First and foremost, it was nice to finally see an end to the TMT earnings storm, with the China Tech companies rounding out the season this week (see Theme #4). The markets were on fire, especially Nasdaq, which rallied +5.3% (NVIDIA up a huge +19%) along with the S&P 500 rising +3% as did the Russell 2000. This action breaks 4 weeks of declines. All macro data this week gave investors comfort that we are headed for a soft-landing scenario, which is course reversal from the recession fears that we have been contending with. Notably, as fast as the VIX spiked to fear levels, it fell back down to earth.

See below for the key focus themes in this edition (all links are clickable):

- Earnings Wrap: Companies Are Still Pushing Hard On The Bottom Line

- The NFL Isn’t The Only Big Sports Game In Town…The Paris Olympics Hits Record Viewership

- Investor Positioning… AT&T, Meta, & Liberty Global Are Hedge Fund “Hot Stocks”

- China Tech Contends With Weakening Domestic Spending Trends

- Grab-Bag: DraftKings Reverses Course On Surcharges/Another Suitor Reportedly Emerges For Paramount/Venu’s Launch Was Blocked By A Judge

Enjoy the weekend.

Best,

Leslie

Earnings Wrap: Companies Are Still Pushing Hard On The Bottom Line

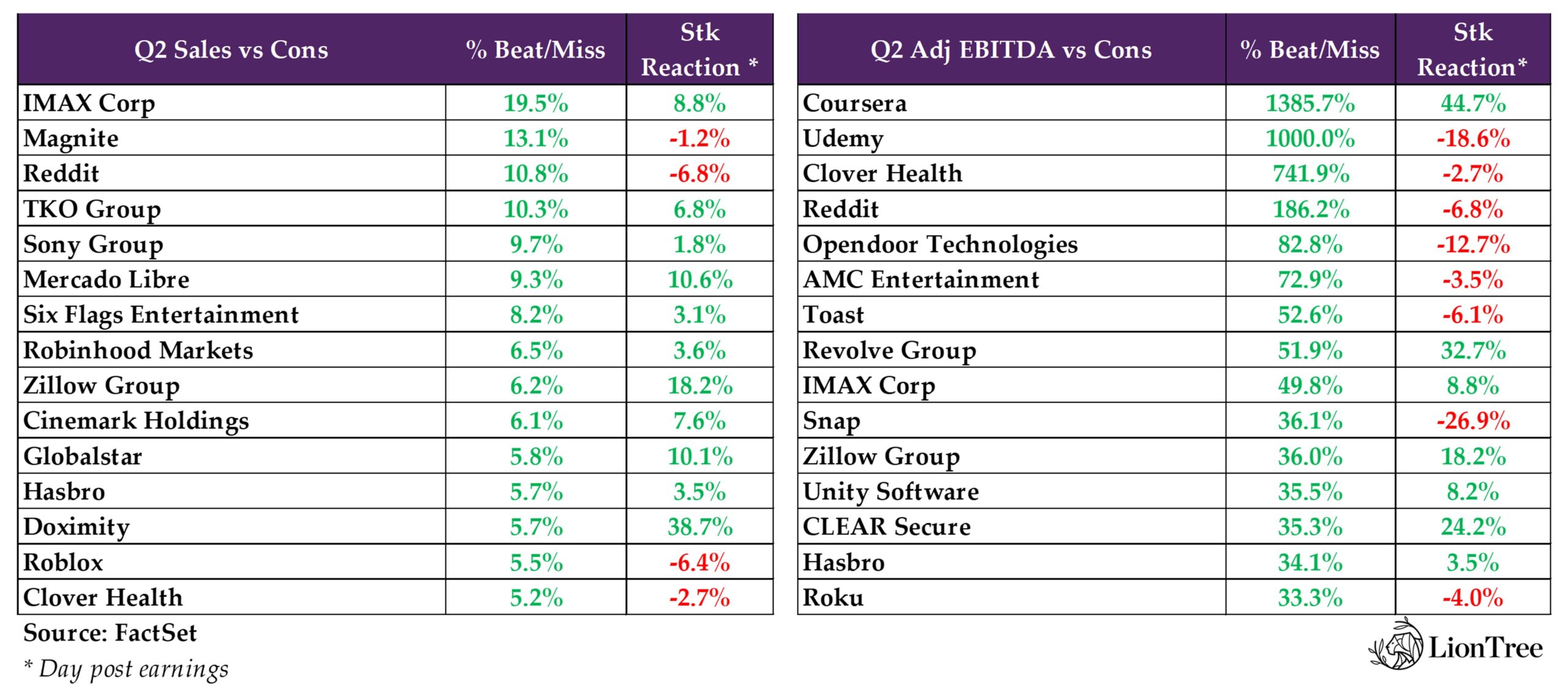

As we reached the end of a whirlwind Q2 earnings season, we took a look at Q2 results across our LionTree TMT and Consumer Universe of ~150 companies (30 sub-sectors) with $1bn+ market cap to highlight the highs and lows of the qtr.

Bigger picture, profitability upside was once again the name of the game, with a huge 82% of companies beating expectations on adj EBITDA (though this is about in-line with last qtr’s 83%). The magnitude of beats slightly tapered down, as 55% of those companies that reported upside to adj EBITDA relative to consensus estimates beat by double, triple, or quadruple-digits (vs 57% last qtr), but still made up the majority.

We also continued to see companies deliver revenue numbers that topped Wall Street estimates, with 70% of companies outperforming consensus on sales (a slight step down from 74% last qtr but still in the ballpark). However, the upside was more limited. Only 4% of the companies that beat estimates beat by 10%+ (vs 7% last qtr), while 20% of companies that beat on adj EBITDA actually missed on sales (up from 18% last qtr).

Digging into stock performance in reaction to results, 53% of stocks traded up post their prints, which is a slight step up from 51% last qtr and 52% in the qtr prior. What stood out more was that a higher number of stocks traded up double-digits in reaction to earnings vs last qtr at 18% vs 13%, respectively. On the flip-side, 10% of stocks traded down double-digits, which was consistent with the prior qtr.

Looking into company-specific performance, Coursera took the crown for best performer in response to earnings, jumping +44.7%, followed by Doximity and Klaviyo, up +38.7% and +33.4%, respectively, to round out the Top 3. On the other hand, while Snap was the best performer post earnings last qtr, it felt the most pain this qtr, falling -26.9% post earnings. Intel was the second worst-performer post earnings, declining -26.1%, followed by Mobileye falling -22.5%.

See below for more of our takeaways on the Q2 financial and stock performance of companies and sub-sectors within our LionTree Universe of TMT and Consumer stocks…

The Vast Majority Of Companies Continue To BEAT Expectations, Most Materially On Profitability

- Adj EBITDA – Of the companies in our LionTree Universe that report adj EBITDA, 82% beat on consensus adj EBITDA, and 55% had double, triple, or quadruple-digit beats

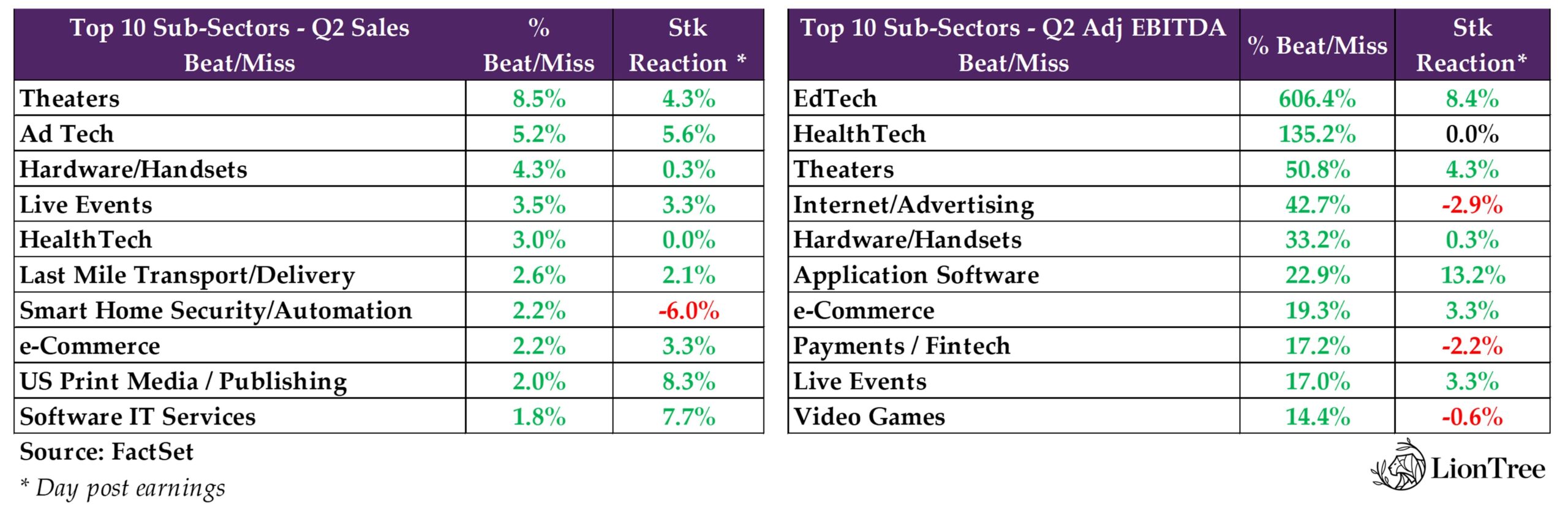

- EdTech had the highest adj EBITDA beat (for the fourth quarter in a row), with an avg beat of +606.4%; Similar to last qtr, the substantial avg beat was mostly driven by Coursera (+1385.7% beat; $10.4mn vs cons $0.7mn) and Udemy (+1000.0% beat; $5.5mn vs cons $0.5mn)

- Smaller beats from Duolingo (+24.6%) and Grand Canyon Education (+15.4%) also propped up the average

- HealthTech had an average beat of +135.2%, which was largely driven by Clover Health’s adj EBITDA beating expectations by +741.9% ($36.2mn vs cons $4.3mn)

- That being said, it was a strong qtr across the sector, with Teladoc beating by +20.5%, Doximity by +19.0%, Hims & Hers by +13.3%, Oscar Health by +12.5%, and GoodRx by +4.1%

- Theaters saw double-digit beats across the sector, which posted an avg beat of +50.8%, driven by AMC Entertainment (+72.9% beat), IMAX (49.8%), and Cinemark (+29.8%)

- EdTech had the highest adj EBITDA beat (for the fourth quarter in a row), with an avg beat of +606.4%; Similar to last qtr, the substantial avg beat was mostly driven by Coursera (+1385.7% beat; $10.4mn vs cons $0.7mn) and Udemy (+1000.0% beat; $5.5mn vs cons $0.5mn)

- Sales – Overall, 70% of the companies in our LionTree Universe beat consensus on sales, but only 4% of those companies beat expectations by double-digits or more

- Theaters had the highest avg sales beat in our Universe (vs second highest avg sales beat last qtr), topping cons by +8.5%, in aggregate, largely driven by IMAX (+19.5% beat; $89mn vs cons $74.5mn)

- Cinemark also beat by +6.1% beat, while AMC Entertainment came in in-line

- AdTech stocks had an aggregate sales beat of +5.2%, largely driven by Magnite (+13.1% beat; $162.9mn vs cons $144mn)

- Criteo SA and The Trade Desk also posted beats of +1.3% and +1.2%, respectively

- Hardware/Handsets stocks beat by +4.3%, on average, driven by Sony Group (+9.7% beat), Apple (+1.6%), and Sonos (+1.5%)

- Theaters had the highest avg sales beat in our Universe (vs second highest avg sales beat last qtr), topping cons by +8.5%, in aggregate, largely driven by IMAX (+19.5% beat; $89mn vs cons $74.5mn)

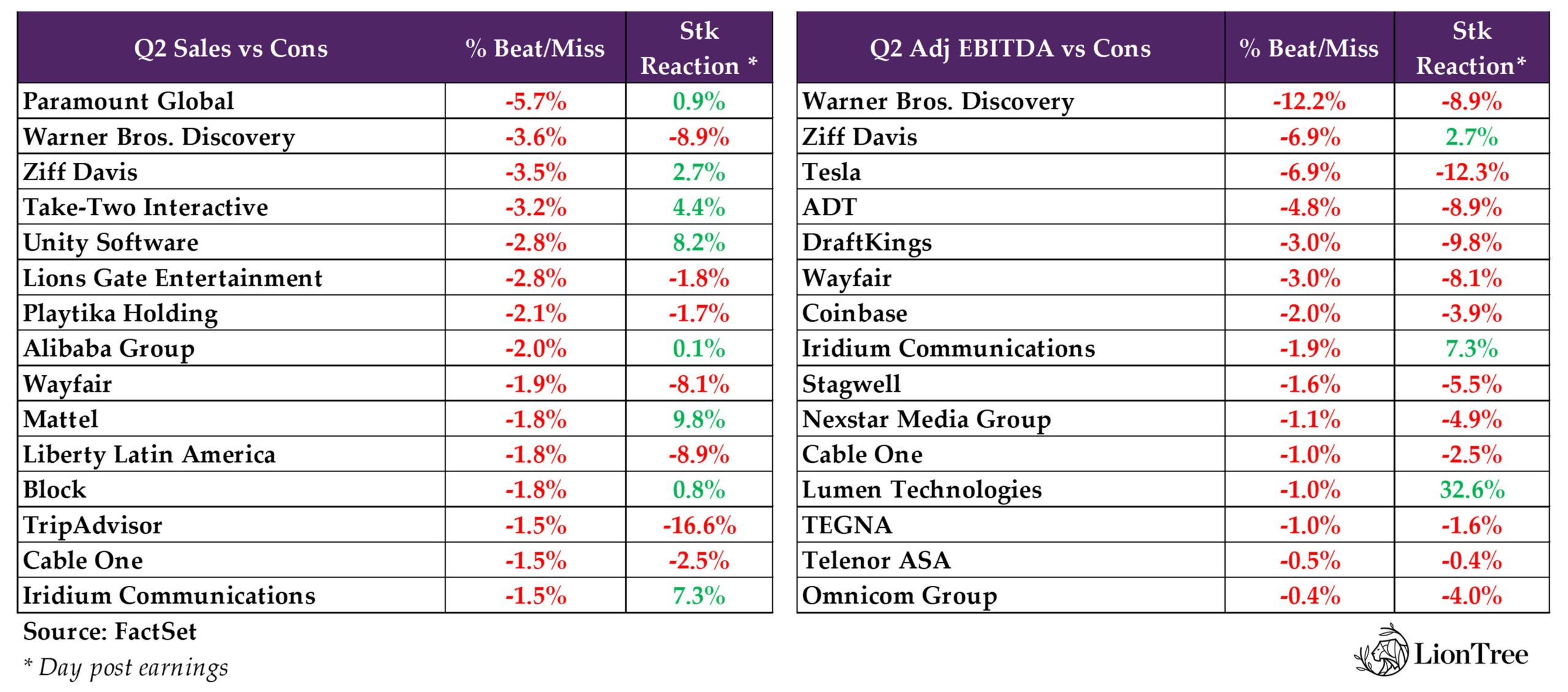

Of the Companies & Sub-Sectors That MISSED Expectations…

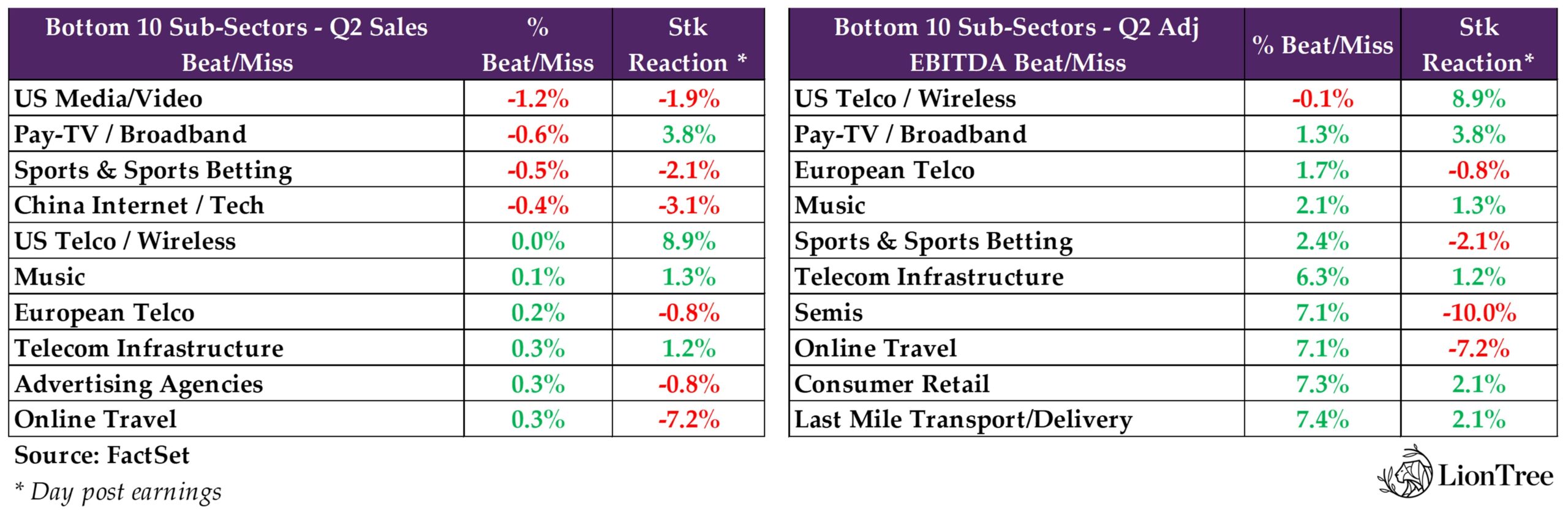

- Adj EBITDA – Of the companies in our LionTree Universe that report adj EBITDA, 18% reported numbers in-line/lower than consensus adj EBITDA

- US Telco/Wireless was the only sector that had a negative average adj EBITDA (coming in at -0.1%), which was mostly driven Lumen Technologies missing by -1.0%

- The Big 3 connectivity names were in-line with or beat expectations, with T-Mobile in-line, Verizon beating by +0.2%, and AT&T beating by +0.3%

- Pay-TV/Broadband had the smallest avg adj EBITDA beat of +1.3%, on average

- Cable One missed by -1.0%, while Comcast and Charter beat by +1.5% and +3.5%, respectively

- European Telco had the second smallest adj EBITDA beat versus expectations of +1.7%, in aggregate

- While Telenor ASA missed by -0.5%, Orange SA beat by +0.3%, as did Liberty Global by +1.1%, Telefonica SA by +1.6%, and SES SA by +5.9%

- US Telco/Wireless was the only sector that had a negative average adj EBITDA (coming in at -0.1%), which was mostly driven Lumen Technologies missing by -1.0%

- Sales – Overall, 30.0% of companies in our LionTree Universe reported sales in-line/lower than consensus

- US Media/Video stocks had the highest sales miss in our Universe, with the sector missing expectations by -1.2%, in aggregate

- The biggest misses came from Paramount, which missed by -5.7% ($6.81bn vs cons $7.22bn) and WBD, which missed by -3.6% ($9.71bn vs cons $10.07bn)

- Lions Gate Entertainment and Fox also missed by -2.8% and -0.3%, respectively

- That being said, Netflix, The Walt Disney Co., and Roku did beat by +0.3%, +0.3%, and +3.2%, respectively

- Pay-TV/Broadband took the second position in the Bottom 3 and missed expectations by -0.6%, in aggregate

- While Cable One and Comcast missed by -1.5% and -1.0%, respectively, Charter beat by +0.7%

- Sports & Sports Betting stocks missed expectations by -0.5%, on average

- Liberty Formula One and DraftKings missed by -1.2% and -0.9%, respectively, while Penn Entertainment beat by +0.6%

- US Media/Video stocks had the highest sales miss in our Universe, with the sector missing expectations by -1.2%, in aggregate

The NFL Isn’t The Only Big Sports Game In Town…The Paris Olympics Hits Record Viewership

After an unusual Olympics event in 2021, when athletes were earning gold metals with largely empty venues and the pandemic in general created a cautious overtone (and not to mention a far, far away time zone in Tokyo), the excitement for and impact of this year’s Paris Olympics reached new levels. Comcast’s NBC posted record viewership and ad dollars associated with the event. Warner Bros Discovery (WBD) also saw strong viewership trends, and both companies talked about the positive impact this Olympics has had on helping to bring in new streaming subscribers, though specific details were limited. Whatever the numbers are, it will be incumbent upon the companies to find ways to keep those new streaming subscribers. Net-net, the Paris Olympics goes down as another successful large live event that was able to bring in eyeballs and engagement. These events are few and far between. See below for some of the stats that we thought were most interesting and impressive over the 17-day event (link /link/link/link).

- Total viewership across all linear and digital platforms

- NBCU total viewership hit a record:6mn avg viewers across NBCU platforms, an +82% increase from the Tokyo Games and was the most streamed Olympics of all time; The Co had a total of 5k+ hours of Olympics coverage and 3.2k live events over the course of the Games

- Telemundo: Spanish-language coverage saw a +26% increase in viewership compared to the Tokyo Games

- Men’s Basketball Final: US vs. France, avg’d 20.3mn viewers, the highest for a gold medal game since 1996

- WBD cumulative reach viewing the Olympics content across WBD’s platforms was more than 215mn in Europe – +23% more than Olympic Games Tokyo 2020 (+40mn)

- NBCU total viewership hit a record:6mn avg viewers across NBCU platforms, an +82% increase from the Tokyo Games and was the most streamed Olympics of all time; The Co had a total of 5k+ hours of Olympics coverage and 3.2k live events over the course of the Games

- Streaming stats

- NBCU:5bn minutes streamed, up +40% from all previous Summer and Winter Games combined

- Peacock and NBCU Digital Platforms drew avg 4.1mn daily streaming viewers during “Paris Prime” and prime time

- WBD: 7bn minutes streamed on Max

- NBCU:5bn minutes streamed, up +40% from all previous Summer and Winter Games combined

- Streaming subscriber adds?

- NBCU – no color on how many new signups the Olympics generated for its Peacock service: Recall that in Q2, NBCU lost -500k Peacock subs, falling to 33mn total (post the Super Bowl)

- WBD- “record” number of new paid streaming subscribers over the Games period: +77% more than Tokyo 2020; Saturday, July 27 was WBD’s biggest ever single day for new paid streaming subscribers in Europe

- “Significant subscriber growth across all major markets in Europe, particularly France, Italy, Poland, Sweden and the UK”

- Other key NBCU updates

- Benefitted from technological innovations: New tools like Peacock’s Discovery Multiview, Live Actions, and its generative AI-powered “Daily Olympic Recap” using sportscaster Al Michael’s voice — helped boost viewership

- Over 25% of viewers who watched Olympics content on Peacock used the platform’s Multiview feature

- NBC sees a “halo” effect given incr’d viewership across its network news broadcasts: “NBC Nightly News” avg’d 7.6mn viewers during the period, and the “Today” show avg’d 3.1mn

- Advertising: The Co has said that it expects to generate more than the $1.25bn in advertising it secured during the Tokyo Olympics, but no specific numbers were confirmed

- Almost $500mn came in from new sponsors to the Games

- Digital ad revenue “more than doubled” vs Tokyo

- The total # of advertisers “more than doubled” vs Tokyo and Rio Games combined

- Benefitted from technological innovations: New tools like Peacock’s Discovery Multiview, Live Actions, and its generative AI-powered “Daily Olympic Recap” using sportscaster Al Michael’s voice — helped boost viewership

- Social stats

- NBCU: Paris Olympics content registered a record55bn impressions across NBC Sports social channels – a +184% increase vs. the Tokyo Olympics and +53% above the Rio Olympics

- WBD: 4.5bn+ video views of WBD’s Olympics posts on social, almost +10x more than Tokyo 2020 and more than +4x greater than Olympic Winter Games Beijing 2022 and Tokyo 2020 combined

- TikTok and Instagram especially drove views

Investor Positioning… AT&T, Meta, & Liberty Global Are Hedge Fund “Hot Stocks”

This week, 13-F data (as of the end of Q2) was released, and as usual, we took a deep-dive into what stock ownership changes have occurred across the sector.

Starting off with the most prominent investor, Berkshire Hathaway took two new positions in Q2, which were Heico, an aerospace and electronics company, as well as Ulta Beauty (which saw its stock jump +11% in reaction). The fund increased its positions in Chubb by +4.3% and SiriusXM by +262.2% (after decreasing by -8.8% last qtr), and further increased its position in Occidental Petroleum by +2.9% (on top of +1.8% last qtr). It decreased its position in several long-time holdings, with the most notable being Apple, which saw its position cut by almost half (-49.3%). Despite the cut, Apple remains Berkshire’s top holding at 30%, but it is down from 49% of the portfolio at the end of 2023.

Other companies it cut positions in were Capital One by -21.3% and T-Mobile by -10.9%, as well as Chevron by -3.6% (after cutting by -2.5% last qtr). The fund also offloaded its positions in Paramount and Snowflake. Finally, it maintained positions in Ally Financial, Amazon, American Express, Atlanta Braves, Bank of America, Charter, Citi, Coca-Cola, Jeffries, Kraft Heinz, Kroger, Liberty Latin America, Liberty Media, Liberty SiriusXM, Liberty Formula One, Mastercard, Mitsubishi, Moody’s, Verisign, and Visa.

We also took a quick look at Michael Burry’s Scion Asset Management (as a reminder, Michael Burry famously predicted the 2008 financial crisis and was one of the main characters in the book and movie, The Big Short), which made headlines this week for cutting its overall equity portfolio in half in Q2 after selling out of its position in 11 stocks, including Advance Auto Parts, Block, Cigna Group, and Citi. On the China Tech side, it increased its positions in Alibaba and Baidu but decreased its position in JD.com (Alibaba has now overtaken JD.com as Scion’s top holding as of the end of Q2). The fund also decreased its position in The RealReal and took new positions in Olaplex and Shift4 Payments (which is now the firm’s second-largest holding). In total, the firm now holds positions in 10 stocks. (link)

Where are the top hedge funds investing, in aggregate? Each quarter, WhaleWisdom tracks the stocks that were most bought and sold during the quarter across 150 of the top hedge funds (link). It ranks the “hottest” stocks based on a formula that takes into account the number of buyers adding and initiating new positions vs sellers, the change in average ranking that the stock had in the portfolios, and the number of times the stock appears in the top 10 holdings of the portfolios. The biggest takeaways were:

- TMT made a bit of a comeback in Q2: 4 of the Top 10 were TMT stocks, which is up from 2 in Q1, in-line with Q4, but still down from 5 in Q3; 7 of the Top 10 stocks were newcomers (had not been previously ranked)

- What TMT stocks made up the Top 10? AT&T (#2), Meta (#4), Liberty Global (#5), and Extreme Networks (#9)

- Only 2 of the MAANG names made to the Top 100 list: Meta (#4) and Amazon (#64)

- Breakdown by sector: Energy Cos once again dominated, as 35 of the Top 100 companies were in the sector (though down from 40 in Q1); Information Technology was a the second most popular industry, with 14 of the Top 100 Cos in the sector (up from 9 in Q1), followed by 13 in Finance, 10 in Consumer Discretionary, and 7 in Healthcare to round out the Top 5

- Increases and decreases in popularity

- There were some notable gainers this quarter that were worth flagging (Q1:24 -> Q2:24)…

- AT&T (#150 -> #2)

- Meta (#101 -> #4)

- Liberty Global (Not ranked -> #5)

- Mastercard (Not ranked -> #7)

- Adobe Systems (#121 -> #13)

- Verizon (#148 -> #15)

- QUALCOMM (#109 -> #23)

- Advanced Micro Devices (#144 -> #49)

- FedEx (#157 -> #51)

- Expedia (#112 -> #63)

- Amazon (#100 -> #64)

- The Walt Disney Co. (#170 -> #67)

- Intel (#140 -> #70)

- Tesla (Not ranked -> #71)

- Walmart (Not ranked -> #74)

- Micron Technology (#17 -> #88)

- Oracle (#3 -> #89)

- NVIDIA (#45 -> #93)

- American Express (#74 -> #100)

- … As well as some losers

- Microsoft (#29 -> #38)

- Warner Bros. Discovery (#40 -> #47)

- PDD Holdings (#57 -> #59)

- Global Payments (#16 -> #87)

- There were some notable gainers this quarter that were worth flagging (Q1:24 -> Q2:24)…

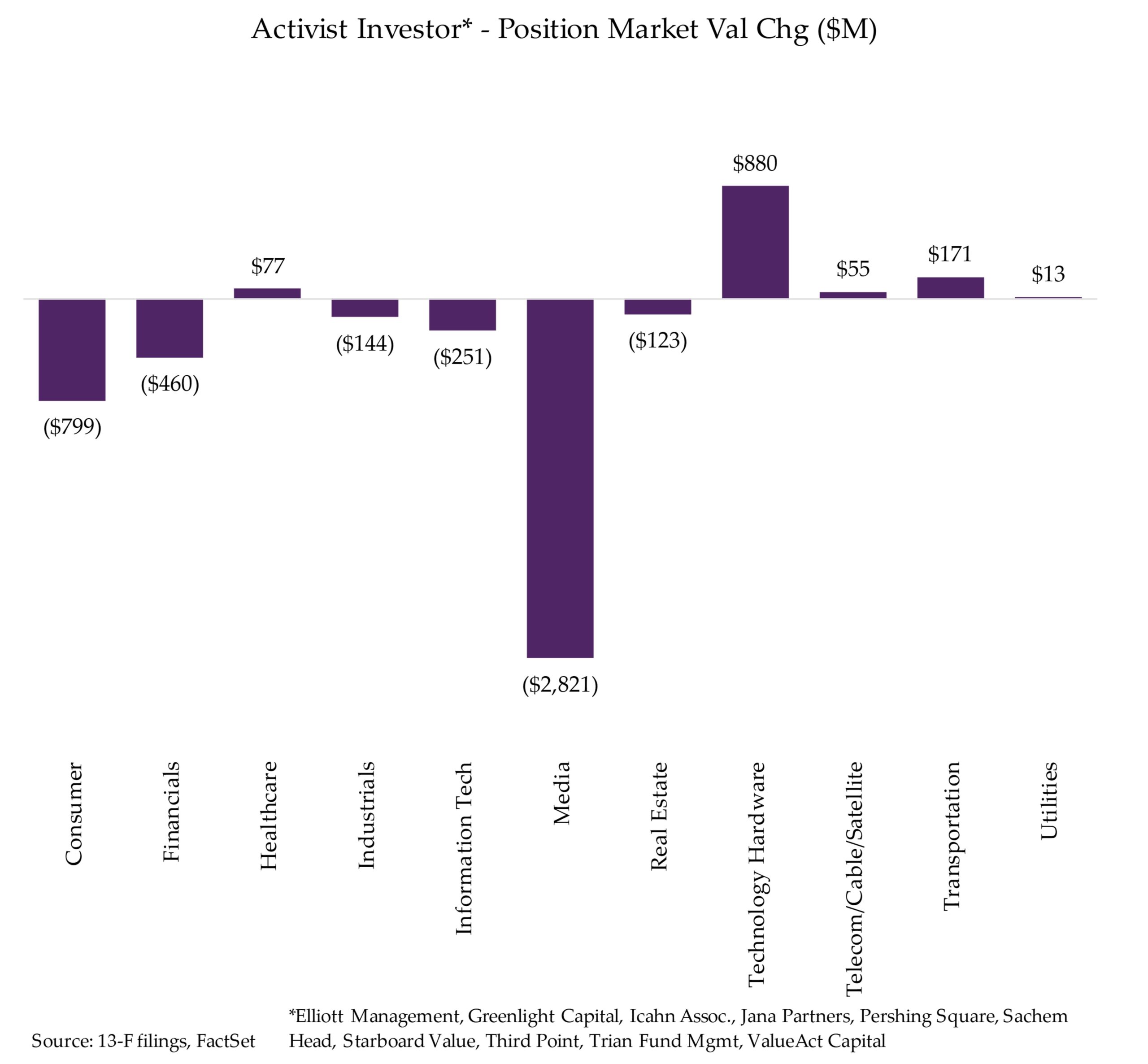

Where are activist/event investors placing their bets, in aggregate? For the fourth quarter in a row, the top 10 activist funds were net sellers, buying ~$1.2bn of stocks (vs $1.3bn last qtr) and selling ~$4.6bn (vs ~$2.4bn last qtr)

- Inflows: Technology Hardware stocks saw the most inflows (+$880mn), which was a reversal from last qtr, when the sector saw the second largest outflows (-$937mn); Transportation saw the second largest outflows (+$171mn), which was a slight step-up from last qtr (+$132mn); Healthcare (+$77mn), Telecom/Cable/Satellite (+$55mn) and Utilities (+$13mn) rounded out the five sectors that saw inflows Q2

- Technology Hardware inflows were dominated by Third Point, which took new positions in Apple (+$410mn) and Amphenol (+$186mn) and increased its position in Taiwan Semiconductor (+$148mn)

- Transportation inflows were almost entirely driven by Elliott Investment Management taking a new position in Southwest Airlines (~$172mn)

- Outflows: Media led the group in Q2 (-$2.8bn), which had seen inflows in the previous qtr (+$171mn); Consumer came in second place (-$799mn), followed by Financials (-$460mn), Information Tech (-$251mn), Industrials (-$144mn), and Real Estate (-$123mn) rounded out the sectors that saw outflows in Q2

- Media outflows were mostly driven by Trian Fund decreasing its position in The Walt Disney Co. (-$2.9bn)

Drilling Deeper Into Individual Activist Funds…

- ValueAct further increased its positions in Salesforce and Disney by +12.3% and +13.2%, respectively and maintained its position in Expedia and Roblox; The fund decreased its position in Flutter (after taking a new position last qtr), and further decreased its positions from last qtr in The New York Times, KKR, and Spotify; It also sold out of its position in Illumina

- Starboard Value took a new position in Match Group, increased its position in Alight (after initiating a position last qtr) and Salesforce (after decreasing its position over the last two qtrs), and further increased its position in News Corp; It maintained its position in Rogers Corp. and further decreased its position in GoDaddy by -28.2% (-14.5% last qtr), Humana by -48.1% (-1.8% last qtr), and Wix by -22.8% (-12.8% last qtr)

- Sachem Head took a new position in CVS and Liberty Global, increased its position in Seagate Technology by +17.0% and Sprinklr by +15.9%, and further increased its position in Nextracker by +20.7% (on top of +315.0% last qtr); It maintained its position in Twilio (after initiating last qtr) and Deliveroo, and sold out of its positions in Okta and Salesforce

- Trian Fund took a new position in U-Haul (the first position its initiated in two qtrs), further increased its position in Wendy’s, and maintained its position in Unilever; It decreased its position in Invesco by -19.8% and The Walt Disney Co. by -91.8%, and further decreased its position in Allstate by -10.0% (-19.9% last qtr) and Ferguson by -21.6% (-40.5% last qtr); The fund sold out of its position in Sysco

- Third Point initiated positions in Amphenol, Apple, Dynatrace, Live Nation, Micron Technology and Roper Technologies; It increased its positions in Cinemark, Taiwan Semiconductor, and Uber, and maintained its positions in Advanced Auto Parts, Amazon, AIG, Apollo Global Mgmt, UScellular, and Verizon; It decreased its positions in Alphabet, Bath & Body Works, Ferguson, Meta, Microsoft, and PG&E and sold out of its positions in SentinelOne, as well as Gartner, Goldman Sachs, and S&P Global (the latter three of which it took new positions in last qtr)

- Pershing Square initiated a position in Nike, and maintained its position in Howard Hughes Holding Corp., and Universal Music Group; It decreased its positions in Apple and Hilton, and further decreased its position in Chipotle by -22.5% (on top of -9.8% last qtr)

- Greenlight Capital maintained all of its positions (for the second qtr in a row), including GoPro, Invesco, Kenvue, and Kendryl; It did not take any new positions, nor did it increase, decrease, or sell out of any positions

- JANA Partners took a new position in Rapid7 and increased its position Wolfspeed (after taking a new position last qtr), and further increased its position in Trimble by +11.1%; It decreased its position in Frontier Communications by -1.5% (after increasing by +7.7% last qtr) and sold out of its position in Freshpet

- Elliott Management initiated new positions in Arm Holdings and Southwest Airlines, and further increased its positions from last qtr in Etsy, Liberty Broadband, and Match Group; It maintained its positions in Bausch Health, Cardinal Health, Crown Castle, Pinterest, and Vantage Towers and sold out of positions in NVIDIA (after taking a new position last qtr), as well as Endeavor and Polestar

China Tech Contends With Weakening Domestic Spending Trends

China Tech was under the microscope this week, as heavyweights Tencent, Alibaba, and JD.com all reported earnings as a bookend, of sorts, to a hectic earning season. Tencent led the group off by releasing headline numbers that beat on both the top- and bottom-line. However, the company’s somber tone regarding the “somewhat challenging economic environment” and weak domestic consumer spending trends spooked the market. For its part, Alibaba avoided directly addressing economic conditions in China on its call, and the company’s stock was relatively flat following a mixed print. JD.com was the outlier in the group in that it was the only stock to trade up, which was in reaction to much better-than-expected profitability (improvement in its supply chain), though “soft consumer spending” weighed on average order value and dragged on revenue growth.

See below for more of our key takeaways from Tencent, Alibaba, and JD.com’s latest prints.

Tencent’s Strong Print Reflected A Turnaround In The Video Game Biz

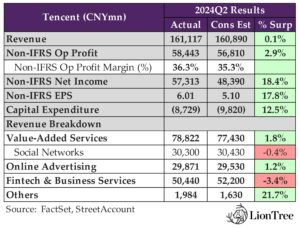

- Tencent’s headline numbers broadly outperformed expectations: Total rev was up +8.0% y/y in Q2 (vs +6.3% y/y in Q1) and beat cons by a slight +0.1%; Non-IFRS op profit grew +26.9% y/y (vs +30.2% y/y in Q1) and topped cons by + 2.9%; Non-IFRS net income beat cons by a wider +18.4%, and Non-IFRS EPS ended +17.8% above cons

- Value-Added Svs (~49% of total rev) – BEAT: Q2 VAS rev incr’d +6.2% y/y (vs -0.9% y/y in Q1) and closed +1.8% ahead of cons; Gross margin was up +3ppts y/y to 57% (flat w/ Q1); Social Networks and Domestic Games returned to positive growth, and International Games rev growth accel’d seq

- Social Networks (~38% of VAS rev) – MISS: Social Networks rev incr’d +2% y/y in Q2 (vs -2% y/y in Q1) but missed by a slight -0.4%; Growth in revs from music and long-form video subscriptions, Mini Games, and app-based virtual item sales, was partially offset by a decline in live streaming revs

- Online Advertising (~19% of total rev) – BEAT: Q2 Online Advertising rev grew +19.5% y/y (vs +26.4% y/y in Q1) and topped cons by +1.2%; Gross margin expanded +7ppts y/y to 56% (vs 57% in Q1); Saw incr’d ad spend from most categories, but slowing consumption in China was a headwind to eCPM pricing

- FinTech & Biz Svs (~31% of total rev) – MISS: FinTech & Biz Svs rev was up +3.7% y/y in Q2 (vs +7.4% y/y in Q1), missing cons by -3.4%; Gross margin rose +9ppts y/y to 48% (vs 46% in Q1); Slow consumer spending weighed on FinTech rev, while Business Svs rev growth was flat seq at a ~teens% y/y rate

- Value-Added Svs (~49% of total rev) – BEAT: Q2 VAS rev incr’d +6.2% y/y (vs -0.9% y/y in Q1) and closed +1.8% ahead of cons; Gross margin was up +3ppts y/y to 57% (flat w/ Q1); Social Networks and Domestic Games returned to positive growth, and International Games rev growth accel’d seq

- It’s a “somewhat challenging economic environment” in China right now: Highlighted that growth in consumption spending in China has been “kind of weak” and decelerating, w/ consumers becoming increasingly “budget-conscious”

- Macro volatility has impacted the Co’s gaming biz: This was evidenced by Tencent’s “pretty low spending per unit of time”

- BUT the Chinese gov’t has been “rolling out very proactive policies to encourage consumption”: Believes that “consumer sentiment as well as the economy will start turning… at some point in time” if these “policies can actually induce more confidence among the consumers”

- Domestic Games rev “resumed growth”, w/ contributions from a new evergreen title: Q2 Domestic Games rev was up +9% y/y in Q2 (vs -2% y/y in Q1), mainly driven by VALORANT, a new title, Dungeon & Fighter (DnF) Mobile, and other flagship games; Growth in gross receipts outpaced growth in rev during the qtr

- “DnF Mobile has emerged as one of the most successful mobile games in China”: The game has reactivated millions of DnF fans, and the Co believes it’s well-positioned for “long-term success” due to the higher user retention rates seen thus far

- Another new release, Need for Speed Mobile, is attracting millions of DAUs: The game was launched in July and provides a range of driving centric activities in an open-world experience

- Tencent also “revitalized” growth in its flagship titles: Honour of Kings and Peacekeeper Elite resumed generating positive y/y growth in gross receipts in Q2, w/ the latter increasing receipts by a double-digit percentage y/y

- Naruto Mobile also achieved a new milestone: Reached 10mn avg DAUs in May, as mkting activities have boosted user acquisition and enriched content has engaged existing players

- The Co is “seeking to build an audience from scratch” w/ future releases: These games will have “different characteristics” than Tencent’s other flagship franchises

- “DnF Mobile has emerged as one of the most successful mobile games in China”: The game has reactivated millions of DnF fans, and the Co believes it’s well-positioned for “long-term success” due to the higher user retention rates seen thus far

- International Games rev growth accel’d seq for second consecutive qtr: International Games rev rose +9% y/y in Q2 (vs +3% y/y in Q4 and +1% y/y in Q3), w/ growth in total gross receipts increasing “substantially faster” than rev during the qtr, driven by PUBG’s “robust performance” and contributions from Supercell games

- Title-specific call outs –

- PUBG Mobile saw double-digit y/y growth in DAU and gross receipts, driven by the new Mecha Fusion mode, the Golden Moon event, and a lion-themed top-tier outfit

- VALORANT’s MAUs grew y/y, “benefiting from high-quality content updates such as new agent, Clove, and [a] new map”; Two international esports events also helped expand the game’s “global IP influence”

- Supercell’s Brawl Stars posted a more than +10x y/y uptick in gross receipts and a “historical high” in avg DAUs, supported by frequent content updates and social features

- Supercell’s Squad Busters has established “critical mass” in key parts of North America and Western Europe, and SuperCell plans to continue adding new game modes and social features

- Title-specific call outs –

- Other highlights –

- Tencent is “generating increasing AI-related external rev from customers”: Along w/ customers utilizing the Co’s high-performance computing infrastructure for AI, Tencent also recently released three AI-powered platform solutions for enterprises and several consumer-facing product enhancements w/ AI

- Regarding potentially monetizing Mini Games on iOS via in-app transactions: The Co believes “it would be in our interests and Apple’s interests, but more so for the game devs and the users’ interests if that monetization were made available”; Wants deal terms that are “economically sustainable” and “fair”

-> Tencent Music also reported earnings this week w/ headline results that modestly surpassed cons expectations; Total rev was down -1.7% y/y but finished a slight +0.1% ahead of cons, and non-IFRS EPADS of CNY1.21 came in +3.4% above cons; Nonetheless, the Co’s Social Entertainment segment, which includes karaoke app WeSing, saw a -31.6% y/y drop in MAUs as well as a -45.8% y/y decline in ARPU; Tencent Music indicated this was “mainly the result of adjustments to certain live-streaming interactive functions and more stringent compliance procedures” that the Co started to implement in Q2:23, as well as “incr’d competition from other platforms”; But investors were concerned, and the stock sold off -15.3% in reaction, ending the week down -18.8%; YTD, Tencent Music shares are still trading up +16.9%

-> Tencent shares dropped -3.3% in reaction to earnings but still closed the week up +1.2%; YTD, Tencent stock is trading up +27.3%

Alibaba’s Main Focus Was On Revitalizing Growth In Its Core Domestic E-Comm & Cloud Segments

- Alibaba printed mixed results, as top-line missed while adj EBITDA comfortably beat estimates: Rev incr’d +3.9% y/y in FQ1 (vs +6.6% y/y in FQ4) and closed -2.0% below cons; Adj EBITDA was down -1.7% y/y (vs -4.1% y/y in FQ4) and beat cons by +7.1%; Adj EPS finished a wider +9.6% above cons

- Core Commerce (~76% of total rev) – MIXED: FQ1 Core Commerce rev rose +6.3% y/y (vs +14.1% y/y in FQ4) and fell -5.7% short of cons; Adj EBITA dropped -5.1% y/y (vs -8.0% y/y in FQ4) but topped cons by +4.8%; Saw a “positive trend” in “gradual mkt share stabilization” despite the top-line miss

- Cloud Intelligence (~11% of total rev) – BEAT: Cloud Intelligence rev grew +5.9% y/y in FQ1 (vs +3.4% y/y in FQ4) and beat cons by +1.8%; Adj EBITA rose +155.1% y/y (vs +45.1% y/y in FQ4) and topped cons by a wide +59.0%

- Digital Media & Entertainment (~2% of total rev) – BEAT: FQ1 Digital Media & Entertainment rev incr’d +3.7% y/y (vs -0.9% y/y in FQ4) and ended +0.4% ahead of cons; Adj EBITA of -CNY103mn in FQ1 (vs the prior yr qtr’s CNY63mn and FQ4’s -CNY884mn) was far better than cons’ -CNY394mn

- All Others (~19% of total rev) – Beat: All Others rev was up +2.7% y/y in FQ1 (vs -3.5% y/y in FQ4) and beat cons by +3.9%; Adj EBITA improved +27.1% y/y to losses of -, $1.26bn (vs -CNY2.82bn in FQ4) and was +48.1% better than cons

- Consolidation adjustments accounted for ~-9% of total rev: This was -9.9% worse than cons

- Taobao and Tmall Group (TTG)’s GMV growth decel’d seq: TTG posted ~+hsd% y/y GMV growth in FQ1, which was down from the “robust” double-digit y/y GMV growth seen in FQ4; Still, orders cont’d to grow at a double-digit rate, driven by “a notable increase in purchase frequency”

- Efforts to enhance the user experience has driven higher repeat rates: Highlighted that “various new products”, including live streaming and the RMB10bn subsidy program, “have resulted in a high user return to platform and high user repurchase rates”

- BUT overall take rate declined on a y/y basis: Primarily due to an increasing mix of GMV being generated by “new models” w/ lower monetization

- Alibaba has been proactively scaling down “certain direct sales bizs”: In turn, volumes from these channels has dropped “quite significantly”; Believes that “1P format probably is not a more efficient format” for certain categories

- Moving forward, the Co is focused on “advancing monetization efforts step-by-step”: This will underpin customer mgmt rev growth gradually aligning w/ GMV growth “over the coming qtrs”

- Cloud Intelligence – Public cloud rev maintained double-digit y/y growth seq: Driven by the execution of the Co’s “integrated Cloud plus AI development strategy”

- AI-related product rev sustained triple digit growth and incr’d its share of public cloud rev: More “major” customers have chosen Alibaba Cloud as their compute infrastructure for AI development, and the Co’s proprietary LLMs are “gaining wider adoption”

- The Co is not seeing any softening in enterprise demand from macro conditions: Instead, underscored that “any enterprise that is digitized… simply has to be investing in AI”

- Alibaba Cloud served as a major cloud svs provider for the Paris Olympics: Two-thirds of broadcasters used live signals transmitted by Alibaba Cloud in real-time around the world, reaching billions of viewers; Also saw the “first widespread application” of Alibaba Cloud’s AI tech

- Excluding subsidiaries, overall cloud rev growth is expected to return to double-digit growth in H2:F25: The Co also anticipates a “gradual acceleration thereafter”

- “Probably most of that growth will be driven by AI products”: Highlighted “very, very robust demand among [Alibaba’s] customers for AI and AI-relevant products” and believes that “demand is still far from being satisfied”

- AI-related product rev sustained triple digit growth and incr’d its share of public cloud rev: More “major” customers have chosen Alibaba Cloud as their compute infrastructure for AI development, and the Co’s proprietary LLMs are “gaining wider adoption”

- Alibaba International Digital Commerce (AIDC) saw a seq slowdown in top-line growth: FQ1 AIDC rev grew +32%% y/y (vs +45% y/y in FQ4) but still topped cons by +1.6%; AIDC adj EBITA losses were also +2.5% better than feared; Growth was mainly driven by the cross-border biz

- “AliExpress maintained rapid y/y order growth”: Flagged that the percentage of AE Choice orders remains high and “gradually stabilizing”; Also, efficiency improvements led to the unit economics of the Choice biz improving by nearly +20% seq

- The Co has also made progress in key mkts: In Türkiye, Trendyol incr’d monetization and profitability while enhancing its product offerings and mkting efficiency; In Southeast Asia, Lazada achieved single-month EBITDA profitability for the first time in July

- Cainiao posted a mixed performance relative to the Street’s estimates: Cainiao rev rose +16% y/y in FQ1 (vs +30% y/y in FQ4) and missed cons by -3.5%; In contrast, adj EBITA of CNY618mn was materially above cons’ CNY72mn; Benefited from “improved op efficiency” and synergies w/ AliExpress in the cross-border biz

-> Alibaba shares were ~flat in reaction to earnings and ended the week up +4.0%; YTD, Alibaba stock is trading up +7.3%

JD.com’s Wide Profitability Beat Overshadowed A Top-Line Miss Amid “Soft Consumer Spending”

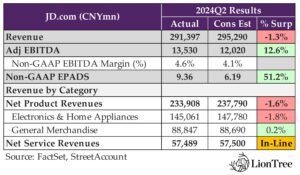

- JD.com’s headline results were mixed relative to consensus forecasts: Rev grew +1.2% y/y in Q2 (vs +7.0% y/y in Q1) and missed cons by -1.3%; But adj EBITDA was up +30.1% y/y (vs +17.5% y/y in Q1) and topped cons by +12.6%; Non-GAAP EPS finished a material +51.2% ahead of cons

- Net Product Revs (~80% of total rev) – MISS: Q2 Net Product Revs were ~flat y/y (vs +6.6% y/y in Q1) and fell -1.6% short of cons

- Electronics & Home Appliance rev missed cons by -1.8%: Rev was down -4.6% y/y in Q2 (vs +5.3% y/y in Q1); The y/y decline was driven by tough comps as well as the Co’s “disciplined strategy” regarding June 18 promos

- General Merchandise rev beat cons by +0.2%: Q2 rev incr’d +8.7% y/y (vs +8.6% y/y in Q1), ending a slight +0.2% above cons and marking the highest growth rate in the last two yrs; Highlighted strength in the supermkt category, specifically

- Net Service Revs (~20% of total rev) – IN-LINE: Net Service Revs rose +6.3% y/y in Q2 (vs +8.8% y/y in Q1) and finished on-par w/ cons estimates

- Net Product Revs (~80% of total rev) – MISS: Q2 Net Product Revs were ~flat y/y (vs +6.6% y/y in Q1) and fell -1.6% short of cons

- “Overall, China’s online retail for physical goods is outpacing the broader retail mkt”: Sees the “emergence of new online shipping formats continuing to drive incr’d online penetration and believes that China’s “vast and dynamic” e-commerce mkt can support multiple players w/ different biz models

- BUT “soft consumer spending” was a headwind during the qtr: In response, JD is focusing by focusing on “price competitiveness” and extended its best price guarantee to up to 365 days for certain categories as part of this strategy

- JD Retail rev decel’d seq due a “mixed category performance”: Q2 JD Retail rev grew +1.5% y/y in Q2 (vs +6.8% y/y in Q1); Despite the seq slowdown in rev growth, the Co’s number of our total qtrly active customers cont’d to grow at a double-digit y/y rate for the third straight qtr

- The Co’s user growth was “broad-based” across both new & existing users: The Co has seen “robust user momentum” in both higher and lower tier mkts; Also, highlighted contributions from users that have stayed w/ the Co for 2+ yrs as well as PLUS members

- JD’s user growth in younger and older cohorts has exceeded growth in its overall user base: Younger cohorts “grow up w/ online shopping” and are “highly accustomed and reliant to e-commerce platforms”, while older generations are increasingly embracing online shopping as well

- Overall shipping frequency and order volume grew by double-digits in Q2: This user momentum is a “strong proof” of the Co’s effective user experience initiatives, including enhancements to its shipping program

- However, avg order value declined y/y: Driven by the softness in consumer spending trends, JD’s low-price strategy, category mix shift, and a broadening of the Co’s free shipping svs

- The Co’s user growth was “broad-based” across both new & existing users: The Co has seen “robust user momentum” in both higher and lower tier mkts; Also, highlighted contributions from users that have stayed w/ the Co for 2+ yrs as well as PLUS members

- The supermkt category has seen double-digit growth for two consecutive qtrs: In Q2, growth in the supermkt category was led by strong order volume and improving user mindshare, and this momentum is expected to continue for the rest of the yr

- Efforts to enhance operational capabilities has resulted in “some healthy rev growth”: The Co still has “very strong confidence in the long-term potential of this category” and believes it will “serve as a key driver for the whole Co”, helping it expand mkt share

- JD Retail’s advertising rev from 3P merchants “bounced back” to double-digit y/y growth: Growth in ad revs also outpaced growth in GMV, as the Co further optimized traffic allocation efficiency; Sees “plenty of room” to further increase advertising rev as it continues to grow users and improve user efficiency

- JD Logistics rev also slowed seq: JD Logistics rev incr’d +7.7% y/y in Q2 (vs +15% y/y in Q1), w/ growth in internal and external revs up +7% and +8%, respectively (seq comps were unclear); Otherwise, commentary was sparse

- The Co’s non-GAAP net profit margin climbed to 5% for the first time: The nearly +2ppts y/y increase was driven primarily the expansion of its gross margin to a “historic level” of 15.8%, w/ improvements “in almost every category”; Supply chain improvements have enabled JD to “continually benefit from scale and efficiency”

- Looking ahead, JD’s mid- to long-term goal is to reach a ~hsd% net profit margin: Key growth drivers include the growth of its platform ecosystem, category mix optimization, and profit margin improvement across various categories

-> JD.com shares rose +4.3% in reaction to earnings, finishing the week up +13.2%; YTD, JD.com stock is trading up +1.4%

Grab-Bag: DraftKings Reverses Course On Surcharges/Another Suitor Reportedly Emerges For Paramount/Venu’s Launch Was Blocked By A Judge

- DraftKings opted not to proceed w/ a proposed gaming tax surcharge (link): This decision comes just two weeks after the Co’s initial announcement regarding its plan to apply the charge in states w/ 20%+ gaming taxes; The surcharge was set to go into effect beginning in 2025

- The Co pointed to customer feedback as the main reason for the reversal: “We always listen to our customers and after hearing their feedback we have decided not to move forward with the gaming tax surcharge”, per a statement from the Co

- BUT FanDuel going in a different direction also likely played a role: On Flutter’s earnings call this week, the Co said that FanDuel would not implement a surcharge and would instead offset the impact of high state taxes w/ more locally tailored mkting and promos

- Separately, Flutter’s Q2 was far better than expected: Rev grew +20% y/y, topping cons by +5.9%, and adj EBITDA rose +17% and beat cons by +13.5%; The Co outperformed estimates in every operating region; FanDuel had an “exceptional qtr”, w/ nearly 40% share of the US sports betting and iGaming mkt

- FY24 guidance was raised to reflect “strong momentum” heading into Q3: US rev is now expected to grow +3% to $6.2bn; US adj EBITDA is projected to increase +4% to $740mn; Ex-US, expects group rev and adj EBITDA gains of +2% to $8.0bn and $1.77bn, respectively

- The Co pointed to customer feedback as the main reason for the reversal: “We always listen to our customers and after hearing their feedback we have decided not to move forward with the gaming tax surcharge”, per a statement from the Co

- Edgar Bronfman Jr is reportedly close to making an offer for Paramount Global (link): Per sources, Bronfman is considering making an offer for National Amusements as well as an investment in Paramount itself, though details are still being worked out and it remains possible that no formal bid will be made

- Bronfman has held discussions about forming a group to back his bid: Including w/ Fortress Investment Group, Roku, and Hollywood producer Steven Paul

- Paramount shareholders will have the option to own more of the Co under Bronfman’s offer than under the Skydance deal: This is b/c Bronfman’s offer won’t include the dilution associated w/ the Skydance merger

- Any offer will still be subject to a counter-offer from Skydance: Notably, Skydance founder David Ellison, who is the son of Oracle co-founder Larry Ellison, has the right to counter any incoming bids

- Bronfman has yrs of experience in media: In 1995, Bronfman sought to diversify his family’s Seagram biz into media, acquiring MCA, which later became UMG and the world’s largest recorded music Co under his watch; In 2004, Bronfman led an investor group that bought Warner Music Group from Time Warner

- A judge blocked WBD, Fox, and Disney’s Venu sports streaming svs from launching later this month (link): US District Judge Margaret Garnett said that Venu Sports would “substantially lessen competition and restrain trade”; Fubo, another sports-focused streaming svs, sued the three Cos earlier this yr after the JV was annc’d

- Fubo’s lawyers argued that Venu is anticompetitive: Given that WBD, Fox, and Disney would force Fubo into paying for a broad bundle of general entertainment channels without the ability to handpick only the sports-centric channels that it wants to distribute

- Fubo CEO David Gandler – The ruling is a victory for the Co and consumers: The decision “will help ensure that consumers have access to a more competitive marketplace with multiple sports streaming options”

- However, Venu’s partners plan to appeal the decision: Per a joint statement from the Cos, “Venu Sports is a pro-competitive option that aims to enhance consumer choice by reaching a segment of viewers who currently are not served by existing subscription options”

- Fubo’s lawyers argued that Venu is anticompetitive: Given that WBD, Fox, and Disney would force Fubo into paying for a broad bundle of general entertainment channels without the ability to handpick only the sports-centric channels that it wants to distribute

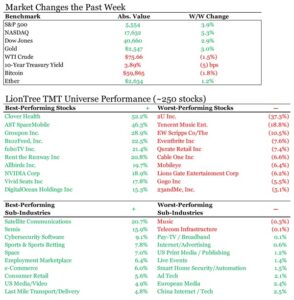

Stock Market Check

This Week's Other Curated News

Advertising/Ad Agencies/Ad Tech

- Dentsu revised its full-yr operating income forecast to 107.1bn yen, down from the previous forecast of 135.4bn yen, missing the estimate of 128.15bn yen. The co now expects net income of 36.7bn yen, a significant decrease from the 61.7bn yen it originally forecasted and below the estimate of 64.41bn yen. The dividend is forecasted to be 139.50 yen, slightly below the estimated 140.55 yen. (Smartkarma)

- Kamala Harris’ presidential campaign is launching a $90mn advertising effort over the next three weeks in Georgia and six other battleground states to introduce the Democrat to voters and sharpen the contrast w/ Republican Donald Trump. The media buy marks her campaign’s largest-yet investment in messaging to voters w/ just 2.5 months until Election Day in Nov. It comes on the heels of a $50mn worth of ads booked last month shortly after Harris replaced President Joe Biden at the top of the party’s ticket. (WABE)

- Meta’s planning to update its approach to ad campaign measurement and attribution, in order to better link user’s Meta ads to conversions, while also giving Meta more data points to work w/ to optimize campaigns. Coming in the second half of the yr, Meta’s annc’d a range of ad optimization and integration options, which could have a significant impact on performance measurement as part of its ongoing work to build AI-enabled automation solutions that allow any biz to grow. (Social Media Today)

- SAG-AFTRA struck a deal with AI startup Narrativ for audio voice replicas in digital advertising that the union asserts sets “a new standard” for ethical use of the tech and also makes it easy for performers to give consent and get paid. Narrativ’s new agreement w/ SAG-AFTRA promises to give the union’s 160,000 members the oppty to add themselves to a database that connects voice talent to advertisers. (Variety)

- The Justice Department is reportedly considering a push for a breakup of Google’s business after a federal judge ruled the co has an illegal monopoly over online search. DOJ attorneys could ask Judge Amit Mehta to order Google to sell portions of its business, with potential candidates for divestment including its Android operating system, Chrome web browser, and advertising platform AdWords, Bloomberg reported. (New York Post)

Artificial Intelligence/Machine Learning

- 8mn AI-capable PCs were shipped in Q2:24, according to the latest Canalys data. These devices are defined as desktops and notebooks that include a chipset or block for dedicated AI workloads, such as an NPU. Shipments of AI-capable PCs represented 14% of all PCs shipped in the quarter. (CANALYS)

- A group of visual artists can continue to pursue claims that Stability AI, Midjourney, DeviantArt and Runway AI’s artificial intelligence-based image generation systems infringe their copyrights. US District Judge William Orrick said the artists plausibly argued that the companies violate their rights by illegally storing their works on their systems. (XM – Global Broker in Forex and CFD Trading)

- A study by researchers from Cornell and other institutions found that all generative AI models, including OpenAI’s GPT-4o and Google’s Gemini, still produce hallucinations, with only about 35% of outputs being hallucination-free. Models vary in their accuracy based on the information sources they’ve been trained on, with some avoiding errors by refusing to answer difficult questions. Despite claims of improvement, hallucinations remain a persistent issue, suggesting the need for better fact-checking tools and human oversight during AI development. (TechCrunch)

- Alphabet said it was expanding its AI-generated summaries for search queries to six new countries, just two months after it rolled back some capabilities following a problem-riddled launch. The Co made AI Overviews, which are displayed atop a search results page before traditional links to the Web, available to all US users in May after spending one yr trialing a limited earlier version. (AsiaOne)

- Chinese courts have been handing down a series of judgments related to generative AI, indicating how Beijing views the technology and aims to take the lead in setting standards. In Apr, a Beijing court made China’s first ruling on a person’s right to their voice. A voice actor had sued several cos for AI-replicated voice infringement. The court found that some of the cos had indeed infringed on the plaintiff’s rights and ordered them to pay 250,000 yuan ($35,000) in damages. (Nikkei Asia)

- On August 7, the FCC voted unanimously to pass a new set of rules aimed at putting the brakes on AI-driven robocalls. AI-powered robocalls are the latest trick in the scammers’ playbook, and they’re getting more sophisticated by the day. FCC Chairwoman Jessica Rosenworcel is leading the charge to give consumers the upper hand. “Bad actors are already using AI technology in robocalls to mislead consumers and misinform the public,” she said. (Cord Cutters News)

- OpenAI annc’d an update on X stating: “there’s a new GPT-4o model out in ChatGPT since last week”. While the account did not provide further information immediately following that post, sources at OpenAI told that the new model was updated based on user feedback. Prior to the announcement, users noted that the underlying model powering ChatGPT, OpenAI’s GPT-4o, seemed to be behaving differently and better than in the recent past. (VentureBeat)

Audio/Music/Podcast

- Meta and Universal Music Group annc’d an “expanded global, multi-yr agreement. The deal will further evolve the creative and commercial oppties” for UMG artists and Universal Music Publishing Group songwriters across Meta’s network of platforms, including Facebook, Instagram, Messenger, Horizon, Threads, and, for the first time, WhatsApp. Terms of the deal were not disclosed. (Variety)

- Spotify will begin showing in-app pricing information for iPhone users in the European Union starting Aug 14, following a yearslong legal battle against Apple. In an update to an old blog post, Spotify says that EU iPhone users will now see things like promotional offers and pricing information for each subscription tier — including how much a plan costs once a promotion ends. (The Verge)

- Warner Music Group annc’d that its Board of Directors declared a regular quarterly cash dividend of $0.18 per share on WMG’s Class A Common Stock and Class B Common Stock. The dividend is payable on Sept. 4, 2024, to stockholders of record as of the close of biz on Aug. 27, 2024. (Yahoo Finance)

Broadcast/Cable Networks

- A+E Networks underwent a round of staff cuts. Every division of the Co, ncluding programming, mkting and public relations at outlets including Lifetime, A&E, and History, were impacted by the layoffs. Among those let go, Lifetime senior VP of unscripted development and programming Amy Savitsky has departed the Co. The layoffs come as part of an overall industry downsizing, particularly in the cable industry. (Yahoo News)

- TelevisaUnivision is adding to its sports portfolio. The Co inked a multi-yr deal with Major League Baseball, including multiple new windows of programming, as well as playoff games. TelevisaUnivision networks will begin broadcasting MLB games Aug 20, continuing through the postseason. The Co also has exclusive Spanish-language rights to the American League Division Series and American League Championship Series games. (The Hollywood Reporter)

- The CW Network and Gray Media said they renewed the affiliation agreements covering 38 of Gray’s local TV stations. The Gray stations reach ~12mn TV households, representing ~10% of the US. Financial terms were not disclosed. Last month, the CW’s owner Nexstar Media Group and Paramount Global reached an affiliation deal that gave the CW coverage in Detroit and Miami. (Broadcasting Cable)

Broader Connectivity

- Indian telecom conglomerate Bharti Global has acquired a 24.5% stake in BT Group from Altice UK. BT Group’s CEO, Allison Kirkby, welcomed the investment, calling it a significant vote of confidence in BT’s long-term value and strategy. She highlighted BT’s long-standing relationship with Bharti and expressed optimism about future collaboration. (ADVANCED-TELEVISION)

Broader Consumer Internet

- A slew of US federal agencies is working to make it easier for Americans to click the unsubscribe button for unwanted memberships and recurring payment services. A broad new government initiative, dubbed “Time Is Money,” includes a rollout of new regulations and the promise of more for industries spanning from healthcare and fitness memberships to media subscriptions. (Boston.com)

Broader Media & Entertainment

- Longtime YouTube and Google executive Adam Smith has been named Chief Product & Technology Officer, Disney Entertainment and ESPN. He takes the senior post after the exit in June of Aaron LaBerge, who is now CTO at PENN Entertainment, Disney’s partner on ESPNBet. The Smith hire was annc’d by Disney Entertainment Co-Chairmen Alan Bergman and Dana Walden and ESPN Chairman Jimmy Pitaro, to whom he will jointly report. (Deadline)

Cable/Pay-TV/Wireless

- China Unicom reports a robust first half of 2024 with a 2.9% increase in operating revenue to RMB197.3bn and an 11.3% rise in profit attributable to equity shareholders, reaching RMB13.8bn. CapEx decreased by 13.4% to RMB23.9bn, indicating efficient cost management. The co also annc’d a 22.2% yr/y increase in interim dividend to RMB0.2481 per share. (TipRanks Financial)

- During EchoStar’s Q2 earnings call last week, CFO Paul Orban acknowledged the co currently “[does] not have the necessary cash on hand” to fund Q4 operations or pay off the $1. 98bn in debt set to mature on Nov 15. As of June 30, the company had $521mn in cash and cash equivalents at the ready. EchoStar closed out the quarter w/ 8.07mn pay-TV subscribers, a head count that includes 6.08mn Dish TV customers, w/ Sling TV accounting for the remainder. (Sportico.com)

- Nielsen announced that starting in January, its local TV ratings will use a combination of big data from set-top boxes and smart TVs with traditional viewer panels as the new currency in all markets, eliminating the parallel transaction period. This change aims to address challenges in local viewership measurement due to fragmented audiences and small panel sizes. Nielsen’s panel-only data will remain for research, while its big data integration is under review by the Media Rating Council. (Broadcasting Cable)

- Rakuten Group and Macquarie Asset Management annc’d that Rakuten Mobile will raise between JPY150-300bn (~$1-2bn) in funds for the sale and leaseback of a portion of its mobile network assets w/ a consortium of global leading infrastructure investors, led by Macquarie Asset Management. Through this arrangement, Rakuten Mobile said it will continue to manage and operate these mobile network assets in Japan. (RCR Wireless News)

- Spectrum News has launched a local linear TV news network serving the St.Louis metropolitan area. Spectrum News St. Louis features local headlines at the top and bottom of every hour and hyperlocal weather forecasts every 10 minutes on the 1s. The news network is also available to Spectrum customers via the Spectrum News App for mobile, Xumo Stream Box, Roku and Apple TV, Spectrum said. (TVTechnology)

- US and Sweden are the latest to partner up, with the pair recently signing a technology and science cooperation agreement. “We intend to engage regularly and focus on cooperation in next generation communications, including 6G and beyond, as outlined in this vision for the mutual benefit of the US, the Kingdom of Sweden and the wider global community,” the US Department of State said in a statement. The move comes as governments, operators and vendors try to get a handle on how to manage the emergence of 6G early on. (Fierce Network)

Cloud/DataCenters/IT Infrastructure

- Wayra, Telefonica’s corporate venture capital arm, has invested in Nearby Computing, a computing orchestration and automation startup. The investment is part of a $7mn Series A financing round designed to drive Nearby Computing’s expansion plans and consolidate its market position. (THEFASTMODE)

Cybersecurity/Security

- Almost 2.7bn records of personal information for people in the US were leaked on a hacking forum, exposing names, social security numbers, all known physical addresses, and possible aliases. The data allegedly comes from National Public Data, a Co that collects and sells access to personal data for use in background checks, obtaining criminal records, and for private investigators. (BleepingComputer)

- California residents will soon be able to store their driver’s license or state ID in their Apple Wallet or Google Wallet apps, as the state’s govt annc’d that support for digital IDs is launching in the coming weeks. Californians w/ an ID in the Apple Wallet or Google Wallet app will be able to use their mobile devices to present their ID in person at select TSA security checkpoints and bizs. They can also use the app to verify their age or identity in select apps. (TechCrunch)

- The FBI said it seized the servers of a ransomware and extortion gang called Radar (aka Dispossessor). Radar’s website features a message from law enforcement, reading: “This website has been seized.” In a statement, the feds said they seized the gang’s domains and servers located in the United Kingdom and Germany. Radar/Dispossessor had at least 43 victim Cos since the gang started out in August 2023, the agency said. (TechCrunch)

eCommerce/Social Commerce/Retail

- Amazon has opened a £500mn state-of-the-art fulfilment centre in Leeds, part of the Co’s more than £1.5bn investment in West Yorkshire since 2010. The robotic facility at the city’s Gateway 45 logistics park uses advanced technology across three floors of Amazon Robotics to stow, pick and ship customer orders. The site is close to an Amazon delivery station and an Amazon Robotics sortation centre, and less than ten miles from the Wakefield fulfilment centre which began operations in Oct. 2022. (Retail Gazette)

- Home Depot topped quarterly expectations, but cautioned that sales will be weaker than expected in the back half of the yr as high interest rates and consumer uncertainty dampen demand. The co said that it now expects full-yr comparable sales to decline by 3% to 4% compared with the prior fiscal yr. It had previously expected comparable sales, a metric that takes out the impact of store openings and closures and other one-time factors, to decline about 1%. (CNBC)

- On Holding reported record net sales of 567.7mn Swiss francs in Q2, up 27.8% from the same period a yr ago. Q2 gross profit margin was 59.9%, which was up from 59.5% in the yr-ago period. Net income came in at 30.8mn Swiss francs, and adj diluted EPS increased to 0.14 Swiss francs from 0.04 Swiss francs a year ago. Adj EBITDA was 90.8mn Swiss francs. Over the last 12 months, On has achieved net sales of over 2bn Swiss francs. (Footwear News)

- Samsonite International’s board approved a dual listing in the US to enhance liquidity and global investor access. Samsonite, which is listed in Hong Kong, said that the US is the appropriate venue based on the Co’s “global footprint, growth drivers, and strategic priorities. Samsonite’s shares have dropped 18% in Hong Kong this yr, valuing the Co at HK$30.9bn ($4bn). (Bloomberg)

- The Federal Trade Commission’s crackdown on fabricated reviews and fake consumer and celebrity testimonials has produced new official federal regulations to prevent the use of these practices on websites and e-commerce hubs. The FTC approved the new rules against the buying and selling of fake reviews and product testimonials w/ a 5-0 vote on Aug 14. The rules will become effective in 60 days. (Engadget)

- The Summer Olympics proved to be a significant win for Nike, as the global event incr’d demand for the Co’s new product launches and helped it surpass competitors, per Similarweb. In the opening week of the Olympics, Nike and Puma managed to increase visits to their D2C sites, while Adidas, Hoka and On all saw their visits decline compared to the week before. (Apparel Resources)

- US CPI figures show overall food prices rose by 2.2% from Jun 2023 to Jun 2024. But food prices at restaurants rose by a lot more than food prices at grocery stores and supermarkets. Two key ingredients feed the demand for restaurant orders: convenience and habit. It’s hard to put a price on free time and relaxation, but it apparently beats the cost of cooking and washing the dishes. (Forbes)

- US retail sales accelerated in July by the most since early 2023 in a broad advance that points to a resilient consumer, even in the face of high prices and borrowing costs. The value of retail purchases, unadjusted for inflation, increased 1% in July and helped by a sharp snapback in car sales, Commerce Department data showed. Excluding autos and gasoline stations, sales were up 0.4%. (Bloomberg)

- Walmart CEO Doug McMillon reported that while many grocery prices have fallen, inflation remains stubborn in dry groceries and processed foods. Walmart is pressuring suppliers to reduce costs, but some are still pushing for increases. Walmart’s Q2 results showed revenue growth from higher unit sales, not price hikes. Despite steady or reduced prices on many items, costs for dairy, eggs, and meat continue to rise. Walmart’s strong performance sparked rallies in other retail stocks. The company emphasizes it’s lowering prices, with profits growing from higher-margin businesses, not retail price increases. (CNBC)

- Walmart raised its forecast for the yr, as qtrly rev grew nearly 5%, the Co’s stores and website drew more visits, and sales outside the grocery dept improved. Walmart said it now expects sales to rise by 3.75-4.75% for the full yr, and adjusted earnings to come in between $2.35-2.43 per share. Analysts also expected adjusted earnings of $2.43 per share for the yr — the top-end of Walmart’s guidance. (CNBC)

EV/ Autonomous Vehicles

- Chinese autonomous vehicle co WeRide has received the green light to test its driverless vehicles w/ passengers in California. The step comes as WeRide begins the process to go public on the US stock market at a nearly $5bn valuation. As of Aug. 2, WeRide holds two permits from the California Public Utilities Commission: A drivered pilot permit and a driverless pilot permit. The permits do not yet allow WeRide to charge passengers for rides, and the service isn’t available to the general public. (TechCrunch)

- Ford and TXU Energy have partnered up to provide customers free EV charging at home. Owners of newer Ford EVs and plug-in hybrids who sign up for TXU’s Free EV Miles program can get full credit back on their utility bill if they charge up during TXU’s free 18-hour window. The “first-of-its-kind” deal will incentivize customers to charge during off-peak hours. Free hours will be between 7:00PM and 1:00PM the next day. (The Verge)

- Ride-hailing and taxi drivers in China are facing threat of job loss from AI as thousands of robotaxis hit Chinese streets, economists and industry experts said. Self-driving technology remains experimental, but China has moved aggressively to green-light trials compared to the US. At least 19 Chinese cities are running robotaxi and robobus tests, disclosures showed. (Business Reporter)

- Rivian halted production of its electric delivery vans for Amazon due to a parts shortage, adding to its supply chain challenges. Over 1,000 vans are parked at its Illinois plant. Despite the halt, Rivian plans to make up for the lost production but hasn’t provided a timeline. Rivian has delivered over 15,000 vans to Amazon, with more in progress, and is exploring deals with other companies like DHL. (EV – EVerything about EVs.)

- Waymo plans to start testing its fully autonomous vehicles w/ no human safety driver on freeways in the San Francisco Bay Area. Its employees will be the first guinea pigs, and initial testing will start outside rush hour w/ “less than a handful” of vehicles. The move comes as Waymo, flush w/ an addt’l $5 bn investment from Alphabet, pushes to expand in San Francisco. (TechCrunch)

Film/Studio/Content/IP/Talent

- Paramount TV Studios, a production facility originally aimed at getting Paramount Pictures back into the biz of making TV series, will shut down, the latest bout of cost cutting by parent corporation Paramount Global, All current series and development projects made under the Paramount Television Studios umbrella will move to CBS Studios. (Variety)

FinTech/InsurTech/Payments

- Amazon teamed up w/ Barclays to launch a co-branded credit card that rewards users for their everyday spending. Amazon Barclaycard customers can earn 1% rewards on purchases made on the site and 0.5% rewards on all other spending for the first six months. Prime members can also benefit from an additional 2% back from Amazon spending during the Co’s designated shopping events. (Retail Gazette)

Handheld Devices & Accessories/Connected Home

- AT&T confirmed that it will not be offering Google’s newest Pixel Fold to its customers. AT&T sold last yr’s original Pixel Fold and still plans to sell much of the rest of Google’s new lineup, including the Pixel 9, 9 Pro, 9 Pro XL, and Pixel Watch 3. That said, other carriers including Verizon and T-Mobile, will be selling Google’s new foldable, which will go on sale on Sept 4 and start at $1,799. (CNET)

Last Mile Transportation/Delivery

- Grab shares slumped after the co reported quarterly rev growth that trailed estimates. The stock slid 5.5% at 9:58 a.m. in New York on Thursday (Aug. 15) after the co said rev rose 17% to $664mn in the three months through Jun. 2024, missing the $676.9mn analysts predicted on avg. Adjusted earnings before interest, taxes, depreciation and amortization were $64mn, roughly in line w/ expectations. (Yahoo Finance)

Macro Updates

- Inflation rose as expected in July, driven by higher housing-related costs, according to a Labor Department report Wednesday (Aug.14) that is likely to keep an interest rate cut on the table in September 2023. CPI increased 0.2% for the month, putting the 12-month inflation rate at 2.9%. Excluding food and energy, the core CPI came in at a 0.2% monthly increase and a 3.2% annual rate, meeting expectations. (CNBC)

- New Zealand’s central bank slashed its benchmark cash rate for the first time since March 2020, sending the kiwi dollar tumbling as policymakers flagged more cuts over the coming months, saying inflation was converging on its target of 1% to 3%. The decision to reduce rates by 25 basis points (0.25%) to 5.25% came almost a yr ahead of the Reserve Bank of New Zealand’s own projections. Rates are seen near 3.0% by the end of 2025, well below the RBNZ’s projection. (Reuters)

- The latest CPI data from the Office for National Statistics showed that food inflation remained unchanged at 1.5%, after falling for the previous 15 months after it hit a 45-yr high of 19.2% in Mar. 2023. Clothing and footwear inflation rose 2.1% in Jul. 2024, up from 1.6% the month before, while furniture and household goods further deflated 1.7% last month. The headline inflation figure, taking into account costs such as housing, transport, and energy, rose above the Bank of England’s 2% target to 2.2%. (Retail Gazette)

- The producer price index increased 0.1% in July 2024, less than 0.2% forecast, opening the door further for the Federal Reserve to start lowering interest rates. Economists surveyed by Dow Jones had been looking for an increase of 0.2% on both the all-items and the core readings. A further core measure that also excludes trade services showed a rise of 0.3%. On a yr-over-yrbasis, the headline PPI increased 2.2%, a sharp drop from the 2.7% reading in Jun. (CNBC)

Satellite/Space

- AT&T and Verizon are urging telecom regulators to reject a key part of SpaceX’s plan to offer cellular svs w/ T-Mobile, claiming the satellite system will interfere w/ and degrade svs for terrestrial mobile broadband networks. Filings urging the Federal Communications Commission to deny SpaceX’s request for a waiver were submitted by AT&T and Verizon this week. As part of that plan, SpaceX is seeking a waiver of FCC rules regarding out-of-band emission limits. (Ars Technica)

- During a panel at the Mountain Connect show, the CEO of the Fiber Broadband Association criticized SpaceX’s Starlink for seeking BEAD funds, arguing it’s “absurd” to use federal funds for LEO satellite broadband. The Wireless Internet Service Providers Association countered that BEAD funding won’t cover fiber everywhere, advocating for alternative technologies like fixed wireless. The NTIA will ultimately decide on the eligible technologies. (Fierce Network)

- EQT annc’d that the EQT Infrastructure VI fund entered into exclusive negotiations to acquire a majority stake in Eutelsat Group’s Ground Station Infrastructure Business. EQT would own 80% of the capital, while Eutelsat Group would remain committed as long-term shareholder, anchor tenant, and partner of the new Co w/ a 20% holding. The contemplated transaction values the new entity at an enterprise value of EUR790mn. (THEFASTMODE)

- SpaceX violated environmental regulations by repeatedly releasing pollutants into or near bodies of water in Texas, a state agency said in a notice of violation focused on the Co’s water deluge system at its Starbase launch facility. The notice from the Texas Commission on Environmental Quality came five months after the EPA Region 6 office informed SpaceX that it violated the Clean Water Act w/ the same type of activity. (CNBC)

- SpaceX will fly the first-ever human spaceflight over the Earth’s poles, possibly before the end of this yr. The private Crew Dragon mission will be led by a Chinese-born cryptocurrency entrepreneur named Chun Wang, who will be joined by a polar explorer, a roboticist, and a filmmaker. The mission will launch into a polar corridor from SpaceX’s launch facilities in Florida and fly directly over the north and south poles. (Ars Technica)

- The Telecommunications Regulatory Commission of Sri Lanka has issued a license to Starlink to provide the country with satellite broadband services. Starlink had approached Sri Lanka in Mar. with a proposal to set up operations. This development was made possible by a new telecommunications bill passed by the country’s parliament last month. The bill, which amended the law for the first time in 28 yrs, will “create a more competitive and fair market in the telecommunications sector,” according to the Parliament’s website. (RCR Wireless News)

Social/Digital Media

- Buzzfeed reported total revenue of $47mn for the Q2, down from $62mn a yr ago. Advertising rev declined 19% y/y to reach $23.8mn, w/ programmatic advertising rev at $16mn compared to $15.5mn a yr ago. Content rev plunged 48% to $11.4mn. The co’s net loss is improving, w/ the media conglomerate reporting a loss of $6mn compared to a loss of $22mn a yr ago. (The Hollywood Reporter)

- Elon Musk’s interview of Donald Trump on X was nearly derailed by technical glitches in the first minutes of the scheduled start time. Users trying to log on to the event reported that they could not join X’s livestream platform. Musk blamed a cyberattack, saying “There appears to be a massive DDOS attack on.” After nearly an hour of troubleshooting, the conversation started in earnest and went another two hours. (CNBC)

- TikTok annc’d that it’s adding group chats to its platform. Users can now create group chats w/ up to 32 people to chat and share content together. As w/ individual messages, group chats are only available to users above the age of 15. TikTok says it has added safety measures to protect teens between the ages of 16 and 17. Everyone, including teens, can only be added to a group chat by a mutual follower. (TechCrunch)

Software

- Apple threatened to remove creator platform Patreon from the App Store if creators use unsupported third-party billing options or disable transactions on iOS instead of using Apple’s own in-app purchasing system for Patreon’s subscriptions. In a blog post and email to Patreon creators, the Co says it’s begun a 16-month-long migration process to move all creators to Apple’s iOS in-app purchase system by Nov 2025. (TechCrunch)

- India’s antitrust body recalled two reports that detailed alleged breaches of competition law by Apple, which complained that the regulator had disclosed commercial secrets to competitors. The move will prolong an already delayed investigation, which began in 2021, centering on Apple’s alleged abuse of its dominant position in the apps mkt to force devs to use its proprietary in-app purchase system, at a fee of up to 30%. (Yahoo Finance)

Sports/Sports Betting

- BBC Sport’s coverage of the Paris 2024 Olympic Games was streamed a record-breaking 218mn times online. This more than doubled the Tokyo Olympic Games total of 104mn, w/ 12.2mn people signed in to BBC iPlayer accounts to watch coverage. BBC One enjoyed consistently high viewing figures throughout the duration of the competition w/ a Total TV reach (15+ mins) of 36.1mn watching Paris 2024 on BBC TV. (ADVANCED-TELEVISION)

- DraftKings will not move forward w/ the proposed gaming tax surcharge, a decision that comes just two weeks after initially planning to implement the charge in high-tax states. The Co shared its reversal through a statement, citing customer feedback as the primary reason for the change in direction, though competitor FanDuel also stated that it wouldn’t implement a similar surcharge. (GAMBLINGINSIDER)

- Flutter Entertainment shares soared as much as 11% in extended trading after the co, the operator of the FanDuel online sportsbook, reported Q2 sales and profit that beat analysts’ expectations. Flutter, which recently moved its stock listing to the New York Stock Exchange from London, generated revenue of $3.61bn in the quarter, exceeding estimates of $3.37bn. Flutter said it didn’t plan to match rival DraftKings in introducing a player surcharge in high-tax states. (Yahoo Finance)

- Football continues to dominate the payments sector in 2024, w/ 140 deals totaling $371.6mn (€340.2mm) annually. Mastercard’s $195mn sponsorship of the UEFA Champions League highlights the game’s commercial value. UEFA’s substantial annual expenditure, followed by FIFA and other major leagues, reinforces the sport’s global appeal. Visa also makes a strong impact w/ high-profile partnerships. (ADVANCED-TELEVISION)

- Fresh off their decision to exit Bally Sports for a local broadcast TV deal w/ Scripps Sports back in June, the NHL’s defending Stanley Cup champion, the Florida Panthers, have to take their games direct-to-consumer. Scripps Sports will broadcast Panthers games on local stations WSFL (channel 39), WHDT (9) and a to-be-annc’d Fort Myers station. And ViewLift will create an app-based subscription DTC platform for fans to stream Panthers games, just as it has for the NHL’s Vegas Golden Knights and Washington Capitals. (NextTV)

- LeBron James, Steph Curry, and Kevin Durant leading the US men’s basketball team over France in the final game at the Paris Summer Olympics brought NBC and Peacock the biggest ratings for a gold medal game since 1996. The gold medal game averaged 19.5mn viewers on Saturday (Aug 10) afternoon, and its tight finish peaked at 22.7mn, per total audience stats from Nielsen and Adobe Analytics. (Broadcasting Cable)

- NBCUniversal said primetime Olympics coverage on both Paris time (2 pm to 5 pm ET) and US time (8 pm to 11 pm) averaged a Total Audience Delivery of 30.6mn viewers across all platforms, up 82% from the pandemic-delayed Tokyo Summer Olympics in 2021. Led by Peacock, NBCU streamed 23.5bn minutes of Olympic programming, up 40% from all previous summer and winter games combined. In primetime, Peacock averaged 4.1mn viewers daily. (Broadcasting Cable)

- The Dallas Cowboys, despite not winning a Super Bowl since 1996, are valued at $10.32bn, making them the first sports franchise to surpass $10bn. This places them atop Sportico’s list of NFL team valuations, followed by the Los Angeles Rams ($7.79bn) and New York Giants ($7.65bn). Collectively, the 32 NFL franchises are worth $190bn. (ESPN.com)

- The Tampa Bay Buccaneers recently reportedly turned down a proposal to buy the franchise for a tick above the $6.05bn that a group led by Josh Harris paid for the Washington Commanders last yr. If accepted, it would have set a record for the transaction of an NFL team and a global record for a control sale of a sports team.” It was noted that the interest came from someone deemed a “qualified buyer”. (The Pewter Plank)

Tech Hardware

- A recent SEC filing shows that Intel sold its stake in Arm Holdings in Q2. The news comes amid the massive job cuts taking place at the co, signaling a larger shakeup w/in the co as it struggles to keep pace w/ competitors like AMD and Qualcomm in the current semiconductor climate. Intel may be also awarded up to $11bn in loans and will be able to claim federal tax credits that could cover as much as 25% of the expense of its US expansion projects. (RCR Wireless News)

- Apple, seeking new sources of rev, is moving forward w/ the development of a pricey tabletop home device that combines an iPad-like display w/ a robotic limb. The Co now has a team of several hundred people working on the device, which uses a thin robotic arm to move around a large screen. The product, which relies on actuators to tilt the display up and down and make it spin 360 degrees, will offer a twist on home products like Amazon.com’s Echo Show 10 and Meta Platforms’ discontinued Portal. (The Straits Times)

- Cisco is cutting thousands of jobs in a second round of layoffs as it shifts focus to growing biz segments like cybersecurity and AI. Early reports indicate the number of affected employees will be similar to the 4,000 cut in Feb, if not slightly higher. Disappointing mkt demand and supply-chain constraints in Cisco’s main biz, routers and switches, is being blamed for the cuts and the heightened focus on AI. (RCR Wireless News)