All of us here at LionTree hope that you have had a nice holiday and New Year. 2025 was certainly a momentous year with many twists and turns but we are optimistic that the stage is set for a year of growth and opportunity in 2026. Deep and trusted relationships are the cornerstone of our culture and we are deeply grateful for our continued partnership with each and every one of you. We look forward to engaging with you across LionTree’s integrated global platform in the year ahead.

- M&A Advisory: Providing specialized, independent advice to public and private companies and financial investors, and executing tailored solutions across sectors, geographies, transaction types, and corporate initiatives.

- Capital Markets Advisory: Serving as a differentiated partner on capital raising initiatives, providing specialized market insights informed by our thematic expertise and long-term capital relationships.

- Asset Management: Coupling capital with ideas, investing in and alongside our relationships to accelerate transformational innovation in the TMT, Entertainment, Consumer, and associated sectors globally.

- Institutional Investor Membership: Offering select institutional investors access to a network of leaders and insights through select events, targeted meetings, weekly industry reports, and broader thematic analysis.

- Kindred Media: LionTree’s in-house media company elevates its people, relationships, and community through differentiated content. The KindredCast podcast has featured prominent CEOs, investors, and changemakers across media, technology, and everything in between. Stay tuned for new episodes coming soon.

Shifting to industry fundamentals, it was off to the races this week and we focused on the below in this edition:

- While The Major US Indices Tweaked Higher In Q4…Under The Hood, The Majority Of TMT Stocks Traded Down…

- Key Takeaway From CES…“The ChatGPT Moment For Robotics Is Here”

- Holiday Spending Wrap…While Y/Y Growth Rates Slowed Vs 2024, Consumer’s Spending Resilience Remains On Track

- Major AI Developments Across Healthcare & Music + Even More Capital Raises

- Live Sports Cont’d To Reign Supreme on US Screens In 2025

- The Streaming & Connectivity Sectors Already See Some +/- Pricing Adjustments To Start The Year

- AV Launch Timelines Slip, While Complex Self-Driving Tech Proves Far Pricier Than Earlier Projected

- Grab Bag: 2025 Set A Record For Shareholder Activism Globally / Meta Announces Nuclear Energy Projects / iOS 26 Adoption Has Been Lagging

Finally, I wanted to flag one last time the recently published Winter edition of our quarterly LionTree’s Lens: Sector Insights & A Look Ahead. CLICK HERE to watch the ~20-minute video presentation and to access the full slide deck. It’s a great refresher ahead of earnings season, which is kicking off in just a few short weeks!

I hope you have a nice weekend.

Best,

Leslie

While The Major US Indices Tweaked Higher In Q4…Under The Hood, The Majority Of TMT Stocks Traded Down…

Following a strong Q3 with the S&P 500 and NASDAQ rallying +8% and +12%, respectively, the major indices pushed slightly higher in Q4, each rising a further ~+2%.

That sounds rosy but when drilling down into performance across our LionTree Universe of ~175 stocks in the TMT and Consumer sector with $1bn+ market caps, the vast majority traded down in the qtr. Only 35% of stocks traded UP in Q4 vs 61% trading up in Q3.

Of those stocks that traded up, 52% traded up double-digits, which was lower than the 67% in Q3, while on the other end, of those stocks that traded down, 61% traded down double-digits, which was higher than the 52% that traded down double double-digits in Q3. So basically, it was a tougher qtr for most companies in the space.

Which stock saw the largest gain in Q4 in our Universe? It was Figs, which was up +70% in the quarter. This was due to strong Q3 results and a boost to the Co’s full-year 2025 revenue outlook to 7% growth from low-single digits. Roth Capital lifted its target to $12/shr from $10 and BTIG initiated with a Buy, highlighting a resilient brand, encouraging demand trends in U.S. healthcare apparel and a debt free balance sheet. Additionally, FIGS expanded its partnership with Team USA and will outfit ~150 healthcare professionals at the 2026 Olympic and Paralympic Winter Games (link). Following Figs, Globalstar traded up +68%, and The RealReal, traded up +48%, rounding out the Top 3 best performers in Q4.

Which stock had the toughest Q4? It was CoreWeave, which fell -48% in the period, followed by Duolingo, down -46% and Hims & Hers, down -43%, to make up the Bottom 3 worst performers.

How did the “Magnificent 7” do in Q4? It was a mixed bag: Alphabet had particularly strong performance with a +29% rally, followed by Apple up +7% and Amazon up +5%; NVIDIA was stagnant this qtr, while Microsoft and Meta were down -7% and -10% respectively; Overall, Amazon was the only Mag 7 to have stronger performance in Q4 than in Q3

Key Takeaway From CES…“The ChatGPT Moment For Robotics Is Here”

Nvidia CEO Jensen Huang’s keynote kick-off at CES was a main focus this week, along with the myriads of interesting product updates that were unveiled at the event. To start, with all the recent debate about an AI bubble, Jensen alleviated some investor concerns by repeatedly citing strong demand and business dynamics…”demand for NVIDIA GPUs is skyrocketing”…“the amount of computation for pretraining, for post-training, for test-time scaling has exploded”…“the race is on for AI, everybody is trying to get to the next level, everybody is trying to get to the next frontier”…“all of these things are simultaneously happening”…etc. Importantly, Jensen also confirmed that its new Vera Rubin chip is now fully in production, which marks a meaningful cost and efficiency breakthrough for large-scale AI workloads.

Bigger picture, physical AI and robotics emerged as the clear standout themes from Jensen and the broader conference. Nvidia’s new Cosmos open models and frameworks are designed to accelerate the development of robots that can reason, adapt, and operate in unpredictable real-world environments. The “ChatGPT moment for robotics” is finally here per Jensen and the Co also released its open source Alpamayo model which enables AV AI to handle these diverse scenarios. “There is no question in my mind that [AVs] will be one of the largest robotics industries and Nvidia is helping the world build robotic systems.”

Lastly, Huang also declared that “we are at the beginning of a new industrial revolution” and that manufacturing is being revolutionized by physical AI, from design and simulation to production and operations. Caterpillar was in the spotlight in this area as well.

Aside from all of Nvidia’s updates, there were a slew of other new robots introduced across a multitude of manufacturers that caught our attention as well.

All in all, there was a lot to digest from the event, but please see below for what we found most interesting. Looking forward, we are only at the starting gate regarding physical AI and we expect this to be a major theme in 2026, and beyond.

-> Nvidia shares +0.5% in reaction after closing 2025 up +31%; Uber shares also traded up +7% (on the back of Nvidia’s Alpamayo model announcement)

Nvidia CEO Jensen Huang’s Positive Comments About Overall Compute Demand & Business Dynamics

- “The amount of computation necessary for AI is skyrocketing”

- ”Demand for NVIDIA GPUs is skyrocketing”

- And “it’s skyrocketing b/c models are increasing by a factor of 10, an order of a magnitude every single year”

- “The amount of computation for pretraining, for post-training, for test-time scaling has exploded”

- Test-time scaling causes the # of tokens to be generated to increase by 5x every single year

- Also, “the race is on for AI, everybody is trying to get to the next level, everybody is trying to get to the next frontier”

- “The faster you compute, the sooner you can get to the next level of the next frontier”

- “All of these things are simultaneously happening”

- “We should have a very good year”

- The Co also confirmed that Vera Rubin is in “full production” which is an important milestone for investors: Vera Rubin is the Co’s next generation AI chip which it says will cut the cost of running AI by 1/10th vs Nvidia’s Blackwell chip and Rubin can train certain large models using roughly 1/4 as many chips as Blackwell requires (link)

“The ChatGPT Moment For Robotics Is Here”…But The Physical World Is Diverse & Unpredictable

- Nvidia is very focused on accelerating the robot development lifecycle and along these lines annc’d new open models, frameworks and AI infrastructure for physical AI and, with global partners, unveiled robots for every industry

- The Co released new open models for robotics development: NVIDIA Cosmos open world foundation models bring “humanlike reasoning and world generation” to accelerate physical AI development and validation

- Cosmos Reason 2 is a new, leaderboard-topping reasoning VLM that helps robots and AI agents see, understand and interact w/ higher accuracy in the physical world

- NVIDIA Isaac GR00T N1.6 (an open reasoning vision language model) was purpose-built for humanoid robots and unlocks full body control…it uses NVIDIA Cosmos Reason for better reasoning and contextual understanding

- Cosmos Transfer 2.5 & Cosmos Predict 2.5 are leading models that generate large-scale synthetic videos across diverse environments and conditions

- Cosmos Reason 2 is a new, leaderboard-topping reasoning VLM that helps robots and AI agents see, understand and interact w/ higher accuracy in the physical world

- “Robotics is now the fastest-growing category on Hugging Face, where NVIDIA’s open models and datasets lead downloads among a surging open-source community”

- Lack of training data has been a gating factor for physical AI to take off as collecting real world training data is slow and costly and the videos available are not enough…

- …But this training can be done using synthetic data generation, that is grounded and conditioned by the laws of physics, and Nvidia can generate this data that can then be used to train the AI

- Cosmos is training AVs for the large tail and enables robots to handle any scenario

- Cosmos has been downloaded “millions” of times globally

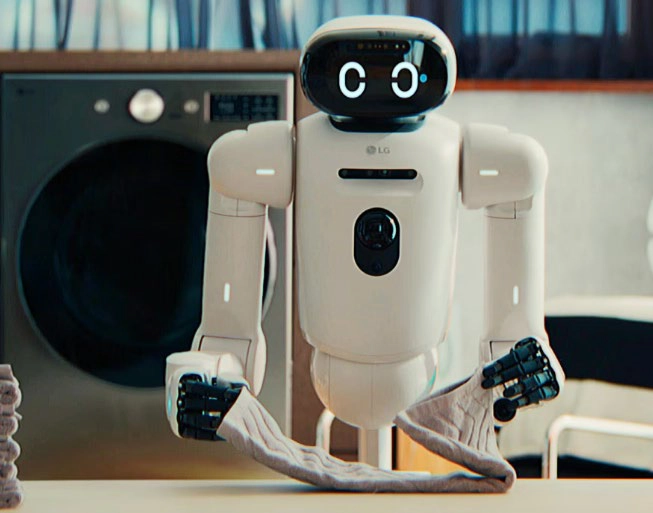

- Partners using NVIDIA robotics stack to debut new AI driven robots include Boston Dynamics, Caterpillar, Franka Robotics, Humanoid, LG Electronics and NEURA Robotics

- See quick 2min Nvidia video clip showing “The Breakthrough Moment for Physical AI”: YouTube Video

The Shift To Autonomous Vehicles Is At “An Inflection”

- Nvidia’s Huang also declared that AVs will be the 1st large scale mainstream physical AI market and it is now “fully here”…the “inflection” is now…”in the next 10 years, I’m fairly certain a very, very large percentage of the world’s cars will be autonomous or highly autonomous”

- The Co released open source Alpamayo model enables AV AI to also handle the long tail of scenarios

- Alpamayo is the world’s first thinking, reasoning AV AI: It takes sensor input & activates the steering wheel, brakes and acceleration: It also reasons about what action it is about to take which is critical when it comes to the long tail of scenarios

- Given that it is impossible to collect every single driving scenario…these long tails will be decomposed into “quite normal circumstances that the car knows how to deal with”

- Alpamayo is the world’s first thinking, reasoning AV AI: It takes sensor input & activates the steering wheel, brakes and acceleration: It also reasons about what action it is about to take which is critical when it comes to the long tail of scenarios

- Timing… the first AV car from Nvidia (Mercedes Benz CLA) is going to be on the road in Q1 in the US and then it goes to Europe in Q2; Then Asia in Q3 and Q4

- Huge focus on safety…the Mercedes Benz CLA just got rated by NCAAP as the world’s safest car: It is the only system that has every single line of code safety certified & has diversity and redundancy w/ running another AV stack at the same time

- They built the entire stack working with Mercedes but that entire stack is also open for the ecosystem

- “There is no question in my mind that [AVs] will be one of the largest robotics industries and Nvidia is helping the world build robotic systems”

-> Also at CES, Lucid in partnership with Uber & Nuro unveiled the Gravity robotaxi prototype for the 1st time, showcasing its advanced autonomous features and rider-focused in-cabin technology; Production of the Gravity robotaxis is expected to begin later in 2025 (link)

“We Are At The Beginning Of A New Industrial Revolution”…Manufacturing Is Being Revolutionized By Physical AI

- Huang also contended that “we are at the beginning of a new industrial revolution” and that manufacturing is being revolutionized by physical AI…from design and simulation to production and operations

- Along these lines, Caterpillar also had some high-profile demos and previewed five autonomous machine categories for construction…excavators, loaders, haul trucks, dozers, and compactors

- These machines integrate AI, machine learning, computer vision, and edge computing with sensors (LiDAR, radar, GPS, cameras), forming a digital nervous system for real-time situational awareness and autonomy

- The Co also unveiled its Cat AI Assistant, a conversational, multimodal AI agent which is accessible via voice, text, image, or video and assists with maintenance, operational advice, safety, and scheduling using contextual data from the Helios platform

- The Cat AI Assistant will “go live” this qtr, w/ in-cab applications in final validation

Examples Of Other Notable Physical AI Announcements At CES That Stood Out To Us

- Arm Holdings intro’d a dedicated Physical AI division, integrating its robotics and automotive initiatives to address shared hardware and sensor needs across these sectors (link)

- LG Electronics presented CLOiD, a humanoid robot assistant under its “Zero Labor Home” vision, capable of physically manipulating household items (like folding laundry, handling dishes, and interacting with smart appliances) using its wheeled base, articulated arms, and Vision‑Language‑Action model (link)

- SwitchBot revealed the Onero H1, described as “the most accessible AI household robot”, w/ 22 degrees of freedom, a wheeled base, and an OmniSense vision‑language‑action system, it performs tasks like cooking, laundry, and window cleaning, and integrates with other smart devices (link)

- Boston Dynamics debuted a fully electric, commercially ready version of Atlas: It is an enterprise-grade humanoid robot for industrial tasks such as material handling and order fulfillment, featuring 56 degrees of freedom, 360° vision, tactile hands, ability to lift up to 110 pounds, & robust performance in a wide temperature range (link)

- Production of Atlas will begin immediately: All units are committed for 2026 with more customers to be added in 2027

- The Co also annc’d a partnership with Google DeepMind to integrate advanced foundation models for enhanced cognitive capabilities in Atlas

- Hyundai Motor Group, the majority shareholder, plans to deploy tens of thousands of Boston Dynamics robots in its manufacturing facilities

- Takway unveiled Sweekar, a palm-sized, Tamagotchi-like AI companion that learns your voice, develops a unique personality, and evolves through life stages before becoming fully autonomous (link)

- It is expected to cost ~ $100–$150 and the customizable virtual pet is designed to travel with you, entertain itself as it matures, and bring back stories from its own AI-driven “adventures”

- German Bionic unveiled Exia, a state-of-the-art robotic exoskeleton featuring up to 38 kg of dynamic lift support per movement, aimed at highly demanding physical tasks in logistics, production, and healthcare (link)

- Roborock, a Chinese robotic vacuum cleaner brand, unveiled a concept device with two legs that can climb stairs in people’s homes; No confirmed launch date, according to the company (link)

-> Per research out from Omdia this week, Humanoid robot makers in China accounted for the vast majority of the ~13k units shipped globally last yr; The number one producer was Chinese startup Shanghai AgiBot Innovation Technology Co. which shipped an est’d 5,168 robots in 2025; The industry’s global sales were up 4x+ y/y in 2025 and Omdia expects global humanoid robot shipments to reach 2.6mn units in 2035 (link)

Quick Hits On A Few Other Interesting Updates From CES

- Samsung unveiled the world’s largest micro RGB TV display … at 130-inches!: The R95H blends a gallery-inspired aesthetic (“floating window”) with integrated sound, powered by the Micro RGB AI Engine Pro, Color Booster Pro, HDR10+ ADVANCED, Glare Free tech, and Vision AI Companion offering voice control, live translation, AI-generated wallpapers, and compatibility with Microsoft Copilot and Perplexity (link / link)

- Amazon rolled out Alexa.com, bringing its AI assistant to the web with new features aimed at enhancing entertainment experiences

- Users can now receive personalized movie & TV recommendations, and ask Alexa to jump directly to specific scenes through natural language descriptions (link)

- Samsung rolled out its Odyssey 3D 6K glasses‑free gaming monitor: The 32-inch monitor is capable of displaying immersive 3D visuals for titles like Stellar Blade and Lies of P: Overture (link)

- Also if interested, see a handy TechCrunch article for a broader list of new tech and gadgets annc’d at CES… CLICK HERE

Holiday Spending Wrap…While Y/Y Growth Rates Slowed Vs 2024, Consumer’s Spending Resilience Remains On Track

With the close of the holiday season, Adobe, Visa, Mastercard and Salesforce all released data on spending trends during the period. Overall spending growth y/y was solid, though in most cases showed decelerating growth vs the year prior. While the datasets are not all apples to apples in terms of the dates analyzed, spending growth rates for the US holiday season ranged from +3.9% y/y (Visa) to +6.8% y/y (Adobe).

Data showed that peak discounts were slightly higher than last year’s level (the largest increase was in apparel) but in many cases, that pushed consumers to trade up. We’d also call out stats on AI driven shopping. Adobe data showed an almost 700% y/y increase in the traffic to retail sites from gen AI tools (though this compares to +1300% y/y in 2024) and Salesforce’s analysis indicated that AI drove 20% of global retail sales, fueling $262bn in revenue through personalized recommendations (both accelerated from 19% and $229bn, respectively, in 2024). Lastly, while returns post-Christmas were up, the overall return rate for the season was still down. With that said, it is expected to remain elevated in January.

In terms of what is selling, electronics and apparel stood out.

See below for more details.

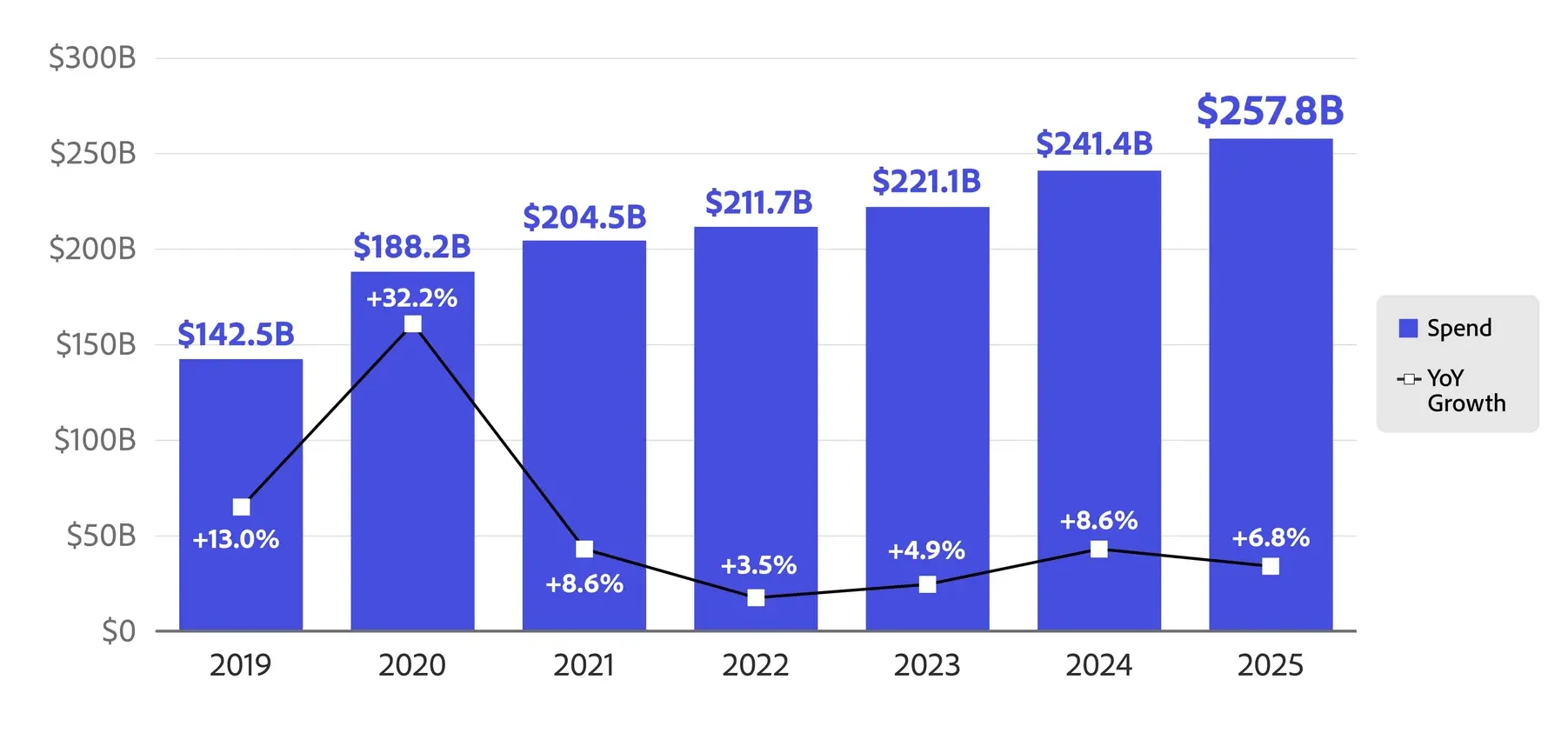

Adobe 2025 US Holiday Shopping Recap Points To A Strong +6.8% y/y Growth

- Overall, US shoppers spent a record $257.8bn, up a solid +6.8% y/y, through the holiday season of Nov 1. to Dec 31, 2025 but it did reflect a decel from +8.7% y/y in 2024 (link/link)

- Of the $257.8bn spent, over half (54%) was driven by three categories… electronics ($59.8bn, up +8.2% y/y vs +8.8% in 2024), apparel ($49.0bn, up +7.4% y/y vs +9.9% y/y in 2024) and furniture ($31.1bn, up +6.6% y/y vs +6.8% y/y in 2024)

- Spending was more spread out, as during 25 days of the season, consumers spent more than $4bn in a single day, which is a significant jump from 15 days in 2024 & 11 days in 2023

- Mobile shopping hit a new milestone, with most online transactions (56.4%) taking place through a smartphone this season (up from 54.5% in 2024)

- Cyber Week brought in $44.2bn online overall, up +7.7% y/y (also a decel from +8.2% y/y in 2024)

- Cyber Monday remained the biggest e-commerce day of the season (and year), driving $14.25bn in online spend, up +7.1% y/y (a slight decel from +7.3% y/y in 2024)

- Cyber Monday growth was outpaced by Black Friday spend of $11.8bn, up +9.1% y/y (vs +10.2% y/y in 2024) as consumers embraced earlier deals

- On Thanksgiving Day, consumers spent $6.4bn online, up +5.3% y/y (vs +8.8% y/y in 2024)

- Competitive discounts pushed consumers to “trade up”

- In electronics, discounts peaked at 30.9% off listed price (slightly higher than the 30.1% peak discount in 2024); The largest increase in peak discounts were in apparel

- Toys at 29.6% (up vs. 28%)

- Apparel at 25.1% (up vs. 23.2%)

- Televisions at 24.3% (up vs. 24.2%)

- Computers at 23.4% (up vs. 22.8%)

- Sporting Goods at 20.3% (up vs. 19.5%)

- Appliances at 20.2% (up vs. 19.2%)

- Furniture at 18.8% (down vs. 19%)

- Deals this season also drove consumers to purchase higher-ticket items in categories such as electronics, sporting goods and appliances

- Within categories, peak discounts were 56% in electronics, 55% in sporting goods, 38% in appliances, 34% in personal care products and 29% in tools

- In electronics, discounts peaked at 30.9% off listed price (slightly higher than the 30.1% peak discount in 2024); The largest increase in peak discounts were in apparel

- There was a huge increase in the traffic to retail sites from gen AI tools…it incr’d by +693% y/y (vs +1300% y/y in 2024)

- Usage of BNPL hit an all-time high at $20bn of online spending, up +9.8% y/y and representing $1.8bn more than last season (accel from +9.6% y/y in 2024

- 82.2% of BNPL purchases this season were for smartphones (79% in 2024)

- A few other interesting holiday insights from the season include –

- While returns post-Christmas were up, the overall return rate for the season was down…with that said, it is expected to tick up in Jan

- Returns were down -1.2% y/y from Nov 1 – Dec 31

- In the days following Christmas (Dec. 26 to Dec. 31), returns were up +4.7%, and 1 out of every 7 returns this season happened during this period

- 38.8% of returns happened on a mobile device, while 56.4% of overall online spend was driven by mobile

- Adobe predicts return levels will remain elevated in the first two weeks of Jan by 8-15%

- Social media was the standout this season, with its share of revenue coming in at 4.6%, up a significant +40.3% y/y (2024: 3.3% share, up +5.4% y/y)

- In affiliates and partners, which includes social media influencers, revenue share came in at 20.4%, up +15.9% y/y (2024: 17.6% share, up +6% y/y)

- While returns post-Christmas were up, the overall return rate for the season was down…with that said, it is expected to tick up in Jan

Visa & Mastercard’s Season Wraps Cite US Holiday Shopping Rising In The Range Of +3.9% to +4.2% y/y

- Data for both companies were for slightly different periods so they are not apples to apples, but US holiday spend numbers incr’d from +3.9% y/y (Mastercard) to +4.2% y/y (Visa)

- Visa analyzed US retail sales activity over a seven-week period beginning Nov 1 (ending ~Dec 19th) and found holiday spending to rise +4.2% y/y (a decel from +4.8% y/y in 2024) (link/link)

- In‑store sales led seasonal spending, capturing 73% of total spending (77% in 2024)

- E‑commerce total sales rose +7.8% y/y (accel from +7.1% y/y in 2024)

- Markets outside the U.S. saw seasonal spending rise, with Australia (+5.0%), Canada (+4.4%), South Africa (+7.9%) and U.K. (+3.6%)

- U.S. seasonal spending snapshots by category include –

- Electronics sales emerged as a top holiday category, growing at +5.8% y/y (accel from +4.2% y/y in 2024)

- Clothing and accessories sales climbed +5.3% y/y (accel from +5% y/y in 2024)

- Furniture and home furnishing sales rose +0.8%, reflecting “consistent seasonal demand”

- Building materials and garden equipment sales decreased by -1.0% (decel from an increase of +4.7% y/y in 2024)

- Mastercard calculated that U.S. spending between Nov 1st – Dec 21st grew +3.9% y/y (accel from +3.8% y/y in 2024) (link/link)

- Online sales rose +7.4% y/y, while in-store sales grew +2.9% y/y

- Apparel specific online sales were up +8.5% y/y and in-store sales also rose +7.0%

- Segment specific spending:

- Apparel spending climbed +7.8% y/y (accel from +3.6% y/y in 2024)

- Jewelry also rose by +1.6% (decel from +3.7% y/y in 2024)

- Restaurant spending grew +5.2% y/y (decel from +6.3% y/y in 2024)

- Online sales rose +7.4% y/y, while in-store sales grew +2.9% y/y

Other Notable Stats / Trends During The 2025 Holiday Season & Beyond

- Salesforce reported record global online spend this season (link/link/link)

- Their data shows that online sales hit $1.29tr globally and $294bn in the US (both up from $1.2tr globally and $282bn in US for 2024)

- Amid higher average selling prices, sales growth hit +7% y/y globally and +4% y/y in the US (compared to +3% globally y/y and +4% y/y in the US in 2024)

- Shoppers showed resilience at the end of the season with a +12% y/y global increase in sales (9% in the US) in the last two weeks of Dec

- AI drove 20% of all retail sales and fueled $262bn in rev through personalized recommendations (both accelerated from 19% and $229bn in 2024)

- Cos that deployed their own AI agents, like Pandora, SharkNinja, and Funko, saw a 59% higher growth rate, averaging a +6.2% y/y sales increase versus +3.9% y/y

- Shoppers used retailers’ AI and agents for customer service 126% more during the holiday rush than in the two months prior

- Lastly… consumer purchasing power trended toward the positive –

- The average selling price (ASP) incr’d +7% y/y both worldwide and in the US

- Order volumes this season moderately incr’d 3% globally and 1% in the U.S. compared with last year

- Price hikes are expected to be on the way given tariffs impacts (link)

- In McKinsey’s State of Fashion 2026 report, ~71% of fashion executivessaid that they are planning to increase their prices in 2026

- 26% of non-luxury brands expect to raise prices by more than 5%, while only 18% of luxury brands reported the same

- Reasons for the increases?

- Tariffs continue to affect their supply chains and those costs will soon be passed on to customers

- Data provided to Glossy by Akeneo found that 91% of customers have already noticed price increases and that 83% want clarity

- In McKinsey’s State of Fashion 2026 report, ~71% of fashion executivessaid that they are planning to increase their prices in 2026

Major AI Developments Across Healthcare & Music + Even More Capital Raises

The “internet doctor” is evolving. Millions of people already turn to ChatGPT for health and wellness questions, and OpenAI is formalizing those conversations with the launch of ChatGPT Health. The new offering helps users make sense of medical information, prepare for doctor visits, and track health patterns over time, including through integration with popular wellness apps like Apple Health and MyFitnessPal. ChatGPT Health is designed to provide guidance in a physician-like way, communicating clearly without oversimplifying, but it is NOT meant to replace professional care. And given the sensitive nature of health information, it comes with additional privacy protections so that no medical data is used to train ChatGPT’s models.

And healthcare isn’t the only sector that AI is further penetrating this week. In music, NVIDIA and Universal Music Group announced a partnership to apply AI to music discovery, creation, and fan engagement, emphasizing artist involvement, attribution, and rights protection. The collaboration will expand NVIDIA’s Music Flamingo model and launch an artist incubator to co-develop AI tools with songwriters, producers, and performers. And at the same time, major AI players continue raising large rounds to fund compute, research, and product development, including xAI, which just raised an upsized $20bn Series E round and Anthropic, which is reportedly raising $10bn at a $350bn valuation.

See below for more on all of the above.

OpenAI Enters The Health Space With The Introduction Of ChatGPT Health (link/link)

- Health is “already one of the most common ways people use ChatGPT”

- 230mn+ people globally ask health & wellness related questions on ChatGPT everyweek

- >5% of all ChatGPT messages globally are about healthcare, averaging billions of messages each week

- What can ChatGPT Health be used for?

- Understanding recent test results

- Preparing for appointments with a doctor

- Getting advice on how to approach diet and workout routine

- Understanding the tradeoffs of different insurance options based on individual healthcare patterns

- Meant to be personalized to the user: Users can securely connect their medical records and wellness apps to ground conversations in their own health information, so responses are more relevant and useful to the individual

- The platform can connect wellness apps like Apple Health, Function, and MyFitnessPal

- The platform was developed alongside physicians: Worked w/ 260+ physicians who have practiced in 60 countries and across “dozens” of specialties

- Built w/ addtl, layered protections designed specifically for health: Conversations in ChatGPT Health would be stored separately to other chats and would not be used to train OpenAI’s AI tools

- If a user starts a health-related conversation in ChatGPT, it will suggest moving into Health for addtl protections

- When helpful, ChatGPT may use context from non-Health chats (i.e., a recent move or lifestyle change) to make a health conversation more relevant

- BUT Health information and memories never flow back into non-Health chats and conversations outside of Health can’t access files, conversations, or memories created within Health

- Designed to “support, not replace”, medical care: NOT intended to be used for “diagnosis or treatment”

- Meant to “navigate everyday questions and understand patterns over time – not just moments of illness – so you can feel more informed and prepared for important medical conversations”

- Available on waitlist: For users with ChatGPT Free, Go, Plus, and Pro plans outside of the European Economic Area, Switzerland, and the UK are eligible

- Currently providing access to a “small group” of early users to learn and continue refining the experience

- As they make improvements, the Co will expand access and make Health available to all users on web and iOS “in the coming weeks”

AI Is Being Incorporated Further Into Music…UMG Signs A New AI Deal With NVIDIA To Build “Responsible AI” For Music (link)

- What is the partnership about? It is meant to “pioneer responsible AI for music discovery, creation, and engagement leveraging NVIDIA AI infrastructure and UMG’s industry-leading music catalog”

- Will undertake “collaborative” R&D to promote shared objectives of “advancing human music creation and rightsholder compensation”

- Exploring “new avenues to enrich music experiences by utilizing AI to elevate discovery, engagement and consumption beyond current constructs of search and personalization”

- Expanding the NVIDIA Music Flamingo model to enable deeper, more intuitive music discovery

- Built on NVIDIA’s Audio Flamingo architecture, the model analyzes full-length tracks to understand harmony, structure, timbre, lyrics, and cultural context

- Moves beyond basic tagging and genre classification to deliver human-like interpretation of songs

- Outperforms leading models across benchmarks in music captioning, instrument recognition, and multilingual lyric transcription, making discovery more personal and meaningful

- Empowering artists with creation tools: Will launch an artist incubator to co-develop AI creation tools with artists, songwriters, and producers

- Pursuing new approaches to leverage AI to protect artists’ work and ensure proper attribution of music-based content

More Capital Raises Across The Major AI Players

- xAI raises $20bn Series E at an undisclosed valuation (link)

- The Co completed its upsized Series E funding round, exceeding the $15bn targeted round size, and raised $20bn

- Investors participating in the round include Valor Equity Partners, Stepstone Group, Fidelity, Qatar Investment Authority, MGX and Baron Capital Group, “amongst other key partners”

- Strategic investors in the round include NVIDIA and Cisco Investments, who continue to support xAI in “rapidly scaling” its compute infrastructure and buildout of the largest GPU clusters in the world

- What will the financing be used for? To accelerate their “world-leading” infrastructure buildout, enable the “rapid development and deployment of transformative AI products reaching billions of users”, and fuel “groundbreaking” research advancing xAI’s core mission of understanding the Universe

- xAI did not disclose the valuation level of the funding round

- Anthropic is said to be in talks to raise $10bn at a $350bn valn (link/link)

- This is a big jump in valn: It follows a $13bn investment in Sept that valued the Co at $183bn

- This latest round is reportedly expected to close in the coming weeks

- Investors: GIC and Coatue reportedly plan to lead the new financing; MSFT and NVDA, which previously said they will invest up to a combined $15bn in Anthropic, are also expected to participate in the new round

- This comes ahead of potential IPO, as Anthropic is expected to go public this yr

- As a reminder, Anthropic is expected to break even for the first time in 2028, putting it on track to turn a profit quicker than OpenAI, which is expected to turn a profit in 2030, per The Wall Street Journal (link)

- This is a big jump in valn: It follows a $13bn investment in Sept that valued the Co at $183bn

-> For some context, globally, the magnitude of total AI investment hit $275bn in 2025, according to PitchBook data, doubling the amount invested in 2024 (link)

Live Sports Cont’d To Reign Supreme on US Screens In 2025

2025 was another year that proved that live sports are still king of the US screen. Nielsen’s new methodology, which expanded to include out-of-home measurement and incorporated big-data components, raised the threshold for the year’s most-watched broadcasts and is not apples to apples with previous viewership numbers but the trends remain intact. Sports accounted for NEARLY ALL of the Top 100 programs, led by the NFL. College football, the Kentucky Derby, and other marquee events contributed to sports’ overwhelming presence, while scripted shows and political programming made up only a handful of entries.

In line with that dominance, the NFL saw its highest viewership in more than 35 years across broadcast and streaming platforms in 2025. CBS, Fox, ESPN, Amazon, and Netflix all posted some of their strongest numbers, with marquee games driving massive audiences. And advertisers have certainly taken notice. NBCUniversal also announced this week that it sold out its advertising inventory for the 2026 Winter Olympics well in advance of the games starting next month, with over 100 new advertisers participating, setting the record for the highest-grossing Winter Olympics of all time.

See below for more on sports’ continuing ability to draw the largest audiences and ad dollars.

The NFL Once Again Dominates US B-Cast TV In 2025

- First note that Nielsen changed the way it measures ratings this yr to include both a big data component and out-of-home viewing(link)

- Because of this, viewership totals were higher across the board and the minimum audience needed to crack the Top 100 jumped higher

- 2023 cutoff: ~15.0mn viewers

- Current cutoff: ~17.4mn viewers

- If you applied the new measurement rules to 2023, 27 broadcasts that made the list back then wouldn’t qualify today

- Because of this, viewership totals were higher across the board and the minimum audience needed to crack the Top 100 jumped higher

- While some of the ratings gains can be attributed to those changes, the NFL is still TV’s biggest audience driver

- The NFL accounted for 83 of the most-watched TV broadcasts in 2025

- That’s its second-best year ever, only behind 2023 (93 entries)

- Which teams appeared the most on the list?

- Kansas City Chiefs appeared 18 times in the Top 100 most-watched broadcasts

- Philadelphia Eagles had 14 appearances

- Dallas Cowboys had 13

- All football (including college) accounted for 90 of the Top 100

- All sports accounted for 95 of the Top 100

- Kentucky Derby returned to the Top 100 after a 3-yr absence with nearly 18mn viewers (~1mn of which came from streaming)

- Political programming collapsed without an election yr…went from 16 spots in 2024 → just 3 this yr

- Only other notable non-sports events this yr were the Macy’s Thanksgiving Day Parade + The Oscars

- The NFL accounted for 83 of the most-watched TV broadcasts in 2025

- What sports didn’t make the list?

- NBA Finals: Missed the Top 100 despite a Game 7 with 16.61mn viewers.

- This marks the 6th straight yr the NBA Finals failed to place

- Women’s college basketball: Couldn’t repeat last year’s Top 100 success

- NBA Finals: Missed the Top 100 despite a Game 7 with 16.61mn viewers.

- Which networks appeared the most on the list?

- Fox: 26 appearances

- NBC: 23

- CBS: 22

- ESPN + ABC (Disney): 19 combined

Click HERE to see the full list of Top 100 Most-Watched US Telecasts of 2025

Additional Engagement Stats Published This Week…The NFL Saw Its Highest Viewership In 35+ Years (link/link)

- The NFL finished the 2025 regular season with a per-game viewership avg of 18.7mn, up +10% y/y

- The best viewership total since 1989, and the second-best figure on record

- Amazon saw the highest viewership levels in the 20-yr history of Thursday Night Football on any network

- Generated a per-game viewership average of 15.33mn, up +16% y/y from last yr

- CBS had its best NFL regular season ever

- Avging 21.3mn for all its games, up +11% y/y

- Set a regular-season NFL record of 57mn+ viewers for a Thanksgiving game b/w the Chiefs and Cowboys

- The late Sunday afternoon NFL window on CBS also averaged 25.8mn viewers, more than any program on U.S. television

- ESPN posted its second-best season in 20 yrs airing Monday Night Football

- Avged 16.5mn viewers when including all of 23 NFL games, up +10% y/y

- Fox saw its highest viewership numbers since 2015

- The network averaged 19.6mn viewers per game for all of its NFL coverage, up +6% y/y

- Fox NFL Sunday also finished as the most-watched NFL pregame show for the 32nd straight year, avging 4.4mn viewers

- Netflix set a league streaming record in its second year with a Christmas doubleheader, avging 27.5mn viewers for a late-afternoon game between the Lions and Vikings

Advertisers Continue To Push Ad Dollars Towards Sports

- NBCUniversal sells out advertising inventory for the upcoming 2026 Winter Olympics (link/link)

- It sold out a month before the Games start in early Feb: This is the 1st time in Co’s history that “we are officially sold out of our inventory this far in advance”

- 100+ new advertisers signed on

- This sets the record for being the highest grossing Winter Olympics of all times, as well as the biggest broadcast and digital rev earner in Winter Olympics history

- The Games kick off a packed sports broadcasting schedule for NBCU in Feb, which also includes the 60th Super Bowl and the NBA’s All‑Star weekend

- NBCU said that the NBA All Star Game has also sold out, and it previously announced in Sept that the Super Bowl had sold out of spots

The Streaming & Connectivity Sectors Already See Some +/- Pricing Adjustments To Start The Year

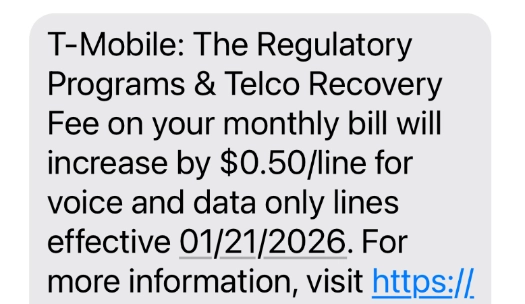

As 2026 begins, the cost of staying connected and entertained is already on the move in certain markets, driven by a mix of new taxes and pricing adjustments. On the tax front, Maine joined the club of states (~30) that have implemented incremental taxes on digital streaming subscriptions, which are being passed along to subscribers. We certainly would not be surprised to see more states follow suit looking ahead. Also, T-Mobile is now informing its subscribers (including us via a text tonight!) that it is passing along a “Regulatory Programs & Telco Recovery” fee starting Jan 21st (which follows a similar increase last year). Also on the price increase side, DirecTV is pushing through another hike on legacy bundles.

At the same time, T-Mobile is also leaning into value with a new long-term price-guaranteed plan…keeping competition in the wireless sector at play.

More details are below.

Streaming Will Be More Expensive In 2026 Given New Taxes

- Starting Jan 1, 2026, Maine residents were hit with an additional charge on their monthly bills from streaming platforms such as Netflix, Hulu, Disney+, Spotify, and similar services (link)

- The state’s 5% sales tax now applies to these digital subscribers, along with podcasts, audiobooks, ringtones, and other online audio and video content

- This expansion brings streaming services in line with traditional cable and satellite TV

- Previously, streaming subs escaped the general sales tax because they involved impermanent electronic transfers rather than permanent downloads or physical products

- The change aligns Maine with more than 30 other states that already tax digital streaming

- The policy stems from a $320mn supplemental budget package approved by the Maine Legislature and signed into law in June 2025

- This addressed funding needs including investments in programs such as MaineCare, nursing home rate reforms, mental health resources, and support for higher education

- Alongside the streaming tax, the supplemental budget repealed the 6% Service Provider Tax previously applied to cable and telecom services

- This repeal shifts those services under the standard 5.5% general sales tax, effectively reducing the burden on providers

- Revenue projections indicate the streaming tax will generate ~$5mn in additional funds during FY2026, which runs through June 30

- This figure is expected to grow in subsequent years, reaching around $12.5mn annually in the near term and climbing to $14.3mn by 2029

- Some estimates suggest the long-term annual yield could stabilize near $12mn or higher

DirectTV & T-Mobile Raise Prices While T-Mobile Both Launches A Value Plan & Increases Fees

- DirecTV annc’d price increases this week for some users across its bundled channels in the US (link)

- It last raised prices for all users 2 months ago in Nov 2025 (when prices rose as much as $11 per month, while add-on services saw rises of $5)

- The increases will apply to ‘legacy’ clients which were not covered by last Nov’s price rises

- DirecTV’s Go Big plan: has extensive channel selection including sports and entertainment networks, and will see a monthly increase of as much as $10

- Its Choice plan: a mid-tier option will see a $9 monthly increase

- Other packages: Its Entertainment and Ultimate plans, also see price rises in the $9-10/mo range

- It will depend on regional variations and what’s included in the bundled services

- It last raised prices for all users 2 months ago in Nov 2025 (when prices rose as much as $11 per month, while add-on services saw rises of $5)

- T-Mobile gets more aggressive with the launch of Better Value (link/link)

- What is it? The new plan delivers the “best price”, with savings of over $1,000 vs. the Carriers and a 5-yr price guarantee

- Price: Available Jan 14, it starts at $140 a month for three lines with AutoPay, plus taxes and fees

- It also comes with a 5-year price guarantee on talk, text and data

- It’s available for new customers with three or more phone lines, switching at least two of those lines to T-Mobile

- And… existing customers with three or more lines that have been with the carrier for five or more years

- T-Mobile is increasing a fee that it already increased less than a year ago (link)

- The “Regulatory Programs & Telco Recovery” fee is described as “not a government tax” but is instead a fee “collected and retained by T-Mobile to help recover certain costs we have already incurred and continue to incur”

- Last yr, T-Mobile increased this fee by $0.50/line for both voice and mobile internet lines

- Now starting Jan 21, they will once again increase this fee by another $0.50 per line

- What are the new changes?

- Voice lines: $3.99 ($4.49 effective Jan 21, 2026) per line every month

- Mobile Internet lines: $1.60 ($2.10 effective Jan 21, 2026) per line every month

AV Launch Timelines Slip, While Complex Self-Driving Tech Proves Far Pricier Than Earlier Projected

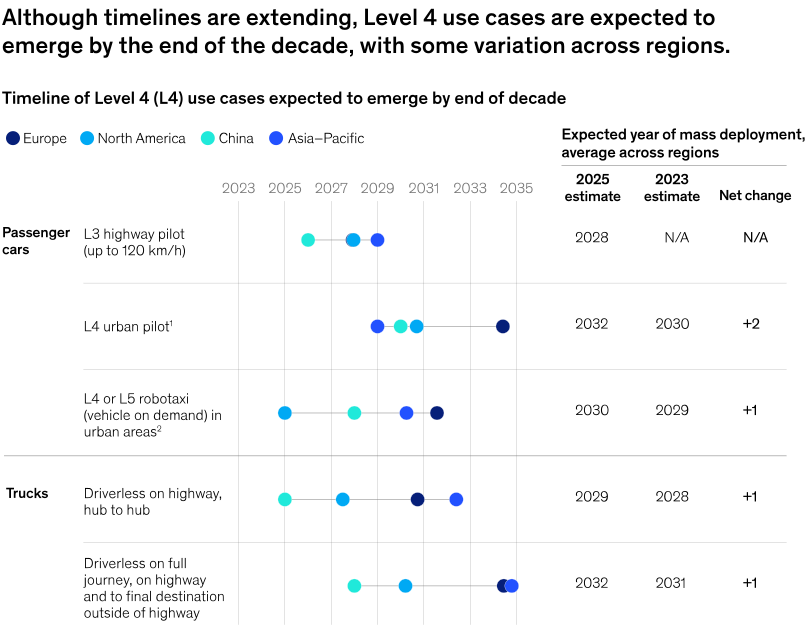

Despite steady technical progress, the path to fully autonomous vehicles is taking a little longer and costing more (and a lot more in some cases) than previously expected. Compared to the last McKinsey study in 2023, the firm is now pushing out adoption timelines across nearly every major AV use case by 1-2 years. Robo-taxis, private passenger vehicles, and autonomous trucking are all seeing delays as the industry moves from pilots to real-world commercialization.

At the same time, projections around the cost of more complex levels of autonomy were revised higher (especially in trucking applications). This data was based on a 2025 survey which included 91 “decision-makers” from around the globe, including start-ups and established Cos automotive, transportation, and software industries.

See below for more color and also see Theme #2 for other important updates and comments regarding AVs/robotaxi’s from CES (Nvidia CEO Jensen Huang says the inflection is now!). For the full McKinsey report, CLICK HERE.

The US & China Are Currently The Furthest Along With Respect To AVs…

- The sector has reached ~700k fully autonomous robo-taxi rides per week

- The US and China each see ~450k and ~250k commercial rides per week, respectively

- Europe has more than 35 AV pilots to date

…But The Expected Timeline For Full AV Adoption Was Slightly Pushed Out

- Adoption timelines for AVs have slipped by 1-2 yrs on avg, relative to McKinsey’s 2023 forecasts

- Global rollout of robo-taxis: Estimates pushed from 2029 to 2030

- L4 urban pilots for private passenger cars: Estimates pushed from 2030 to 2032

- Fully autonomous trucking: Estimates pushed from 2031 to 2032

- The availability of AVs is also expected to vary across geographies due to –

- Faster development cycles

- Agile commercial orgs and start-up cultures

- Regulatory support

- Funding availability

- A strong available AI and software base

- Built environments that are more conducive to AVs

- Larger market sizes

- Stronger willingness to test new tech at large scale

AND Anticipated Costs To Deploy More Advanced AVs (Esp For Trucking) Are Much Higher Than Early Expected

- The increase in expected cost to deploy vs the 2023 survey includes –

- L4 or L5 (vehicle on demand) in urban areas:

- 10% higher than previous projections

- Autonomous trucks (driverless on highway, hub to hub):

- 50% higher than previous projections

- Autonomous trucks (driverless on full journey, on highway and to final destination outside of highway):

- 60% higher than previous projections

- L4 or L5 (vehicle on demand) in urban areas:

- With robotaxis already scaling, these costs are likely more visible hence the lower adjustment vs autonomous trucking which is further from reaching commercial readiness

Grab Bag: 2025 Set A Record For Shareholder Activism Globally / Meta Announces Nuclear Energy Projects / iOS 26 Adoption Has Been Lagging

- 2025 set a record for global shareholder activism campaigns (link/link/link)

- 255 campaigns launched (up +5% y/y), which is the highest on record

- Eclipsed the previous record of 249 made in 2018

- Geographic breakdown – more than half of all global campaigns remained in the US

- US led with 141, which was up +23% y/y

- Japan hit a record 56, which made up half of global activity outside of the US

- Europe declined ~18% y/y to 39

- Activists won 120 board seats, driven by a record 52 US settlements

- CEO turnover hit an all-time high as 32 US CEOs resigned within a yr of an activist campaign, including 16% at S&P 500 companies

- That’s up from 27 CEOs that resigned in 2024, and 24 CEOs who left in 2023 after pressure from an activist

- M&A activism surged, esp in the back half of the yr

- M&A demands were present in 35% of H1 campaigns and 54% of H2 campaigns

- They were also included in 61% of Q4 campaigns, making it the busiest qtr for M&A demands in five yrs

- Who has been launching campaigns?

- Elliott Investment Management led activist firms…: Deploying $19bn across 18 new campaigns,

- Elliott also won 17 board seats over the yr

- …followed by Starboard: With $2bn in 11 campaigns

- 42 unique activists launched campaigns, with ~29% first-timers as an increasing number of investors are using activist tactics

- Elliott Investment Management led activist firms…: Deploying $19bn across 18 new campaigns,

- 255 campaigns launched (up +5% y/y), which is the highest on record

- Meta announces 6.6 GW of nuclear energy projects (link/link/link): Signed agreements w/ Vistra, Oklo, and TerraPower

- The projects are expected to support up to 6.6 GW of new and existing clean energy by 2035

- Meta aims to see the first new reactors delivered as early as 2030 and 2032

- Projects are expected to provide “thousands” of construction jobs and “hundreds” of long-term operational jobs

- The announcements didn’t provide any specific funding information

- Not Meta’s first nuclear energy deal: Meta and Constellation signed a 20-yr deal last year for Meta to buy about 1.1 gigawatts of nuclear power from Constellation’s plant in Illinois

- And Meta isn’t the only tech giant backing nuclear –

- Google signed a deal with Kairos Power to buy power from a new fleet of advanced reactors to supply its data centers

- Amazon has partnered with Energy Northwest and Dominion Energy to develop nuclear

- Microsoft committed to a 20-year deal to restart Pennsylvania’s Three Mile Island plant

- The projects are expected to support up to 6.6 GW of new and existing clean energy by 2035

-> Vistra was up +10.5% on the back of the announcement, while Oklo was up +7.9% (TerraPower is privately held)

- Apple’s iOS 26 adoption trails past releases (link)…this is as per usage data published by StatCounter

- Only ~15-16% of active iPhones worldwide are running any version of iOS 26

- Original iOS 26.0 release accounts for ~1.1% of devices

- iOS 26.1 accounts for ~10.6% of devices

- iOS 26.2 accounts for ~4.6% of devices

- In contrast, 60%+ of iPhones tracked by StatCounter remain on iOS 18, with iOS 18.7 and iOS 18.6 alone representing a majority of active devices

- How does this compare historically? iOS 26 adoption appears to be running at less than one-quarter of the rate achieved by recent predecessors during the same post-release window

- ~63% of iPhones were running some version of iOS 18 over a similar time frame

- ~54% of iPhones were running some version of iOS 17 over a similar time frame

- 60%+ of iPhones were running some version of iOS 16 over a similar time frame

- What may be driving the slowdown?

- Unlike many previous releases, iOS 26 introduces Liquid Glass as a fundamental visual overhaul, and the redesign received mixed reviews

- Apple now continues to support older operating systems with security updates, allowing users to remain on iOS 18 without immediate pressure to update or forfeit critical patches

- Only ~15-16% of active iPhones worldwide are running any version of iOS 26

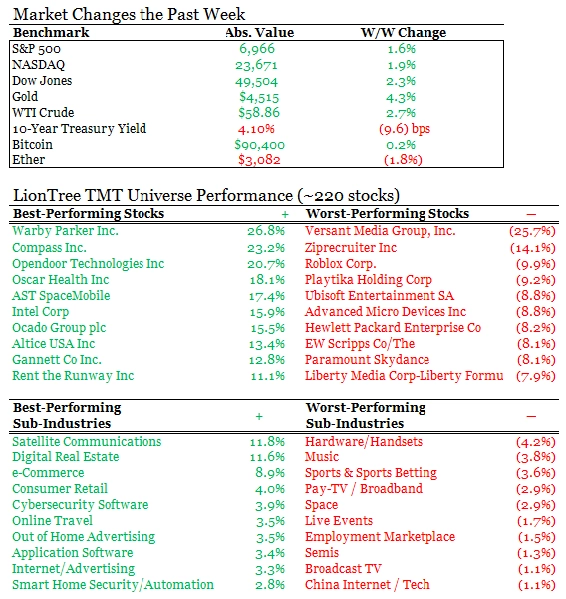

Stock Market Check

This Week's Other Curated News

Artificial Intelligence/Machine Learning

- Copilot annc’d Copilot Checkout & Brand Agents to turn conversations into conversions. Checkout enables frictionless purchases w/ merchants retaining data & control; early results show 53% more buys in 30 mins, 194% higher intent-to-purchase. Rollout starts in U.S. via PayPal, Stripe, Shopify. (Microsoft Ads)

- Gmail enters Gemini era, adding AI tools to manage inbox overload. New features: AI Overviews for instant answers & convo summaries; Help Me Write, Suggested Replies, and Proofread for polished emails; AI Inbox to prioritize VIPs & key to-dos. Most tools free; advanced options for Google AI Pro/Ultra subs. (Google)

- Chinese regulators are reviewing Meta’s $2bn acquisition of AI startup Manus, annc’d in Dec., for compliance and national security concerns. The probe, still early, could lead to penalties or conditions if violations arise. Manus, founded in China and now in Singapore, is known for AI agents handling tasks like resume screening and stock analysis. (Yahoo Finance)

- DeepSeek, a Chinese tech startup rivaling OpenAI, is driving AI adoption in developing nations, per Microsoft’s report. Global generative AI use hit 16.3% in Q4, up from 15.1%, but the gap between global north and south widens. DeepSeek’s free, open-source models and its R1 release in Jan. 2025 boosted uptake. . (Yahoo Finance)

- Microsoft annc’d agentic AI solutions to transform retail biz w/ intelligent automation across merchandising, mkts, store ops & fulfillment. Features include Copilot Checkout for frictionless purchases, Brand Agents & shopping templates for personalized experiences, and catalog enrichment for smarter discovery. (Microsoft News)

- Amazon’s “Shop Direct” program, annc’d in Feb, lets users buy items from other cos’ sites via a “Buy for Me” AI tool. Some retailers objected, saying products were scraped w/o consent, causing wrong or out-of-stock listings. Amazon claims it boosts sales and allows opt-outs. Buy for Me grew from 65K to 500K items since Nov., part of Amazon’s push into AI-driven e-commerce agents amid rising backlash. (CNBC)

- Business Insider, after removing AI-written essays in Aug, annc’d a pilot to publish AI-generated stories under “AI News Desk,” overseen by editors. CEO Peng’s May plan to go “all-in on AI” followed layoffs of ~20% staff, sparking fears among employees. Editor Heller said AI can’t replace reporters but offers speed for low-value stories. (Yahoo)

- Ray Dalio warned AI boom is in early bubble phase, noting US stocks lagged non- US equities and gold in 2025. Gold surged 60%, emerging mkts and FTSE 100 outperformed. Wall Street saw double-digit gains for 3rd straight yr, driven by AI-linked stocks. Dalio expects Fed to push rates down, inflating bubbles. (Reuters)

Audio/Music/Podcast

- Spotify annc’d two new Messages features: Listening activity and Request to Jam. Listening activity lets users share real-time tracks w/ friends, while Request to Jam enables remote shared sessions via Jam. Premium users can invite others; Free users can join when invited. Features roll out on iOS/Android in Messages-enabled mkts by early Feb., aiming to boost music discovery and social engagement. (Spotify)

- Spotify annc’d major updates to its Partner Program, marking its 1-yr milestone. Eligibility lowered to 1K engaged listeners, 2K hrs consumed, and 3 episodes. New tools launching Apr. enable creators to manage sponsorships w/ ease, track performance, and schedule edits. (Spotify)

Broadcast/Cable Networks

- Paramount Skydance Corp. aims to revive MTV and seeks music industry support. It’s in talks w/ major cos and top figures to acquire a stake in the cable network. Paramount has hired financial advisors to find a strategic partner willing to invest funds and provide assets like music rights or artist connections. (Bloomberg)

- Fox News led cable ratings for U.S. op capturing Venezuelan Pres. Maduro, drawing ~4.4mn viewers & 642K in 25-54 demo as Trump spoke. CNN hit 2.3mn viewers & 500K demo, ranking No.3 behind ESPN & Fox, marking best wknd since Biden ended reelection bid in Jul. 2024. (Yahoo News)

Cable/Pay-TV/Wireless

- US cable operators, led by Comcast, Charter & Optimum, captured 39% of US smartphone net adds in Q3’25, adding 945K lines. Though slightly down YoY, analysts expect mobile growth to accelerate in 2026 w/ Comcast’s aggressive plans & Charter-Cox merger by mid-yr. Cable’s convergence strategy—bundling broadband & mobile—remains strong vs telcos’ fiber push. (Light Reading)

- Cable One annc’d a deal to acquire full ownership of MBI for ~$1.3bn. Cable One, which already holds 45%, will pay $475mn–$495mn for the remaining 55%. MBI, a leading broadband svs provider w/~210,000 customers, will carry net debt of $845mn–$895mn post-close. Cravath advises Cable One on M&A, tax, financing, IP, antitrust & other matters in this transaction. (Cravath)

Capital Market Updates

- GameStop annc’d a $35bn pay plan for CEO Ryan Cohen, tied to boosting mkts cap to $100bn and achieving $10bn cumulative EBITDA. Cohen gets no salary, cash bonus or stock options upfront; package includes 171.5mn options at $20.66/share, vesting in nine tranches. Current mkts cap is $9.26bn, down 80% from 2021 highs. Shareholder approval expected Mar./Apr. (Reuters)

- JPMorgan’s asset mgmt unit has fully parted ways w/ proxy advisors for shareholder votes, replacing them w/ AI tool “Proxy IQ” to aggregate & analyze data from ~3,000 annual Co meetings. The move makes JPM the first major investment firm to drop such cos, amid criticism from Trump & Musk over advisors’ influence. (CNBC)

- US VC fundraising fell 35% in 2025 to $66bn, a 70% drop from 2022’s record, as cos stay private longer amid IPO drought and liquidity crunch. Capital is concentrating in top firms; Lightspeed raised $9bn in Dec., Founders Fund $4.6bn in Apr. AI funding hit $222bn, incl. OpenAI’s $40bn. Cash-heavy AI biz seek sovereign funds, family offices. (Yahoo Finance)

- Global bond sales hit a record ~$260bn to kick off 2026 as cos and govts in US, Europe, Asia tap mkts amid strong demand. Issuers rushed post-Dec. to lock funding ahead of earnings blackout. US high-grade supply topped $88bn this wk; deals include Broadcom ($4.5bn) and Orange SA ($6bn). (Yahoo Finance)

- Samsung is set to annc’d Q4 operating profit of 16.9 trln won ($11.7bn), up 160% YoY, driven by AI boom and tight chip supply. Analysts see potential >20 trln won profit as DDR5 DRAM prices surged 314% YoY; conventional DRAM expected to rise 55–60% this qtr. Shares jumped 125% last yr; outlook strong w/ HBM4 chips gaining traction vs rivals. (Reuters)

- Charter Comm Inc sold $3bn junk bonds Tues to pay off debt due through 2027 & repurchase equity. The 2-part deal, via 2 units of the major cable-TV provider, comes ahead of its planned acquisition of peer Cox Comm. Inc. The takeover is expected to close by end of Jun. (Bloomberg)

- Discord has confidentially filed for a US IPO, Bloomberg reported. The IPO mkts regained momentum in 2025 after a 3-yr slump, though volatility from tariffs, gov’t shutdown, and AI stock selloff tempered hopes. Deliberations are ongoing; Discord may not proceed. Founded in 2015, the Co offers voice, video & text chat for gamers, w/200mn+ monthly active users per Dec. statement. (Yahoo Finance)

Cloud/DataCenters/IT Infrastructure

- AMD annc’d MI440X chip for smaller corporate data centers at CES, aiming to challenge Nvidia’s AI hardware dominance. MI440X enables local hardware deployment, keeping data in-house. CEO Lisa Su also highlighted MI455X as AMD’s top-tier offering, claiming systems based on it deliver major capability leaps. (Bloomberg)

- Data centers linked to the largest US grid added $6.5bn to power procurement costs, fueling concerns over AI-driven energy inflation. Following PJM’s Dec. auction, data center costs hit $23.1bn for Jun. 2025–May 2028, per Monitoring Analytics. These fast-growing consumers made up 49% of the $47.2bn total from three auctions since mid-2024. (Bloomberg)

Crypto/Blockchain/web3/NFTs

- Crypto crime hit record highs in 2025, w/ illicit addresses receiving $154bn (+162% YoY), driven by a 694% surge in sanctioned entities’ activity. Stablecoins dominated 84% of illicit volume. DPRK hackers stole $2bn, incl. a $1.5bn Bybit hack, while Russia’s A7A5 token moved $93.3bn for sanctions evasion. Iran proxies laundered $2bn; CMLNs rose as major laundering hubs. (Chainalysis)

- Stablecoin transactions surged 72% in 2025 to $33T, per Artemis data. USDC led w/$18.3T, while USDT posted $13.3T despite topping mkt cap at $187bn. Growth followed GENIUS Act [Jul. 2025], enabling regulatory clarity. DeFi traders favor USDC for flexibility; USDT dominates daily biz use. Q4 vol hit $11T vs $8.8T in Q3. Bloomberg projects flows to reach $56T by 2030, though IMF warns of risks. (Yahoo Finance)

- Polymarket, the world’s largest prediction mkts platform, and Dow Jones annc’d an exclusive partnership. Polymarket’s real-time data will appear across WSJ, Barron’s, MarketWatch, and other Dow Jones properties via dedicated modules and print. New features include a custom earnings calendar w/ market-implied expectations. (Business Wire)

Cybersecurity/Security

- Wegmans Food Mkts annc’d use of facial recognition tech in select “elevated risk” stores to boost security. Data is limited to flagged individuals; no other biometrics collected. Images retained only as needed, not shared w/ third parties. Decisions based on law enforcement info & internal review. NYC stores comply w/ signage rules. (Chain Store Age)

- CrowdStrike annc’d, it will acquire SGNL to boost Falcon Next-Gen Identity Security for the AI era. Deal aims to deliver continuous, real-time access control for humans, NHIs & AI agents, eliminating legacy standing privileges. SGNL adds dynamic authorization across SaaS & cloud, enhancing PAM, ITDR & governance. Identity security mkts projected to grow from ~$29bn in 2025 to $56bn by 2029. (CrowdStrike)

Electric & Autonomous Vehicles

- Ford annc’d at CES that its AI voice assistant will launch in 2026 via Ford/Lincoln apps, expanding to cars in 2027. L3 autonomous driving will debut in 2028 on its UEV platform. Ford aims to cut costs by building core tech in-house, incl. smaller, efficient modules, not its own LLMs. Strategy shift follows EV sales slump, F-150 Lightning cancelation, and Argo AI shutdown. (The Verge)

Film/Studio/Content/IP/Talent

- James Cameron’s “Avatar: Fire and Ash” crossed $1bn in global box office, marking his 4th film to hit that milestone. The 3rd in the franchise, released during holidays, earned $306mn in U.S./Canada and $777.1mn internationally, per Disney. The series has grossed ~$6.35bn globally, w/ prior hits incl. “Avatar” ($2.9bn) and “Way of Water” ($2.3bn). (Reuters)

- Universal Music India annc’d a 30% stake in Excel Entertainment, valuing the Co at ~$290mn. The pact aims to boost Excel’s growth and UMG’s presence in India’s music-driven screen economy. UMG gains global rights to future soundtracks, launches an Excel music label, and becomes Excel’s exclusive publishing partner. (The Hollywood Reporter)

HealthTech/Wellness

- Utah annc’d a groundbreaking partnership w/ Doctronic AI to pilot autonomous prescription renewals for chronic conditions, marking the first state-approved program in the U.S. The initiative aims to improve medication compliance, reduce costs, and enhance patient access via Utah’s regulatory sandbox. (Utah Department of Commerce)

Live Entertainment/Theme Parks/Concerts/Experiential

- Live Nation & Ticketmaster filed a motion seeking dismissal of FTC’s Sept. lawsuit, calling it “egregious overreach.” FTC alleges cos violated BOTS Act by enabling scalpers to bypass limits, reselling tickets at steep markups in a multibn resale mkts. Cos argue law targets scalpers, not issuers, and Ticketmaster only intermediates resales. (Variety)

Macro Updates

- U.S. nonfarm productivity surged 4.9% annualized in Q3, fastest pace since 2023, driven by heavy AI investment lowering labor costs. This follows an adj 4.1% rise in Q2 vs forecasted 3%. GDP grew 4.3% while private job gains averaged 55K/month. Unit labor costs fell 1.9% after a 2.9% drop in Q2; up 1.2% YoY. (Reuters)

- U.S. trade deficit fell to $29.4bn in Oct., lowest since ’09, as Trump’s tariffs reshaped global trade. Imports dropped 3.2% to $331.4bn, exports rose 2.6% to $302bn. Gold drove ~90% of export rise; pharma imports collapsed post-tariff fears. Despite cont’d volatility, Jan.–Oct. deficit still up 7.7% YoY. Effective tariff rate hit 16%, highest since 1935. (The New York Times)

- U.S. job openings fell 303K to 7.146mn in Nov., a 14-month low, w/ hires down 253K to 5.115mn; layoffs remain low. Accommodation & food svs led declines, while retail & construction saw gains. Quits rose slightly; unemployment projected at 4.5% for Dec. Economists cite tariff uncertainty and AI integration as drivers of weak labor demand. (Reuters)

- Global mkts surged on AI optimism, but investors warn inflation risk is underappreciated. Heavy AI-driven data center spending, rising chip & power costs may keep U.S. CPI above Fed’s 2% target till 2027. Analysts expect tighter money as central banks halt cuts, hitting AI stocks. Deutsche Bank sees AI capex up to $4tn by 2030, fueling supply bottlenecks. (Reuters)

Media Conglomerates

- Comcast annc’d completion of Versant Media Group separation, effective Jan. 2, 2026. Versant begins trading on Nasdaq as VSNT today. Comcast shareholders received 1 Versant share for every 25 Comcast shares held as of Dec. 16, 2025. Goldman Sachs, Morgan Stanley & PJT Partners advised; Davis Polk served as legal counsel. (Business Wire)

Metaverse/AR & VR

- Meta annc’d major CES 2026 updates for its AI glasses. New teleprompter feature on Meta Ray-Ban Display enables seamless script delivery w/ Neural Band navigation. EMG handwriting lets users send msgs via finger gestures on any surface; early access limited to US. Pedestrian navigation expands to 32 cities. Int’l rollout paused due to high demand. (Meta)

- Xreal annc’d new 1S AR glasses & Neo dock at CES 2026, plus a collab w/ Asus for ROG Xreal R1 gaming glasses. These feature 240Hz refresh rate (double current 120Hz), 1080p micro-OLED panels, USB-C connectivity, and a ROG Control Dock w/ HDMI 2.0 & DisplayPort 1.4 for PC/console gamers. (The Verge)

Regulatory

- Alphabet, Meta, Netflix, Microsoft & Amazon will avoid strict EU digital rules despite telecom cos’ push. Under the draft Digital Networks Act, tech giants face a voluntary framework, not binding obligations, moderated by BEREC. DNA aims to boost EU competitiveness, harmonise spectrum allocation & guide fibre rollout. (Reuters)

- FDA annc’d new guidance to limit regulation of wearables and wellness software, classifying low-risk tools like fitness apps as non-medical if they avoid disease claims. Commissioner Makary stressed promoting such tech w/ safety oversight, citing AI symptom checks. Shares of Abbott, Medtronic, Dexcom rose 1–4%, Garmin ~3%. (Reuters)

- Google annc’d a $32bn bid to acquire cybersecurity firm Wiz Inc, now facing EU merger probe. EU set a Feb. 10 deadline to decide on approval or deeper review. Deal was notified Jan. 6 and already cleared by US & Saudi antitrust authorities. Acquisition aims to bolster Google’s cloud biz and security svs amid growing tech competition. (Bloomberg)

- A US judge rejected Amazon’s bid to dismiss a class-action lawsuit alleging price gouging during COVID-19. Consumers claim Amazon inflated prices on food, staples and let sellers charge “unlawful” rates, w/ hikes like 233% on Aleve, 1,044% on toilet paper, 1,523% on baking soda, 1,800% on masks. Judge found Amazon’s defense “unpersuasive.” (Reuters)

Social/Digital Media

- LinkedIn, now 22 yrs old, has evolved from a job-hunting site into a thriving biz platform. Rev surged to $17bn in 2025 from $7bn in 2020, w/ membership doubling to 1.3bn. Users spend more time due to real-name policy curbing toxicity, smarter discourse, and a gentler algorithm prioritizing constructive posts. (The Wall Street Journal)

Sports/Sports Betting

- FanDuel Sports Networks, under Main Street Sports Group, missed Jan NBA media rights payments, impacting 13 teams incl. Hawks, Heat & Spurs. Default notices loom w/15-day cure period. Main Street is in talks to sell ops to DAZN; failure may force shutdown post-NBA/NHL seasons. NBA plans contingencies for local broadcasts. (Cord Cutters News)

Tech Hardware

- Samsung Electronics Co. has cont’d delays for Ballie, a robot first annc’d at CES 2020. Despite CES 2025 demos and a Google Gemini AI partnership aiming for a late-summer 2025 launch, Ballie is absent from CES 2026. Samsung now calls it an “active innovation platform,” applying lessons to smart home devices and robot vacuums. (Bloomberg)

- Chinese firms dominated global humanoid robot shipments in 2025, accounting for most of ~13,000 units, per Omdia. Shanghai AgiBot led w/5,168 units, followed by Unitree & UBTech. Global sales quintupled YoY, driven by AI integration for complex tasks in manufacturing, logistics, healthcare & svs. Chinese models are cheaper ($6K–$14K) vs Tesla’s $20K–$30K. (MSN)

- Beijing asked Chinese tech cos to halt Nvidia H200 chip orders this wk, per The Information. Move aims to curb stockpiling as gov’t weighs access terms. Tensions over U.S.-China tech trade cont’d, w/ semiconductors as flashpoint. Nvidia CEO said demand in China strong; U.S. export licenses still pending. (Reuters)

- Foxconn, world’s largest contract electronics maker, annc’d record Q4 rev of T$2. 6028tn ($82.73bn), up 22.07% YoY, driven by AI demand. Growth beat LSEG SmartEstimate; USD basis rev rose 26.4%. Cloud/networking biz surged, while smart consumer electronics saw slight decline. Dec. rev hit T$862.86bn (+31.77%), a monthly record. (Reuters)

Video Games/Interactive Entertainment

- Ubisoft is shutting its Halifax studio, just 16 days after unionizing. Co claims closure is part of cos’ 24-mo effort to streamline ops, cut costs, and improve efficiency, not linked to unionization. 71 roles impacted; severance + career svs offered. Studio worked on Rainbow Six & Assassin’s Creed mobile titles. (Engadget)

- PlayStation annc’d the Hyperpop Collection for PS5 accessories, featuring 3 new designs—Techno Red, Remix Green, Rhythm Blue—w/ glossy black-to-neon gradients. DualSense controllers priced at $84.99; console covers at $74.99. (PlayStation)

- Roblox annc’d a new safety standard, requiring global users to complete facial age estimation to access chat. Images are deleted post-processing to ensure privacy. This move, part of Roblox’s vision for age-based communication, includes Persona ID verification and enhanced parental controls. (Roblox)

- Xbox Game Pass kicks off the new yr w/ fresh titles. Available now: Brews & Bastards, Little Nightmares Enhanced. Coming soon: Atomfall, Lost in Random: The Eternal Die, Rematch, Warhammer 40K: Space Marine, Final Fantasy, Star Wars Outlaws, My Little Pony: A Zephyr Heights Mystery, Resident Evil Village, MIO: Memories in Orbit. (Xbox)

Video Streaming

- RTL+ will be the exclusive bundle partner for HBO Max’s Germany, offering both svs under one subscription. The bundle combines RTL+ local hits like Neue Geschichten vom Pumuckl and UEFA Europa League w/ HBO Max titles incl. House of the Dragon & Game of Thrones. (RTL)

- Roku CEO Anthony Wood, speaking at CES, predicted a 100% AI-generated hit movie within 3 yrs, citing AI’s role in lowering content costs and boosting efficiency. Roku, processing 40% of streaming flows, posted $4bn rev in 2025. Wood detailed AI use in ops, ads, and recs, shifting to generative AI. (Variety)

- ‘Stranger Things 5’ finale pushed the show into Netflix’s all-time top 10 English series, ranking ninth w/106mn views in its first 13 wks. For Dec. 29–Jan. 4, it logged 31.3mn views and 325.6mn hrs watched. Theatrical screenings on Dec. 31–Jan. 1 added ~$20–25mn rev. (The Hollywood Reporter)

- Smart TVs dominate US streaming, w/61% of internet households using them as primary device, per Parks Associates CES® 2026 report. Samsung’s Tizen leads smart TV OS at 34%, though mkts remain fragmented w/competition from Roku, LG, Vizio. Roku tops overall CTV use at 28%, growing from 8% in 2020 to 18% in 2025. (Parks Associates)

- BBC Studios annc’d expansion of its US pay model to the BBC App, offering 1,600+ hrs of documentaries, global news, and premium features for $49.99/yr or $8.99/mo. Free users still access select news, radio svs, and newsletters. UK users unaffected. Launch follows 12% NA and 13% global growth, w/ Sept. hitting 77mn visitors. (BBC)

- Google annc’d new Gemini features for Google TV at CES 2026. Updates include visually rich responses w/ imagery, videos & real-time sports, “Deep dives” for complex topics, and photo tools like Photos Remix, Nano Banana & Veo for cinematic slideshows. Users can optimize settings via natural language. (Google)

- Netflix & WWE annc’d an expanded partnership, making Netflix the new US home for WWE’s library of Premium Live Events (pre-Sept 2025) incl. WrestleMania, SummerSlam & Royal Rumble, plus docs & originals. This builds on WWE’s Jan. 2025 debut on Netflix w/ Monday Night Raw in global Top 10. Launch aligns w/ Season 2 of WWE: Unreal on Jan. 20. (WWE)