluctance to break up the Co (despite the fact that the DOJ’s case targeting its online search monopoly began in 2020 during Trump’s first term in office)

- Trump heavily criticized Google throughout his campaign, saying the tech giant was “rigged” and called the Co “very bad,” and suggested he would “do something” about its power

- But he also said during an event in Chicago last month that “it’d a very dangerous thing because we want to have great companies… [and] we don’t want China to have these companies. Right now, China is afraid of Google”

- Trump referred to both Google and Apple as “great companies” during a conversation with radio host Hugh Hewitt

- Trump said in October that if reelected he would do something to make Google more fair and told attendees at The Economic Club of Chicago that Google has too much power; However, he said breaking up the company is not the answer

- The President-elect also slammed the European Union for stepping up regulatory enforcement against US tech firms

- Trump has also expressed skepticism about the ongoing effort in Congress to force a divestment or ban of China-owned TikTok

- But while on the campaign trail, Trump threatened retribution against some tech companies, including jailing Meta’s Mark Zuckerberg

- However, respected DoJ antitrust authority George Hay highlighted that “it’s very rare that, at the presidential level, there’s any attempt to influence the course of cases which have already been filed”; But we know that Trump could be different…

- And Vice President-elect JD Vance has been a major critic of Big Tech

- Changes to immigration policies, particularly regarding H-1B visas, could affect the tech industry’s ability to attract and retain international talent

- Trump’s approach to trade, including potential tariffs on foreign goods, could impact tech companies’ supply chains and international sales

- The impact on AI investment and development is unclear

- Trump promised to rescind Biden’s executive order on AI, which outlines policies around AI governance, promotes competition, and addresses AI-enabled threats (he said the order challenged free speech)

- While there might be less regulatory oversight, which could accelerate development, there could also be concerns about ethical and safety standards

- He called AI “very dangerous” after posting what was deemed an AI-generated image of “Swifties for Trump”

- The Connectivity / Infrastructure sector is expected to see some impact

- The FCC under Trump’s leadership is expected to maintain its stance against net neutrality: This could allow internet service providers (ISPs) to prioritize certain types of traffic, potentially impacting the open internet principle

- The FCC’s spectrum auction authority, which lapsed in 2023, is expected to be reinstated: This would enable the allocation of more spectrum for 5G and other wireless services, which would be a plus for the telcos

- Space and satellite are viewed as well-positioned to advance in a Republican administration

- On a recent episode of the Joe Rogan podcast, Trump said of BEAD, “We’re spending a trillion dollars to get cables all over the country, up to upstate areas where you have two farms, and they are spending millions of dollars to have a cable. Elon can do it for nothing.”

- The FCC might push for Big Tech companies to contribute to the Universal Service Fund, which supports telecom services in rural and low-income areas: This would be a plus for the connectivity players

- Crypto is seen as a big beneficiary of the new administration

- Trump is expected to replace SEC Chair Gary Gensler, who has had a stringent approach to crypto regulation

- Trump’s administration is expected to push for clearer regulations around cryptocurrencies: This could include moving regulatory oversight from the SEC to the CFTC, which is seen as more favorable for the industry

- There are more pro-crypto lawmakers in Congress, hence the potential for new legislation that supports the growth of the crypto industry

- Trump has floated the idea of establishing a federal Bitcoin reserve that could further legitimize Bitcoin as a strategic asset and encourage other countries to follow suit

- There is likely to be a push to expand Bitcoin mining operations w/in the US, aiming to make the country a leader in crypto mining and reduce reliance on foreign mining operations

-> The strongest market reaction in our LionTree TMT & Consumer universe came from the crypto sector; Bitcoin itself was up +10.6% on the day and related stocks such as Coinbase and Robinhood were up +31.1% and +19.6%, respectively

Visibility On Take-Two’s Multi-Year Growth Trajectory Is Improving

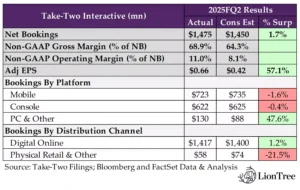

After EA and Roblox’s prints impressed investors last week (see Theme #11 from last week’s Weekly), Take-Two continued the strong showing for the interactive entertainment space this week with headline results that broadly surpassed consensus estimates. Take-Two’s FQ2 net bookings came in +2.1% ahead of expectations, benefiting from stronger than anticipated growth in recurrent consumer spend that was driven by outperformances across the company’s core franchises. In particular, the NBA 2K franchise returned to y/y growth following the “stellar” launch of the 2K25 edition, which saw higher than expected levels of per user monetization despite flat unit sales. The Grand Theft Auto (GTA) series also outperformed. GTA V unit sales exceeded expectations, a new summer content pack, Billion Dollar Bounties, drove “sustained engagement” in GTA Online, and momentum continued in growing GTA+ membership. However, there were some puts and takes on the mobile side. Take-Two’s net bookings ended -1.6% below consensus forecasts, as strong growth in Match Factory! and Toon Blast was offset by declines in the hyper-casual portfolio. Otherwise, upside in the company’s margins was driven by a shift in marketing expenses out of FQ2.

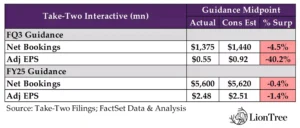

Looking ahead, while Take-Two issued a disappointing outlook for FQ3, the Co reaffirmed its FY25 net bookings and earnings guidance. The implied sequential acceleration in FQ4 net bookings growth will be driven by the release of Sid Meier’s Civilization VII, WWE 2K25, and a PGA Golf title. Commentary was even more positive regarding FY26, which is expected to be a “milestone year” with “several blockbuster titles” on the horizon. Along with GTA VI still being scheduled for fall 2025, Take-Two also highlighted the upcoming releases of Borderlands 4 and Mafia: The Old Country in FY26. As a result, the company still anticipates sequential increases and “record levels of net bookings” in FY26 and FY27, though it is unclear whether sequential improvements in margins are still expected in both years as well. Partnerships could also be another interesting emerging growth channel for the company in the future, as Take-Two is “very, very happy” with its partnership with Netflix and “hope[s] to do more” with the company moving forward.

See below for more of our key takeaways from Take-Two’s FQ2 earnings.

-> Take-Two shares were up +7.5% in response to earnings and closed the week up +8.6%; YTD, Take-Two stock is trading up +10.5%

“Strong” FQ2 Operating Results Were Led By The Co’s “Diversified Portfolio Of Industry-Leading IP”

- Take-Two’s headline numbers beat across the board w/ MUCH better margins and EPS growth mainly due to a shift in marketing expense timing: Net bookings rose +2.1% y/y in FQ2 (vs +1.4% y/y in FQ1) and topped cons by +1.7%; Non-GAAP gross margin of 68.9% was better than cons’ 64.3%, and non-GAAP op margin of 11.0% surpassed cons’ 8.1%; Adj EPS of $0.66 came in +57.1% ahead of cons

- Console net bookings (42% of total bookings) – MISS: Fell -8.3% y/y in FQ2 (vs -3.3% y/y in FQ1) and closed a slight -0.4% below cons

- Mobile net bookings (49% of total bookings) – MISS: Incr’d +9.2% y/y in FQ2 (vs +2.9% y/y in Q2) but ended -1.7% short of cons

- PC & other (9% of total bookings) – BEAT: Was up +24.5% y/y (vs +11.5% y/y) and beat cons by a wide +47.6%

- Recurrent consumer spend (RCS) was better than expected: Grew ~+6% y/y in FQ2 (vs flat y/y in FQ1), exceeding the Co’s expectations for a ~+5% y/y gain; RCS accounted for ~81% of net bookings (vs ~83% in FQ1); Mobile incr’d ~+hsd% y/y, NBA 2K rose ~+lsd% y/y, and GTA Online was ~flat y/y

- A shift in timing of mkting spend was mainly responsible for the upside in the Co’s operating results: Indicated a portion of mkting expenses for both released and unreleased titles shifted out of Q2 due to timing, though they will all still occur “within the yr”

Nearer-Term Guidance Fell Short Of The Street’s Estimates… BUT The Outlook For FY26 & FY27 Remains Optimistic

- FQ3 outlook was underwhelming: Anticipates net bookings between $1.375-$1.440bn, representing a +5.2% y/y increase and missed cons by -4.5% at the mid-pt; The adj EPS range of $0.50-0.60 would mark a -22.5% y/y decline and was -40.2% below cons at the mid-pt

- The largest contributors to net bookings: Include NBA 2K, the GTA series, Toon Blast, the hyper-casual mobile portfolio, Match Factory!, Empires & Puzzles, the Red Dead Redemption series, Words with Friends, and Merge Dragons!

- RCS growth is expected to expand further seq: RCS is expected to rise ~+9% y/y (vs ~+6% y/y in FQ2), consisting of a ~+ldd% y/y uptick in mobile as well as an increase in NBA 2K, offset by a decline in GTA Online

- OpEx growth is projected to decel seq: Forecasts OpEx growth of ~+11% y/y on a mgmt basis (vs ~+24% y/y in FQ2), driven mainly by addt’l mkting for Match Factory! and the addition of Gearbox, partially offset by savings from the cost reduction program

- FQ4 net bookings growth is expected to accel seq: The “big difference” vs last yr will be driven by the Civ 7 launch, as well as a PGA and WWE title being released during the qtr (last yr the Co only had the WWE title)

- FY25 net bookings guidance was reiterated: Still expects net bookings to grow ~+5% y/y to $5.55-5.65bn, which is slightly below cons at the mid-pt

- BUT the Co now anticipates higher RCS growth due to NBA 2K: Now projects RCS to be up ~+4% y/y (vs prior ~+3% y/y) and account for 78% of net bookings; Continues to assume a ~+hsd% y/y increase in mobile and a decline in GTA online; NBA 2K is expected to grow ~+lsd% y/y growth (vs prior flat y/y)

- The breakdown by labels is expected to be ~51% Zynga, ~32% 2K, and ~17% Rockstar Games (previously Zynga was projected to comprise ~50% of the mix and ~1% was assigned to “other”)

- EPS guidance was unchanged: Still forecasts GAAP EPS net losses of -$4.33 to -$3.95; The implied adj EPS range of $2.35-2.60 is -1.4% below cons at the mid-pt; Reminder, Take Two originally guided for GAAP EPS between -$3.90 to -$3.50 at the start of the yr

- OpEx is still projected to increase ~+10% y/y on a mgmt basis: Along w/ the addition of Gearbox as well as higher personnel costs, increases in ongoing mkting support for Match Factory! and other launches planned for next yr will be partially offset by savings from the cost reduction program

- Take-Two “remain[s] confident” it will achieve seq increases and “record levels of net bookings” in FY26 & FY27: The release of GTA VI, Mafia: The Old Country, and Borderlands 4 will all be drivers in FY26; Although the Co is “really excited” about the pipeline for FY27, it did not share specifics on titles

- Unclear if margin improvements are still expected in FY26 & FY27: Although the Co highlighted these long-term targets on previous call, it didn’t comment on them this time around

Take-Two Delivered Strong Performances Across Its Key Franchises

- The Grand Theft Auto (GTA) series has been seeing “cont’d success”: Performance has been broad-based, as “the title has been doing extremely well” and engagement has been “strong” coming out Q2; These trends are expected to continue throughout the rest of the yr

- GTA V sales outperformed: The title has sold-in 205mn+ titles worldwide to-date (vs 200mn+ units exiting FQ1)

- GTA online also exceeded the Co’s expectations: RCS for GTA Online was flat y/y vs expectations for a decline, driven by sustained engagement w/ the summer content pack Bottom Dollar Bounties and “an array of updates… and experience improvements”, such as a new anti-cheat system for the PC version

- “Momentum also cont’d w/ GTA+”: Membership grew by +35% y/y (vs growth in the “strong double-digits” in FQ1); Added the classic title Bully to the library of available games

- NBA 2K25 had a “stellar launch”: The title was released on Sept 6

- NBA 2K25 “achieved phenomenal RCS performance”: “Engagement on a player basis is up significantly over the last game”; Compared to 2K24 for the same period last yr, 2K25 saw “meaningful double-digit growth” in ARPU and +40% growth in avg games per user

- BUT the gen 9 console transition weighed on unit sales: The title has sold-in nearly 4.5mn units (~flat y/y), as the Co is “still being hurt” by declines in gen 8 consoles outpacing growth in gen 9 ones; That said, bringing the gen 9 version of the game to PC has helped

- NBA 2K25 “scored among the highest ratings on new gen consoles in recent franchise history”: The new edition added 9,000 new ProPLAY animations, an all-new dribble engine (“the biggest technological update in the series’ 26-yr history”), and a “more interactive and engaging” city experience

- “There’s a whole lot more ground to cover”: “The NBA is making big strides internationally and obviously made new broadcast deals that are very robust… there’s every reason to believe that this is a huge growth biz going forward”

- “Read Dead Redemption 2 posted another fantastic qtr”: Has sold-in 67mn+ units to-date (vs 65mn+ exiting FQ1) and still ranks in the top 10 globally for unit sales six yrs after its release, per GSD; Commentary on Red Dead Online was sparse

- Red Dead Redemption: Undead Nightmare for PC launched last week: Was a “successful” release, though details were limited

- The Borderlands franchise has been “immensely popular”: The “strength” of Borderlands contributed to the overall outperformance in TTWO’s FQ2 net bookings, and the Co sees “many potential growth oppties” for the franchise and other Gearbox titles moving forward

- The Borderlands film was “economically positive” but “wasn’t material” to results: Acknowledged the film was “disappointing” but highlighted that it “actually benefited catalog sales”

- Take-Two will be “really selective” about licensing IP moving forward: The Co “would really prefer that everything that comes out w/ [its] brands… is really, really successful” and “can’t guarantee that, especially when [it’s] out of [their] hands”

- The Borderlands film was “economically positive” but “wasn’t material” to results: Acknowledged the film was “disappointing” but highlighted that it “actually benefited catalog sales”

Take-Two Is “Confident In The Future Outlook Of The Mobile Biz”

- “Zynga delivered another qtr of solid results” –

- “Match Factory! is scaling rapidly”: The title grew +16% q/q in FQ2, driven by “engaging gameplay” and “strategic investments in user acquisition”; The game is on track to become Zynga’s second-largest title in terms of project annual net bookings by the end of this yr

- Toon Blast has maintained its “fantastic” growth trajectory: Net bookings incr’d +50% y/y in FQ2, supported by “highly-engaging” new features; Key learnings from Toon Blast have been applied to Zynga’s other games, including Toy Blast

- Blended monetization efforts in hyper-casual have been “advancing well”: Highlighted that Screw Jam, specifically, remains a top 50 game in the US Apple App; The Co has been encouraged by the net bookings and profitability milestones the title has reached and is optimistic about it going forward

- The Co is “really excited” about new titles coming out: Game of Thrones: Legends and Nordeus’ Top Eleven soccer manager game launched in FQ2, w/ the latter generating “positive sentiment around the community”; CSR 3 – Street Car Racing is coming later as well

- The Co also continues to expand its offerings within its “highly accretive” DTC biz

- Take-Two is “feeling pretty sanguine” about the mobile mkt right now: Believes “consumers are actually rewarding people for taking risks and releasing new titles that are compelling and engaging”

- “New IP is the lifeblood of the industry”: This has been “the biggest change in the mobile industry over the last couple of yrs”, and the Co’s “commitment to investing in new IP is serving [it] well”

- On mobile advertising – Take-Two is “a little bit less reliant on third-parties than some of [its] other competitors”: This is based on the Co’s “broad portfolio of mobile games” and its “enormous database” across those

- Still, “working w/ third-parties is something… [it] will continue to do in the future”: Emphasized that the Co has “always used more than Chartboost” and “would never rely just on one”

The Co “Cont’d To Make Great Progress In Advancing Its Development Pipeline”

- Three major releases are slated for FQ4: Including Sid Meier’s Civilization VII, WWE 2K25, and a PGA Golf game

- WWE 2K25 “is a really important title” for Take-Two: The iteration “promises to take the Co’s successful pro wrestling franchise to “new heights”; Will share more details in the coming months

- FY26 is expected to be a “milestone yr” w/ “several blockbuster titles” slated to launch:

- GTA VI is still scheduled to be released in fall 2025

- GTA Online: Rockstar also plans to bring the “much-requested” PS5 and Xbox Series features of GTA Online to the PC platform “in the new yr”

- Borderlands 4 and Mafia: The Old Country are also coming during the yr

- GTA VI is still scheduled to be released in fall 2025

- Release timeframes for CSR Racing 3 and Judas still have yet to be announced

- Tales of the Shire: A Lord of The Rings Game was omitted from the release schedule after being included last qtr

Other Highlights

- Take Two “hope[s] to do more” w/ Netflix moving forward: “We think very, very highly of Netflix. We value the relationship w/ them greatly. I think it is pretty important for them to offer a robust array of audio-visual entertainment to their subs, and that by definition has to include interactive entertainment’

- Regarding the decision to sell Private Division –

- “It became clear that our thesis… was going to be challenging at best”: Private Division’s strategy was to work w/ independent devs to create “huge, durable” IP; However, while some of these titles “pretty big breakouts”, they “were not big in the context of [Take Two’s] core IP at 2K and Rockstar”

- Take Two’s “job really is to focus on making the biggest and best hits for the mktplace”: Take Two is focused on “being a top 10 player”, which is “the core of any mature entertainment biz”; “Those are the Cos that matter. Those are the Cos that grow. Those are the Cos w/ op margins”

- “It’s the big 4 [sports] that really matter”: “That’s a pretty competitive space… but the footprint is big enough now and the growth oppties are great enough now that even working on what we have gives us plenty to do with plenty of opportunity leavened by great optimism”

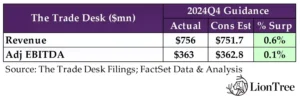

10 Significant “Landscape Changes” Are Driving The Trade Desk’s Business

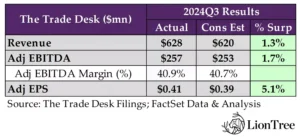

The Trade Desk has been one of the best performing stocks in our LionTree TMT/Consumer Universe, trading up +84.2% YTD ahead of results this past Thursday. While we would argue that performance was solid and the visibility to future growth remains high, it turned into a sell-the-news event, given that expectations were already high. Q3 results marginally topped Wall Street estimates but reflected a strong +27% y/y top line growth rate as well as strong 41% adj EBITDA margins. Q4’s revenue growth guidance of +25% is a slight sequential deceleration but was underpinned by several secular growth drives, which will support growth in 2025 and beyond. Mgmt did a great job on the call detailing the 10 “significant landscape changes” that are expected to drive the Co’s business looking ahead. We’ve heard about some of these growth areas already (like CTV and retail media), but the very bullish tone on the audio opportunity stood out as did some of the other factors mentioned. Big picture, the Trade Desk estimates that its business accounts for ~1% of the total global advertising market, and it has 99% more of the market left to explore.

See below for our main takeaways from the Co’s earnings and results.

-> TTD shares initially trade down as much a -12.5% on the back of results but came back a bit and closed the day down -5.6%

Solid Q3 Results Were Slightly Better Than Consensus, While Q4 Guidance Was In-Line

- Q3 results slightly topped consensus expectations: Q3 rev incr’d +27.3% y/y (vs +25.9% y/y in Q2), topping cons by +0.3%; Adj EBITDA rose +40.9% y/y (vs +41.4% y/y in Q2), beating cons by +1.7%; Adj EPS beat by +5.1%

- CTV was the main growth driver

- Percentage shr of the biz:

- Video, which includes CTV, represented a high 40s% (and continues to grow as a % of mix)

- Mobile represented a mid-30s %

- Audio represented ~5%

- Display represented a low double-digit %

- For the past 7 quarters in a row, ad spend outside of North America has increased more quickly: North America represented 88.0% of the biz in Q3 and international represented 12.0%

- But Q4 guidance was in-line to a tad worse than expected: Anticipates rev to increase ~+24.8% y/y to $756mn, which was in-line w/ cons; However, adj EBITDA guidance was -0.2% below cons

- Despite some caution from advertisers in certain verticals, such as autos, consumer electronics, and media, the Co remains optimistic for the remainder of Q4 and thinks the Co is well positioned in 2025, given advancements in Kokai platform, expansion in CTV, retail media and supply chain innovations, like OpenPath technology

- Political ad spending for 2024 is expected to be in the low single digits as a percentage of overall spend, down from the mid-single digits in 2020; Some brands are not as interested as advertising in a polarized political environment, and so those dynamics have made things a little bit different in this Q4 vs other Q4s

Ten “Significant Landscape Changes” That Create Tailwinds For TTD’s Business Looking Ahead

- The macro environment itself: The Fed’s efforts to combat inflation through interest rate hikes mean consumers are more cautious about their spending

- As a result, advertising becomes crucial in helping brands compete for market share, influencing which products consumers choose based on perceived value

- Increasing pressure on CMOs: They are under more pressure to drive revenue and are working more closely with CFOs in this regard

- The Trade Desk’s AI and data science enhancements in their latest product, Kokai, are helping both CMOs and CFOs rely on TTD for delivering measurable growth

- The Co’s Tools like UID2 and OpenPath are helping advertisers gain insights into their audience, leading to better monetization strategies; For instance, a news publisher using OpenPath saw their fill rate increase by +7x, leading to a revenue increase of more than +25%

- The move to AI: Kokai, which includes significant AI and data science advancements enhances ad optimization and targeting, allows for better data insights, and helps advertisers to make informed decisions about ad placements across various platforms

- Evolving situation at Google: Google excels in Search and YouTube, and it also has an incredible opportunity in Cloud and AI, most notably in Gemini, and is focusing priorities there

- Expect Google to continue to de-emphasize its network business, where it competes with TTD

- Believe that Google’s pending antitrust trial will cause the Co to change its behavior and become more “cautious” on the business where it competes with TTD

- Changes in CTV market dynamics: CTV is both The Trade Desk’s largest and fastest-growing channel, and advertisers can see the contrast between TTD’s offering and the role they play with brands and agencies compared to walled garden

- Inventory is no longer an issue; Now it’s about the quality of the inventory as well as the quality of the signal

- As inventory scales and scarcity decreases, advertisers have a lot more choice; They also have a harder job, which is assigning value to a lot more inventory

- The competition for quality content is intensifying: Variety reported that the top six media companies will increase content spending this year by +9% to a record $126bn, all of which needs to be funded

- Intl is a big growth driver: International spend growth outpaced North America once again with notably strong performance in CTV

- Have been expanding in the UK and Germany; India is also a big opportunity

- Not concerned about Amazon as a competitor in CTV: This is given Amazon’s conflict of interest; “They are going to be pushing ads on premium content that they own, meanwhile, neglecting premium content that others own, while we have no dog in the hunt, and we’re just trying to help people objectively decide”

- “I could not be more excited about our position in CTV and the size of growth opportunity for us in the years ahead”

- Inventory is no longer an issue; Now it’s about the quality of the inventory as well as the quality of the signal

- The macro environment itself: The Fed’s efforts to combat inflation through interest rate hikes mean consumers are more cautious about their spending

-

- There’s pressure to make the supply chain better: The advertising ecosystem is refining its supply chain to become more efficient than walled gardens; Companies focused on adding value will likely gain market share, while those focused on extraction will lose share

- The Co remains optimistic about OpenPath’s long-term impact, believing it will play a crucial role in navigating the complexities of the advertising supply chain and improving market efficiency

- Trends in audio: The TAM of audio is wrongly defined in comparison to legacy radio; It is much bigger than understood

- Digital audio is still in its early stages, similar to where CTV was a few years ago, with US consumers now averaging 3 hours of digital audio consumption daily

- The recent partnership between TTD and Spotify aims to enhance addressability and insights for advertisers, leveraging tools like UID2 and OpenPath, and is seen as a promising opportunity to capitalize on the growing engagement in digital audio

- Retail media: There is significant opportunity in retail media, highlighted by Amazon’s success in using retail purchase data to enhance business performance

- Major retailers like Walmart and Target can boost sales by advertising products that consumers frequently buy

- Retail media’s rapid growth is expected to accelerate through 2025: “Retail data on our platform is transforming how many CPG advertisers approach measurement and attribution.”

- Trade Desk continues to win incremental shopper marketing budgets

- Changes in live sports: The Co is experiencing strong engagement in live sports, with an avg of 1.5bn ad impressions per weekend during the football season; Live sports content is premium and often scarce, making it ideal for programmatic advertising

- Cumulative impact of various industry changes: The complexity of the advertising landscape, particularly in light of challenges faced by companies like Google, creates a need for guidance among clients navigating these shifts

- The Trade Desk’s focus on the buy-side, and its objectivity align its interests with those of agencies and brands, positioning it as a supportive partner during these transitions

- The Co has established itself as a leader in the open Internet, leveraging its global presence and innovative products, including recent platform enhancements

- There’s pressure to make the supply chain better: The advertising ecosystem is refining its supply chain to become more efficient than walled gardens; Companies focused on adding value will likely gain market share, while those focused on extraction will lose share

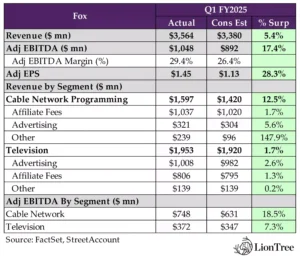

Fox Continues To Pull Away From The Pack… It’s Been Good To Be In Sports & News

Fox had a stellar quarter, surpassing expectations with a +5% revenue beat and a +17.4% EBITDA beat, driven by strong performance in Cable Networks, in particular, which was across the board but included a notable +160% y/y increase in “Other” revenues, thanks to sports sublicensing. Advertising revenue saw a nice gain of +11% y/y due to Political ad spend (set a company “record”) at the local stations, but a re-acceleration of revenue at Tubi was also a key highlight (also bolstered by political advertising and benefitted from improved fill rates). Tubi is on track to hit the $1bn revenue mark this fiscal year. Ratings and viewership dynamics in Fox’s Sports and News properties continue to be positive. The MLB postseason and NFL games drew impressive audiences, while Fox News maintained its strong ratings. Despite some challenges, like increased rights fees and NFL scheduling changes, we’d expect that strong performance to continue in the coming quarters, with significant contributions from the Super Bowl and a solid entertainment lineup. Overall, Fox’s positioning in sports and news has been a differentiator relative to other big Media conglomerates, and this is certainly reflected in the Co’s shares rallying +50.3% YTD vs Paramount -25.2%, Warner Bros Discovery down -19%, and Disney up +9.7%.

-> Fox shares rose +3% on the back of result and is up a whopping 50% YTD

It Was A Blowout Qtr Relative To Expectations, Especially In Cable Networks

- Total revs beat cons by +5% (grew +11% y/y), and total adj EBITDA beat by +17.4% (grew +21% y/y), with the biggest upside coming from Cable Nets

- Cable Networks – Rev beat by +12.5%, and adj EBITDA by +17.5% with big upside in “Other”

- Revenue grew +15% y/y

- Other revenue grew +160% y/y, which was primarily due to higher sports sublicensing revenues at the national sports networks

- Adj. EBITDA grew +23% y/y

- Revenue grew +15% y/y

- TV Stations – revs beat by +1.2%, and adj EBITDA beat by +7.2%

- Revenue grew +10% y/y

- Adj EBITDA grew +3% y/y

- Bought back $300mn so far this fiscal year

An Improvement In The Pace Of Cable Nets Subscriber Losses Stood Out

- Total affiliate revs grew +6% y/y, with +10% y/y growth at TV (vs +9% in FQ4) and +3% y/y increases at cable (vs +2% y/y in FQ4)

- Industry subscriber declines were “a touch under 8%”, a slight improvement from last quarter’s “mid-8% range”

Tubi Re-Accelerates Growth

- Total Tubi revenues accelerated significantly from +7% in FQ4 to +19% in FQ1

- Tubi revenue growth has “accelerated” in FQ2 thus far

- Pacing to surpass the $1bn revenue mark this fiscal year

- Drivers:

- Tubi has the scale and marketplace awareness to be a must-buy for advertisers wanting to reach this audience

- Tubi’s fill rate has improved significantly, helping drive revenue growth

- Political was a key driver but seeing underlying core growth as well

- Tubi has become a material recipient of and gaining share in political advertising

- Ex-political, continue to see growth in FQ2 and “we think beyond”

- Haven’t seen any evidence of cannibalization from stations into digital or into Tubi: “Tubi was able to capture money that we couldn’t take entirely on the station”

Fox Should Continue To Outperform The Overall Ad Market Trends Given Sports & News

- Total ad revs were up +11% y/y (accel from flat y/y in FQ4), boosted by political advertising at the stations, continued momentum at Tubi, and “strong” audience growth at Fox News Media

- Cable ad revs grew +11% y/y (accel from +3% y/y in FQ4), predominantly driven by FOX News media, which saw higher ratings, direct response pricing, and digital rev, partially offset by higher preemptions associated w/ breaking news coverage

- TV ad revs grew +11% y/y (accel from -1% y/y in FQ4), led by the “strong” political cycle at their local stations, cont’d growth at Tubi, and the benefit of higher NFL ratings and NFL scheduling w/ week 4 of the season sliding back into the Sept qtr; Benefit of UEFA EURO and Copa America in the current yr qtr were “more than offset” by the absence of the FIFA Women’s World Cup

- Seeing “very healthy growth” across all the markets they participate in

- Helps that Fox is not “overly exposed” to general entertainment

- Achieved record political rev for both FQ1 and the full fiscal year: Inclusive of the “very substantial and dramatic” impact of the 2020 Georgia Senate runoff

- Tubi has become a “material” recipient of political advertising: As campaigns look to maximize reach and efficiency, Tubi has “clearly differentiated” itself with its large, hard to reach audience coupled with its advanced targeting and geo targeting capabilities

- “From a revenue perspective, it’s the local stations that are our election heroes”

- Local political advertising did push out some local-based inventory: Auto and retail was soft, though betting has returned growth and was “pretty strong”

- Do you expect any affects from outcome of election? “I don’t think it would impact us”

- Sports continues to be a point of strength

- Had a “tremendous” World Series that outperformed budget and expectations

- Football has sold “very well”; Super Bowl is already sold out at record pricing

- News ratings were “strong”, particularly amongst the key 24-54-year-old key demographics

- Helped with direct response pricing being up “very significantly” in FQ1 and “almost double significantly” in FQ2

- Entertainment scatter is also “strong”

Having A “Strong” Fall Season Across Fox’s Sports Portfolio

- MLB postseason has been “both impressive and dramatic”: FOX had the highest rated divisional series ever on FOX Sports 1, the most watched league championship series in the past five years, and the best MLB postseason on FOX since 2017

- World Series in particular was a big hit: Saw an avg of 6mn viewers tuned in each night of the 5-game series across their networks, with ~19mn viewers watching Game 5, making it the most watched World Series in Game 5 in 7 years

- NFL on Fox is off to its best start in five years

- America’s Game of the Week (“the #1 TV program on all TV”) is averaging ~26mn viewers, incl a +28% increase in viewership in younger demos vs last season

- Successfully launched new Fox College Football Fridays in Sept, which is averaging ~3mn viewers each week, “handily out-rating” their prior Friday night programming by 40%+ in its first month

News Segments Sustained Momentum

- In FQ1, total News audience grew 40%+ y/y w/ 60%+ y/y increases amongst 25-54-yr-olds

- Fox News Channel was the second most watched network in all of television in FQ1, trailing the “Summer Olympics enhanced NBC”

- Fox News ended the quarter as the most watched cable network in total day and in primetime

- Fox News was also the #1 cable news channel

- Momentum is continuing through October, with FQ2 total day ratings up +20% y/y and prime ratings up 30%+ y/y

Some Color On EBITDA Bridge That Will Impact TV Earnings In FY25

- General momentum from –

- “Enormous cyclical tailwind” from political advertising, across Cable and Tubi

- Underlying momentum from Tubi

- MLB postseason, which will be an uplift first from both a rev and margin perspective

- Some challenges in FQ2 –

- Increased rights fees across the board

- NFL scheduling will be a headwind to ad rev b/c there won’t be a Christmas game, which they had last year

- Reorientation in college sports rights will be a “big shift”, and weekend expansion will increase costs

- Partially offset by no WWE for the rest of the year and the discontinuation of Pac-12

- Looking into FQ3 and FQ4 –

- Super Bowl in FQ3 will be “very, very” cash flow accretive but not from an EBITDA perspective

- Impact of FQ3 entertainment schedule coming back vs last yr

- Won’t have large soccer tournaments in FQ4 (like UEFA Euro or FIFA) which will be helpful in FQ4

- “Generally speaking… we think TV is going to have a really, really strong sort of second, third and fourth quarter”

Other Key Comments On Venu, Sports Betting, And Comcast

- No new news on Venu: Awaiting their appeal of the injunction, and “we’ll see where we go from there”

- The narrative on sports betting remains the same: Working through approvals process for Flutter / FanDuel; Have to get a license in every state that FanDuel operates in; Think this process will be completed in a year

- Have 6 years in their option

- Doesn’t see any impact from a potential Comcast Cable Nets spin-off: And in Fox’s case, “breaking apart part of the business would be very difficult, both from a cost point of view and from a revenue and a promotional synergy point of view”

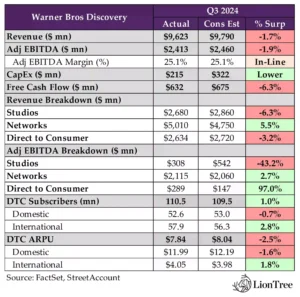

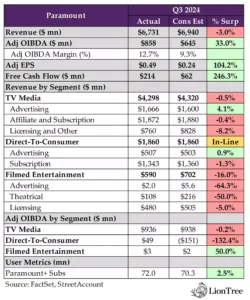

WBD & PARA: The Streaming Transition Has Its Ups & Down

The legacy media names took center stage on the TMT earnings circuit this week. In addition to Fox (see Theme #5), Warner Bros Discovery (WBD) and Paramount (PARA) were the other two big reports out this week.

Starting off with WBD, there was a lot of enthusiasm about its DTC segment surprising the Street with profit that was ~+98% above expectations, fueled by its largest-ever quarter of subscriber growth since the launch of Max (added +7.2mn in Q3, which is double the +3.6mn added in Q2). Streaming profitability for WBD’s Max reached an “inflection point” where subscriber growth, revenue growth, and adj EBITDA growth is all happening at the same time, as years of investment are now starting to bear fruit. On the advertising side though, WBD posted yet another seq decline, with ad rev falling -6.3% y/y (from -3.5% y/y in Q2), with growth at DTC unable to offset the decline in Networks. Lastly, the Studios segment was a drag in the qtr. Several changes are in process, but it will take some time for the financial impact to flow through and benefit the top-line.

Over at Paramount, in many ways it felt like a déjà vu quarter. The top-line slightly missed vs Wall Street (by -3.0% in Q3, vs -5.6% in Q2 and vs -0.5% in Q1), but a strong adj OIBDA beat (by +33% in Q3, vs +53% in Q2 and vs +31% in Q1). Similar to WBD, Paramount’s DTC business was also its shining star, with the segment posting another profitable qtr (its second in a row), largely driven by marketing efficiency in acquiring subscribers across many of its channels. But the Co’s DTC business will move to a loss in Q4 (a negative surprise) due to the timing of content marketing spend. Nonetheless, mgmt still reiterated their guidance for domestic P+ profitability in 2025 and also mentioned that international streaming profitability is tracking 12-18 months behind domestic. On the positive side, Paramount’s ad rev outperformed Street expectations, growing +2% y/y, with particular upside in TV Media; however, total affiliate revs disappointed at down -1% y/y (but ex Showtime PPV events, it would have incr’d by +1% y/y). Like WBD, PARA’s filmed entertainment business disappointed. Mgmt still expects the Skydance transaction to close in H1:25.

Overall, there were a lot of moving parts and a lot to dig into… See below for more of our takeaways. There are 2 sections below – one for WBD and one for PARA.

-> The 2 stocks had divergent reactions to earnings, with WBD trading up a notable +11%, while PARA traded down -4%; YTD, WBD is now down -19%, while PARA is down -25%

1) WARNER BROS DISCOVERY (WBD) – See below for what we thought was most important and incremental from its results and conference call

WBD – Top-Line Disappointed in Q3

- Consolidated revs missed by -1.7%: Fell -3% y/y (vs -5% y/y)

- Studios and DTC missed, while Networks beat

- Adj EBITDA missed by -1.9%: Fell -19% y/y (vs -16% y/y in Q2)

- Studios missed, while Networks and DTC beat

WBD – Continue To Act “Aggressively” To Reduce Expense Base And Lift FCF Conversion

- FCF decreased -$1.4bn y/y and missed by -6.3% in Q3: Decreased to $632mn from $2.1bn in year-ago qtr, largely due to higher net cash content spend after lapping last year’s Q3 strike impact and unfavorable Olympics-related working capital dynamics

- Looking into Q4, while another y/y increase in net cash content spend in Q4 is expected, FCF should represent a healthy conversion of EBITDA

- Saw seq increase in net leverage from ~4x in Q2 to 4.2x in Q3, which was directionally in-line with expectations, given the seasonality of free cash flow and Olympics-related free cash flow headwinds

- Continue to expect to delever y/y “albeit much more modestly than initially planned” (in-line with commentary last qtr), in part due to the Studios shortfalls and impairment

- Repurchased and repaid ~$900mn in Q3; Have paid down $16bn+ in debt to-date

- Continue to target 2.5-3x gross leverage for the longer-term

- Did not share updated view on M&A and potential asset sales/acquisitions, given recent political shifts and reports of Comcast splitting/selling cable asset

- Reiterated belief that current stock price “doesn’t adequately reflect the underlying value of these great assets that we have”

- Focused on driving growth through operational improvements worldwide and always looking at way to enhance shareholder value.

WBD – Advertising Continued To Decel Seq Across The Board In Q3 / Taking Measured Approach With DTC Advertising, Which Is Still In Early Stages

- Q3 total ad rev fell -6.3% y/y, which was a seq decel from -3.5% y/y in Q2: Seq step-down was expected and was in large due to their seasonally slower sports schedule, as well as the Olympics, which Europe benefitted “modestly” from, but the much larger US biz was adversely impacted by

- DTC ad revs were up +49% y/y (decel from +98% y/y in Q2), driven by “healthy” demand for Max in the US

- While the intl contribution to DTC advertising is still “quite small”, see oppty ahead as they scale the subscriber base and drive monetization

- Networks ad revs were down -13% y/y (decel from -9% y/y in Q2)

- DTC ad revs were up +49% y/y (decel from +98% y/y in Q2), driven by “healthy” demand for Max in the US

- Still in the “very early innings” of advertising scale and rev growth and still have “enormous runway” in qtrs ahead: Plan to grow through –

- Expanding availability of their ad-supported streaming svs to more markets

- Increasing the number of ads shown (ad load) within their content, as they currently have a lighter ad load than many competitors

- Developing new, creative ad formats that are more appealing to advertisers and provide better engagement for viewers

- Focused on balancing ad load w/o hurting viewer experience: Learned lesson from cable that too much advertising impacts quality of the experience

- “As others add a lot of inventory, we really like the idea that we’re not doing that. You’re not going to be interrupted watching House of the Dragon or White Lotus, at least for the foreseeable future”

WBD – Q3 Was A “Material Inflection Point” For Max / Profitability Beat Was A Standout And Subscriber Adds Doubled Q/Q

- Saw a big beat on profitability, despite revenue miss in DTC in Q3

- DTC rev missed by -3.2%…: Grew +9% y/y (vs -6% y/y in Q2) to $2.6bn

- … But DTC adj EBITDA turned positive and beat by substantial +97.0%: Came in at $289mn vs Q2’s -$107mn

- Expect continued strength in Q4 / “Highly” confident they are on track to “meaningfully exceed” $1bn adj EBITDA target in 2025

- Q4 outlook: “Expect similar levels of subscriber-related revenue growth and EBITDA contribution”

- Longer-term outlook: “Expect every quarter that we’re going to be seeing revenue growth, profit growth and subscriber growth”

- Max added 7.2mn subs in Q3 to reach 110.5mn (beat by +1.0%): Was double the +3.6mn subscribers added in Q2

- Driven by Olympics in Europe, traction from recent intl launches, momentum on bundles, and a more consistent and resonant content lineup

- ~40% of global gross adds signed up for the ad-lite tier and global ad-lite subs grew 70%+ y/y

- Max is now available in 65 markets: Started the year of only available in the US

- Later this month, will launch in 7 markets across Southeast Asia

- In 2026, will be available in Australia and over a dozen other markets, with more to come, including three of the biggest mkts in Europe

- “We have 2+ years of growth ahead of us” – What have been and will be Max’s growth drivers?

- “Great content”: “We believe our content will continue to provide us a meaningful, competitive advantage and we are only scratching the surface of what we can achieve through added scale”

- Consistent release of tentpole series, new originals, and feature films through at least 2026

- Beginning this past June, with S2 of House of the Dragon, and continuing now with The Penguin and expanding forward with titles like Dune: Prophecy, White Lotus, The Last of Us and Peacemaker

- 15+ years of local sports and region-specific content across Europe and Latin America, creating a competitive advantage few can rival

- Exclusive streaming of major events, like the Olympics, in many markets across Europe

- “Even without the Olympics, we expect our momentum in driving Max subscriber growth to continue going forward”

- Only in just over half of the addressable broadband markets around the world (excluding markets like China, Russia and India)

- Password-sharing crackdown

- Improving product experience, where “we’ve gotten better, but are not great yet”

- Factors impacting growth of Max in the US

- Headwinds –

- Mix is changing, and the shift from HBO’s older, wholesale model to Max means they’re losing some subscribers through traditional pay-TV but making up for it with retail subscribers

- Penetration gap is largely in lower-income, more price-sensitive households (sub-$100k) which may already have 1-2 streaming svs and Max becomes an “in-demand but harder-to-finance proposition”

- Solutions –

- Ad-lite offering is “best way” to penetrate more price-sensitive consumers

- More bundles, like those w/ Disney and Hulu

- More partnerships, like those they have with Charter and DoorDash

- Industry consolidation to improve the consumer experience, as viewers are overwhelmed by a variety of apps with different pricing, which can be confusing and inconvenient

- Headwinds –

- Continue to be a big proponent of bundling and shared several learnings –

- Consumers not only want lower prices for more svs, but also the ability to navigate seamlessly between those products

- Seeing “a lot” of strength in partnership w/ Disney and Hulu; It’s early, but subscriber growth is “significant” and consumer satisfaction is “quite high”

- Seeing “big” advantage from leveraging relationships they have in intl markets, and entering them w/ local sport, local entertainment, and the HBO and Max content

- Financial framework by which DTC biz is managed has not changed, despite increased options to reach consumers

- Whether it be directly, bundled, in partnership, or more traditional wholesale agreements, which all have implications for certain KPIs

- Focus is on lifetime value vs subscriber acq cost, making tradeoffs between distribution channels and models based on ARPU, upfront investment, and churn

- Focus is also on subscriber-related rev (subscription + ad rev) as best measure for progress being made in scaling the DTC biz

- Expect ARPU to trend lower in the near-term…: Given cadence of Max’s rollout over the next ~18 months in intl mkts and launch of ad-supported offering in many more markets

- … But strong future subscriber-related rev and adj EBITDA growth, as well as enhanced retention, the cadence of which will reflect when, where and how heavily they invest in subscriber acquisition

- On price increases – Highlighted “premium nature of our product” is providing WBD a “fair amount of room” to continue to push price

- Have been “judicious” about prior price hikes, but each one done so far has seen churn come in lower than projected and retention continue to be strong

- Have password sharing kicking off in 2025 and into 2026 which “in effect is a form of a price rise…you’re going to see that as an additional kicked”

- Room to increase price internationally, though still early as international rollout began just 6 months ago

WBD – The Studios Biz “Must Deliver More Consistency”

- Studios missed expectations on both rev and adj EBITDA in Q3

- Studios rev missed by -6.3%: Down -17% y/y (vs -5% y/y in Q2) to $2.7bn

- Adj EBITDA missed by -43.2%: Down -58% y/y (vs -31% y/y in Q2) to $308mn

- Anticipates improved profit results for overall Studios biz in Q4, driven by what is expected to be “another successful quarter for Warner Bros TV”

- Expect Studios Q4 EBITDA to be up “a few hundred million dollars y/y”, depending on the timing of certain content licensing deals

- Longer term – “Our ambition is to get back to at least $3bn and then start growing… Over the next several years, we expect our Games and Motion Picture businesses to deliver more consistency, resume industry-leading performance, and contribute substantially to Warner Bros. Discovery’s business success”

- Have held back ~$1bn worth of content that could have been sold, investing instead in Max and HBO streaming platforms: While this impacts short-term profitability in Studios, it is expected to enhance DTC growth over the coming years

- TV is on track to have its most profitable year in scripted content in the last five years / TV rev grew +30% y/y (vs -27% y/y in Q2)

- Q3 benefited from y/y comp against impact of strikes last yr, though “the underlying performance remains robust”

- “We believe we’re benefitting from a flight to quality”

- Currently making 80+ live action scripted, unscripted and animated series for nearly 20 platforms, including all the major US broadcast networks and key US SVOD platforms

- Expect momentum to continue in Q4, and TV is expected to be up “significantly” y/y

- Motion picture biz continues to face issues of inconsistency / Theatrical rev fell -40% y/y (vs +19% y/y in Q2)

- Q3 was largely driven by “strong success” of Beetlejuice Beetlejuice, though Barbie in the prior year and bulk of marketing spend for October release of Joker: Folie à Deux weighed on y/y comps

- Looking into Q4, expect film biz to be “more or less in-line” with yr-ago qtr: Despite Joker’s underperformance weighing on Q4 profitability

- Easier comp in Q4: Had 3 theatrical releases in last two weeks of 2023, for which they realized “hefty” marketing spend with a “relatively limited” amount of rev; Have only one release remaining in Q4 this year, which is the “modestly budgeted” The Lord of the Rings: War of the Rohirrim

- Longer-term, have been focused on improving greenlight governance and franchise mgmt for the past two years, and believe these strategic shifts will deliver improved outcomes in the coming years

- Will start to see lineup of films that new mgmt has been involved w/ from start to finish (vs inherited from prior mgmt) starting this year

- Characterize film slate under new mgmt as “more balanced, both creatively and financially”

- Games biz is “substantially underperforming its potential right now” / Games rev fell -31% y/y in Q3 (vs -41% y/y in Q2)

- Q3 decline was primarily driven by the better performance of the prior year slate, mainly Mortal Kombat 1, compared to the current year slate

- Have four “strong and profitable” game franchises with “loyal global fans”: Hogwarts Legacy, Mortal Kombat, Game of Thrones, and DC (in particular, Batman)

- Focusing development efforts on those core franchises to improve success ratio (vs “trying to launch 10, 12, 15, 20 different games”)

- YTD write-downs in Games biz are $300mn+, which are a “key factor” in this yr’s Studio profit decline: Includes $122mn in Q3 that were due to underperforming releases

- Looking into Q4, expect Games biz to be flat to modestly better y/y, as last year’s launch of Hogwarts Legacy on the Switch platform in November is offset by lower costs

- Role and impact of content licensing strategy in 2024, which have burdened consolidated adj EBITDA and FCF in a “material” way, but will benefit future financial performance –

- Limited library licensing, which are expected to return to more normalized availability levels next year

- “Significant” y/y increase in internal licensing to support the rollout and growth of Max, “which will pay dividends in top and bottom-line performance of the DTC biz for years to come”

WBD – Adapting To Industry Shifts Within Networks Biz By Leveraging Partnerships To Drive Rev Growth Across Distribution Channels

- Networks was the only segment to beat on revenue and adj EBITDA in Q3

- Networks rev beat by +5.5%: Grew +3% y/y (vs -8% y/y in Q2) to $5.0bn

- Networks adj EBITDA beat by +2.7%: Fell -12% y/y (vs -8% y/y in Q2) to $2.1bn

- Linear TV “is still an extraordinarily important part of our business”

- “Core vehicle to deliver WBD storytelling to hundreds of millions of fans worldwide”

- “The significant profits it generates helps fund building the investments that will carry Warner Bros. Discovery into the future”

- Renewal agreement struck w/ Charter is “the best evidence of the important role our linear business continues to play for Warner Bros Discovery”

- Extending Charter’s carriage of WBD’s linear networks while also giving their subscribers ad-lite access to Max was beneficial to Charter, WBD, and consumers

- “This is a sign that these types of agreements will create more stability in our industry”

- Similar deals in the works? “We’re in some discussions with some that are quite interested in doing it, and we’ll just have to see”

- Confidence as they approach renewal negotiations w/ Comcast in the US and Sky internationally? “I suspect we’ll be doing a lot more stuff in the future”

- Can’t go into details about specific deals, but have built decades of various successful partnerships across several markets, including the US, UK, Germany, and Italy

- WBD also has “highly valued” content that strengthens the appeal of cable bundles, which distributors like Comcast recognize

- “Our affiliate renewal pipeline is active, and we remain focused on working with our partners across the fluid distribution landscape”

- Seeing net growth in total Co revenue through these partnerships, as reductions in linear have been “more than offset” by gains in DTC

2) PARAMOUNT (PARA) – See below for what we thought was most important and incremental from its results and conference call

PARA – Q3 Reflects Continued Outperformance On DTC Profitability

- Missed on total revs by -3%, while adj OIBDA beat by a huge +33%: Total revs fell -6% y/y (vs -11% in Q2), while adj OIBDA grew +20% y/y (vs +43% y/y in Q2)

- Revenue miss was from Filmed Entertainment

- TV Media rev – IN-LINE: Revs fell -6% y/y (vs -17% in Q2)

- DTC rev – IN-LINE: Revs grew 10% y/y (vs +13% y/y in Q2)

- Filmed Entertainment rev – MISS by -16%: Revs fell -34% y/y (vs -18% in Q2)

- Revenue miss was from Filmed Entertainment

- Adj OIBDA upside was mostly due to better marketing efficiency in DTC division

- TV Media OIBDA

- DTC OIBDA

- Filmed Entertainment adj OIBDA

- EPS of 49c was well above cons 24c, and the Co delivered $214mn in FCF, which was much better than cons $62mn

PARA – Making Progress On Restructuring Plans, Which Will Have More Of An Impact In Q4

- “Continue to successfully execute” cost reductions that will result in $500mn in annual run rate saving, which will reduce US-based workforce by -15%

- To date, have executed 90% of these reductions and expect to have a remaining completed by EOY

- Restructuring work should have more of an impact in Q4: It was relatively modest in Q3, given timing

- FCF in Q4 will be negative due to content spend timing and cash restructuring payment headwind, but proceeds of Viacom 18 transaction will offset

- Overall puts and takes on Q4:

- Tailwinds: More benefits from the restructuring, political, and it is the strongest ad quarter of the year generally

- Headwinds: Higher content expenses with sports and streaming originals, no true ups from under reporting like before, and some shift of marketing expenses from Q3 into Q4.

PARA – DTC Profitability Will Take A Breather But The Positive Trajectory Is Intact

- DTC posted another profitable qtr (its second in a row), largely driven by marketing efficiency in acquiring subscribers across many of its channels

- BUT DTC will move into a loss in Q4 due to the timing of content marketing spend, but reiterated P+ profitability in 2025

- Intl streaming profitability is tracking 12-18 months behind domestic given relative maturity of the launch; That is “the right way” to think profitability for the streaming biz as a whole

- Paramount+: Revs up +25% y/y, which is a seq decel from +46% y/y in Q2

- Big boost in P+ subscriber adds – Added 3.5mn subs vs -2.8mn in Q2

- Drivers: Helped by an expansion of an international hard bundle deal and the return of NFL and college football, new originals, and theatrical releases; Charter renewal also had a contribution

- Outlook: Expect cont’d subscriber growth (but do not expect to add another new hard bundle partnership in Q4); Impact from Charter renewal will also grow

- P+ global ARPU grew +11% y/y vs +26% in Q2

- Tough comps with last yr’s price increase and a greater than expected shift in the mix to the essential tier and hard bundle subscribers

- Price hike annc’d in Aug 2024 will take some time to be reflected due to the grandfathering of existing essential tier subscribers

- These dynamics will “continue to influence” ARPU growth in Q4

- Some content call outs looking ahead for P+-

- Return of big hit series, like Mayor of Kingstown and Tulsa King

- Internationally have South Park exclusively for SVOD

- South Park return to P+ in the US starting in June of 2025

- Return of Lioness followed by Landman (premieres November 17)

- Big boost in P+ subscriber adds – Added 3.5mn subs vs -2.8mn in Q2

- Pluto reached record engagement: YTD, Pluto delivered its highest consumption increase ever of +5% to 5.6bn viewing hours

- Growth is being driven by incr’d use of VOD w/ more available content, enhanced discoverability, and a better user experience

- Open to evaluating potential partnerships in streaming: Feel good standalone but will be “opportunistic” at looking at partnerships

PARA – Advertising Growth Trends Are Anticipated To be Similar In Q4 vs Q3 & Underlying Affiliate Growth Was Positive

- Total advertising rev incr’d by +2% y/y, beating expectations in both TV Media and DTC

- DTC ads revs were up +18% vs +16% in Q2 due to double-digit increase in sold impressions and higher CPMs

- Outlook: These trends are continuing and expect another quarter of double-digit DTC ad growth in Q4

- TV media advertising rev fell -2% y/y (better than Q2’s -11%), reflecting the return of football and higher political spending

- Similar to last qtr, international advertising benefited from the recognition of previously underreported revenue by an international sales partner

- Outlook: Expect TV media ad growth in Q4 to be similar to the growth rate reported in Q3

- DTC ads revs were up +18% vs +16% in Q2 due to double-digit increase in sold impressions and higher CPMs

- Total affiliate revs disappointed at down -1% y/y, but excluding Showtime PPV events, it would have incr’d by +1%, with growth in DTC more than offsetting declines in linear

- TV media affiliate rev fell -6.6% y/y due to ecosystem trends and the impact of Showtime PPV

- DTC subscription rev grew by +6.8% y/y, with P+ subscription rev up +27% y/y

PARA – Revenue Is Under Pressure

- Licensing and other revenue fell -9% y/y in Q3 and missed cons estimates, given lower volume of licensing in the secondary mkt and lower home entertainment revs: For FY24, expect licensing revenues to decline y/y

- More than half the y/y decline will come from made-for-3P productions which are strategically valuable, but the scale of the business has been impacted by the decision to steer more content to internal platforms

- A smaller part of the y/y decline in licensing is related to second run in library licensing activity, partially reflecting lingering strike impact on the business; It will take longer than expected to return to pre-strike level of output.

PARA – Hopeful Regarding A Resolution Of The Nielsen Dispute But It Is Not Having A Neg Impact On The Business In The Meantime

- Regarding the dispute with Nielsen:

- The Co remains engaged w/ them and are” hopeful for a resolution”: It has been five weeks of this impasse

- “So far, we’re encouraged by our partners’ willingness to lean into innovation and adopt alternative measurement solutions”

- But the economics have to make sense for the business

- What has the impact been from not having Nielsen data? None: “We haven’t seen any adverse impact on ad revenue to date, and we don’t expect a material impact in Q4”

- There is a lot of speculation in the market that PARA’s savings could reach hundreds of millions of dollars a run rate basis

- The Co remains engaged w/ them and are” hopeful for a resolution”: It has been five weeks of this impasse

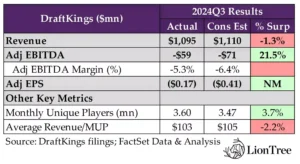

DraftKings: “Hot” Customer Acquisition Trends Outweighed Setbacks From “Customer-Friendly” Sport Outcomes

Amid all the other earnings updates out across the tech, media, and entertainment spaces this week, investors also received a glimpse into how trends in the sports betting industry have been playing out, as DraftKings reported its Q3 results. The company’s headline numbers finished mixed relative to consensus expectations, with revenue coming in -1.3% below estimates, but adj EBITDA beating forecasts by a wide +21.5%. In terms of some of the main highlights from the quarter, the impact of structural sportsbook hold was neutral (though DraftKings didn’t provide a figure on it this time around), while customer acquisition efforts have continued to be more effective than anticipated with the NFL season in full swing and the recent kick off the new NBA season. DraftKings took a “cautious” approach to customer acquisition during the quarter, which was reflected in a +300bps y/y improvement in its promotional reinvestment rate and a nearly -20% y/y decline in CACs; however, the company’s MUPs still exceeded expectations by +3.7%. Additionally, the more “muted” promotional stance helped drive a better than expected top-line flow-through, resulting in the outperformance on adj EBITDA.

Despite DraftKings’ solid showing in Q3, the more incremental commentary on the company’s earnings call was related to its downward revisions to FY24 guidance and its updates to the FY25 outlook. Beginning in October, DraftKings was “stung” by “the most customer-friendly stretch of NFL sport outcomes [it has] ever seen”, and this prompted the company to lower its forecast for FY24 revenue and adj EBITDA by -$250mn and -$120mn at the midpoint, respectively. Nonetheless, DraftKings’ FY25 outlook was still better than the sell-side anticipated, with revenue that is expected to finish +2.6% ahead of estimates and adj EBITDA that was projected to beat the Street’s expectations by a slight +0.2%. Notably, the company emphasized that its adj EBITDA guidance for next year incorporates a degree of conservatism, given the recent strength of the company’s recent user acquisition. In the meantime, DraftKings will look to get the ball rolling on launching in Missouri, which approved OSB earlier this week. There are paths to regulatory approval in Texas, Georgia, and Minnesota as well, but Florida still appears to be far off. All said, the company’s business fundamentals look “healthy” heading into Q4 and 2025.

See below for more of our key takeaways from DraftKings’ Q3 print:

-> DraftKings shares rose +3.0% in reaction to the print, ending the week up +12.4%; YTD, DraftKings stock is trading up +13.8%

DraftKings’ Headline Results Reflected “Healthy” Biz Fundamentals

- Headline numbers were MIXED, with a miss on the top-line but a beat on adj EBITDA: Rev was up +38.7% y/y in Q3 (vs +26.2% y/y in Q2) but closed -1.3% short of cons; Adj EBITDA of -$58.5mn (vs -$153.4mn the prior yr qtr and $128.0mn in Q2) was +21.5% better than cons; Adj EPS of -$0.17 beat cons’ -$0.41

- Adj gross margin returned to y/y growth and was better than expected: Q3 adj gross margin of 40% incr’d ~+300bps y/y (vs ~-400 bps y/y in Q2), driven by declining CACs, higher structural sportsbook hold, and an improvement in the promo reinvestment rate

Lowered FY24 Guidance Was Disappointing, But The FY25 Outlook Surprised To The Upside

- The FY24 outlook was revised downwards due to customer-friendly sport outcomes

- Rev is now projected to be -$250mn lower at the mid-pt: Now anticipates a rev range of $4.85-4.95bn (vs prior $5.05-5.25bn), representing a +33.7% y/y increase and missing cons by -4.5% at the mid-pt

- Guidance assumes that mkt share will be flat: The Co is basing its cohort data and customer acquisition estimates on what it’s seen in the past for mkt share and what that would imply for mkt growth

- Adj EBITDA is now expected to be -$120mn lower at the mid-pt: Forecasts Adj EBITDA between $240-280mn (vs prior $340-420mn), which was -33.1% below cons at the mid-pt

- Rev is now projected to be -$250mn lower at the mid-pt: Now anticipates a rev range of $4.85-4.95bn (vs prior $5.05-5.25bn), representing a +33.7% y/y increase and missing cons by -4.5% at the mid-pt

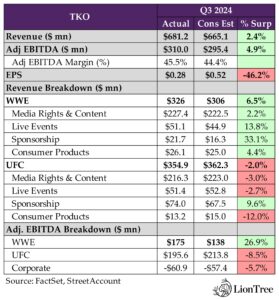

TKO Gets Through The Toughest Quarter Of The Year…

A year into WWE and UFC completing a merger to create TKO, CEO Ari Emanuel’s “conviction in this business is as strong as ever.” Q3 saw a top-line beat driven by better-than-expected performance at WWE, more than offsetting weaker UFC results due to unfavorable timing of events (the qtr only had 10 UFC games vs 13 in the prior-yr qtr). That being said, those three events will benefit Q4, and given the momentum in the business, full year revenue and adj EBITDA is now expected to come in at the upper end of their provided guidance (though analysts had expected more).

Digging into the qtr, demand across both WWE and UFC remains strong, with both leagues hosting several record-breaking events in the quarter. While WWE remains strong in the US, momentum is growing internationally, with 18 shows in Q3, up from 11 in the yr-ago period. Meanwhile at UFC, despite fewer shows in qtr, the league still managed to host its highest grossing event ever in UFC history, which was UFC 306 at the Sphere Las Vegas. It was the first event to feature a title partner sponsor and is expected to be the first of many more title sponsorships in the future, in addition to other sponsorship opportunities that may arise, particularly through its upcoming partnership with Netflix (kicks off in January). Touching on distribution, confidence in the pay-per-view model remains solid, but that doesn’t mean they aren’t open to exploring broader distribution options, especially as new partners may emerge as DirecTV and Dish explore consolidation and Paramount and Skydance close their deal next year.

2025 will be a busy year and will include the absorption of PBR, On Location, and IMG from Endeavor, which is scheduled to close in H1:25. On that front, TKO made it clear on the call that it does not plan to bid on any other Endeavor assets moving forward and emphasized its vision of being a “sports pure play”. And while boxing is a “ripe” oppty that they are open to exploring, it would have to come about in an “organic way”, as M&A is not a route they are looking to pursue on that front.

Also in 2025, TKO will begin a $2bn stock buyback program and pay its first dividend to shareholders in March.

See below for more of our highlights from the qtr.

-> TKO’s stock fell -2.0% in reaction to its report, but ended the week up +0.9%; YTD, the stock is up +47.3%

As Expected, Q3 Was The Toughest Qtr Of The Yr

- Revenue – beat: Grew +52% y/y (vs +179% y/y in Q2) to $681.2mn, which reflected an increase in revenue at WWE, partially offset by a decrease in revenue at UFC

- Adj. EBITDA – beat: Grew +29% y/y (vs +142% y/y in Q2) to $310mn, due to an increase in adj EBITDA at WWE, partially offset by a decrease at UFC and an increase in corporate expenses

- Adj EPS – miss: $0.28 vs cons $0.52

- Authorized a $75mn quarterly cash dividend program, and will make the first dividend payment on March 31, 2025

Expect To Hit Upper End Of FY Guidance Ranges (Though Analysts Expected More)

- What drove the increase in expectations on rev and adj EBITDA? Related primarily to “strong” operating performance on a YTD basis, particularly in live events and sponsorship at both of bizs and visibility through the end of the year

- 2024 revenue – miss: Guided to the upper end of $2.67bn-$2.745bn range vs cons $2.76bn

- 2024 adj EBITDA – generally in-line: Guided to upper end of $1.22bn-$1.24bn vs cons $1.24bn

- Reaffirmed target for FCF conversation in excess of 40%+

Integration Update – “We’re Still In At Least Mid-Innings” In Integration Of WWE And UFC

- Reiterated expectations of exceeding $100mn in annualized net savings

- Expect continued improvement in margin: Driven by –

- Continued cost savings measures and initiatives flowing through to make the Co more efficient top to bottom

- Structuring deals at higher margins than in the past

- Having UFC, WWE, and PBR events on the same week, weekend, or subsequent weekends, which will help save on the cost side

- Selling “Triple Headers”, allowing someone to come in and sponsors all three events, which will be “huge for us and will drive local ad sales”

- Expect FCF conversion to be 60% on a standardized basis and in excess of 60% over time

- For the year, guided to ~50% estimated FCF conversion from adj. EBITDA, impacted by timing of working capital, investments in WWE headquarters, and certain one-time items

- Will make organic investments to further fuel growth, but in conjunction w/ media rights renewals slated for 2026, have a “clear path to continued conversion in excess of the numbers that we’ve said historically”

- Despite recent acquisitions, 85-90% of adj EBITDA going forward will come from WWE and UFC

WWE Posted Strong Results Across The Board, With Adj. EBITDA Margin In Particular Shining Through

- Q3 WWE rev grew +72% y/y (vs +11% y/y in Q2) and was primarily driven by an increase in media rights and content, live events, and sponsorship revenue

- Media Rights & Content grew +8% y/y, which was primarily related to the contractual escalation of media rights fees as well as the timing of their weekly programming, which resulted in one addtl episode of Raw in the qtr compared to the prior year

- Live Events rev grew +31% y/y, which was primarily related to an increase in ticket sales

- Sponsorship rev grew +54% y/y, due to new partnerships and renewals across multiple categories, including beverage, QSR, spirits, entertainment and communications

- Q3 WWE adj. EBITDA grew +18% y/y (vs +45% y/y in Q2), reflecting the increase in rev and decrease in expenses (which primarily reflected lower personnel costs and production costs related to their planned cost reduction initiatives implemented following the formation of TKO)

- WWE’s adj EBITDA margin was 54%, up from 36% in the prior-yr period